Industrial Workwear Market Size

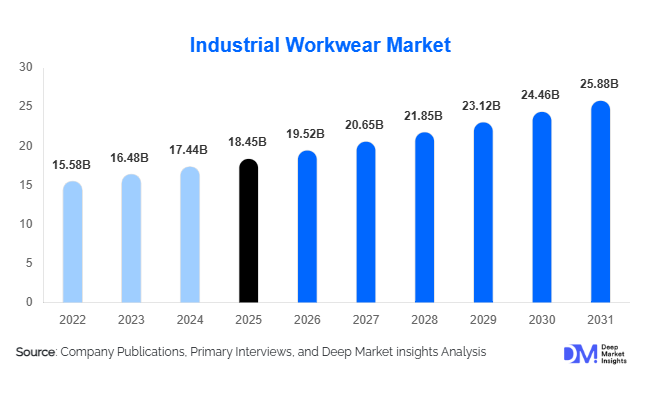

According to Deep Market Insights, the global industrial workwear market size was valued at USD 18.45 billion in 2025 and is projected to grow from USD 19.52 billion in 2026 to reach USD 25.88 billion by 2031, expanding at a CAGR of 5.8% during the forecast period (2026–2031). The industrial workwear market is experiencing growth primarily driven by increasing industrial safety regulations, rising infrastructure and manufacturing investments, and the growing adoption of advanced protective clothing technologies in hazardous working environments.

Key Market Insights

- Industrial safety regulations are becoming increasingly stringent globally, driving mandatory adoption of certified protective clothing across construction, oil & gas, manufacturing, mining, and chemical industries.

- Asia-Pacific dominates the global industrial workwear market, supported by strong manufacturing output, rapid industrialization, and large-scale infrastructure projects across China, India, Vietnam, and Southeast Asia.

- Smart and connected workwear technologies are gaining traction, including RFID-enabled garments, wearable sensors, biometric monitoring, and IoT-integrated protective apparel.

- Sustainable industrial workwear is emerging as a major industry trend, with manufacturers increasingly utilizing recycled polyester, bio-based textiles, and low-carbon production systems.

- Flame-resistant and high-visibility clothing remain the fastest-growing product categories, driven by stricter workplace compliance standards in energy, utilities, mining, and heavy manufacturing sectors.

- Uniform rental and managed workwear services are expanding globally, enabling industrial employers to outsource garment maintenance, compliance management, and inventory tracking.

Industrial Workwear Market Trends

Smart Protective Clothing and Connected Workwear Adoption

The industrial workwear market is increasingly transitioning toward smart protective clothing integrated with wearable technologies and connected safety systems. Industrial employers are deploying RFID-enabled garments, biometric monitoring sensors, GPS tracking systems, and real-time environmental hazard detection technologies to improve worker safety and operational productivity. Smart workwear solutions capable of monitoring worker fatigue, temperature exposure, toxic gas levels, and movement patterns are gaining significant adoption across mining, oil & gas, utilities, and construction industries. These technologies enable faster emergency response, improve workforce monitoring, and reduce workplace accident risks. Manufacturers are also investing heavily in lightweight ergonomic smart fabrics that enhance worker comfort without compromising protection standards. The growing integration of IoT platforms and industrial digitalization initiatives is expected to further accelerate demand for connected industrial workwear over the forecast period.

Sustainable and Eco-Friendly Workwear Manufacturing

Sustainability has emerged as a critical trend reshaping the global industrial workwear industry. Corporate ESG goals, environmental regulations, and growing customer preference for low-carbon procurement are driving manufacturers toward eco-friendly production methods and sustainable textile materials. Industrial workwear companies are increasingly adopting recycled polyester, organic cotton, biodegradable fibers, and water-efficient dyeing technologies to reduce environmental impact. Circular workwear programs focused on garment recycling, refurbishment, and reuse are also gaining momentum among large industrial employers seeking to minimize textile waste. European and North American buyers are particularly prioritizing sustainability certifications and supply chain transparency while selecting industrial apparel suppliers. Additionally, manufacturers are integrating renewable energy systems and automated low-emission production facilities into textile manufacturing operations to align with global sustainability targets.

Industrial Workwear Market Drivers

Stringent Workplace Safety Regulations

The implementation of stricter occupational health and safety regulations remains one of the primary drivers supporting industrial workwear market growth globally. Regulatory authorities such as OSHA in the United States, EU-OSHA in Europe, and industrial safety agencies across Asia-Pacific are enforcing rigorous workplace protection standards for hazardous industries. Employers operating in sectors including construction, manufacturing, oil & gas, mining, chemicals, and utilities are increasingly required to provide certified protective apparel that complies with flame resistance, chemical protection, high-visibility, and anti-static performance standards. Rising penalties associated with workplace accidents and non-compliance are compelling organizations to invest heavily in advanced industrial workwear solutions. Additionally, multinational corporations are implementing global worker safety programs that standardize protective clothing procurement across international operations, further boosting market demand.

Rapid Industrialization and Infrastructure Expansion

Growing industrialization and infrastructure development across emerging economies are significantly accelerating demand for industrial workwear products. Governments in countries including China, India, Saudi Arabia, Indonesia, Vietnam, and the UAE are investing heavily in transportation infrastructure, industrial corridors, energy projects, logistics facilities, and manufacturing hubs. These projects generate substantial demand for protective apparel among construction workers, engineers, technicians, and industrial laborers operating in high-risk environments. The expansion of semiconductor plants, electric vehicle factories, renewable energy facilities, and petrochemical complexes is also contributing to industrial workforce growth globally. Rising urbanization and export-driven manufacturing activity continue to support long-term demand for certified industrial workwear solutions.

Industrial Workwear Market Restraints

Raw Material Price Volatility

Industrial workwear manufacturers remain highly exposed to fluctuations in raw material prices, particularly cotton, polyester, aramid fibers, and specialty synthetic textiles. Changes in crude oil prices, global supply chain disruptions, transportation costs, and geopolitical instability directly impact textile production costs and profit margins. Price volatility creates challenges for manufacturers attempting to maintain competitive pricing while complying with stringent quality and safety standards. Rising energy costs and inflationary pressures have also increased manufacturing expenses across global textile supply chains, affecting both premium and mid-range workwear producers.

Competition from Low-Cost Unorganized Suppliers

The presence of low-cost regional and unorganized manufacturers remains a major challenge within the industrial workwear market. In several developing economies, uncertified protective garments are sold at significantly lower prices compared to globally compliant workwear products. These low-quality alternatives reduce pricing power for established manufacturers that invest heavily in safety certifications, advanced textile technologies, and regulatory compliance. Counterfeit protective apparel also raises concerns regarding worker safety and operational reliability, particularly in cost-sensitive industrial sectors. This competitive pressure continues to impact premium manufacturers seeking to expand market penetration across emerging regions.

Industrial Workwear Market Opportunities

Expansion of Smart Workwear Technologies

The growing adoption of Industry 4.0 technologies presents major opportunities for industrial workwear manufacturers to develop connected protective apparel solutions. Smart garments equipped with biometric sensors, heat monitoring systems, fatigue detection, and real-time communication features are becoming increasingly valuable across hazardous industrial environments. Industries such as mining, energy, utilities, and logistics are prioritizing advanced safety monitoring systems to improve workforce management and reduce accident risks. Manufacturers capable of integrating IoT-enabled technologies into industrial workwear are expected to benefit from premium pricing opportunities and long-term institutional contracts.

Growth in Sustainable and Circular Workwear Solutions

The rising focus on sustainability and corporate ESG initiatives is creating strong opportunities for eco-friendly industrial workwear manufacturers. Large multinational companies are increasingly demanding recycled fabrics, low-carbon manufacturing processes, and circular garment management programs to support sustainability targets. Industrial employers are also adopting rental and managed uniform services that improve garment reuse and reduce textile waste generation. Manufacturers investing in sustainable fabric innovation, renewable energy production systems, and transparent supply chain practices are likely to gain significant competitive advantages in global procurement contracts.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.45 Billion |

| Market Size in 2026 | USD 19.52 Billion |

| Market Size in 2031 | USD 25.88 Billion |

| CAGR | 5.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Workwear apparel dominates the industrial workwear market, accounting for the majority of global revenues due to widespread usage across construction, manufacturing, utilities, and oil & gas industries. Flame-resistant apparel and high-visibility garments represent the fastest-growing categories within industrial apparel as regulatory standards continue to tighten globally. Industrial footwear also maintains strong demand, particularly safety shoes and puncture-resistant boots used across heavy manufacturing and mining operations. Protective gloves are witnessing rising adoption due to increasing awareness regarding hand injury prevention in chemical processing and industrial assembly environments. Smart wearable garments and connected protective clothing are emerging as premium product segments, particularly across technologically advanced industrial sectors in North America and Europe.

Protection Type Insights

Flame-resistant and thermal protective workwear represents one of the largest segments within the industrial workwear market due to rising demand from oil & gas, utilities, mining, and petrochemical industries. High-visibility workwear continues to expand rapidly across transportation infrastructure and construction projects where worker visibility is critical for operational safety. Chemical-resistant protective clothing remains essential across pharmaceutical manufacturing, chemical processing, and hazardous waste management industries. Waterproof and weather-resistant workwear products are also gaining traction in outdoor industrial operations, particularly within construction, agriculture, and logistics sectors operating under extreme environmental conditions.

Material Type Insights

Polyester blends account for a significant share of global industrial workwear demand due to their durability, moisture resistance, and cost efficiency. Cotton-based fabrics remain widely utilized for general industrial uniforms because of comfort and breathability advantages. Aramid fibers such as Nomex and Kevlar are experiencing rapid growth owing to superior flame resistance and thermal protection capabilities required in hazardous industrial applications. Sustainable textile materials, including recycled polyester and bio-based fabrics, are emerging as fast-growing segments driven by environmental regulations and corporate sustainability commitments. Manufacturers are also increasingly utilizing laminated and coated fabrics to improve chemical resistance and weather protection performance.

Distribution Channel Insights

Direct B2B procurement remains the leading distribution channel within the industrial workwear market as large industrial employers increasingly establish long-term supply agreements with manufacturers. Industrial distributors and specialty safety equipment providers continue to play an important role by offering technical consultation, compliance expertise, and localized inventory management. E-commerce and digital procurement platforms are rapidly gaining popularity, particularly among SMEs seeking cost-effective purchasing options and transparent pricing models. Uniform rental and managed service providers are also expanding significantly by offering garment maintenance, laundering, replacement, and compliance management solutions for large industrial organizations.

End-Use Industry Insights

Manufacturing remains the largest end-use industry for industrial workwear globally due to extensive worker populations across automotive, machinery, electronics, and heavy engineering sectors. Construction represents another major demand segment supported by global infrastructure investments and urban development projects. The oil and gas, as well as petrochemical industries, continue to drive demand for premium flame-resistant and chemically protective apparel due to high workplace hazard exposure. The pharmaceutical and healthcare industries are emerging as fast-growing end-use segments due to the increasing demand for contamination-resistant protective clothing and biological safety garments. Logistics and warehousing sectors are also witnessing growing demand for high-visibility apparel as global e-commerce and supply chain operations expand.

Explore more data points, trends and opportunities Download Free Sample Report

Industrial Workwear Market Segmentations

By Product Type

- Workwear Apparel

- Industrial Footwear

- Protective Gloves

- Head, Eye & Face Protection

- Respiratory & Full-Body Protection

By Protection Type

- Flame-Resistant Workwear

- High-Visibility Workwear

- Chemical Protective Workwear

- Mechanical Protective Workwear

- Anti-Static & Electrical Arc Protection Workwear

- Waterproof & Weather-Resistant Workwear

By Material Type

- Cotton-Based Fabrics

- Polyester & Polyester Blends

- Aramid Fibers

- FR-Treated Fabrics

- Sustainable & Recycled Fabrics

By Distribution Channel

- Direct B2B Sales

- Industrial Distributors

- Specialty Safety Equipment Retailers

- E-Commerce Platforms

- Uniform Rental & Managed Services

By End-Use Industry

- Manufacturing

- Construction & Infrastructure

- Oil & Gas

- Mining

- Chemicals & Petrochemicals

- Transportation & Logistics

- Utilities & Power Generation

- Healthcare & Pharmaceuticals

Regional Insights

North America

North America accounts for a substantial share of the global industrial workwear market, supported by strict occupational safety standards and strong industrial activity across the United States and Canada. The U.S. remains the largest regional market due to extensive demand from manufacturing, oil & gas, aerospace, construction, and utilities sectors. High adoption of premium flame-resistant and smart protective clothing technologies continues to strengthen regional market growth. Canada contributes significantly through mining, energy, and infrastructure development projects requiring advanced industrial safety apparel.

Europe

Europe represents a mature but highly innovative industrial workwear market led by Germany, France, the United Kingdom, and Italy. Strong regulatory compliance standards, industrial automation investments, and sustainability-focused procurement strategies are supporting demand for advanced protective clothing solutions. European manufacturers and industrial buyers are increasingly prioritizing recycled materials, low-emission production systems, and circular garment management programs. Automotive manufacturing, chemicals, and engineering industries remain major contributors to regional industrial workwear consumption.

Asia-Pacific

Asia-Pacific dominates the global industrial workwear market, accounting for the largest revenue share globally. China remains the leading country due to its massive manufacturing ecosystem, infrastructure development activity, and industrial workforce size. India is among the fastest-growing markets supported by rapid industrialization, expanding infrastructure projects, and government manufacturing initiatives such as “Make in India.” Southeast Asian countries including Vietnam and Indonesia are also witnessing strong growth due to export manufacturing expansion and rising workplace safety awareness. Increasing industrial investments across renewable energy, semiconductors, and logistics infrastructure continue to strengthen regional demand.

Latin America

Latin America is experiencing steady industrial workwear demand growth led by Brazil and Mexico. Brazil’s mining, manufacturing, agriculture, and oil industries generate consistent demand for industrial protective apparel. Mexico is emerging as a key market due to strong export manufacturing growth linked to North American supply chains. Industrial safety compliance improvements and foreign manufacturing investments are further supporting regional market expansion.

Middle East & Africa

The Middle East & Africa region represents one of the fastest-growing industrial workwear markets globally. Saudi Arabia and the UAE are investing heavily in industrial diversification, infrastructure megaprojects, petrochemical facilities, and logistics infrastructure under long-term economic transformation programs. South Africa remains an important market due to strong mining and heavy industrial activity. Demand for flame-resistant clothing, chemical protection apparel, and high-visibility garments continues to expand rapidly across the region.

Key Players in the Industrial Workwear Market

- Honeywell International

- 3M

- Ansell

- DuPont

- Kimberly-Clark

- Lakeland Industries

- Aramark

- Carhartt

- Alsico Group

- Fristads

- Sioen Industries

- VF Corporation

- UniFirst

- Cintas

- Delta Plus Group