Frozen Peas Market Size

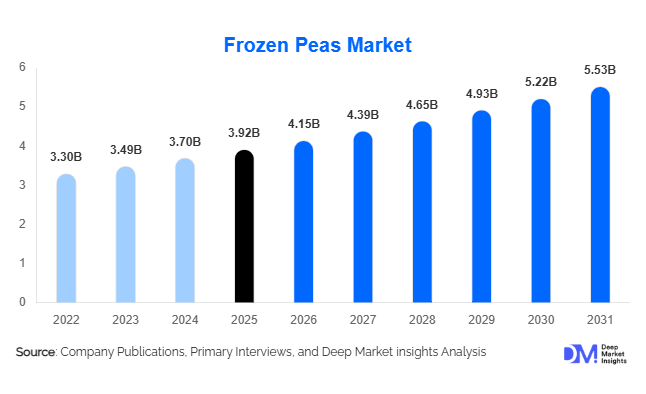

According to Deep Market Insights, the global frozen peas market size was valued at USD 3.92 billion in 2025 and is projected to grow from USD 4.15 billion in 2026 to reach USD 5.53 billion by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The frozen peas market growth is primarily driven by increasing consumer demand for convenient and nutritious frozen vegetables, expanding cold-chain infrastructure across emerging economies, and rising utilization of frozen peas in ready meals, foodservice applications, and plant-based food products. Advances in individual quick freezing (IQF) technology, growth in organized retail, and increasing awareness regarding food waste reduction are further supporting market expansion globally. Frozen peas have become a staple ingredient across households, institutional kitchens, and food manufacturing facilities due to their year-round availability, longer shelf life, and consistent quality.

Key Market Insights

- IQF frozen peas dominate the market, accounting for over 70% of global frozen peas production due to superior texture retention and product quality.

- Green frozen peas remain the leading product category, contributing nearly 67% of global market revenue owing to widespread consumer acceptance and diverse culinary applications.

- Europe dominates the global frozen peas market, supported by strong frozen food consumption habits, advanced processing infrastructure, and extensive retail penetration.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization, increasing disposable incomes, and significant investments in cold-chain logistics.

- Food processing applications are expanding rapidly, particularly in frozen meals, soups, plant-based foods, and vegetable blends.

- Sustainability and organic frozen vegetables are gaining traction, creating premium pricing opportunities for manufacturers globally.

Frozen Peas Market Latest Trends

Plant-Based Food Manufacturing Driving Ingredient Demand

The growing global adoption of plant-based diets is significantly influencing frozen peas demand. Food manufacturers are increasingly incorporating frozen peas into meat alternatives, plant-based ready meals, protein-enriched snacks, and vegan convenience foods. Frozen peas provide nutritional benefits, protein content, and processing versatility, making them a preferred ingredient for food innovators. As consumers continue shifting toward healthier and environmentally sustainable diets, frozen peas are becoming an important raw material within the broader plant-based food ecosystem. Manufacturers are also introducing pea-based vegetable blends and functional food products targeted at health-conscious consumers.

Premium Organic Frozen Vegetables Expanding Market Opportunities

Organic frozen peas are emerging as one of the fastest-growing premium segments within the market. Consumers increasingly seek clean-label, pesticide-free, and sustainably produced food products, particularly across Europe and North America. Retailers are expanding shelf space for certified organic frozen vegetables, while foodservice operators are incorporating organic ingredients into premium menus. Producers are investing in traceability systems, regenerative farming practices, and sustainable packaging solutions to capitalize on rising demand. This trend is supporting margin expansion and product differentiation within an otherwise highly competitive market.

Frozen Peas Market Drivers

Growing Demand for Convenient Food Products

Modern consumers increasingly prioritize convenience without compromising nutritional quality. Frozen peas require minimal preparation, offer extended shelf life, and reduce food wastage compared to fresh vegetables. Urbanization, increasing workforce participation, and growth in dual-income households continue driving demand for frozen vegetables globally. Retailers and foodservice operators benefit from lower spoilage rates and consistent product availability, further strengthening frozen peas market growth.

Expansion of Frozen Food Consumption Worldwide

The broader frozen food industry continues to expand as consumers recognize improvements in freezing technologies and nutritional retention. Frozen peas have benefited significantly from advancements in IQF processing, which preserves taste, texture, color, and nutritional value. Growing consumption of frozen meals, soups, prepared foods, and vegetable blends is generating substantial procurement demand from food manufacturers. Increased freezer ownership and improved distribution infrastructure are also contributing to long-term market expansion.

Growth of Organized Retail and E-Commerce Channels

Supermarkets, hypermarkets, and online grocery platforms are improving consumer access to frozen vegetables. Modern retail chains are allocating larger shelf space to frozen foods, while e-commerce providers increasingly offer temperature-controlled delivery services. This has expanded market penetration in both developed and emerging economies. Online grocery platforms are particularly influencing younger consumers who value convenience, home delivery, and access to premium frozen food products.

Frozen Peas Market Restraints

Dependence on Cold Chain Infrastructure

Frozen peas require uninterrupted refrigeration throughout storage, transportation, and retail distribution. Infrastructure gaps in emerging economies continue to limit market penetration and increase logistics costs. Temperature fluctuations can negatively impact product quality, creating operational challenges for manufacturers and distributors.

Agricultural Yield Volatility and Raw Material Risks

Pea cultivation remains vulnerable to weather conditions, water availability, fertilizer costs, and changing climatic patterns. Crop failures and reduced yields can create supply shortages and price volatility. Manufacturers must increasingly invest in diversified sourcing strategies and long-term grower partnerships to mitigate agricultural risks and ensure consistent supply.

Frozen Peas Industry Key Opportunities

Expansion of Cold-Chain Infrastructure in Emerging Markets

Rapid investments in refrigerated warehousing, transportation networks, and food preservation facilities across Asia-Pacific, Latin America, and the Middle East present substantial growth opportunities. Countries such as India, Indonesia, Vietnam, Saudi Arabia, and Brazil are actively modernizing their cold-chain ecosystems. These investments are enabling frozen food manufacturers to reach previously underserved consumer segments and expand product availability beyond major urban centers. The development of integrated cold storage hubs and government-supported food logistics initiatives is expected to significantly increase frozen peas consumption over the next decade.

Sustainable and Organic Product Development

Sustainability-focused consumers are increasingly influencing purchasing decisions across retail and foodservice channels. Manufacturers that invest in organic farming, recyclable packaging, renewable energy-powered processing facilities, and carbon reduction programs are likely to gain competitive advantages. Organic frozen peas command premium pricing in developed markets and are becoming increasingly important within private-label retail portfolios. Sustainability certifications and transparent sourcing practices are also strengthening relationships with institutional buyers and multinational foodservice operators.

Industrial Food Processing Applications

The food processing industry presents a major growth avenue for frozen peas suppliers. Demand from frozen meal manufacturers, soup producers, vegetable blend processors, and plant-based food companies continues to increase globally. Industrial buyers value frozen peas for their consistency, cost-effectiveness, and year-round availability. Long-term supply contracts with food manufacturers provide stable revenue streams and reduce dependence on seasonal retail demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.92 Billion |

| Market Size in 2026 | USD 4.15 Billion |

| Market Size in 2031 | USD 5.53 Billion |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global frozen peas market is led by green frozen peas, which account for approximately 67% of total market revenue. The segment maintains its dominant position due to extensive consumer familiarity, affordability, broad availability, and versatility across multiple culinary applications. Green frozen peas are widely used in household cooking, foodservice operations, frozen vegetable blends, soups, ready meals, and processed food products. Their ability to retain nutritional value, texture, and flavor during freezing further supports strong consumer preference. The leading growth driver for this segment is the increasing global demand for convenient, nutrient-rich vegetables that offer year-round availability and reduced preparation time.Sweet frozen peas represent the second-largest product category, supported by their naturally sweeter taste, superior sensory characteristics, and growing adoption in premium retail offerings. Demand for sweet peas continues to rise among consumers seeking higher-quality frozen vegetables and enhanced meal experiences. In developed markets, manufacturers are increasingly introducing premium frozen vegetable ranges featuring sweet peas to capture value-added opportunities.Sugar snap peas and snow peas collectively represent a smaller share of the market but are witnessing steady growth, particularly within premium foodservice establishments, health-focused retail channels, and Asian cuisine applications. Their popularity is supported by changing dietary preferences, increasing consumption of vegetable-based meals, and growing consumer interest in diverse frozen vegetable options. Meanwhile, mixed frozen vegetable products containing peas are gaining significant traction as consumers increasingly favor ready-to-cook meal solutions, meal kits, and multifunctional vegetable combinations that simplify meal preparation while minimizing food waste.The product landscape is also benefiting from ongoing innovation in freezing technologies, packaging solutions, and product differentiation strategies. Manufacturers are increasingly focusing on organic variants, steam-ready packaging, and blended vegetable offerings to address evolving consumer preferences for convenience, nutrition, and sustainability.

Application Insights

Direct consumption remains the largest application segment, accounting for approximately 41% of global frozen peas demand. Frozen peas are extensively used as standalone side dishes, ingredients in home-cooked meals, and nutritional additions to a wide range of recipes. Their convenience, affordability, long shelf life, and ability to preserve nutritional quality continue to make them a preferred vegetable choice among households worldwide. The primary growth driver for this segment is the increasing consumer demand for convenient and healthy food options that require minimal preparation while maintaining nutritional value.Ready meals and frozen meal applications represent one of the fastest-growing segments within the market. The rapid pace of modern lifestyles, increasing workforce participation, and rising preference for convenient meal solutions have significantly expanded demand for frozen peas as a key ingredient in prepared foods. Food manufacturers increasingly incorporate frozen peas into microwaveable meals, frozen entrées, meal kits, and convenience-focused food products due to their versatility and consumer acceptance.Soups, sauces, salads, vegetable blends, and prepared food products collectively account for a substantial share of industrial demand. Frozen peas contribute texture, color, flavor, and nutritional value across numerous processed food categories, making them an essential ingredient for food manufacturers. The bakery and prepared food sectors are also creating additional opportunities through the incorporation of vegetable-based fillings and nutritional product formulations.Plant-based food applications are emerging as a particularly dynamic growth area. As consumers increasingly adopt vegetarian, vegan, and flexitarian diets, manufacturers are utilizing peas and pea-derived ingredients in alternative protein products, plant-based ready meals, and functional food formulations. This trend is expected to strengthen over the forecast period as demand for sustainable and protein-rich food solutions continues to expand globally.

Distribution Channel Insights

Supermarkets and hypermarkets dominate global frozen peas sales, accounting for nearly 48% of total market revenue. These retail channels benefit from extensive frozen food assortments, established cold storage infrastructure, high consumer footfall, and strong brand visibility. Their ability to provide consumers with a wide variety of frozen vegetable options under one roof continues to reinforce market leadership. The leading growth driver for this segment is the ongoing expansion of organized retail networks and enhanced availability of frozen food products across urban and suburban markets.Convenience stores play an important role in supporting demand, particularly in densely populated urban areas where consumers prioritize quick purchasing decisions and smaller package formats. The segment benefits from increasing urbanization and growing consumer preference for easily accessible food products.Online retail channels are experiencing rapid growth and are transforming frozen food distribution across many regions. Rising consumer confidence in grocery e-commerce platforms, advancements in temperature-controlled logistics, and expanding home delivery services have significantly improved access to frozen products. The channel is particularly benefiting from the growing adoption of digital shopping platforms among younger consumers and working households.Specialty food retailers continue to support sales of premium, organic, and health-oriented frozen peas, while wholesale distributors and direct business-to-business supply channels remain essential for serving restaurants, hotels, catering operators, institutions, and food processing companies. As cold-chain capabilities continue to improve globally, distribution efficiency and product availability are expected to strengthen across all channels.

End User Insights

Household consumers represent the largest end-user segment, accounting for approximately 52% of global frozen peas consumption. The segment continues to benefit from rising freezer ownership, increasing demand for convenient vegetables, growing health awareness, and consumer efforts to reduce food waste through longer-lasting food products. Frozen peas provide households with a reliable source of vegetables that can be stored for extended periods without significant quality degradation. The primary growth driver for this segment is the increasing preference for convenient, nutritious, and cost-effective meal ingredients among consumers.Foodservice operators, including restaurants, hotels, quick-service restaurants, catering companies, and institutional kitchens, constitute a significant commercial user base. Frozen peas are widely utilized due to their consistent quality, reduced preparation requirements, portion control advantages, and year-round availability. The continued expansion of foodservice industries in both developed and emerging economies supports stable demand from this segment.The food processing industry represents the fastest-growing end-user category within the frozen peas market. Manufacturers increasingly rely on frozen peas for the production of ready meals, soups, sauces, frozen vegetable blends, prepared foods, and plant-based products. Growth in convenience foods, private-label frozen offerings, and value-added vegetable products is significantly increasing industrial consumption of frozen peas.Institutional buyers, including schools, hospitals, government facilities, and corporate cafeterias, also contribute stable procurement volumes. These organizations favor frozen peas due to their ease of storage, predictable supply availability, nutritional consistency, and suitability for large-scale meal preparation programs.

Farming Method Insights

Conventional frozen peas account for approximately 84% of total market value and remain the dominant farming method segment. Large-scale cultivation practices, established supply chains, higher production volumes, and favorable cost structures support widespread adoption among growers and processors. Conventional farming enables manufacturers to maintain consistent supply levels and competitive pricing across major consumer markets. The leading growth driver for this segment is the ability to support large-scale commercial production at lower costs while ensuring reliable year-round availability.Organic frozen peas, although representing a smaller market share, are growing at a significantly faster pace than the overall industry. Rising consumer awareness regarding food quality, environmental sustainability, and health-conscious purchasing decisions is driving increased demand for organically certified frozen vegetables. Retailers are expanding shelf space dedicated to organic frozen products, while foodservice operators increasingly incorporate organic ingredients into premium and health-focused menu offerings.The segment is further supported by expanding organic farming acreage, government initiatives promoting sustainable agricultural practices, and increasing availability of certification programs across developed and emerging markets. As consumer willingness to pay premium prices for organic food products continues to strengthen, organic frozen peas are expected to capture an increasing share of future market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Peas Market Segmentations

By Product Type

- Green Frozen Peas

- Sweet Frozen Peas

- Yellow Frozen Peas

- Snow Peas

- Sugar Snap Peas

- Mixed Frozen Pea Products

By Farming Method

- Conventional Frozen Peas

- Organic Frozen Peas

By Product Form

- Whole Peas

- Shelled Peas

- Split Peas

- Pureed Frozen Peas

- Frozen Pea Ingredients

By Freezing Technology

- Individually Quick Frozen (IQF) Peas

- Blast Frozen Peas

- Cryogenically Frozen Peas

- Other Commercial Freezing Technologies

By Packaging Format

- Retail Bags

- Retail Pouches

- Retail Boxes

- Bulk Foodservice Packs

- Industrial Bulk Packaging

Regional Insights

North America

North America accounts for approximately 28% of global frozen peas demand, with the United States representing nearly 22% of worldwide consumption. The region benefits from a highly developed frozen food industry, advanced cold-chain infrastructure, extensive retail distribution networks, and strong consumer acceptance of frozen vegetables. Frozen peas are widely utilized across households, foodservice establishments, and food manufacturing applications, including soups, ready meals, vegetable blends, and plant-based foods. Regional growth is primarily driven by increasing demand for convenience foods, rising consumption of healthy frozen vegetable products, expansion of plant-based food manufacturing, and continued innovation in frozen meal categories. Canada also contributes significantly through strong agricultural production capabilities, modern food processing infrastructure, and established frozen food distribution systems.

Europe

Europe remains the largest regional market, accounting for approximately 36% of global revenue. Major demand centers include Germany, the United Kingdom, France, Italy, Spain, Belgium, and the Netherlands. The region exhibits one of the highest levels of frozen vegetable consumption globally, supported by mature consumer purchasing habits and highly efficient cold-chain logistics networks. Europe also serves as a major production and export hub, with Belgium, France, and Poland playing important roles in frozen vegetable processing and international trade. Regional growth is driven by strong consumer preference for convenient and nutritious food products, increasing demand for organic and sustainably sourced vegetables, growing adoption of clean-label food products, and ongoing investments in energy-efficient cold storage and food processing technologies. Sustainability initiatives and food waste reduction efforts further encourage frozen vegetable consumption across European markets.

Asia-Pacific

Asia-Pacific represents approximately 22% of global market value and is the fastest-growing regional market, expanding at a CAGR exceeding 7%. China, India, Japan, South Korea, and Australia are among the key contributors to regional demand. Rapid urbanization, changing dietary patterns, rising disposable incomes, and expanding organized retail networks continue to accelerate market growth. Significant investments in refrigerated logistics infrastructure and cold-chain development have improved frozen food accessibility across both metropolitan and secondary cities. The primary drivers of regional growth include increasing adoption of convenience foods, expansion of modern supermarket chains, growth in e-commerce grocery platforms, rising participation of working professionals, and improving consumer awareness regarding the nutritional benefits of frozen vegetables. India remains one of the fastest-growing national markets due to strong government support for cold storage infrastructure, increasing frozen food penetration, and rapid modernization of food retail channels.

Latin America

Latin America contributes approximately 7% of global frozen peas demand, led by Brazil, Mexico, Argentina, and Chile. The regional market is undergoing steady development as modern retail formats continue to expand and cold-chain capabilities improve. Consumer awareness regarding the convenience, affordability, and nutritional benefits of frozen vegetables is increasing across major urban centers. Growth in the region is driven by rising urbanization, increasing disposable incomes, expanding supermarket penetration, greater workforce participation among women, and growing demand for time-saving food products. Investments in food distribution infrastructure and improvements in refrigerated transportation networks are further supporting market expansion throughout Latin America.

Middle East & Africa

The Middle East and Africa account for approximately 7% of global market revenue, with Saudi Arabia, the United Arab Emirates, South Africa, Egypt, and Qatar representing major consuming countries. Demand for frozen peas is supported by high dependence on imported food products, increasing urban populations, and expanding modern retail channels. Governments across the region continue to prioritize food security initiatives, encouraging investments in cold storage facilities and refrigerated logistics infrastructure. Key regional growth drivers include rising consumption of convenience foods, expansion of the hospitality and foodservice sectors, increasing expatriate populations, growth in organized retail, and ongoing investments in food supply chain modernization. The United Arab Emirates and Saudi Arabia are among the fastest-growing frozen vegetable import markets, benefiting from strong consumer purchasing power, evolving dietary habits, and increasing demand for premium and imported food products.

Key Players in the Frozen Peas Market

- Bonduelle

- Ardo Group

- McCain Foods

- Birds Eye Foods

- Greenyard

- B&G Foods

- Pinguin Foods

- Hanover Foods

- Nomad Foods

- IQF Frost

- Conagra Brands

- Dujardin Foods

- Oerlemans Foods

- Chiangmai Frozen Foods

- Virto Group