Instant Noodles and Ramen Market Size

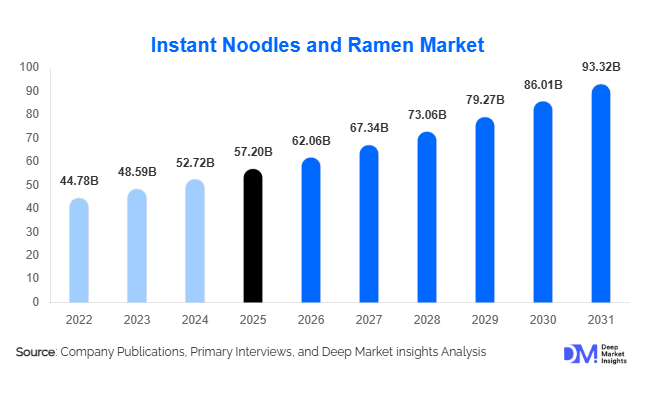

According to Deep Market Insights, the global instant noodles and ramen market size was valued at USD 57.2 billion in 2025 and is projected to grow from USD 62.06 billion in 2026 to reach USD 93.32 billion by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The instant noodles and ramen market growth is primarily driven by rising urbanization, increasing demand for convenient meal solutions, growing adoption of premium and health-focused noodle products, and expanding retail and e-commerce distribution networks worldwide. The category continues to benefit from its affordability, long shelf life, and adaptability across diverse consumer demographics. While Asia-Pacific remains the largest consumer and manufacturing hub, increasing acceptance of Asian cuisine, premium ramen offerings, and functional food innovations are accelerating market growth across North America, Europe, Latin America, and the Middle East & Africa.

Key Market Insights

- Asia-Pacific accounts for nearly 75% of global consumption, led by China, Indonesia, India, Japan, Vietnam, and South Korea.

- Premium and restaurant-style ramen products are growing significantly faster than conventional offerings, supported by changing consumer preferences and premiumization trends.

- Packet noodles remain the dominant packaging format, accounting for more than 60% of global sales due to affordability and extensive retail availability.

- Foodservice applications are emerging as one of the fastest-growing end-use segments, supported by the expansion of ramen restaurants and Asian-themed quick-service concepts.

- Health-focused innovations such as low-sodium, high-protein, gluten-free, and plant-based noodles are reshaping product development strategies.

- E-commerce and quick-commerce channels are becoming increasingly important, enabling manufacturers to reach younger consumers directly while expanding premium product accessibility.

Instant Noodles and Ramen Market Latest Trends

Premiumization and Restaurant-Style Ramen Expansion

Consumer demand for higher-quality convenience foods is accelerating the growth of premium instant noodles and ramen products. Manufacturers are increasingly introducing authentic Japanese, Korean, Chinese, and Southeast Asian flavor profiles with premium ingredients, richer broths, and enhanced packaging formats. Restaurant-inspired ramen kits, gourmet flavor combinations, and chef-developed recipes are attracting middle-income and affluent consumers seeking elevated at-home dining experiences. This trend is particularly strong across North America, Europe, China, Japan, and South Korea, where consumers are willing to pay higher prices for authenticity and superior taste experiences.

Health-Oriented Product Innovation

The industry is witnessing substantial innovation in response to growing health awareness. Companies are launching reduced-sodium formulations, non-fried noodles, high-protein variants, whole-grain products, plant-based alternatives, and fortified noodles containing vitamins, minerals, and functional ingredients. Air-dried noodles are increasingly replacing traditional fried products in premium segments. Manufacturers are also investing in clean-label formulations and sustainable sourcing initiatives to address changing consumer expectations. These innovations are helping the category attract health-conscious consumers who previously viewed instant noodles as nutritionally inferior convenience foods.

Instant Noodles and Ramen Market Drivers

Growing Urbanization and Demand for Convenience Foods

Rapid urbanization continues to support demand for ready-to-prepare meal solutions. Growing populations of students, working professionals, and single-person households are increasingly seeking affordable and convenient food products that require minimal preparation time. Instant noodles provide a practical solution for consumers with busy lifestyles, particularly in densely populated urban centers across Asia-Pacific, Latin America, and Africa. The expansion of modern retail infrastructure further supports market accessibility and consumption growth.

Affordability During Economic Uncertainty

Instant noodles remain one of the most economical meal options globally, making them particularly resilient during periods of inflation, economic slowdown, and consumer spending pressure. Their low unit cost and long shelf life continue to attract value-conscious consumers. During periods of rising food prices, many households increase consumption of affordable packaged foods, supporting steady demand growth. This defensive consumption characteristic has historically enabled the industry to maintain stable performance across economic cycles.

Product Diversification and Flavor Innovation

Manufacturers continue expanding product portfolios through innovative flavors, premium ingredients, regional customization, and functional nutrition enhancements. Spicy Korean ramen, authentic Japanese tonkotsu varieties, Southeast Asian seafood flavors, and plant-based alternatives are attracting new consumer segments globally. This diversification strategy allows brands to expand beyond traditional value-oriented positioning and increase average selling prices while improving profitability.

Instant Noodles and Ramen Market Restraints

Health and Nutritional Concerns

Traditional instant noodles continue to face criticism related to sodium content, preservatives, and perceived nutritional limitations. Growing consumer awareness regarding healthy eating habits may restrict demand growth among health-conscious demographics. Regulatory scrutiny surrounding nutritional labeling and sodium reduction initiatives is also increasing across several developed markets. Manufacturers must continue investing in healthier formulations to address these concerns and maintain long-term consumer acceptance.

Volatility in Raw Material and Packaging Costs

Fluctuating prices of wheat flour, palm oil, seasonings, packaging materials, and logistics services remain significant operational challenges. Supply chain disruptions and agricultural commodity price fluctuations can directly impact manufacturing costs and profit margins. Rising sustainability requirements for packaging materials further increase production expenses, particularly for manufacturers operating in highly competitive price-sensitive markets.

Instant Noodles and Ramen Industry Key Opportunities

Expansion Across Emerging Markets

Emerging economies across Africa, South Asia, and Latin America present substantial growth opportunities. Rising urban populations, increasing disposable incomes, and expanding retail infrastructure are driving packaged food adoption in countries such as Nigeria, Kenya, Ethiopia, Bangladesh, Pakistan, Peru, and Colombia. Local manufacturing investments can improve affordability while reducing supply chain costs. Market participants establishing early production and distribution networks in these regions are expected to capture significant long-term growth opportunities.

Premium Health and Functional Noodle Categories

The growing consumer focus on wellness presents opportunities for manufacturers to introduce premium functional noodle products. High-protein formulations, fortified noodles, plant-based variants, probiotic-enhanced products, and low-glycemic alternatives can command premium pricing while attracting health-conscious consumers. These categories are expected to grow significantly faster than conventional products over the forecast period, offering higher margins and stronger brand differentiation.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 57.20 Billion |

| Market Size in 2026 | USD 62.06 Billion |

| Market Size in 2031 | USD 93.32 Billion |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fried instant noodles continue to dominate the global market, contributing approximately 58% of total revenue. This leadership is primarily driven by cost-efficient large-scale production processes, long shelf stability, and strong historical consumer familiarity across both developed and emerging economies. Their affordability and ease of preparation make them a staple in price-sensitive markets, particularly where packaged food penetration is still expanding. The segment’s leading growth driver remains mass affordability combined with widespread retail accessibility, enabling consistent consumption across income groups and geographies.Air-dried and non-fried noodles represent the fastest-growing product category, supported by the rising shift toward healthier eating patterns and consumer demand for low-fat, minimally processed food alternatives. Fresh-pack and frozen ramen offerings are gaining traction in developed markets where consumers increasingly seek restaurant-quality dining experiences at home, supported by cold-chain logistics improvements and premium product positioning. Ready-to-eat noodle meals are also expanding at a strong pace, fueled by urban lifestyles, time-constrained consumers, and advancements in food preservation and packaging technologies that extend product freshness without compromising quality.

Flavor Insights

Chicken flavor remains the most dominant category globally, accounting for nearly 29% of total sales, largely due to its universal taste acceptance, adaptability across cuisines, and affordability in formulation. The leading growth driver for this segment is its broad cultural compatibility, allowing manufacturers to scale across diverse regions without significant product adaptation.Beef and seafood flavors maintain strong performance in Asia-Pacific and North America, supported by established culinary preferences and the popularity of protein-rich taste profiles. Spicy variants are experiencing exceptional global momentum, driven by the international rise of Korean and Southeast Asian food culture, social media influence, and consumer preference for bold, high-intensity taste experiences. Regional and ethnic flavors inspired by Thai, Vietnamese, Japanese, and Chinese culinary traditions are expanding rapidly as globalization and travel exposure continue to shape consumer palates. Premium gourmet flavor innovations, often incorporating artisanal seasoning blends and specialty ingredients, are contributing significantly to market premiumization and brand differentiation strategies.

Packaging Format Insights

Packet noodles dominate the packaging landscape with approximately 64% market share, primarily driven by their affordability, lightweight structure, and widespread distribution across both modern retail chains and traditional trade networks. The leading driver of this segment is cost efficiency at scale, enabling manufacturers to maintain price competitiveness while ensuring high-volume distribution in both urban and rural markets.Cup noodles continue to gain strong traction among urban consumers due to their portability, ease of preparation, and suitability for on-the-go consumption, particularly in densely populated metropolitan areas across Asia-Pacific, North America, Japan, and South Korea. Bowl and tray formats are increasingly positioned within the premium segment, offering improved presentation, portion control, and enhanced sensory experience, thereby aligning with rising consumer expectations for convenience combined with quality. Multipack formats are also expanding steadily, driven by household stocking behavior, value-oriented purchasing patterns, and increased supermarket penetration in both emerging and developed economies.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channel, accounting for approximately 43% of global sales. Their dominance is driven by wide product assortment, strong brand visibility, and high consumer footfall, making them a primary destination for both planned and impulse purchases. The key growth driver for this channel is organized retail expansion, particularly in emerging economies where modern trade infrastructure continues to develop rapidly.Convenience stores play a crucial role in urban consumption ecosystems, benefiting from extended operating hours and proximity-based purchasing behavior. Traditional grocery stores continue to maintain relevance in rural and semi-urban regions, especially in developing markets where informal retail networks remain dominant. Online retail is emerging as one of the fastest-growing channels globally, fueled by the expansion of e-commerce platforms, quick-commerce delivery models, and direct-to-consumer strategies that enhance product accessibility, particularly for premium and niche noodle variants.

End-Use Insights

Household consumption remains the largest end-use segment, accounting for approximately 72% of global demand. This dominance is driven by the product’s role as an affordable meal substitute, snack option, and convenient food solution across diverse demographic groups. The primary growth driver for household consumption is increasing urbanization combined with demand for quick, cost-effective meal solutions in fast-paced lifestyles.Foodservice applications represent the fastest-growing end-use segment, supported by the rapid expansion of ramen restaurants, Asian quick-service chains, and institutional catering services. Demand is further strengthened by the integration of instant noodles into travel, hospitality, military provisioning, and emergency food supply systems, where long shelf life and ease of preparation provide significant logistical advantages. Industrial meal providers are also incorporating instant noodles into structured employee meal programs, reinforcing their role in large-scale food distribution systems.

Consumer Group Insights

Working professionals represent the largest consumer group, accounting for approximately 34% of global consumption, driven by time constraints, urban lifestyles, and a strong preference for quick and affordable meal solutions. The leading driver within this segment is convenience-oriented consumption behavior, particularly in high-density urban economies.Students continue to represent a foundational consumer base due to affordability and ease of preparation, while family households maintain strong demand, particularly in emerging markets where instant noodles are integrated into daily dietary routines. Health-conscious consumers are increasingly influencing market evolution through demand for premium variants such as high-protein, low-sodium, and plant-based formulations. Additionally, travelers, military personnel, and emergency relief organizations contribute to stable institutional demand, leveraging the product’s portability, shelf stability, and low storage requirements.

Explore more data points, trends and opportunities Download Free Sample Report

Instant Noodles and Ramen Market Segmentations

By Product Type

- Fried Instant Noodles

- Air-Dried / Non-Fried Instant Noodles

- Fresh-Pack Instant Ramen

- Frozen Instant Ramen

- Ready-to-Eat (RTE) Instant Noodle Meals

By Flavor Category

- Chicken

- Beef

- Seafood

- Pork

- Vegetable

- Spicy/Hot Variants

- Regional/Ethnic Flavors

- Premium Gourmet Flavors

By Raw Material

- Wheat-Based

- Rice-Based

- Oat-Based

- Multigrain-Based

- Legume-Based

- Other Specialty Grain-Based

By Packaging Format

- Packet/Bag Noodles

- Cup Noodles

- Bowl Noodles

- Tray-Based Noodles

- Multipack Formats

By Price Tier

- Economy

- Mid-Range

- Premium

- Super-Premium/Artisanal

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global instant noodles and ramen market with approximately 75% share, driven by deeply embedded consumption habits, strong domestic production ecosystems, and continuous product innovation. China leads as the largest individual market, accounting for nearly 36% of global consumption, supported by large-scale manufacturing capacity, urban population density, and strong retail penetration. The leading growth driver in China is rapid urban lifestyle acceleration combined with mass-market affordability. Indonesia remains one of the highest per-capita consumers globally, supported by cultural integration of instant noodles into daily diets, while India is witnessing rapid expansion driven by urbanization, rising disposable incomes, and increasing penetration of organized retail. Japan and South Korea continue to drive premiumization trends through innovation, premium ramen culture, and high-value product diversification. Vietnam and Thailand are strengthening their positions as major export-oriented manufacturing hubs, supported by competitive production costs and expanding global supply chains.

North America

North America accounts for approximately 7% of global revenue, with the United States leading regional consumption. The primary growth driver is increasing multicultural food adoption, particularly the rising popularity of Asian cuisine among younger demographics. Premium ramen offerings and gourmet instant noodle products are expanding rapidly as consumers trade up from traditional convenience foods. Canada is experiencing growing demand for imported premium noodles, while foodservice operators are expanding ramen-centric restaurant concepts across major cities. E-commerce grocery platforms and social media-driven food trends are further accelerating category awareness and consumption.

Europe

Europe represents approximately 5% of global consumption, with key markets including the United Kingdom, Germany, France, the Netherlands, and Poland. Growth is primarily driven by increasing exposure to Asian culinary culture, expanding immigrant populations, and shifting consumer preferences toward convenient meal solutions. The leading driver in Europe is premiumization combined with health-conscious product adoption, as consumers increasingly seek low-fat, organic, and high-quality instant noodle options. Supermarkets across the region are expanding international food aisles, improving accessibility and visibility of diverse noodle offerings.

Latin America

Brazil and Mexico dominate the Latin American instant noodle market, supported by affordability-driven consumption patterns and growing urban populations. The primary growth driver is rising demand for low-cost meal solutions amid expanding urbanization and economic diversity. Peru, Colombia, and Chile are emerging as high-potential growth markets, driven by improving disposable incomes and evolving dietary habits. Investments in local production facilities are enhancing supply chain efficiency and product availability, supporting long-term market penetration and regional expansion.

Middle East & Africa

The Middle East and Africa collectively account for approximately 7% of global demand, with Nigeria leading as Africa’s largest and fastest-growing market. Growth is primarily driven by rapid population expansion, urbanization, and strong demand for affordable, shelf-stable food products. South Africa, Egypt, Kenya, Saudi Arabia, and the United Arab Emirates are also witnessing increasing consumption supported by retail modernization and rising expatriate populations. The leading regional driver is expanding retail infrastructure combined with increasing demand for low-cost convenience foods, particularly in densely populated urban centers.

Key Players in the Instant Noodles and Ramen Market

- Nissin Foods Holdings

- Tingyi (Master Kong)

- Uni-President Enterprises

- Nestlé

- Indofood Sukses Makmur

- Toyo Suisan

- Acecook Vietnam

- ITC Limited

- Ottogi Corporation

- Nongshim

- Sanyo Foods

- Vietnam Food Industries

- MAMA Products

- Capital Foods

- Tat Hui Foods