Kids Wear Market Size

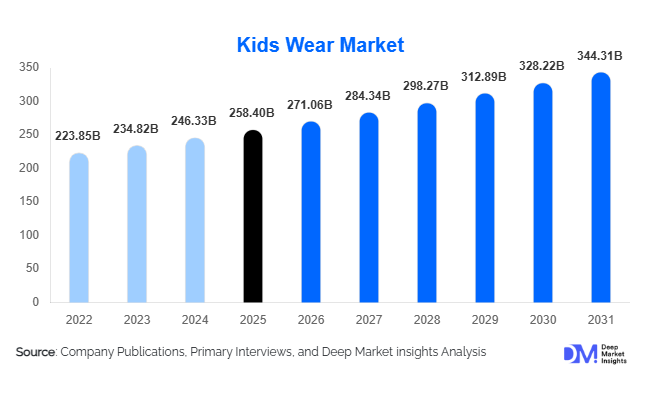

According to Deep Market Insights, the global kids wear market size was valued at USD 258.4 billion in 2025 and is projected to grow from USD 271.06 billion in 2026 to reach USD 343.7 billion by 2031, expanding at a CAGR of 4.9% during the forecast period (2026–2031). The kids wear market growth is primarily driven by rising disposable incomes, increasing fashion awareness among parents, rapid expansion of e-commerce channels, and growing demand for premium and sustainable children's apparel. Frequent replacement cycles due to children's growth, coupled with higher spending on branded clothing, continue to provide stable demand across developed and emerging economies.

Key Market Insights

- Apparel remains the dominant product category, accounting for nearly 68% of global kids wear revenue due to recurring purchases of casualwear, schoolwear, and seasonal clothing.

- Asia-Pacific dominates the global market, supported by large child populations, increasing urbanization, and expanding middle-class spending in China, India, and Southeast Asia.

- Sustainable and organic kids' clothing is witnessing accelerated adoption, particularly across North America and Europe, driven by environmentally conscious parents.

- Online retail channels continue to gain market share, supported by digital-first brands, AI-powered sizing tools, and convenient home delivery services.

- Premium and fashion-forward children's apparel is expanding rapidly, fueled by social media influence and increasing consumer preference for branded products.

- Technological innovation in textiles and supply chains, including smart fabrics, inventory automation, and digital merchandising, is transforming the competitive landscape.

Kids Wear Market Trends

Sustainability Becoming a Core Purchasing Factor

Parents are increasingly prioritizing environmentally responsible apparel for children. Demand for organic cotton, recycled polyester, biodegradable fabrics, and ethically manufactured garments has expanded significantly over the past few years. Global apparel brands are responding by introducing sustainable collections specifically designed for infants, toddlers, and school-age children. Regulatory pressure across Europe and growing consumer awareness regarding environmental impact have accelerated investment in sustainable sourcing and circular fashion initiatives. Several manufacturers are also introducing take-back programs, recycled packaging, and carbon-neutral production practices to strengthen their sustainability credentials.

Rise of Digital-First and Omnichannel Retail Models

The rapid growth of e-commerce continues to reshape the kids wear industry. Parents increasingly prefer online shopping due to convenience, wider product selections, price transparency, and personalized recommendations. Artificial intelligence-powered sizing solutions, virtual fitting tools, and mobile shopping applications are improving customer experience and reducing return rates. Brands are simultaneously investing in omnichannel strategies that integrate physical stores with digital platforms, enabling seamless shopping experiences. Social commerce, influencer marketing, and direct-to-consumer sales channels are emerging as critical growth drivers, particularly among younger millennial and Gen Z parents.

Kids Wear Market Drivers

Growing Disposable Income and Urban Middle-Class Expansion

Rising household incomes across developing economies are significantly contributing to higher expenditure on children's apparel. Emerging markets such as India, China, Indonesia, Vietnam, Brazil, and Mexico are witnessing increasing consumer spending on branded and premium kids wear products. Urban families are allocating larger portions of their budgets toward quality clothing, fashion-oriented products, and lifestyle-driven purchases. The growth of dual-income households has further strengthened purchasing power, enabling frequent wardrobe replacement and premium brand adoption.

Increasing Fashion Consciousness Among Parents

Children's apparel has evolved from a necessity-driven category into a fashion-focused segment. Parents are increasingly influenced by celebrity culture, social media trends, and digital marketing campaigns when purchasing clothing for children. Fashion brands are launching seasonal collections, limited-edition products, and designer collaborations targeted specifically at younger consumers. This shift has increased purchase frequency and encouraged consumers to spend on occasion wear, activewear, and premium casual apparel.

Kids Wear Market Restraints

Volatility in Raw Material and Manufacturing Costs

The industry remains highly exposed to fluctuations in cotton prices, synthetic fiber costs, labor expenses, and transportation charges. Rising input costs can negatively impact manufacturer profitability and create pricing challenges, particularly in highly competitive markets where consumers remain price-sensitive. Supply chain disruptions and inflationary pressures have further increased operational uncertainty for apparel manufacturers.

Intense Competitive Pressure and Market Fragmentation

The kids wear industry is characterized by the presence of global brands, regional manufacturers, fast-fashion retailers, private-label offerings, and digital-native entrants. Intense competition places pressure on pricing, marketing expenditures, and inventory management. Maintaining product differentiation while preserving profitability remains a major challenge for market participants, particularly within the mid-market and value segments.

Kids Wear Market Opportunities

Expansion of Sustainable and Organic Apparel Categories

Sustainable children's apparel represents one of the most attractive opportunities within the global kids wear market. Parents are increasingly willing to pay premium prices for products manufactured using organic cotton, recycled materials, and environmentally responsible production methods. Brands that successfully integrate sustainability throughout their value chains can strengthen customer loyalty, command higher margins, and differentiate themselves in an increasingly crowded marketplace. Growing regulatory support for sustainable textiles further enhances the long-term growth potential of this segment.

Direct-to-Consumer and Subscription-Based Business Models

Direct-to-consumer (DTC) strategies are enabling brands to improve customer engagement while reducing dependence on traditional retail channels. Subscription-based clothing services tailored to children's rapid growth cycles are also gaining popularity. These models provide convenience for parents while generating recurring revenue streams for brands. Enhanced consumer data collection and personalized product recommendations further support long-term customer retention and profitability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 258.4 Billion |

| Market Size in 2026 | USD 271.06 Billion |

| Market Size in 2031 | USD 344.31 Billion |

| CAGR | 4.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Apparel dominates the global kids wear market, accounting for approximately 67.8% of total revenue in 2025. Casualwear, school uniforms, sportswear, and seasonal clothing collectively drive the segment's leadership position due to frequent replacement needs associated with children's growth. Sportswear and activewear represent some of the fastest-growing apparel categories as participation in youth sports and recreational activities increases globally. Footwear remains an important secondary segment, supported by demand for school shoes, athletic footwear, and casual styles. Accessories such as backpacks, socks, hats, and fashion accessories continue to gain traction as brands expand lifestyle-oriented product portfolios.

Age Group Insights

Children aged 5–12 years represent the largest age-group segment, accounting for approximately 36.2% of global market demand. This category benefits from multiple apparel requirements, including school uniforms, sportswear, casual clothing, and occasion wear. Preschool children and toddlers continue to generate significant recurring demand due to rapid growth rates and frequent clothing replacement. Meanwhile, the teenage segment is emerging as one of the fastest-growing categories, supported by rising fashion consciousness, social media influence, and increasing preference for branded apparel among young consumers.

Gender Insights

Boys' apparel remains the largest gender-based segment, representing approximately 38.4% of global revenue. Demand is supported by strong sales of activewear, schoolwear, and casual clothing categories. Girls' apparel closely follows, benefiting from greater product diversity and fashion-oriented purchases. The unisex category is experiencing rapid growth as brands respond to evolving consumer preferences and increasing acceptance of gender-neutral clothing collections. Sustainability-driven purchasing decisions are also encouraging demand for versatile and long-lasting unisex apparel products.

Distribution Channel Insights

Offline retail channels continue to account for the majority of global sales, representing approximately 61.4% of market revenue. Parents frequently prefer physical stores to assess product quality, fabric comfort, and fit before purchasing. Specialty children's stores and brand-owned outlets remain particularly influential within premium categories. However, online retail channels are expanding at a significantly faster pace, supported by growing internet penetration, mobile commerce adoption, and enhanced digital shopping experiences. Marketplace platforms, brand websites, and social commerce channels are becoming increasingly important for customer acquisition and retention.

Price Positioning Insights

The mid-market segment accounts for nearly 48.7% of global kids wear sales and remains the largest pricing category worldwide. Parents typically seek a balance between affordability, durability, and quality, making mid-priced apparel highly attractive across most regions. Premium and luxury segments are witnessing above-average growth due to increasing disposable incomes and demand for branded products. Economy-priced apparel continues to dominate demand in developing economies where affordability remains a key purchasing criterion.

Explore more data points, trends and opportunities Download Free Sample Report

Kids Wear Market Segmentations

By Product Type

- Apparel

- Footwear

- Accessories

By Age Group

- Infants (0–12 Months)

- Toddlers (1–3 Years)

- Preschool (3–5 Years)

- Children (5–12 Years)

- Teenagers (13–16 Years)

By Gender

- Boys

- Girls

- Unisex

By Price Range

- Economy / Value Segment

- Mid-Market Segment

- Premium Segment

- Luxury Segment

By Distribution Channel

- Offline Retail

- Online Retail

- By Material Type

- Cotton-Based Apparel

- Synthetic Fibers

- Organic Cotton

- Wool-Based Clothing

- Blended Fabrics

- Sustainable/Recycled Materials

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 41.8% of the global kids wear market and remains the largest regional market. China represents the largest individual country market globally, supported by urbanization, rising household incomes, and premiumization trends. India is emerging as one of the fastest-growing markets due to favorable demographics, increasing middle-class consumption, and expanding e-commerce penetration. Southeast Asian countries including Indonesia, Vietnam, Thailand, and the Philippines are also contributing significantly to regional growth through rising apparel spending and population expansion.

North America

North America accounts for approximately 24.5% of global market revenue. The United States remains the dominant market within the region, supported by high per-child apparel spending, strong brand penetration, and growing demand for sustainable products. Premium clothing, organic apparel, and direct-to-consumer brands continue to gain traction among affluent consumers. Canada contributes additional growth through rising online retail adoption and increasing interest in environmentally responsible apparel.

Europe

Europe remains a mature but highly attractive market characterized by strong demand for premium children's apparel and sustainable products. Germany, the United Kingdom, France, Italy, and Spain represent the largest national markets. Strict environmental regulations and growing consumer awareness are accelerating demand for organic fabrics, ethical sourcing, and circular fashion initiatives. Premium fashion brands continue to expand children's collections throughout the region.

Latin America

Brazil represents the largest market in Latin America, followed by Mexico and Argentina. Rising urbanization, increasing disposable income, and growing digital retail penetration are supporting regional growth. International apparel brands are strengthening their presence across major metropolitan markets while local manufacturers continue to compete through value-oriented offerings.

Middle East & Africa

The Middle East and Africa region continues to demonstrate strong growth potential, particularly across the Gulf Cooperation Council countries. Saudi Arabia and the UAE account for the largest share of regional demand, supported by high disposable incomes and strong preference for premium international brands. South Africa remains the largest African market, while growing urban populations across Kenya, Nigeria, and Egypt are creating new opportunities for apparel manufacturers and retailers.

Key Players in the Kids Wear Market

- Carter's Inc.

- The Children's Place

- H&M

- Zara

- Gap Inc.

- Nike Inc.

- Adidas AG

- Benetton Group

- Mothercare plc

- VF Corporation

- Cotton On Group

- Levi Strauss & Co.

- Next plc

- Primark

- Uniqlo