Granola Cereal Market Size

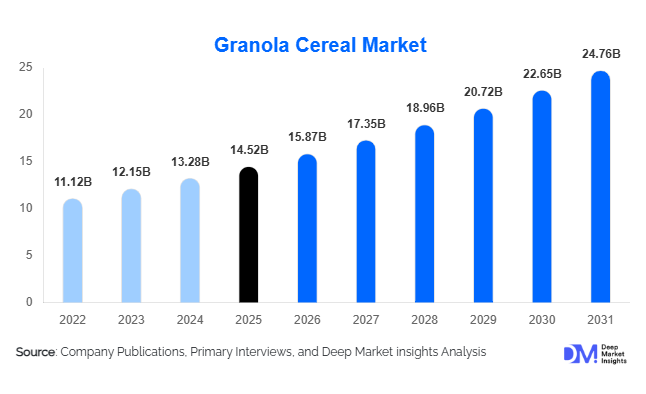

According to Deep Market Insights, the global granola cereal market size was valued at USD 14.52 billion in 2025 and is projected to grow from USD 15.87 billion in 2026 to reach USD 24.76 billion by 2031, expanding at a CAGR of 9.3% during the forecast period (2026–2031). The granola cereal market growth is primarily driven by increasing consumer preference for healthy breakfast products, rising adoption of clean-label and organic food products, and growing demand for convenient on-the-go nutrition solutions among urban consumers globally.

Key Market Insights

- Granola cereals are increasingly evolving into functional nutrition products, with demand rising for high-protein, probiotic-enriched, and low-sugar formulations.

- Organic and clean-label granola categories are witnessing strong growth globally, supported by growing consumer awareness regarding ingredient transparency and sustainable sourcing.

- North America dominates the global granola cereal market, led by high breakfast cereal consumption and strong health-food awareness in the United States and Canada.

- Asia-Pacific is emerging as the fastest-growing regional market, driven by urbanization, westernization of dietary habits, and expanding middle-class populations.

- E-commerce and direct-to-consumer distribution channels are transforming market accessibility, enabling premium and niche granola brands to scale rapidly.

- Sustainable packaging and plant-based innovations are becoming critical competitive differentiators among global manufacturers.

Granola Cereal Market Latest Trends

Functional and Protein-Enriched Granola Products Gaining Popularity

Consumers are increasingly shifting toward granola cereals that provide additional health benefits beyond basic nutrition. High-protein granola products fortified with whey protein, pea protein, soy protein, collagen, probiotics, and superfoods are gaining strong traction among fitness-focused and health-conscious consumers. Manufacturers are introducing formulations targeting digestive health, weight management, sports nutrition, and immunity support. Ingredients such as chia seeds, flaxseeds, quinoa, hemp, and almonds are increasingly incorporated into premium product offerings. The demand for keto-friendly, low-carb, and sugar-free granola products is also accelerating, particularly in North America and Europe where consumers are actively adopting healthier dietary lifestyles. Functional granola is transitioning from a niche health-food category into a mainstream breakfast and snack segment globally.

Sustainable Packaging and Clean-Label Innovation

Sustainability has become a major trend shaping the granola cereal market. Consumers increasingly prefer products packaged in recyclable, biodegradable, or reusable materials. Granola brands are investing heavily in eco-friendly pouches, paper-based packaging, and carbon-neutral manufacturing practices to strengthen brand positioning among environmentally conscious buyers. Simultaneously, clean-label formulations are becoming increasingly important, with consumers demanding shorter ingredient lists, non-GMO certifications, and minimally processed products. Organic granola cereals free from artificial preservatives, additives, and refined sugars are witnessing robust growth globally. Companies are also improving supply-chain transparency by highlighting ethically sourced oats, nuts, seeds, and sweeteners, reinforcing consumer trust and premium product positioning.

Granola Cereal Market Drivers

Growing Consumer Focus on Healthy Breakfast Habits

Rising health awareness globally is significantly driving demand for granola cereal products. Consumers are increasingly replacing sugary breakfast foods with healthier alternatives containing whole grains, fiber, nuts, and plant proteins. Granola cereals are widely perceived as nutritious, energy-rich, and beneficial for digestive and cardiovascular health. Increasing obesity rates, growing focus on preventive healthcare, and expanding awareness regarding balanced nutrition continue to support long-term market growth. Consumers are particularly seeking products with reduced sugar content, high protein levels, and natural ingredients, encouraging manufacturers to expand functional and clean-label product portfolios.

Rapid Urbanization and Demand for Convenient Foods

Busy lifestyles and urban working populations are accelerating demand for convenient ready-to-eat breakfast products globally. Granola cereals provide quick meal solutions requiring minimal preparation, making them highly attractive among working professionals, students, and fitness-oriented consumers. Single-serve cups, snack packs, and resealable packaging formats are further improving product convenience and portability. Growing participation of women in the workforce and increasing preference for on-the-go meal options continue to strengthen granola cereal consumption across both developed and developing economies.

Granola Cereal Market Restraints

Premium Product Pricing and Cost Sensitivity

Premium granola products containing organic ingredients, nuts, seeds, superfoods, and functional additives are typically priced significantly higher than conventional breakfast cereals. This creates affordability challenges in price-sensitive emerging markets where consumers may prioritize lower-cost breakfast alternatives. High production costs associated with sustainable sourcing and clean-label ingredients also limit pricing flexibility for manufacturers. Fluctuating raw material prices for oats, almonds, honey, and dried fruits further impact profit margins and retail pricing strategies.

Intense Competition from Alternative Healthy Breakfast Products

The granola cereal market faces strong competition from alternative health-focused breakfast and snack categories including protein bars, overnight oats, yogurt parfaits, smoothies, and fortified cereals. Consumers increasingly seek variety in healthy eating habits, resulting in frequent switching between product categories. In addition, concerns regarding hidden sugar content in certain granola products have created challenges for some manufacturers. Companies must continuously innovate formulations and improve nutritional positioning to maintain long-term consumer loyalty and competitive differentiation.

Granola Cereal Industry Key Opportunities

Expansion into Emerging Markets

Emerging economies across Asia-Pacific, Latin America, and the Middle East present substantial growth opportunities for granola cereal manufacturers. Rising disposable incomes, expanding urban middle-class populations, and increasing exposure to Western dietary habits are accelerating demand for packaged healthy breakfast products. Countries such as China, India, Indonesia, Brazil, and the UAE are witnessing rapid growth in modern retail infrastructure and e-commerce grocery platforms, improving product accessibility. Manufacturers are increasingly localizing flavors and introducing affordable pack sizes to strengthen penetration in price-sensitive consumer markets. These regions are expected to contribute significant incremental revenue growth over the next five years.

Personalized and Functional Nutrition Trends

The growing popularity of personalized nutrition is creating new opportunities within the granola cereal market. Consumers increasingly seek products tailored to specific health goals such as weight management, digestive wellness, sports recovery, and diabetic-friendly nutrition. Functional granola formulations enriched with probiotics, adaptogens, plant proteins, collagen, omega-3 fatty acids, and vitamin fortification are witnessing accelerating demand. Digital nutrition platforms and AI-driven dietary recommendation systems are further supporting customized product development. Brands that successfully combine health functionality with taste, convenience, and sustainability are expected to achieve strong long-term competitive advantages.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14.52 Billion |

| Market Size in 2026 | USD 15.87 Billion |

| Market Size in 2031 | USD 24.76 Billion |

| CAGR | 9.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Organic granola cereals represent one of the fastest-growing product categories globally, supported by rising consumer preference for clean-label and minimally processed foods. High-protein granola products are gaining traction among fitness-focused consumers seeking convenient sports nutrition solutions. Gluten-free and vegan granola products are also witnessing strong demand growth due to increasing dietary restrictions and plant-based food adoption. Traditional oat-based granola continues to dominate overall market volume due to affordability, nutritional value, and strong consumer familiarity. Functional granola enriched with probiotics, fiber, and superfoods is increasingly positioned as a premium category within the broader breakfast cereal market. Premiumization trends are further encouraging innovation in indulgent flavors such as chocolate, maple, nut-based, and fruit-infused granola variants.

Application Insights

Breakfast consumption remains the primary application segment for granola cereal products globally. Consumers continue to prefer granola as a convenient and nutritious breakfast option paired with milk, yogurt, fruits, or smoothies. Snacking applications are rapidly expanding as granola increasingly competes with conventional packaged snacks. Granola clusters, bars, and bite-sized formats are gaining popularity among younger demographics seeking healthier snack alternatives. Foodservice applications are also growing steadily, particularly in cafés, hotels, restaurants, and smoothie chains where granola is widely used in parfaits, smoothie bowls, desserts, and breakfast buffets. Sports nutrition applications are emerging strongly as high-protein granola products become integrated into pre-workout and post-workout meal routines.

Distribution Channel Insights

Supermarkets and hypermarkets dominate global granola cereal sales due to extensive shelf visibility, broad product availability, and promotional pricing strategies. Health-food stores and specialty retailers remain important for premium organic and functional granola categories. Online retail channels are witnessing the fastest growth rates globally, driven by convenience, subscription-based purchasing models, and growing digital grocery adoption. Direct-to-consumer sales channels are also expanding rapidly as granola brands increasingly leverage social media marketing, influencer partnerships, and personalized nutrition subscriptions. E-commerce platforms enable smaller niche brands to compete effectively against multinational cereal manufacturers by improving direct consumer engagement and brand loyalty.

End-Use Insights

Household consumers account for the largest share of the global granola cereal market, driven by growing home consumption of healthy breakfast and snack products. Working professionals, students, and fitness-conscious consumers remain key contributors to retail demand. The foodservice industry represents one of the fastest-growing end-use segments, particularly across cafés, hotels, bakeries, and quick-service restaurants integrating granola into healthy menu offerings. Institutional demand from schools, hospitals, and corporate cafeterias is also increasing due to growing focus on nutritious meal programs. Sports nutrition and wellness-focused end-use industries are emerging as important growth areas for protein-enriched and functional granola products.

Nature Insights

Conventional granola cereals continue to hold the largest market share due to broader affordability and mass-market availability. However, organic granola products are expanding rapidly as consumers increasingly prioritize food safety, sustainability, and ingredient transparency. Non-GMO and clean-label granola categories are gaining strong traction, particularly in North America and Europe where regulatory standards and consumer awareness regarding natural foods are well established. Manufacturers are increasingly investing in certified organic supply chains and sustainable ingredient sourcing to strengthen premium market positioning.

Explore more data points, trends and opportunities Download Free Sample Report

Granola Cereal Market Segmentations

By Product Type

- Traditional Granola Cereal

- Organic Granola Cereal

- Gluten-Free Granola Cereal

- High-Protein Granola Cereal

- Low-Sugar / Sugar-Free Granola Cereal

- Keto-Friendly Granola Cereal

- Vegan Granola Cereal

- Functional Granola Cereal

- Muesli-Style Granola

- Granola Clusters & Crisps

By Ingredient Base

- Oat-Based Granola

- Wheat-Based Granola

- Rice-Based Granola

- Quinoa-Based Granola

- Millet-Based Granola

- Mixed Grain Granola

- Nut-Based Granola

- Seed-Based Granola

By Flavor

- Chocolate

- Honey

- Vanilla

- Fruit-Based

- Nut-Based

- Cinnamon & Spice

- Maple

- Coconut

- Coffee-Flavored

- Savory Granola

By Nature

- Conventional

- Organic

- Non-GMO

- Clean-Label

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail

- Direct-to-Consumer (DTC)

- Warehouse Clubs

- Health Food Stores

Regional Insights

North America

North America accounted for nearly 38% of the global granola cereal market in 2025, making it the dominant regional market. The United States leads regional demand due to strong breakfast cereal consumption, growing health-conscious populations, and widespread availability of premium organic products. Consumers increasingly prefer low-sugar, high-protein, and plant-based granola formulations. Canada also demonstrates strong market growth supported by rising adoption of clean-label and gluten-free products. Advanced retail infrastructure and strong e-commerce penetration further support regional market expansion.

Europe

Europe represented approximately 29% of the global granola cereal market in 2025. Germany, the United Kingdom, France, and the Netherlands remain key contributors due to growing demand for healthy packaged foods and sustainable product offerings. European consumers strongly prioritize organic certifications, recyclable packaging, and ethical ingredient sourcing. The United Kingdom continues to witness strong growth in premium granola categories, while Germany leads demand for organic cereal products. Health-conscious dietary trends and increasing adoption of vegan products continue to support regional growth.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is projected to expand at a CAGR exceeding 11% during the forecast period. China, India, Japan, South Korea, and Australia are driving regional growth due to rapid urbanization, westernization of diets, and increasing disposable incomes. China currently dominates regional demand due to expansion of modern retail channels and online grocery platforms. India is witnessing increasing adoption of healthy breakfast products among urban millennials and working professionals. Japanese and Australian consumers demonstrate strong demand for premium and functional granola products with clean-label positioning.

Latin America

Latin America is emerging as a promising growth market, particularly in Brazil, Mexico, Argentina, and Chile. Rising middle-class incomes, growing awareness regarding healthy eating habits, and increasing availability of imported granola brands are supporting market expansion. Consumers in major urban centers are increasingly adopting granola products as convenient breakfast and snack alternatives. Premium and organic granola categories are gradually gaining popularity among affluent consumers across the region.

Middle East & Africa

The Middle East & Africa region is witnessing gradual but steady growth in granola cereal demand. The UAE and Saudi Arabia remain key regional markets due to increasing health awareness, rising expatriate populations, and strong premium retail expansion. South Africa also demonstrates growing demand for nutritious packaged breakfast products. Urbanization, lifestyle changes, and increasing availability of imported cereal brands are expected to support long-term market development across the region.

Key Players in the Granola Cereal Market

- Kellanova

- General Mills

- PepsiCo

- Nature's Path Foods

- Post Holdings

- Bob's Red Mill Natural Foods

- Calbee Inc.

- Nestlé

- The Jordans & Ryvita Company

- Bagrrys India

- Marico Limited

- Freedom Foods Group

- Lizi's Granola

- Bear Naked

- Sunny Crunch Foods