Garment Manufacturing Market Size

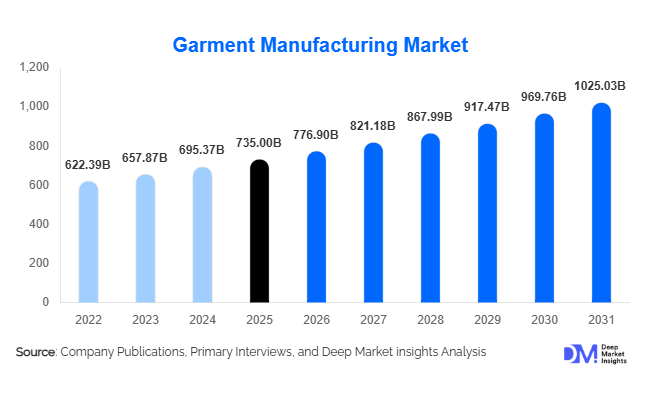

According to Deep Market Insights, the global garment manufacturing market size was valued at USD 735 billion in 2025 and is projected to grow from USD 776.90 billion in 2026 to reach USD 1,025.03 billion by 2031, expanding at a CAGR of 5.7% during the forecast period (2026–2031). The garment manufacturing market growth is driven by increasing apparel consumption across emerging economies, the rapid expansion of e-commerce fashion retail, rising demand for fast-fashion products, and growing investments in automated and sustainable manufacturing technologies. As global brands continue to diversify sourcing networks and strengthen supply chain resilience, garment manufacturing hubs across Asia-Pacific, Latin America, and Africa are experiencing significant capacity expansion. The industry is also benefiting from rising consumer demand for activewear, athleisure, sustainable apparel, and customized clothing products.

Key Market Insights

- Asia-Pacific dominates global garment manufacturing, accounting for approximately 56% of total market revenue, led by China, Bangladesh, India, and Vietnam.

- Women's apparel remains the largest product category, contributing nearly 48% of global garment manufacturing revenues in 2025.

- Export-oriented manufacturing continues to drive industry growth, representing over 56% of total production volumes worldwide.

- Smart manufacturing adoption is accelerating, with AI-enabled production planning, automated cutting systems, and digital sampling becoming mainstream.

- Sustainable garment production is emerging as a major competitive differentiator, with global brands prioritizing suppliers that meet ESG and traceability standards.

- India is expected to be the fastest-growing major garment manufacturing country, supported by government incentives, infrastructure development, and expanding export opportunities.

Garment Manufacturing Market Trends

Shift Toward Sustainable and Circular Apparel Production

Sustainability has become a defining trend across the garment manufacturing industry. Global apparel brands are increasingly requiring suppliers to adopt environmentally responsible manufacturing processes, reduce carbon emissions, and improve supply chain transparency. Manufacturers are investing in recycled polyester, organic cotton, water-efficient dyeing technologies, and renewable energy-powered production facilities. Circular fashion initiatives involving textile recycling, garment reuse, and waste reduction programs are gaining momentum across Europe and North America. As sustainability regulations continue to tighten globally, manufacturers capable of providing traceable and environmentally compliant products are securing long-term contracts with leading fashion brands and retailers.

Digitalization and Smart Factory Adoption

Industry 4.0 technologies are reshaping garment manufacturing operations worldwide. Automated cutting systems, digital pattern development, AI-powered production scheduling, robotics-assisted sewing, and IoT-enabled factory monitoring solutions are improving productivity and reducing production costs. Manufacturers are increasingly deploying digital twins and predictive maintenance systems to optimize factory performance and minimize downtime. These technologies enable shorter lead times, improved product consistency, and greater flexibility in responding to rapidly changing fashion trends. Smart manufacturing facilities are also helping producers overcome labor shortages while maintaining competitive operating margins.

Garment Manufacturing Market Drivers

Expansion of Global E-Commerce Fashion Sales

The continued growth of online apparel retailing is significantly increasing demand for garment manufacturing services. Digital-first brands require agile production capabilities, faster inventory replenishment, and shorter product development cycles. The rise of direct-to-consumer fashion companies and online marketplaces has created sustained demand for both mass production and smaller customized production runs. Manufacturers capable of offering speed-to-market advantages are increasingly becoming preferred partners for global retailers and fashion brands.

Rising Disposable Income and Urbanization

Growing middle-class populations across Asia-Pacific, Africa, and Latin America are contributing to increased apparel consumption. Urbanization, rising workforce participation, and changing fashion preferences are driving demand for premium apparel, activewear, and fashion-forward clothing products. Consumers are purchasing garments more frequently, supporting consistent production growth across both domestic and export-oriented manufacturing markets.

Growing Demand for Sportswear and Athleisure

The global shift toward health-conscious lifestyles and fitness activities is driving strong growth in sportswear and athleisure apparel production. Consumers increasingly seek versatile clothing that combines comfort, functionality, and style. This trend has encouraged major apparel brands to expand activewear collections, resulting in increased production volumes and higher manufacturing investments in performance fabrics and technical apparel.

Garment Manufacturing Market Restraints

Raw Material Price Volatility

Fluctuations in cotton, polyester, wool, and viscose prices continue to create uncertainty for garment manufacturers. Changes in energy costs, weather conditions, trade restrictions, and geopolitical developments can significantly affect input costs and profit margins. Manufacturers often face challenges in passing these cost increases through supply chains, particularly under fixed-price contracts with global retailers.

Increasing Compliance and Sustainability Costs

Global apparel brands are imposing stricter requirements regarding labor practices, workplace safety, environmental management, and supply chain transparency. Compliance with international standards requires significant investments in factory upgrades, wastewater treatment systems, employee welfare programs, and sustainability certifications. Smaller manufacturers often face financial constraints in meeting these evolving requirements, creating barriers to market participation.

Garment Manufacturing Market Opportunities

Supply Chain Diversification and China+1 Strategies

Global apparel brands are increasingly diversifying sourcing operations beyond China to reduce supply chain concentration risks. Countries such as India, Vietnam, Bangladesh, Indonesia, and Mexico are benefiting from growing manufacturing investments as brands adopt China+1 sourcing strategies. Manufacturers in these regions have significant opportunities to secure new export contracts and expand production capacity. Favorable trade agreements, competitive labor costs, and government incentives are further supporting investment inflows into emerging garment manufacturing hubs.

Smart Manufacturing and Automation Investments

The growing adoption of automated production technologies presents substantial opportunities for manufacturers seeking to improve productivity and profitability. Automated cutting systems, robotic sewing equipment, AI-powered planning software, and digital quality control solutions can significantly reduce production costs while enhancing product consistency. Companies investing in advanced manufacturing technologies are likely to gain competitive advantages as labor costs rise globally and brands increasingly prioritize efficiency and responsiveness.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 735 Billion |

| Market Size in 2026 | USD 776.90 Billion |

| Market Size in 2031 | USD 1025.03 Billion |

| CAGR | 5.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Category Insights

Women's apparel dominates the garment manufacturing market, accounting for approximately 48% of global revenue in 2025. The segment benefits from broader product diversity, higher purchasing frequency, and continuous fashion innovation across formal wear, casual wear, activewear, and luxury categories. Sportswear and activewear represent the fastest-growing product category, supported by rising fitness participation, athleisure trends, and increasing consumer demand for performance-oriented apparel. Children's apparel continues to demonstrate steady growth due to rising birth rates in emerging economies and increasing expenditure on premium children's clothing. Workwear and uniforms are also expanding, driven by demand from healthcare, hospitality, industrial, and corporate sectors.

Fiber Type Insights

Polyester-based garments account for approximately 42% of global garment manufacturing output, making polyester the dominant fiber category. The material's durability, affordability, moisture resistance, and versatility support widespread adoption across sportswear, casual apparel, and fashion garments. Cotton remains the second-largest fiber segment, particularly in premium apparel and sustainable clothing applications. Recycled polyester is emerging as a high-growth category as apparel brands seek to reduce environmental impact and meet sustainability targets. Blended fibers are increasingly utilized to improve garment performance, comfort, and durability across various apparel categories.

Manufacturing Process Insights

Original Equipment Manufacturing (OEM) accounts for approximately 38% of the global garment manufacturing market. OEM production allows apparel brands to outsource manufacturing while retaining control over product design, branding, and marketing activities. Full Package Production (FPP) is gaining popularity as brands seek integrated manufacturing solutions that include sourcing, production, and logistics management. Original Design Manufacturing (ODM) is also expanding as retailers increasingly rely on manufacturers for product innovation and design support. These integrated manufacturing models provide higher value-added services and stronger customer relationships.

End User Insights

Women represent the largest end-user segment, accounting for nearly half of total garment manufacturing demand worldwide. The segment benefits from rapid product turnover, seasonal fashion trends, and premium pricing opportunities. Men's apparel continues to experience stable growth, supported by increasing demand for business casual, activewear, and lifestyle clothing. Children's apparel remains an important growth category due to rising disposable incomes and increasing spending on premium and branded products. The sportswear and fitness apparel segment is emerging as one of the fastest-growing end-use categories globally.

Technology Adoption Insights

Semi-automated manufacturing systems account for approximately 45% of global garment production facilities. These systems provide a balance between cost efficiency and productivity improvements. Smart manufacturing technologies are gaining momentum, particularly among large export-oriented producers seeking to improve operational efficiency. AI-powered production planning, digital sampling, automated cutting, and robotics-assisted sewing are becoming increasingly common. Fully integrated smart factories are expected to represent a growing share of garment production capacity over the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Garment Manufacturing Market Segmentations

By Product Category

- Upper Body Apparel

- Lower Body Apparel

- Full-Body Apparel

- Outerwear

- Innerwear & Sleepwear

- Sportswear & Activewear

- Workwear & Uniforms

- Children’s Apparel

By Fiber Type

- Natural Fibers

- Man-Made Fibers

- Blended Fibers

By Manufacturing Process

- Cut-Make-Trim (CMT)

- Full Package Production (FPP)

- Original Equipment Manufacturing (OEM)

- Original Design Manufacturing (ODM)

- Original Brand Manufacturing (OBM)

By Production Scale

- Mass Production

- Medium Batch Production

- Small Batch Production

- Custom/Bespoke Production

By Distribution Channel

- Export Manufacturing

- Domestic Brand Manufacturing

- Private Label Manufacturing

- Contract Manufacturing

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global garment manufacturing market with approximately 56% market share in 2025. China remains the world's largest garment manufacturing country, accounting for nearly 28% of global production value. Bangladesh continues to strengthen its position as a leading exporter of ready-made garments, while Vietnam benefits from extensive free trade agreements and growing foreign direct investment. India is emerging as the fastest-growing manufacturing hub, supported by government initiatives such as the Production Linked Incentive (PLI) scheme and PM-MITRA textile parks. Indonesia and Pakistan also continue expanding export-oriented apparel production capabilities.

North America

North America accounts for approximately 12% of the global garment manufacturing market. The United States remains the largest apparel consumption market globally, creating substantial demand for imported garments. Mexico is benefiting from nearshoring trends and regional trade agreements that encourage production closer to North American consumers. Domestic manufacturing growth is concentrated in specialized apparel, quick-response production, and premium garment categories.

Europe

Europe represents approximately 16% of global garment manufacturing revenue. Turkey remains a key production center due to its strategic location and proximity to major European fashion markets. Italy continues to dominate luxury apparel manufacturing, while Portugal and Eastern European countries are attracting investments in sustainable and high-quality garment production. European demand is increasingly influenced by environmental regulations and sustainability-focused sourcing strategies.

Latin America

Latin America accounts for roughly 8% of the global market. Brazil and Mexico are the largest regional markets, supported by strong domestic apparel demand and expanding manufacturing capabilities. Mexico's strategic position within North American supply chains continues to attract investment from international apparel brands seeking nearshore production alternatives.

Middle East & Africa

The Middle East and Africa collectively represent approximately 8% of global garment manufacturing revenue. Egypt, Morocco, Ethiopia, Kenya, and South Africa are emerging as important manufacturing destinations due to competitive labor costs and favorable export opportunities. Ethiopia and Egypt are among the fastest-growing production centers in the region, supported by government-led industrialization programs and increasing foreign investment.

Key Players in the Garment Manufacturing Market

- Shenzhou International Group Holdings

- Crystal International Group

- MAS Holdings

- Eclat Textile Co., Ltd.

- Luen Thai Holdings

- TAL Apparel

- Esquel Group

- Gokaldas Exports Ltd.

- KPR Mill Limited

- Vardhman Textiles Limited

- Pou Chen Corporation

- Makalot Industrial Co., Ltd.

- PDS Limited

- Hirdaramani Group

- Orient Craft Limited