Kids Snacks Market Size

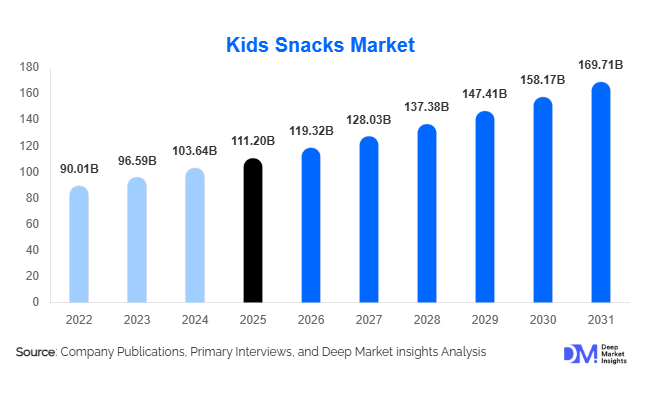

According to Deep Market Insights, the global kids snacks market size was valued at USD 111.2 billion in 2025 and is projected to grow from USD 119.32 billion in 2026 to reach USD 169.71 billion by 2031, expanding at a CAGR of 7.3% during the forecast period (2026–2031). The kids snacks market growth is primarily driven by increasing parental demand for convenient and nutritious food products, rising urbanization, expanding organized retail penetration, and the growing popularity of healthy packaged snacks among school-age children.

Key Market Insights

- Healthy and functional snacks are rapidly replacing traditional sugary products, with growing demand for clean-label, protein-rich, low-sugar, and fortified snack offerings for children.

- Single-serve and portion-controlled packaging formats dominate the market, driven by increasing lunchbox consumption and on-the-go snacking trends among school-going children.

- North America leads the global market, supported by strong packaged food penetration, premium product adoption, and advanced retail distribution networks.

- Asia-Pacific is the fastest-growing region, fueled by urbanization, rising disposable incomes, and expanding middle-class populations in China, India, and Southeast Asia.

- E-commerce and quick-commerce channels are reshaping snack distribution, allowing emerging brands to reach consumers directly through digital grocery ecosystems.

- Sustainable packaging and ingredient transparency are becoming critical purchasing factors, especially among millennial and Gen Z parents seeking environmentally responsible brands.

kids snacks market latest trends

Shift Toward Functional and Nutrient-Enriched Snacks

The kids snacks industry is increasingly moving toward functional nutrition products that provide health benefits beyond basic calorie intake. Manufacturers are introducing snacks fortified with vitamins, minerals, probiotics, calcium, fiber, and plant-based proteins to address growing parental concerns regarding childhood immunity, digestive health, and balanced nutrition. Protein bars for children, probiotic yogurt snacks, fruit-based functional gummies, and fortified granola bars are becoming mainstream across developed markets. Clean-label claims such as non-GMO, organic, gluten-free, and preservative-free are also influencing consumer purchasing decisions. Major companies are reformulating legacy products by reducing sugar, sodium, and artificial ingredients while maintaining child-friendly flavors and textures.

Growth of Digital and Quick-Commerce Snack Retail

The expansion of digital grocery ecosystems and quick-commerce platforms is transforming how parents purchase kids snacks globally. Online channels are enabling consumers to compare nutritional labels, access subscription snack boxes, and discover premium niche brands previously unavailable through traditional retail outlets. Quick-commerce platforms offering delivery within minutes are accelerating impulse purchases of lunchbox snacks, dairy snacks, and healthy packaged foods in urban markets. Social media marketing, influencer-driven promotions, and animated digital campaigns targeting younger consumers are further increasing online engagement. Direct-to-consumer snack brands are also utilizing AI-driven recommendation systems and personalized subscription models to strengthen customer retention and improve recurring revenues.

kids snacks market drivers

Rising Demand for Convenient On-the-Go Nutrition

Modern family lifestyles and the increasing participation of women in the workforce are significantly driving demand for portable and ready-to-eat kids snacks. Parents increasingly prefer products that require minimal preparation while still delivering balanced nutrition suitable for school lunches, travel, and extracurricular activities. Single-serve packs, resealable snack pouches, and portion-controlled products are witnessing particularly strong growth due to their convenience and ease of consumption. Urbanization and growing dual-income households in emerging economies are further accelerating demand for packaged snack solutions designed specifically for children.

Increasing Health Awareness Among Parents

Rising concerns regarding childhood obesity, sugar consumption, and artificial additives are reshaping product development strategies across the kids snacks industry. Parents are actively seeking healthier alternatives containing whole grains, fruits, dairy proteins, natural sweeteners, and functional ingredients. This trend has encouraged manufacturers to introduce low-sugar cookies, baked savory snacks, organic fruit bars, and allergen-free snack products. Government-backed school nutrition programs and stricter food-labeling regulations are also supporting the transition toward healthier snacking options globally.

global market restraints

Volatility in Raw Material Prices

The kids snacks market remains vulnerable to fluctuations in the prices of key raw materials including cocoa, dairy ingredients, edible oils, grains, fruits, and packaging materials. Climate-related agricultural disruptions and global supply-chain uncertainties continue to increase production costs for snack manufacturers. Companies operating in price-sensitive emerging markets face significant margin pressures, especially when passing higher costs onto consumers becomes difficult. Packaging inflation and transportation costs further intensify operational challenges across the value chain.

Stringent Food Regulations and Marketing Restrictions

Governments across North America and Europe are implementing increasingly strict regulations related to child nutrition, food labeling, and advertising practices targeting children. Sugar reduction mandates, restrictions on cartoon-based marketing, and school-compliant nutritional standards are forcing manufacturers to invest heavily in reformulation and compliance initiatives. Failure to align with evolving regulations may result in limited retail access, reputational risks, and reduced participation in institutional food programs. These regulatory complexities remain a major challenge for both global and regional market participants.

kids snacks industry key opportunities

Expansion of Organic and Clean-Label Product Lines

The growing consumer preference for organic and clean-label foods presents a significant opportunity for snack manufacturers globally. Parents increasingly prefer products free from artificial colors, preservatives, high-fructose corn syrup, and synthetic additives. This trend is creating strong growth potential for organic fruit snacks, plant-based granola bars, low-sugar cookies, and natural dairy snacks targeted at children. Premium healthy snack categories also allow companies to achieve higher profit margins and stronger customer loyalty. Emerging economies such as India, Brazil, and Indonesia are gradually witnessing increased adoption of premium nutritional snacks among urban middle-class households.

Institutional Demand Through Schools and Childcare Centers

School nutrition programs and institutional procurement channels are emerging as major growth opportunities within the global kids snacks market. Governments and educational institutions are increasingly emphasizing healthier meal and snack standards to combat rising childhood obesity rates. Portion-controlled granola bars, fruit cups, yogurt snacks, and fortified products are gaining strong demand across schools, daycare centers, and youth sports academies. Manufacturers that align products with school nutrition compliance standards can secure long-term supply contracts and stable volume growth. In addition, partnerships with educational institutions provide companies with early brand exposure among children, strengthening long-term consumer loyalty and repeat purchasing behavior.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 111.20 Billion |

| Market Size in 2026 | USD 119.32 Billion |

| Market Size in 2031 | USD 169.71 Billion |

| CAGR | 7.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Healthy and functional snacks represent the leading product category, accounting for nearly 24% of the global kids snacks market in 2025. Demand is being driven by growing parental preference for fortified, protein-rich, and clean-label products designed to support balanced childhood nutrition. Fruit-based snacks, probiotic dairy snacks, and low-sugar granola bars are witnessing particularly strong growth across North America and Europe. Savory snacks such as baked chips, popcorn, and multigrain snacks continue to hold substantial market share due to their affordability and widespread availability. Dairy-based snacks including yogurt tubes and cheese snacks are also expanding rapidly, supported by increasing protein consumption trends and school lunchbox demand. Frozen kids snacks and plant-based protein snacks are emerging as niche but high-growth categories, especially among urban consumers seeking healthier convenience foods.

Age Group Insights

School-age children aged 7–12 years account for the largest share of the global kids snacks market, representing approximately 38% of total demand in 2025. This segment consumes high volumes of packaged snacks through school lunches, after-school activities, and digital entertainment occasions. Manufacturers heavily target this demographic through animated packaging, flavor innovation, and portion-controlled snack formats. Preschool children aged 4–6 years represent another important consumer group, particularly for dairy-based snacks, fruit pouches, and fortified products. Teenagers are increasingly influencing demand for protein-based snacks, functional beverages, and healthier savory snack options as fitness awareness and active lifestyles become more common among older children.

Packaging Type Insights

Single-serve packaging dominates the market with nearly 46% share globally due to its convenience, hygiene, portability, and suitability for lunchbox applications. Parents increasingly prefer portion-controlled packs that help manage calorie intake while minimizing food waste. Multi-pack pouches and resealable packaging formats are also experiencing rising demand, particularly among larger households seeking value-oriented purchases. Sustainable and eco-friendly packaging is becoming a major innovation area within the market, especially in Europe and developed Asia-Pacific countries where environmental awareness strongly influences consumer purchasing decisions. Manufacturers are investing in recyclable packaging materials, biodegradable snack pouches, and reduced-plastic packaging technologies to strengthen brand positioning.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channels for kids snacks, accounting for approximately 41% of global sales in 2025. These retail formats offer extensive product assortments, promotional visibility, and strong shelf presence for both multinational and regional snack brands. Convenience stores continue to perform strongly in urban areas where impulse snack purchases are common. However, online retail is the fastest-growing distribution channel, supported by rising digital grocery adoption and quick-commerce expansion. Direct-to-consumer snack subscriptions, mobile grocery applications, and online health-food retailers are increasingly reshaping purchasing behavior among younger parents seeking convenience and broader product variety.

Ingredient Profile Insights

Reduced-sugar and clean-label snacks collectively accounted for nearly 29% of the global market in 2025, reflecting growing parental concerns regarding childhood obesity and excessive sugar consumption. Products featuring natural sweeteners, whole grains, fruit-based ingredients, and preservative-free formulations are gaining stronger retail shelf presence. Organic snacks are witnessing rapid growth in developed markets due to increasing willingness among consumers to pay premium prices for healthier food options. Plant-based ingredient formulations are also gaining traction, particularly in North America and Europe where vegan and flexitarian dietary trends are influencing family food consumption habits.

Explore more data points, trends and opportunities Download Free Sample Report

Kids Snacks Market Segmentations

By Product Type

- Savory Snacks

- Sweet Snacks

- Healthy & Functional Snacks

- Fruit & Natural Snacks

- Dairy-Based Snacks

- Bakery & Grain Snacks

- Frozen Kids Snacks

- Meat & Protein Snacks

By Age Group

- Toddlers

- Preschool Children

- School-Age Children

- Teenagers

By Ingredient Profile

- Conventional

- Organic

- Plant-Based

- High-Protein

- Reduced-Sugar

- Clean Label

- Fortified/Nutraceutical

By Packaging Type

- Single-Serve Packs

- Multi-Pack Pouches

- Resealable Packs

- Eco-Friendly Packaging

- Portion-Control Packs

- On-the-Go Packs

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Grocery Stores

- Specialty Health Stores

- E-Commerce Marketplaces

- Direct-to-Consumer (D2C)

- Quick Commerce Platforms

Regional Insights

North America

North America accounted for approximately 34% of the global kids snacks market in 2025, making it the leading regional market. The United States dominates regional demand due to high packaged food consumption, strong retail infrastructure, and rising adoption of premium healthy snacks. Parents increasingly prefer organic, allergen-free, and functional products containing reduced sugar and natural ingredients. Canada is also witnessing strong demand growth for clean-label and environmentally sustainable snack offerings. E-commerce penetration and subscription snack services remain highly developed across the region, supporting innovation and premium product accessibility.

Europe

Europe represented nearly 27% of the global market in 2025, driven by strong demand across Germany, the United Kingdom, France, and Italy. Consumers in the region are increasingly prioritizing healthier snack alternatives and sustainable packaging solutions. Strict food-labeling regulations and sugar-reduction initiatives are encouraging manufacturers to reformulate products and introduce cleaner ingredient profiles. The United Kingdom remains a key innovation hub for low-calorie snacks, organic fruit products, and dairy-based nutritional snacks targeted at children.

Asia-Pacific

Asia-Pacific is projected to register the fastest CAGR globally, exceeding 9% during the forecast period. China represents the largest market within the region due to its large child population, rising middle-class income, and expanding urban retail networks. India is emerging as one of the fastest-growing countries, supported by increasing urbanization, rapid quick-commerce adoption, and growing awareness regarding packaged nutrition products. Japan and South Korea continue to demonstrate strong demand for premium and visually appealing functional snacks designed for children. Rising digital grocery adoption and modern retail expansion across Southeast Asia are further accelerating regional market growth.

Latin America

Latin America is experiencing steady growth led by Brazil and Mexico, where expanding supermarket penetration and rising disposable incomes are driving packaged snack demand. Multinational food companies are increasing investments across the region to capitalize on growing urban populations and changing dietary habits. Fruit-based snacks, affordable savory products, and dairy snacks remain popular categories among middle-income households.

Middle East & Africa

The Middle East & Africa region is witnessing growing demand for imported packaged kids snacks, particularly in the UAE, Saudi Arabia, and South Africa. Rising household spending on convenience foods, expanding organized retail infrastructure, and growing youth populations are supporting market expansion. Premium healthy snacks and fortified dairy products are becoming increasingly popular among affluent urban consumers across Gulf countries. South Africa remains one of the leading regional markets due to its established food processing industry and modern retail ecosystem.