Gum Base Candy Market Size

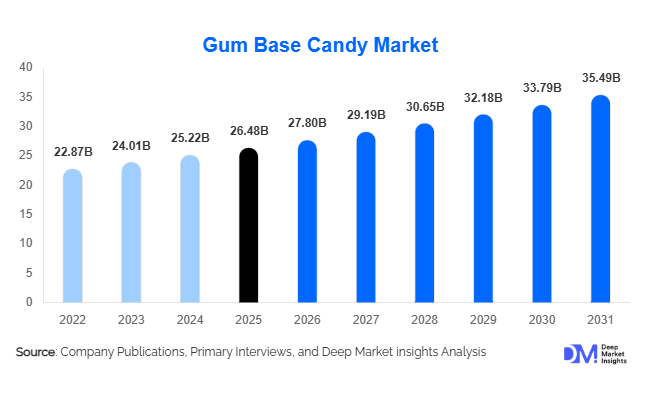

According to Deep Market Insights, the global gum base candy market size was valued at USD 26.48 billion in 2025 and is projected to grow from USD 27.80 billion in 2026 to reach USD 35.49 billion by 2031, expanding at a CAGR of 5.0% during the forecast period (2026–2031). The gum base candy market growth is primarily driven by increasing consumer preference for sugar-free confectionery, rising demand for functional chewing gum products, and continuous innovation in flavors, packaging, and natural gum base formulations. The industry is also benefiting from growing demand for oral care products, wellness-oriented confectionery, and premium snacking solutions across both developed and emerging markets.

Key Market Insights

- Sugar-free gum products account for nearly half of global market revenues, driven by growing health consciousness and increasing awareness regarding dental hygiene.

- Functional gum products containing vitamins, caffeine, probiotics, and oral care ingredients are expanding rapidly, creating new opportunities beyond traditional confectionery applications.

- North America dominates the global market, accounting for approximately 35% of total revenues due to high per-capita gum consumption and strong premium product demand.

- Asia-Pacific is the fastest-growing regional market, supported by rising disposable incomes, urbanization, and expanding organized retail infrastructure.

- Sustainability initiatives are reshaping product development, with manufacturers increasingly investing in biodegradable gum bases and environmentally friendly packaging.

- E-commerce and direct-to-consumer channels are becoming important distribution platforms, particularly for premium and functional gum products.

Gum Base Candy Market Latest Trends

Functional and Wellness-Based Gum Products Gaining Traction

The global gum base candy industry is increasingly transitioning toward functional confectionery products that offer health benefits beyond traditional taste and refreshment. Manufacturers are introducing chewing gums infused with vitamins, caffeine, probiotics, herbal extracts, and oral health ingredients to address growing consumer demand for convenient wellness solutions. Functional gum products are particularly popular among millennials and working professionals seeking portable nutritional supplements and energy products. Nicotine replacement chewing gums and digestive health formulations are also gaining commercial acceptance, broadening the addressable market for gum base candy manufacturers.

Sustainable and Natural Gum Bases Becoming Industry Priorities

Environmental concerns surrounding synthetic gum disposal have accelerated investments in biodegradable and plant-based gum base technologies. Companies are increasingly utilizing natural ingredients such as chicle and plant resins to develop eco-friendly products that appeal to environmentally conscious consumers. The trend is particularly prominent in Europe and North America, where sustainability considerations are increasingly influencing purchasing decisions. Manufacturers are also reducing plastic packaging and implementing recyclable materials to strengthen their environmental credentials and comply with evolving regulatory standards.

Gum Base Candy Market Drivers

Growing Demand for Sugar-Free Confectionery Products

Rising concerns regarding obesity, diabetes, and oral health have significantly increased consumer preference for sugar-free chewing gum products. Dental associations across numerous countries recommend sugar-free chewing gum as a tool for maintaining oral hygiene and stimulating saliva production. Consequently, sugar-free products accounted for approximately 48% of global gum base candy revenues in 2025 and continue to gain market share across both developed and emerging markets.

Rapid Expansion of Functional Confectionery Applications

The increasing popularity of functional foods and nutraceutical products has created significant opportunities for gum base candy manufacturers. Functional chewing gum serves as an efficient delivery mechanism for vitamins, caffeine, minerals, and herbal ingredients due to its convenience and relatively rapid absorption properties. This trend has encouraged manufacturers to diversify product portfolios and move beyond conventional confectionery offerings.

Premiumization and Continuous Product Innovation

Manufacturers are increasingly focusing on premium formulations, innovative flavors, and superior packaging designs to attract consumers seeking differentiated confectionery experiences. Premium chewing gums incorporating natural sweeteners, advanced flavor encapsulation technologies, and functional ingredients command significantly higher prices and contribute positively to market value growth.

Gum Base Candy Market Restraints

Environmental Concerns Regarding Gum Waste

Chewing gum litter remains a significant environmental challenge globally. Municipal authorities spend considerable resources on removing discarded gum from public spaces, increasing pressure on manufacturers to develop biodegradable products. Environmental concerns and potential regulations regarding gum disposal could impact market growth over the long term.

Volatility in Raw Material Prices

Fluctuations in prices of sweeteners, flavor compounds, packaging materials, and gum base ingredients continue to create cost pressures for manufacturers. Supply chain disruptions and inflationary conditions have increased production costs, reducing profit margins and potentially impacting pricing strategies across the industry.

Gum Base Candy Industry Key Opportunities

Expansion of Functional and Nutraceutical Gum Products

The functional confectionery market is growing considerably faster than traditional confectionery segments, creating significant opportunities for manufacturers to introduce vitamin-enriched, energy-enhancing, stress-relief, and digestive health chewing gums. Functional gums are increasingly viewed as convenient wellness products and are expected to become an important growth driver during the forecast period.

Penetration into Emerging Markets

Emerging economies such as India, Indonesia, Vietnam, Saudi Arabia, and Brazil continue to exhibit relatively low per-capita gum consumption compared with developed countries. Rising disposable incomes, rapid urbanization, and increasing availability of modern retail channels create substantial opportunities for manufacturers to expand their consumer base. Localized flavor innovations and affordable packaging formats are expected to accelerate market penetration.

Sustainable Gum Base Innovation

The development of biodegradable gum bases and natural formulations presents a substantial opportunity for both established companies and new entrants. Sustainability-focused products can command premium pricing and improve brand differentiation while helping manufacturers address growing environmental concerns and evolving regulatory expectations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 26.48 Billion |

| Market Size in 2026 | USD 27.80 Billion |

| Market Size in 2031 | USD 35.49 Billion |

| CAGR | 5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Chewing gum continues to dominate the global gum base candy market and accounted for nearly 72% of total market revenues in 2025. The segment's leadership is primarily driven by its widespread consumer acceptance, high purchase frequency, strong penetration across both developed and emerging markets, and continuous product innovation in flavor and functional formulations. Among product categories, sugar-free chewing gum represents the largest sub-segment, benefiting from increasing consumer awareness regarding oral health, sugar reduction, and preventive dental care. The growing prevalence of lifestyle-related health concerns, including obesity and diabetes, has further accelerated the shift toward sugar-free formulations, encouraging manufacturers to expand their portfolios with xylitol-based and low-calorie products.Bubble gum continues to maintain significant demand, particularly among younger demographics and family-oriented consumers. The segment remains highly popular across Asia-Pacific and Latin America, where affordability, flavor diversity, and strong cultural preferences for confectionery products support sustained consumption. Manufacturers continue to introduce innovative flavors, colorful packaging, and limited-edition products to maintain consumer engagement and encourage repeat purchases.Specialty gum products incorporating herbal extracts, botanical ingredients, and naturally derived sweeteners are also gaining traction among premium consumers seeking healthier confectionery alternatives. The growing demand for clean-label products, plant-based ingredients, and sustainable formulations is expected to further diversify product offerings and stimulate innovation across the global gum base candy industry.

Gum Base Composition Insights

Synthetic gum bases accounted for approximately 74% of the global market in 2025 and continue to represent the largest composition segment due to their superior cost efficiency, formulation consistency, and scalability in mass production. The segment's leadership is primarily supported by manufacturers' preference for standardized ingredients that provide stable texture, extended shelf life, and efficient processing capabilities. Synthetic gum bases also enable manufacturers to achieve consistent product performance while maintaining competitive pricing across high-volume production environments.Despite the dominance of synthetic formulations, natural gum bases are steadily gaining traction as sustainability considerations increasingly influence consumer purchasing decisions. Consumers are becoming more aware of environmental concerns associated with conventional chewing gum ingredients, prompting manufacturers to explore plant-derived alternatives and biodegradable formulations. Growing demand for clean-label and naturally sourced confectionery products is expected to further support the adoption of natural gum bases.Hybrid formulations that combine synthetic and natural ingredients are also becoming increasingly popular as manufacturers seek to balance performance characteristics with environmental considerations and cost efficiency. Such formulations offer improved elasticity and shelf stability while addressing consumer demand for more sustainable products. Moreover, increasing investments in biodegradable gum base technologies and sustainable raw material sourcing are expected to significantly reshape the competitive landscape over the coming decade, creating new opportunities for innovation and product differentiation.

Flavor Category Insights

Mint and peppermint flavors dominate the global gum base candy market, accounting for approximately 39% of total demand in 2025. The segment's leadership is primarily driven by the strong association between mint flavors and breath freshening, oral hygiene, and everyday wellness benefits. Consumers frequently perceive mint-flavored chewing gum as a convenient solution for maintaining fresh breath and improving oral cleanliness, resulting in consistently high consumption across all age groups and geographic regions.Fruit-flavored gum products continue to maintain substantial market share and remain particularly popular among younger consumers and emerging markets. The category benefits from extensive flavor variety, affordable pricing, and strong appeal among children and teenagers. Increasing disposable incomes and rising confectionery consumption in developing economies continue to support demand for fruit-based chewing gum products.Novelty and mixed flavors are increasingly being introduced to attract younger demographics and stimulate repeat purchases through continuous product innovation. Manufacturers are focusing on unique taste combinations, seasonal offerings, and limited-edition flavors to strengthen brand engagement and differentiate their products in highly competitive markets.Furthermore, dessert-inspired, botanical, and herbal flavors are contributing to premiumization strategies adopted by major manufacturers. The increasing consumer preference for sophisticated flavor experiences and premium confectionery products is encouraging the development of differentiated offerings that command higher margins and appeal to health-conscious and affluent consumers.

Distribution Channel Insights

Supermarkets and hypermarkets accounted for approximately 33% of global gum base candy sales in 2025, making them the leading distribution channel. The segment's dominance is primarily attributable to extensive product visibility, broad consumer reach, large shelf space allocation, and consumers' preference for one-stop shopping experiences. These retail formats enable manufacturers to introduce new products effectively while supporting impulse purchases through strategic product placement and promotional activities.Convenience stores remain an essential distribution channel for chewing gum products and continue to generate significant sales volumes, particularly in developed markets. The channel's importance stems from the impulse-driven nature of gum purchases and the convenience of immediate product accessibility. High foot traffic in urban areas and transportation hubs further strengthens the position of convenience stores within the market.Online retail and direct-to-consumer channels are experiencing rapid growth, particularly for premium, functional, and specialty gum products. E-commerce platforms allow manufacturers to target niche consumer segments more effectively, offer personalized product recommendations, and introduce subscription-based purchasing models. Digital channels also provide opportunities for direct consumer engagement, data-driven marketing strategies, and efficient product launches, which are expected to support long-term growth across the market.

Consumer Demographic Insights

Adult consumers represented the largest demographic segment in 2025, accounting for approximately 52% of global market demand. The segment's leadership is primarily driven by increasing awareness regarding oral health, the growing popularity of functional ingredients, and rising demand for wellness-oriented products that offer benefits beyond traditional confectionery consumption. Adults increasingly prefer sugar-free and functional chewing gum products that support fresh breath, stress management, energy enhancement, and digestive health.Teenagers continue to represent an important consumer base for flavored and novelty chewing gum products, supported by strong preferences for innovative flavors, attractive packaging, and social consumption trends. Manufacturers continue to target this demographic through product differentiation and experiential marketing initiatives.Children's demand remains a key contributor to bubble gum sales globally, particularly in emerging economies where youthful population structures and increasing confectionery consumption continue to support market expansion. Meanwhile, senior consumers are increasingly adopting sugar-free and functional chewing gums for oral care, dry mouth management, and digestive health applications, creating new opportunities for manufacturers to develop age-specific formulations and expand their consumer base.

End-Use Insights

Retail consumer consumption dominates the global gum base candy market and accounted for nearly 80% of total demand in 2025. The segment's leadership is primarily driven by the widespread popularity of chewing gum as an affordable, convenient, and frequently consumed confectionery product across diverse consumer demographics and geographic markets. Continuous product innovation, extensive retail availability, and high impulse purchasing behavior further reinforce the dominance of retail consumption.Healthcare and pharmaceutical applications represent one of the fastest-growing end-use segments due to increasing demand for nicotine replacement therapies, vitamin delivery systems, medicated chewing gums, and nutraceutical formulations. The growing acceptance of chewing gum as an effective delivery mechanism for active ingredients is encouraging pharmaceutical companies to expand product development initiatives in this area.Hospitality and travel retail channels are also experiencing strong recovery following the resurgence of global tourism and air travel. Premium chewing gum products increasingly benefit from purchases at airports, hotels, and travel convenience stores, particularly among consumers seeking portable and convenient refreshment products.Corporate and institutional procurement remains a comparatively niche segment but continues to expand steadily, particularly within workplace wellness initiatives, hospitality services, and corporate gifting programs. Growing awareness regarding employee wellness and consumer convenience is expected to support further development of this segment over the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Gum Base Candy Market Segmentations

By Product Type

- Chewing Gum

- Bubble Gum

- Specialty Gum Candy

By Gum Base Composition

- Synthetic Gum Base

- Natural Gum Base

- Hybrid Gum Base

By Flavor Category

- Mint and Peppermint

- Fruit Flavors

- Spice and Herbal Flavors

- Dessert and Confectionery Flavors

- Mixed and Novelty Flavors

By Functional Benefit

- Breath Freshening

- Oral Care and Teeth Whitening

- Stress Relief and Cognitive Wellness

- Nutraceutical and Vitamin Delivery

- Smoking Cessation

- Digestive Health

- Energy Enhancement

By Packaging Format

- Stick Packs

- Pellet Packs

- Pouches

- Bottles and Jars

- Tape and Roll Formats

- Single-Serve Impulse Packs

Regional Insights

North America

North America accounted for approximately 35% of global gum base candy revenues in 2025, making it the largest regional market. The United States alone contributed nearly 30% of global demand, supported by high per-capita consumption, widespread adoption of sugar-free products, and strong demand for functional chewing gums. Canada also represents a significant market for premium and natural formulations, driven by growing health consciousness and consumer willingness to pay for innovative products.Regional growth is being driven by increasing consumer preference for functional and wellness-oriented chewing gum products, continuous product innovation in sugar-free and nutraceutical formulations, rising demand for premium and natural ingredients, and the strong presence of leading confectionery manufacturers with extensive distribution networks. The growing popularity of chewing gum as a convenient oral care and wellness product, coupled with high disposable incomes and advanced retail infrastructure, continues to reinforce North America's leadership position in the global market.

Europe

Europe represented approximately 28% of the global market in 2025. Germany, the United Kingdom, France, Italy, and Spain are among the region's leading consumers of gum products. European consumers increasingly favor sugar-free and environmentally sustainable products, prompting manufacturers to invest heavily in biodegradable gum bases and natural ingredients. Stringent regulatory standards also encourage product innovation and premiumization.Regional growth is supported by increasing demand for clean-label and sustainable confectionery products, rising adoption of sugar-free formulations, strong consumer awareness regarding oral health, and growing investment in environmentally friendly gum base technologies. Premiumization trends, coupled with increasing demand for natural ingredients and functional chewing gum products, continue to create significant opportunities for manufacturers across the region.

Asia-Pacific

Asia-Pacific accounted for nearly 25% of global revenues and is expected to be the fastest-growing regional market during the forecast period, expanding at a CAGR exceeding 6.5%. China, India, Japan, Indonesia, and South Korea are driving growth due to rapid urbanization, increasing disposable incomes, and expanding retail infrastructure. China represents approximately 8% of global demand, while India is emerging as one of the fastest-growing markets because of its large young population and rising confectionery consumption.The region's growth is further supported by favorable demographic trends, increasing westernization of dietary preferences, expanding middle-class populations, rising penetration of organized retail and e-commerce channels, and growing consumer acceptance of premium and functional confectionery products. Product innovation tailored to local flavor preferences and increasing investments by international manufacturers are also accelerating market expansion throughout the region.

Latin America

Brazil and Mexico dominate regional demand, supported by favorable demographic structures and increasing penetration of modern retail channels. The region continues to exhibit strong demand for flavored and affordable gum products, particularly among younger consumers.Regional growth is primarily driven by a large youth population, increasing urbanization, improving retail accessibility, and rising demand for affordable confectionery products. The introduction of innovative flavors and attractive packaging, coupled with expanding supermarket and convenience store networks, continues to strengthen chewing gum consumption across major Latin American markets.

Middle East & Africa

The Middle East and Africa region is witnessing steady growth, led by Saudi Arabia, the United Arab Emirates, and South Africa. Rising tourism activity, increasing urbanization, and expanding westernized consumption habits are supporting market development. Growing investments in organized retail and premium confectionery products are expected to further stimulate demand across the region.Regional growth is additionally supported by rising disposable incomes in key economies, expanding young consumer populations, increasing penetration of international confectionery brands, and continuous development of modern retail infrastructure. Growing demand for premium and functional chewing gum products, particularly in urban centers and tourism-driven markets, is expected to create substantial growth opportunities across the Middle East and Africa during the forecast period.

Key Players in the Gum Base Candy Market

- Mars Incorporated

- Perfetti Van Melle

- Mondelez International

- Lotte Wellfood

- Grupo Arcor

- Cloetta AB

- The Hershey Company

- Meiji Holdings

- Orkla ASA

- Ferrero Group

- Yildiz Holding

- Nestlé S.A.

- Haribo GmbH & Co. KG

- Roshen Confectionery Corporation

- August Storck KG