Khari Biscuit Market Size

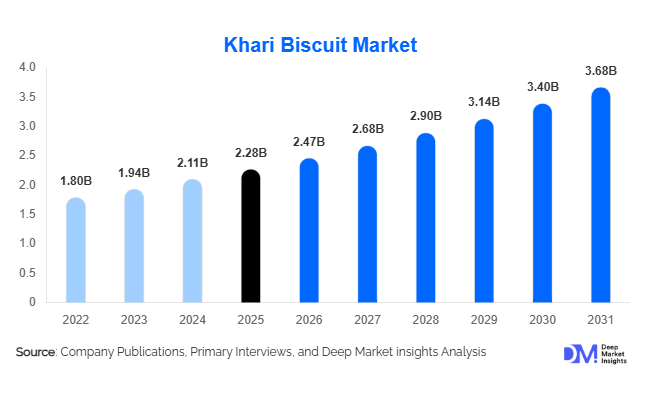

According to Deep Market Insights, the global khari biscuit market size was valued at USD 2.28 billion in 2025 and is projected to grow from USD 2.47 billion in 2026 to reach USD 3.68 billion by 2031, expanding at a CAGR of 8.3% during the forecast period (2026–2031). The khari biscuit market growth is primarily driven by rising demand for convenient bakery snacks, increasing consumption of ethnic and premium food products, growing penetration of organized retail channels, and expanding exports of South Asian bakery products to developed markets. Product innovation in healthier formulations, including multigrain, low-fat, and gluten-free variants, is further supporting market expansion globally.

Key Market Insights

- Tea-time consumption continues to dominate global demand, with khari biscuits remaining one of the most preferred accompaniments to tea and coffee, particularly in Asia and the Middle East.

- Premium and health-oriented product variants are gaining traction, driven by consumer demand for low-fat, multigrain, high-fiber, and clean-label bakery snacks.

- Asia-Pacific dominates the global market, accounting for more than half of global demand owing to strong consumption in India and increasing popularity across neighboring countries.

- Middle East & Africa is emerging as the fastest-growing region, supported by high consumption among expatriate populations and increasing imports of packaged ethnic foods.

- E-commerce and direct-to-consumer channels are transforming distribution, enabling smaller manufacturers to access international markets with limited investment in physical retail networks.

- Technological advancements in baking automation and packaging are improving production efficiency, shelf life, and product quality, enhancing global competitiveness among manufacturers.

Khari Biscuit Market Latest Trends

Premium and Health-Focused Khari Biscuits Gaining Popularity

Consumers are increasingly shifting toward healthier and premium bakery snacks, creating substantial opportunities within the khari biscuit market. Manufacturers are introducing multigrain, whole wheat, high-fiber, protein-enriched, and low-fat product formulations to cater to health-conscious consumers. Premium variants featuring cheese, herbs, butter, and specialty ingredients are also becoming increasingly popular among urban consumers seeking differentiated snacking experiences. This trend is particularly evident in developed markets where consumers are willing to pay higher prices for premium bakery products with clean labels and natural ingredients. Manufacturers are further strengthening their premium portfolios by introducing artisanal packaging and gourmet flavors targeted at gifting and specialty retail channels.

Digital and Export-Led Market Expansion

E-commerce has become a significant growth channel for khari biscuit manufacturers. Online grocery platforms, ethnic food marketplaces, and direct-to-consumer websites are enabling brands to expand beyond traditional retail networks. International demand is also increasing due to growing South Asian diaspora populations in North America, Europe, Australia, and the Middle East. Specialty retailers are increasingly stocking premium khari biscuit products, while digital platforms allow manufacturers to directly engage with overseas consumers. The ability to sell through online channels has significantly lowered entry barriers for small and medium-sized bakery companies seeking global expansion opportunities.

Khari Biscuit Market Drivers

Growing Demand for Convenient Ready-to-Eat Snacks

Rapid urbanization and increasingly busy lifestyles are driving global demand for convenient and affordable snacking products. Khari biscuits offer long shelf life, easy portability, and affordability, making them an attractive option for everyday consumption. The growing preference for packaged snacks among working professionals and younger consumers is significantly supporting market growth.

Premiumization of Bakery Products

Consumers are increasingly willing to spend on premium bakery products that offer unique flavors, superior ingredients, and artisanal experiences. Manufacturers have responded by introducing premium khari biscuits incorporating imported butter, cheese, herbs, and gourmet seasonings. The premiumization trend has increased average selling prices and improved profitability for organized manufacturers globally.

Expansion of Organized Retail and E-Commerce

The rapid growth of supermarkets, hypermarkets, convenience stores, and online grocery channels has significantly improved product accessibility. Organized retail channels are helping branded manufacturers gain market share from local bakeries and unorganized players. Digital retail platforms have further accelerated product availability and consumer reach, particularly in export markets.

Khari Biscuit Market Restraints

Volatility in Raw Material Prices

Manufacturers remain exposed to significant fluctuations in the prices of wheat flour, butter, edible oils, sugar, and packaging materials. Raw material inflation directly impacts production costs and can compress margins, particularly in the highly competitive economy segment where pricing flexibility remains limited.

Competition from Alternative Snack Categories

The market faces intense competition from cookies, crackers, chips, savory snacks, and healthier alternatives such as granola bars and protein snacks. Maintaining product differentiation and customer loyalty remains a challenge, especially in developed markets where consumers have a wide range of snacking options.

Khari Biscuit Industry Key Opportunities

Expansion into Health and Functional Bakery Segments

The increasing demand for healthier snacking presents significant opportunities for manufacturers to introduce functional khari biscuit products. High-fiber, protein-enriched, gluten-free, and organic formulations are expected to witness strong demand among health-conscious consumers. Premium functional products also offer significantly higher margins compared to conventional variants, making this segment particularly attractive for both existing players and new market entrants.

Export-Led Growth and Ethnic Food Retail Expansion

International demand for ethnic bakery products continues to rise due to increasing migration and multicultural food consumption patterns. Markets such as the United States, Canada, Australia, the United Kingdom, and the UAE are witnessing growing demand for packaged khari biscuits through ethnic grocery stores and online retailers. Export-led expansion provides manufacturers with opportunities to diversify revenues and reduce dependence on domestic markets.

Digital Retail and Direct-to-Consumer Business Models

The rapid growth of online grocery platforms is creating new opportunities for manufacturers to directly engage with consumers. Subscription-based snack boxes, digital marketing campaigns, and personalized product offerings are enabling brands to expand globally with relatively low distribution investments. Direct-to-consumer channels also provide valuable consumer insights that support product innovation and customer retention.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.28 Billion |

| Market Size in 2026 | USD 2.47 Billion |

| Market Size in 2031 | USD 3.68 Billion |

| CAGR | 8.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Plain and classic khari biscuits account for approximately 38% of global market revenue, making them the leading product category in the global khari biscuits market. The segment's dominance is primarily attributed to its deep-rooted consumption habits across South Asian households, affordable pricing, widespread availability across traditional retail channels, and broad consumer appeal across all age groups. These products are frequently consumed as a tea-time accompaniment, particularly in India and neighboring countries, where demand for traditional bakery products remains consistently high. The simplicity of ingredients and familiarity of taste further support repeat purchases and high-volume consumption, enabling the segment to maintain its market leadership.Premium cheese and gourmet variants are also expanding rapidly, particularly in developed economies where consumers increasingly seek differentiated bakery experiences and premium snacking options. Rising disposable incomes, growing café culture, and increasing willingness to spend on artisanal bakery products have significantly contributed to demand for premium khari biscuit offerings. In addition, manufacturers are emphasizing product innovation through the incorporation of exotic seasonings, specialty cheeses, and premium ingredients to cater to evolving consumer preferences.Health-oriented khari biscuits, including multigrain, whole wheat, low-fat, high-fiber, and gluten-free variants, represent one of the fastest-growing categories within the market. Growing awareness regarding healthy eating habits, increasing incidences of lifestyle diseases, and rising demand for clean-label and functional food products are encouraging manufacturers to diversify their portfolios with nutritionally enhanced offerings. The health and wellness trend is expected to create significant opportunities for product innovation over the forecast period.

Packaging Insights

Flexible pouches dominate the global market with nearly 48% share of revenue, making them the preferred packaging format for khari biscuits. The segment's leadership is primarily driven by its cost-effectiveness, lightweight structure, ease of transportation, and ability to preserve product freshness while minimizing packaging costs. Flexible pouches also offer excellent shelf visibility and are highly suitable for mass retail distribution, making them particularly attractive for manufacturers targeting price-sensitive consumers and high-volume markets.Family packs continue to gain popularity due to increasing household consumption and value-oriented purchasing behavior. Larger pack sizes provide economic benefits to consumers while supporting higher sales volumes for manufacturers. The increasing prevalence of at-home snacking and family consumption occasions has further accelerated demand for larger packaging formats.Premium gift boxes are witnessing substantial demand during festive seasons and in export markets where consumers increasingly seek premium packaged ethnic food products. Attractive packaging designs and premium positioning are helping manufacturers capitalize on gifting occasions and the growing demand for culturally inspired food products in international markets.Single-serve and on-the-go packaging formats are emerging as attractive solutions among younger consumers, office workers, and urban populations seeking convenience-oriented snacking products. Rising mobility, busy lifestyles, and increasing demand for portion-controlled snacks are expected to support continued growth in this packaging segment.

Distribution Channel Insights

Traditional grocery stores and neighborhood retail outlets account for approximately 41% of global market sales, making them the leading distribution channel in the khari biscuits market. The segment's dominance is largely attributed to the extensive presence of small-format retail stores, particularly across Asia-Pacific, where consumers continue to rely heavily on local kirana stores and independent retailers for daily food purchases. Strong retailer-consumer relationships, widespread geographic penetration, and the availability of affordable products continue to reinforce the importance of traditional retail channels.Supermarkets and hypermarkets are steadily expanding their market share due to increasing urbanization, rising disposable incomes, and growing penetration of organized retail infrastructure. These channels provide consumers with greater product variety, premium offerings, and enhanced shopping experiences, enabling manufacturers to improve product visibility and strengthen brand positioning.E-commerce channels represent one of the fastest-growing distribution formats, driven by the rapid adoption of online grocery platforms, increasing smartphone penetration, and rising consumer preference for doorstep delivery services. The availability of wider product assortments, promotional discounts, and subscription-based purchasing models is further accelerating online sales of packaged bakery products.Bakery chains and specialty stores are increasingly focusing on premium and artisanal khari biscuit offerings to differentiate themselves in a highly competitive market environment. The growing popularity of fresh bakery products and premium snacking experiences is encouraging the expansion of specialized retail formats worldwide.

Consumer Group Insights

Young adults aged 18–35 years represent the largest consumer segment, accounting for approximately 34% of global demand. The segment's leadership is primarily driven by high snacking frequency, increasing preference for convenience foods, and strong interest in flavored, premium, and innovative bakery products. Urban lifestyles, rising disposable incomes, and increasing experimentation with new food products continue to support robust demand among this demographic group.Middle-aged consumers remain an important contributor to market demand, particularly for traditional khari biscuit variants consumed during tea-time occasions and family gatherings. Their purchasing behavior is largely influenced by product familiarity, affordability, and long-standing consumption habits.Senior consumers continue to represent a stable market segment due to their preference for light bakery snacks and products with mild flavors and simple ingredients. The ease of consumption and traditional appeal of khari biscuits contribute significantly to demand among older consumers.Children's consumption is increasingly being influenced by innovative packaging, attractive branding, and the introduction of new flavors. Manufacturers are focusing on product differentiation and visually appealing packaging formats to attract younger consumers and encourage trial purchases.

End-Use Insights

Household retail consumption dominates the market, accounting for nearly 72% of global demand, making it the leading end-use segment. The segment's dominance is primarily supported by the strong cultural association of khari biscuits with daily tea consumption, frequent household snacking occasions, and widespread availability across traditional and modern retail channels. The affordability of products and high repeat purchase rates further strengthen the segment's market position.The HoReCa segment is emerging as one of the fastest-growing end-use categories due to increasing consumption in cafés, quick-service restaurants, hotels, and food service establishments. The expansion of organized food service infrastructure and rising consumer preference for bakery accompaniments are creating substantial opportunities for manufacturers.Corporate pantry demand and institutional catering applications are also expanding as packaged bakery snacks become increasingly popular in workplaces, educational institutions, healthcare facilities, and transportation catering services. The convenience and long shelf life of khari biscuits make them an attractive option for institutional procurement.Export-oriented ethnic retail channels continue to create substantial growth opportunities, particularly in North America, Europe, and the Middle East, where growing immigrant populations and rising interest in international cuisines are supporting demand for traditional South Asian bakery products.

Explore more data points, trends and opportunities Download Free Sample Report

Khari Biscuit Market Segmentations

By Product Type

- Plain/Classic Khari Biscuits

- Masala & Spiced Khari Biscuits

- Sweet Khari Biscuits

- Cheese & Savory Flavored Khari Biscuits

- Whole Wheat & Multigrain Khari Biscuits

- Health & Functional Khari Biscuits

- Premium & Gourmet Khari Biscuits

By Packaging Type

- Flexible Pouches

- Family Packs

- Bulk Foodservice Packs

- Gift & Premium Boxes

- Single-Serve and On-the-Go Packs

By Nature

- Conventional

- Organic/Clean Label

By Price Positioning

- Economy

- Mid-Range

- Premium

By Distribution Channel

- Traditional Grocery & Kirana Stores

- Supermarkets & Hypermarkets

- Convenience Stores

- Bakery Chains & Specialty Stores

- Online Retail/E-Commerce

- Foodservice & Institutional Sales

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 53% of the global market in 2025, making it the largest regional market for khari biscuits. India alone contributes nearly 36% of global market revenue, supported by strong cultural affinity toward bakery snacks, extensive manufacturing capacity, and a rapidly expanding organized retail sector. China and Southeast Asian countries are increasingly adopting packaged bakery products, further strengthening regional demand.The region's growth is being driven by rapid urbanization, rising disposable incomes, expanding middle-class populations, increasing penetration of organized retail and e-commerce channels, and strong demand for convenient packaged snacks. Additionally, changing lifestyles, increasing female workforce participation, and the growing preference for ready-to-eat bakery products are encouraging higher consumption of packaged snack items. Continuous product innovation and expanding domestic manufacturing capabilities are expected to maintain Asia-Pacific's leadership position throughout the forecast period.

North America

North America accounts for approximately 16% of global market demand. The United States represents the largest market within the region, driven primarily by ethnic food consumption and increasing multicultural eating habits. Canadian demand is also increasing through specialty retailers and online grocery channels that cater to immigrant populations and consumers seeking international food experiences.Regional growth is supported by rising consumer interest in international cuisines, expanding South Asian diaspora populations, increasing penetration of specialty food retailers, and growing demand for premium and artisanal bakery products. The rapid expansion of e-commerce platforms and increasing availability of imported ethnic food products across mainstream retail channels are also contributing significantly to market growth in the region.

Europe

Europe contributes approximately 14% of global market revenue. The United Kingdom remains the largest consumer market within the region due to its significant South Asian population and well-developed ethnic food retail infrastructure. Germany and France are witnessing increasing demand for premium packaged bakery products and international snack offerings.The region's growth is primarily driven by increasing multicultural consumption patterns, rising popularity of ethnic cuisines, growing demand for premium bakery products, and the expansion of international food sections within supermarkets and hypermarkets. Consumers are increasingly seeking authentic and differentiated snack experiences, creating opportunities for imported ethnic bakery products and premium khari biscuit offerings.

Latin America

Latin America represents nearly 6% of global demand and remains an underpenetrated market. Brazil and Mexico are witnessing gradual increases in demand for imported bakery products, particularly among affluent urban consumers and multicultural food enthusiasts.Regional growth is being supported by increasing urbanization, rising disposable incomes among middle-income households, expanding modern retail infrastructure, and growing consumer exposure to international cuisines through digital media and tourism. The gradual development of premium food retail channels and increasing demand for differentiated snack products are expected to create long-term opportunities in the region.

Middle East & Africa

The Middle East and Africa account for approximately 11% of global market revenue and represent the fastest-growing regional market, with an estimated CAGR of nearly 9.5%. The United Arab Emirates and Saudi Arabia are major demand centers due to large expatriate populations and strong demand for packaged ethnic foods. Increasing retail investments and growing premium food consumption continue to support regional market expansion.The region's rapid growth is being driven by a large South Asian expatriate workforce, increasing demand for convenient packaged foods, expanding supermarket and hypermarket networks, rising disposable incomes, and significant investments in food retail infrastructure. The flourishing hospitality sector, increasing tourism activities, and growing consumer preference for premium and imported food products are further accelerating demand for khari biscuits across the Middle East and Africa.

Key Players in the Khari Biscuit Market

- Britannia Industries Limited

- Parle Products Private Limited

- ITC Limited

- PriyaGold Biscuits

- Surya Food & Agro Limited

- Bisk Farm

- Cremica Food Industries

- Monginis Foods

- Bonn Group of Industries

- Karachi Bakery

- Baker Street Foods

- Patel Brothers

- Home Breads

- Anis Export

- Nafees Bakery