Frozen Durian Market Size

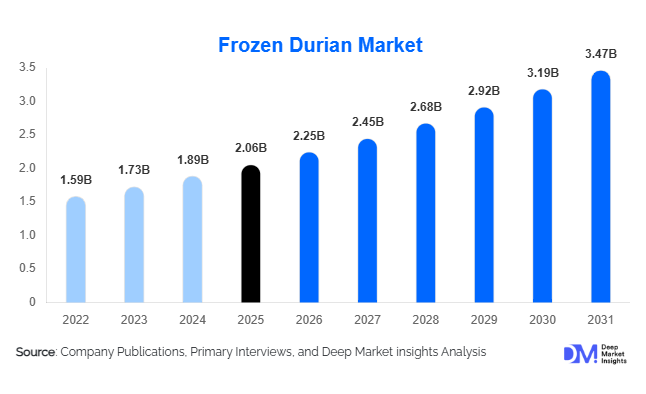

According to Deep Market Insights, the global frozen durian market size was valued at USD 2.06 billion in 2025 and is projected to grow from USD 2.25 billion in 2026 to reach USD 3.47 billion by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The frozen durian market growth is primarily driven by increasing international demand for premium tropical fruits, expanding cold-chain infrastructure, rising consumption of Asian fruit products across Western markets, and the growing use of frozen durian as an ingredient in desserts, bakery products, beverages, and processed foods. Advancements in freezing technologies such as Individually Quick Frozen (IQF) processing are helping manufacturers preserve flavor, texture, and nutritional quality while extending shelf life, making frozen durian increasingly suitable for global trade.

Key Market Insights

- Asia-Pacific dominates the global frozen durian market, accounting for more than 72% of global demand, led by China, Thailand, Malaysia, and Vietnam.

- China remains the largest importer of frozen durian globally, driven by strong consumer preference for premium durian varieties such as Musang King and Monthong.

- Frozen durian pulp is the leading product segment, accounting for nearly 38% of global market revenue due to its versatility across food processing applications.

- Food manufacturing applications are growing rapidly, particularly in bakery, confectionery, dairy, and frozen dessert industries.

- E-commerce channels are transforming frozen durian distribution, enabling direct-to-consumer sales and improving accessibility in non-traditional markets.

- North America and Europe are emerging as high-growth consumption regions, supported by increasing Asian populations, multicultural food trends, and premium fruit consumption.

Frozen Durian Market Latest Trends

Premium Durian Varieties Driving International Trade

Demand for premium frozen durian varieties such as Musang King, Black Thorn, and D24 continues to accelerate globally. Consumers are increasingly willing to pay premium prices for superior flavor profiles, texture consistency, and traceability. Malaysian exporters have particularly benefited from growing demand for premium cultivars in China, Singapore, Hong Kong, and emerging Western markets. Premium frozen durian products are increasingly positioned as luxury fruit products, supporting higher profit margins throughout the supply chain. Brand differentiation based on origin, variety certification, and quality grading has become a major competitive factor among suppliers.

Expansion of Durian-Based Processed Foods

Frozen durian is increasingly being utilized as a raw material for value-added food applications. Manufacturers are introducing durian ice cream, cakes, pastries, smoothies, milk beverages, confectionery products, chocolates, and ready-to-eat desserts. Foodservice operators and industrial processors are expanding their use of frozen pulp and puree due to consistent quality and year-round availability. This trend is helping diversify demand beyond direct consumption while increasing overall market value. The emergence of durian-flavored premium snack products and specialty dairy offerings is creating new revenue streams for processors globally.

Frozen Durian Market Drivers

Rapid Growth of Chinese Import Demand

China continues to be the primary engine of growth for the frozen durian industry. Rising disposable incomes, expanding middle-class populations, and increasing consumer preference for premium tropical fruits have significantly boosted imports. Frozen durian offers logistical advantages compared to fresh durian, allowing suppliers to serve distant markets while maintaining product quality. The expansion of cross-border e-commerce and premium grocery retail channels is further accelerating consumption across major Chinese cities.

Advancements in Cold-Chain Infrastructure

Significant investments in refrigerated logistics, cold storage facilities, and frozen transportation networks across Asia have improved supply chain efficiency. Countries such as China, Thailand, Malaysia, and Vietnam have expanded cold-chain capabilities, reducing spoilage and facilitating larger export volumes. These infrastructure improvements are enabling exporters to access new international markets while improving product consistency and profitability.

Growing Popularity of Asian Foods Worldwide

The globalization of Asian cuisine has increased awareness and acceptance of durian-based products. Consumers in North America, Europe, Australia, and the Middle East are increasingly exploring exotic fruits and authentic Asian food experiences. Frozen durian products allow retailers and foodservice operators to offer consistent availability without the challenges associated with fresh durian distribution, driving broader market penetration.

Frozen Durian Market Restraints

High Logistics and Refrigeration Costs

Frozen durian products require uninterrupted cold-chain transportation and storage. Energy-intensive freezing processes, refrigerated warehousing, and temperature-controlled logistics contribute significantly to operating costs. Smaller producers often struggle to compete with large exporters possessing established logistics networks, creating barriers to market entry.

Regulatory and Phytosanitary Compliance Challenges

International trade in frozen durian remains subject to strict food safety regulations, import protocols, and phytosanitary requirements. Exporters must comply with varying standards across different countries, increasing administrative complexity and compliance costs. Delays in certification or inspections can disrupt supply chains and impact profitability.

Frozen Durian Industry Key Opportunities

Expansion into Western Retail Markets

The growing popularity of Asian cuisine across North America and Europe presents substantial opportunities for frozen durian suppliers. Major supermarket chains are expanding ethnic and exotic fruit offerings, creating shelf space for frozen durian products. As consumer familiarity increases, frozen durian is expected to transition from niche ethnic stores into mainstream retail channels. Premium packaging, branding, and educational marketing campaigns can further accelerate adoption.

Growth of Food Processing and Ingredient Applications

Food manufacturers are increasingly utilizing frozen durian as an ingredient in premium desserts, dairy products, bakery items, confectionery products, and beverages. This industrial demand offers higher volume opportunities compared to direct consumer sales. Manufacturers can benefit from long-term supply agreements with food processors seeking consistent quality and reliable ingredient sourcing. New product development within premium dessert categories continues to support growth.

Government-Led Export Promotion Programs

Several producing countries, including Malaysia, Thailand, and Vietnam, are actively supporting durian exports through agricultural modernization programs, export incentives, and trade agreements. Investments in agricultural infrastructure, quality certification systems, and international marketing initiatives are improving competitiveness. Export-focused policies are expected to strengthen global supply chains and expand market access opportunities over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.06 Billion |

| Market Size in 2026 | USD 2.25 Billion |

| Market Size in 2031 | USD 3.47 Billion |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

Frozen durian pulp continues to dominate the global frozen durian market, accounting for approximately 38% of total market share in 2025. Its leadership is primarily driven by its high versatility across industrial food processing, foodservice applications, and household consumption channels. The segment benefits from the ability to eliminate labor-intensive seed removal while delivering standardized texture, flavor consistency, and extended shelf stability, which are critical requirements for large-scale manufacturers. Demand is particularly reinforced by bakery, dairy, and dessert producers that increasingly rely on tropical fruit inclusions to develop premium and differentiated offerings. The growth of ready-to-use ingredient systems in industrial kitchens further strengthens frozen pulp adoption, as it reduces preparation time and improves operational efficiency across high-volume production environments.

Durian Variety Insights

Monthong durian accounted for approximately 34% of global market revenue in 2025, maintaining its position as the leading variety segment. The segment’s dominance is primarily driven by Thailand’s strong export infrastructure and established global branding as the most reliable source of high-quality durian. Monthong’s extended shelf life, larger fruit size, and milder aroma profile compared to other varieties enhance its suitability for frozen processing and long-distance export logistics. Strong and sustained import demand from China remains the key growth driver, supported by rising disposable incomes and increasing consumer acceptance of premium tropical fruits. Additionally, consistent quality grading standards and improved cold-chain logistics across Southeast Asia continue to reinforce Monthong’s leadership in international trade flows.

Processing Technology Insights

Individually Quick Frozen (IQF) technology held nearly 44% of global market value in 2025, making it the most widely adopted processing method. The leading driver of this segment is the superior preservation of sensory and nutritional attributes, including texture integrity, aroma retention, and natural sweetness, which are critical for premium positioning in export markets. IQF technology also enables precise portion control, reduces product wastage, and enhances supply chain flexibility, making it highly suitable for both retail and foodservice applications. Growing demand from high-end import markets, where product appearance and quality consistency are key purchasing factors, continues to accelerate adoption. Furthermore, advancements in freezing efficiency and energy-optimized cryogenic systems are improving scalability and cost-effectiveness for exporters.

Packaging Type Insights

Retail pouches captured approximately 36% market share in 2025, emerging as the leading packaging format in the frozen durian market. The primary growth driver is rising consumer preference for convenience-oriented packaging solutions that support portion control, resealability, and minimal product handling. Expansion of e-commerce grocery platforms and direct-to-consumer frozen food delivery models has further reinforced demand for durable, freezer-safe pouch formats. In addition, premium branding and visually appealing packaging design are increasingly influencing purchase decisions in export markets, particularly in urban retail environments. Manufacturers are also adopting sustainable and lightweight packaging materials to align with evolving environmental regulations and consumer expectations.

Distribution Channel Insights

Modern grocery retail accounted for approximately 31% of global frozen durian sales in 2025, positioning it as the leading distribution channel. This dominance is driven by the strong expansion of organized retail infrastructure, particularly supermarkets and hypermarkets equipped with advanced cold-chain storage capabilities. Retail chains in key markets such as China, Singapore, and other metropolitan Asian cities are increasingly dedicating freezer space to premium imported tropical fruits, reflecting growing consumer willingness to explore exotic fruit categories. The channel also benefits from strong consumer trust, in-store product visibility, and promotional activities that encourage trial purchases. The integration of premium frozen fruit sections within mainstream retail outlets continues to significantly enhance product accessibility and market penetration.

Application Insights

Direct consumer consumption represented approximately 42% of global demand in 2025, maintaining its position as the largest application segment. The key driver for this segment is rising consumer preference for convenient, ready-to-eat exotic fruit products that offer year-round availability regardless of seasonal constraints. Consistency in taste and quality, combined with improved frozen storage technology, has strengthened household adoption. At the same time, food processing applications are expanding at a faster growth rate, driven by increasing incorporation of durian into value-added product categories such as ice cream, bakery fillings, confectionery, and flavored beverages. This dual demand structure reflects a maturing market where both direct consumption and industrial utilization are expanding simultaneously, with innovation-led applications expected to further accelerate segment diversification.

End-Use Insights

Food manufacturers represent the fastest-growing end-use segment in the frozen durian market, supported by increasing integration of durian ingredients across bakery, confectionery, dairy, and frozen dessert industries. The primary growth driver is rising demand for premium natural fruit flavors in processed food formulations, particularly within large-scale global food categories such as frozen desserts and bakery products. The global frozen dessert industry, valued at over USD 110 billion, and the bakery sector, exceeding USD 500 billion, continue to create substantial demand for consistent and high-quality fruit inputs. Manufacturers across China, Japan, South Korea, and Southeast Asia are increasingly leveraging frozen durian pulp and puree for product innovation, flavor differentiation, and premium product positioning. This industrial demand is expected to outpace household consumption growth through 2031, supported by continued expansion of processed food exports and R&D-driven product development.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Durian Market Segmentations

By Product Form

- Frozen Durian Pulp

- Whole Frozen Durian

- Frozen Durian Puree

- Frozen Durian Paste

- Frozen Durian Cubes & Chunks

- Frozen Durian Concentrate

By Durian Variety

- Musang King

- Monthong

- D24

- Black Thorn

- Red Prawn

- Other Commercial Varieties

By Processing Technology

- Individually Quick Frozen

- Blast Frozen

- Cryogenic Freezing

- Vacuum Frozen

- Conventional Deep Freezing

By Application

- Direct Consumption

- Frozen Desserts & Ice Cream

- Bakery & Confectionery

- Beverages & Smoothies

- Dairy Products

- Food Ingredients & Processing

- HORECA

By Distribution Channel

- Modern Grocery Retail

- E-Commerce Platforms

- Specialty Asian Stores

- Convenience Stores

- Direct Export Sales

Regional Insights

Asia-Pacific

Asia-Pacific dominated the global frozen durian market with approximately 72% revenue share in 2025, driven by strong production capabilities and exceptionally high consumer demand. China, contributing nearly 41% of global demand, remains the central consumption hub due to rising disposable incomes, expanding premium fruit consumption, and deepening penetration of imported frozen fruits. The region’s growth is primarily driven by rapid urbanization, expanding cold-chain logistics infrastructure, and increasing popularity of Southeast Asian tropical fruits in mainstream diets. Thailand continues to lead global exports with well-established processing ecosystems, while Malaysia is strengthening its position in premium Musang King exports. Vietnam is emerging as a key supply-side growth engine due to expanding cultivation areas and investment in export-oriented processing facilities. Additionally, Japan, South Korea, Singapore, and Hong Kong contribute to demand growth through premium niche consumption driven by high-income urban populations and strong culinary experimentation trends.

North America

North America accounted for approximately 9% of global demand in 2025, with the United States representing the largest consumption base. Market growth in this region is primarily driven by increasing multicultural demographics, particularly Asian immigrant populations, alongside growing mainstream acceptance of exotic and tropical fruit products. Expansion of specialty grocery chains and improved availability of frozen Asian food products in major retail networks are key growth enablers. Canada is also witnessing steady growth supported by rising imports through both ethnic grocery stores and mainstream supermarket channels. The overall regional demand is concentrated in urban metropolitan areas where exposure to international cuisines and premium frozen fruit offerings is significantly higher.

Europe

Europe represented approximately 8% of global market revenue in 2025, with demand primarily concentrated in the United Kingdom, Germany, France, and the Netherlands. The key growth driver in this region is the increasing multicultural population base combined with rising consumer interest in Asian cuisine and exotic fruit experiences. The expansion of frozen durian availability beyond ethnic grocery stores into mainstream supermarket chains is significantly enhancing accessibility and awareness. Additionally, premium food trends and growing demand for plant-based and natural fruit-based ingredients are supporting market expansion across bakery and dessert segments. Improved import logistics and regulatory standardization across the European Union are also contributing to more stable and scalable supply chains.

Latin America

Latin America accounted for approximately 4% of global demand in 2025, with Brazil and Mexico emerging as the primary consumption markets. Market growth is driven by gradual expansion of middle-class populations, increasing exposure to Asian food culture, and rising imports of exotic fruits through specialty distributors. Although the market remains relatively small, awareness is steadily increasing through urban retail penetration and foodservice adoption in premium hospitality sectors. The growing influence of global culinary trends and international tourism exposure is further contributing to incremental demand expansion. Over time, improving cold-chain logistics and retail modernization are expected to support stronger market penetration across major urban centers.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7% of global frozen durian market revenue in 2025, with the United Arab Emirates and Saudi Arabia serving as the primary import hubs. Market expansion is primarily driven by high disposable incomes, strong demand for premium imported food products, and a large expatriate population with established consumption familiarity. The region is also benefiting from rapid modernization of retail infrastructure, including expansion of premium supermarket chains and cold-storage facilities. Growth momentum is expected to remain strong, supported by rising consumer interest in luxury food experiences and diversification of retail food offerings. In Africa, gradual improvements in urban retail ecosystems and increasing exposure to international cuisines are expected to contribute to long-term demand development, albeit from a smaller base.

Key Players in the Frozen Durian Market

- Top Fruits Sdn Bhd

- Hextar Global Berhad

- Interfresh Co. Ltd.

- Thai Agri Foods Public Company Limited

- Chainoi Food Company Limited

- Xiang Wang Group

- Mao Shan Wang Holdings

- Duria International

- Dking Group

- Grand World International

- Royal Fruits Group

- Sime Darby Plantation (Durian Division)

- BMS Organics Group

- Green World Import Export

- Jfruit International