Instant Pudding Market Size

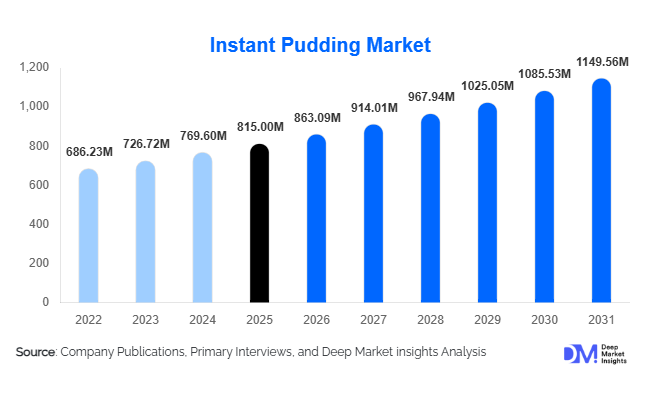

According to Deep Market Insights, the global instant pudding market size was valued at USD 815 million in 2025 and is projected to grow from USD 863.09 million in 2026 to reach USD 1,149.56 million by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The instant pudding market growth is primarily driven by rising demand for convenient dessert solutions, increasing home baking activities, expanding foodservice applications, and continuous innovation in healthier pudding formulations. Growing consumer preference for ready-to-prepare foods, combined with the increasing availability of sugar-free, protein-enriched, and plant-based pudding products, is supporting market expansion across both developed and emerging economies. The market also benefits from strong retail penetration, increasing e-commerce adoption, and rising consumption of packaged desserts among urban households globally.

Key Market Insights

- Instant pudding mixes account for nearly 68% of global market revenue, driven by longer shelf life, affordability, and broad household adoption.

- Vanilla remains the leading flavor category, representing approximately 29% of global demand due to its versatility across dessert and bakery applications.

- North America dominates the global market, accounting for nearly 35% of total revenue, led by strong household consumption and home baking trends.

- Asia-Pacific is the fastest-growing regional market, supported by rising disposable incomes, westernization of diets, and expansion of organized retail channels.

- Commercial bakery applications are expanding rapidly, with manufacturers increasingly utilizing instant pudding as fillings, toppings, and texture-enhancing ingredients.

- Health-oriented product innovation, including sugar-free, clean-label, gluten-free, and plant-based formulations, is reshaping competitive strategies across the industry.

Instant Pudding Market Latest Trends

Growth of Clean-Label and Health-Focused Formulations

Consumer preferences are increasingly shifting toward healthier dessert options, encouraging manufacturers to introduce clean-label instant pudding products containing natural ingredients, reduced sugar content, and fewer artificial additives. The growing prevalence of lifestyle-related health concerns such as obesity and diabetes has accelerated demand for sugar-free and low-calorie alternatives. Manufacturers are also incorporating protein fortification, fiber enrichment, and functional ingredients into pudding formulations to attract health-conscious consumers. Plant-based variants utilizing oat, coconut, almond, and soy ingredients are gaining popularity among vegan and lactose-intolerant consumers. As regulatory scrutiny over ingredient transparency increases globally, clean-label positioning is expected to remain one of the most influential trends shaping product development strategies throughout the forecast period.

Expansion of Home Baking and Dessert Customization

The growing popularity of home baking continues to drive demand for instant pudding products beyond traditional dessert consumption. Consumers increasingly utilize pudding mixes in cakes, cheesecakes, pastries, pie fillings, frostings, trifles, and other dessert preparations. Social media platforms, online recipe communities, and food content creators have significantly expanded consumer awareness of pudding-based baking applications. Manufacturers are responding by launching specialized formulations optimized for baking performance and texture enhancement. The trend is particularly pronounced among younger consumers who seek convenient ingredients that simplify baking while delivering professional-quality results. As home cooking and baking remain popular across North America, Europe, and parts of Asia-Pacific, instant pudding is evolving into a multifunctional ingredient category rather than solely a standalone dessert product.

Instant Pudding Market Drivers

Increasing Demand for Convenience Foods

One of the primary drivers of the instant pudding market is the growing global demand for convenient and time-saving food products. Urbanization, busy work schedules, and rising participation of dual-income households have encouraged consumers to seek ready-to-prepare food options that require minimal effort. Instant pudding products offer quick preparation, consistent taste, and extended shelf life, making them highly attractive across household and foodservice environments. The convenience factor remains particularly important among younger consumers and working professionals who prioritize ease of preparation without compromising on taste and indulgence.

Rising Home Baking and Dessert Consumption

The global increase in home baking activities has significantly contributed to market growth. Instant pudding is widely used in bakery applications as a filling, frosting ingredient, and moisture enhancer in cakes and pastries. The rise of digital recipe platforms and social media food trends has encouraged consumers to experiment with new dessert recipes incorporating pudding mixes. This trend has expanded the addressable market beyond direct dessert consumption and created additional demand from amateur bakers and home chefs seeking versatile baking ingredients.

Product Innovation and Premiumization

Manufacturers continue investing in flavor innovation, premium product positioning, and healthier formulations to differentiate themselves in a competitive market. Premium flavors such as salted caramel, cookies and cream, Belgian chocolate, and seasonal limited-edition variants are attracting consumers seeking indulgent experiences. Simultaneously, clean-label and plant-based products are helping companies access higher-margin consumer segments. These innovations support pricing power while broadening the market’s appeal across multiple demographic groups.

Instant Pudding Market Restraints

Health Concerns Related to Sugar and Additives

Traditional instant pudding products often contain significant amounts of sugar, artificial flavors, and preservatives. Increasing awareness of nutrition and wellness may discourage consumption among health-conscious consumers. Regulatory initiatives targeting sugar reduction and stricter food labeling requirements may also create challenges for manufacturers that rely heavily on conventional formulations. Companies must continuously invest in reformulation efforts to maintain competitiveness and align with evolving consumer expectations.

Competition from Alternative Dessert Categories

The market faces growing competition from yogurt desserts, refrigerated puddings, protein snacks, frozen desserts, and premium bakery products. Many alternative dessert categories are perceived as fresher, healthier, or more indulgent than traditional instant pudding products. To remain competitive, manufacturers must continue emphasizing convenience, affordability, and product innovation while expanding into adjacent functional dessert categories.

Instant Pudding Industry Key Opportunities

Expansion of Plant-Based and Functional Dessert Products

The growing global market for plant-based foods presents a significant opportunity for instant pudding manufacturers. Consumers increasingly seek dairy-free, vegan, and allergen-friendly alternatives that align with dietary preferences and sustainability goals. Product innovations utilizing oat milk, almond milk, soy protein, and coconut ingredients can help manufacturers access rapidly expanding consumer segments. Functional formulations featuring added protein, probiotics, collagen, and fiber are also creating opportunities to position instant pudding as both an indulgent and health-oriented product category.

Emerging Market Expansion and Retail Modernization

Developing economies across Asia-Pacific, Latin America, and the Middle East represent substantial growth opportunities due to rising disposable incomes and increasing penetration of organized retail channels. Urban consumers in countries such as China, India, Indonesia, Saudi Arabia, and the UAE are increasingly adopting packaged dessert products as western-style eating habits become more prevalent. Manufacturers can capitalize on these trends through localized flavors, smaller packaging formats, and targeted marketing strategies. The expansion of e-commerce and digital grocery platforms further enhances accessibility and supports market penetration in previously underserved regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 815.00 Million |

| Market Size in 2026 | USD 863.09 Million |

| Market Size in 2031 | USD 1149.56 Million |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The powder-based instant pudding mix segment dominates the global instant pudding market, accounting for approximately 68% of total revenue in 2025. Its market leadership is primarily driven by its extended shelf life, cost-effective storage and transportation advantages, ease of handling, and widespread consumer familiarity. Powder formulations offer significant flexibility for both household and commercial applications, allowing consumers and foodservice operators to customize texture, flavor intensity, and portion sizes according to specific requirements. In addition, the growing popularity of home baking, dessert preparation, and meal-kit solutions continues to reinforce demand for powdered instant pudding products. Manufacturers also benefit from lower production and distribution costs compared to ready-to-eat alternatives, supporting broader market availability and competitive pricing across both developed and emerging economies.The ready-to-eat pudding segment is experiencing steady growth as consumers increasingly prioritize convenience, portability, and time-saving food solutions. Single-serve pudding cups have gained substantial popularity among busy professionals, students, and families seeking convenient snack and dessert options. Refrigerated ready-to-eat variants are witnessing rising demand among consumers looking for fresher textures, premium ingredients, and enhanced sensory experiences, particularly in North America and Europe. Meanwhile, shelf-stable pudding cups continue expanding their presence through convenience stores, vending machines, travel retail outlets, and institutional foodservice channels. Product innovations involving plant-based ingredients, reduced sugar formulations, and protein-enriched recipes are further enhancing the appeal of ready-to-eat pudding products across multiple consumer demographics.

Flavor Insights

Vanilla remains the leading flavor segment, accounting for approximately 29% of global market demand in 2025. The segment’s dominance is largely attributed to its versatility across multiple applications, including standalone desserts, bakery fillings, layered desserts, and customized recipes. Vanilla serves as a neutral base flavor that appeals to a broad consumer audience and allows manufacturers to cater to diverse regional taste preferences. Its widespread use in both household and commercial food preparation continues to strengthen its market position, making it the preferred choice among consumers and foodservice operators alike.Chocolate represents the second-largest flavor category and continues to benefit from strong global consumer acceptance across all age groups. The flavor's established popularity in desserts, confectionery products, and bakery applications supports consistent demand worldwide. Beyond traditional flavors, manufacturers are increasingly expanding their portfolios with butterscotch, caramel, banana, strawberry, and fruit-inspired variants to address evolving consumer preferences. The growing demand for indulgent and premium dessert experiences has further accelerated the adoption of specialty flavors such as salted caramel, cookies-and-cream, mocha, hazelnut, and limited-edition seasonal offerings. These innovations are particularly resonating with younger consumers seeking novel taste experiences and premium dessert options.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, accounting for nearly 48% of global instant pudding sales in 2025. The segment's leadership is supported by extensive shelf visibility, broad product assortments, competitive pricing strategies, promotional activities, and strong consumer trust in organized retail formats. These retail outlets provide manufacturers with access to large consumer bases while enabling effective product merchandising and brand positioning. Growing investments in modern retail infrastructure across developing economies are further strengthening the importance of supermarkets and hypermarkets within the global distribution landscape.Convenience stores continue to play a critical role in the distribution of ready-to-eat pudding products, particularly in urban centers where demand for quick and portable snack options remains high. At the same time, e-commerce has emerged as one of the fastest-growing distribution channels, driven by increasing online grocery adoption, expanding digital retail ecosystems, and shifting consumer purchasing behaviors. Online platforms allow manufacturers to reach wider geographic markets, offer subscription-based purchasing models, and cater to consumers seeking specialty, organic, allergen-free, and functional pudding products. The growing integration of direct-to-consumer strategies, digital marketing campaigns, and omnichannel retail approaches is expected to further accelerate online sales growth throughout the forecast period.

Application Insights

Direct dessert consumption represents the largest application segment, accounting for approximately 38% of global market value in 2025. The segment continues to benefit from strong consumer demand for affordable, convenient, and easy-to-prepare dessert solutions suitable for all age groups. Instant pudding remains a popular choice for everyday consumption due to its quick preparation time, versatility, and ability to satisfy consumer demand for indulgent yet economical dessert options. Increasing demand for packaged desserts and convenient meal solutions further supports the growth of this segment across both developed and emerging markets.Bakery applications represent one of the fastest-growing areas of demand, supported by the expanding global bakery industry and rising consumer interest in premium baked goods. Commercial bakeries and home bakers increasingly utilize instant pudding products in cakes, pastries, pie fillings, mousse preparations, dessert toppings, and specialty confectionery items to enhance texture, flavor, and consistency. Foodservice establishments, including cafés, restaurants, hotels, quick-service restaurants, and catering providers, are also expanding their use of instant pudding products due to their labor efficiency, predictable quality, cost-effectiveness, and versatility across diverse menu offerings. The growing popularity of customized desserts and premium bakery products is expected to further stimulate application growth in commercial settings.

End User Insights

Household consumers constitute the largest end-user segment, accounting for approximately 57% of total market demand in 2025. The segment’s dominance is driven by widespread consumer familiarity, ease of preparation, affordability, and growing demand for convenient dessert options. Families, home bakers, and convenience-oriented consumers continue to rely on instant pudding products for everyday dessert preparation, baking applications, and snack consumption. The increasing popularity of home cooking and baking activities, supported by digital recipe platforms and social media food trends, continues to reinforce household demand globally.Commercial bakeries represent the fastest-growing end-user category, benefiting from increasing global demand for premium baked goods, customized desserts, and value-added confectionery products. Instant pudding products provide bakeries with a cost-efficient ingredient that enhances product quality while simplifying production processes. Additionally, hotels, restaurants, catering companies, educational institutions, healthcare facilities, and institutional foodservice operators are increasingly incorporating instant pudding into their offerings due to its scalability, affordability, consistency, and operational efficiency. The expansion of organized foodservice industries worldwide is expected to create significant growth opportunities across commercial end-user segments.

Explore more data points, trends and opportunities Download Free Sample Report

Instant Pudding Market Segmentations

By Product Type

- Instant Pudding Mix

- Ready-to-Eat Pudding Cups

By Flavor Type

- Vanilla

- Chocolate

- Butterscotch/Toffee

- Caramel

- Lemon/Citrus

- Strawberry

- Banana

- Coconut

- Mixed Fruit

- Specialty & Seasonal Flavors

By Sugar Formulation

- Regular Sugar

- Reduced Sugar

- Sugar-Free

- Protein-Enriched/Functional

By Ingredient Profile

- Conventional

- Organic

- Clean Label/Natural

- Gluten-Free

- Plant-Based/Vegan

By Packaging Format

- Sachets/Pouches

- Cartons/Boxes

- Single-Serve Cups

- Bulk Foodservice Packs

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 35% of global revenue in 2025. The United States contributes nearly 28% of worldwide demand, supported by strong household consumption, extensive retail distribution networks, and a deeply established home baking culture. The region benefits from high consumer awareness of convenience foods, widespread availability of branded dessert products, and strong penetration of organized retail channels. Growing demand for healthier dessert alternatives, including sugar-free, reduced-calorie, protein-enriched, and plant-based pudding formulations, continues to drive product innovation. The expansion of e-commerce grocery platforms, rising demand for premium ready-to-eat desserts, and increasing consumer preference for convenient snacking solutions further support regional market growth. Canada continues to demonstrate steady expansion, driven by rising demand for premium dessert products and growing adoption of clean-label and functional food offerings.

Europe

Europe accounts for approximately 28% of global market revenue, with Germany, the United Kingdom, France, Italy, and Spain representing the largest consumer markets. Regional growth is supported by strong dessert consumption traditions, well-developed retail infrastructure, and increasing consumer demand for premium-quality food products. The growing preference for organic, clean-label, and naturally sourced ingredients is encouraging manufacturers to reformulate products and introduce healthier pudding alternatives. Germany remains a major production and consumption hub due to its mature food processing industry and strong bakery sector. Additionally, rising demand for indulgent premium desserts, expanding private-label offerings, and growing interest in sustainable packaging solutions are contributing to market expansion across Western and Northern Europe.

Asia-Pacific

Asia-Pacific accounts for nearly 25% of global demand and represents the fastest-growing regional market, projected to expand at approximately 7% CAGR through 2031. Rapid urbanization, rising disposable incomes, changing dietary habits, and increasing consumption of packaged convenience foods are major drivers supporting regional growth. China leads regional demand due to its large consumer base, expanding middle class, and growing preference for ready-to-prepare dessert products. India is emerging as one of the fastest-growing national markets, supported by increasing westernization of food preferences, rapid growth in modern retail formats, and expanding adoption of packaged dessert mixes among younger consumers. Japan, South Korea, and Australia continue contributing stable demand through mature retail networks, strong convenience food consumption, and growing interest in premium and functional dessert products. The continued expansion of e-commerce and food delivery ecosystems is expected to further accelerate market penetration across the region.

Latin America

Latin America represents approximately 7% of global market revenue, led by Brazil, Mexico, Argentina, and Chile. Market growth is driven by rising disposable incomes, expanding urban populations, increasing penetration of organized retail channels, and growing consumer demand for affordable packaged dessert solutions. The region is witnessing greater adoption of convenience foods as changing lifestyles and increasing workforce participation encourage demand for quick and easy meal and dessert options. Manufacturers are increasingly focusing on value-oriented product offerings, localized flavor innovations, and broader retail distribution strategies to strengthen their market presence. The expansion of supermarket chains and improving cold-chain logistics infrastructure are further supporting regional market development.

Middle East & Africa

The Middle East & Africa region accounts for approximately 5% of global demand and continues to present significant long-term growth opportunities. Market expansion is supported by rapid urbanization, population growth, rising disposable incomes, and the ongoing modernization of retail infrastructure. Saudi Arabia, the United Arab Emirates, South Africa, and Egypt remain key growth markets due to increasing consumer demand for packaged convenience foods and premium imported dessert products. In Gulf Cooperation Council countries, rising expenditure on premium food products, expanding hospitality sectors, and strong demand for international food brands are driving market growth. Across Africa, improvements in food retail infrastructure, growing supermarket penetration, increasing availability of packaged foods, and a rising young consumer population are supporting broader adoption of instant pudding products. Continued investments in food processing, retail development, and distribution networks are expected to enhance market accessibility throughout the forecast period.

Key Players in the Instant Pudding Market

- Kraft Heinz Company

- Dr. Oetker

- Kroger

- Goodman Fielder

- Jotis Foods

- Hy-Vee

- Epicure

- Edlyn Foods

- Bakels Group

- Puratos

- Nestlé

- Archer Daniels Midland (ADM)

- Ingredion Incorporated

- Barry Callebaut

- General Mills