Frozen Berries Market Size

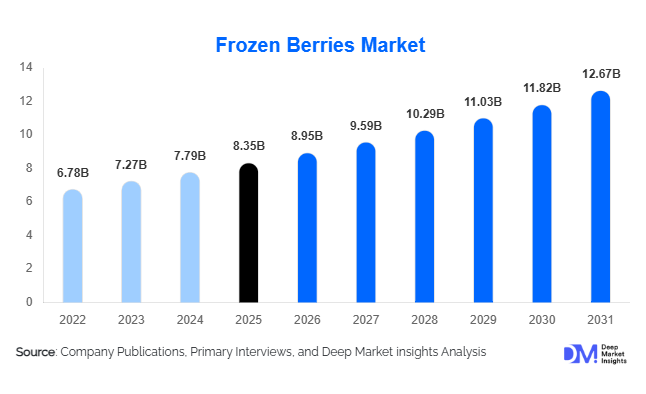

According to Deep Market Insights, the global frozen berries market size was valued at USD 8.35 billion in 2025 and is projected to grow from USD 8.95 billion in 2026 to reach USD 12.67 billion by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). The frozen berries market growth is primarily driven by increasing consumer preference for healthy and convenient food products, rising demand for antioxidant-rich ingredients, expansion of smoothie and functional beverage consumption, and growing utilization of berries across dairy, bakery, nutraceutical, and foodservice applications. Advancements in individual quick freezing (IQF) technology, expansion of cold-chain infrastructure, and increasing availability of premium and organic frozen fruit products are further supporting market expansion globally.

Key Market Insights

- Strawberries remain the largest berry category, accounting for approximately 36% of the global frozen berries market due to extensive use in dairy products, bakery applications, smoothies, and frozen desserts.

- Individual Quick Frozen (IQF) technology dominates processing, representing nearly 72% of global production owing to superior product quality, texture preservation, and shelf-life benefits.

- North America leads global consumption, accounting for approximately 32% of market revenue, supported by mature frozen food retail channels and strong demand from food processors.

- Asia-Pacific is the fastest-growing regional market, driven by rapid urbanization, increasing disposable income, and expansion of modern grocery retail formats across China and India.

- Functional nutrition and nutraceutical applications are emerging as high-growth segments, with berry powders, concentrates, and extracts witnessing increased adoption in immunity and wellness products.

- Sustainability initiatives and food waste reduction strategies are encouraging retailers and consumers to shift toward frozen fruits due to their extended shelf life and reduced spoilage compared to fresh produce.

Frozen Berries Market Latest Trends

Growing Demand for Functional and Superfood Ingredients

Frozen berries are increasingly being positioned as functional food ingredients due to their high antioxidant content, anthocyanins, vitamins, and dietary fiber. Manufacturers across dairy, beverages, and nutritional supplements are incorporating blueberries, cranberries, raspberries, and blackberries into product formulations targeted toward immunity support, digestive health, cardiovascular wellness, and sports nutrition. Consumers are increasingly seeking naturally derived ingredients with scientifically recognized health benefits, making frozen berries a preferred ingredient across clean-label product portfolios. Berry concentrates, powders, and purees are experiencing particularly strong demand from nutraceutical and functional food manufacturers seeking premium plant-based ingredients.

Expansion of Premium and Organic Frozen Fruit Offerings

Retailers and food manufacturers are expanding premium frozen fruit assortments to capitalize on growing demand for organic, sustainably sourced, and minimally processed products. Organic frozen berry sales continue to outpace conventional frozen fruit growth in developed markets, particularly across North America and Europe. Consumers increasingly value traceability, environmentally responsible sourcing, and pesticide-free cultivation practices. In response, processors are investing in certified organic berry cultivation, sustainable packaging solutions, and transparent supply chain programs. Premium mixed berry blends, smoothie kits, and value-added frozen fruit products are becoming increasingly common across supermarket freezer aisles.

Frozen Berries Market Drivers

Increasing Consumer Focus on Health and Wellness

Growing awareness regarding nutrition, immunity, and preventive healthcare is driving consumption of antioxidant-rich foods worldwide. Frozen berries retain much of their nutritional profile due to advanced freezing technologies, making them an attractive alternative to fresh berries. Consumers increasingly incorporate frozen berries into smoothies, breakfast bowls, yogurts, and healthy snacks, supporting strong demand growth across retail and foodservice channels. Rising adoption of plant-based diets and clean-label food products further strengthens long-term consumption trends.

Rapid Growth of Smoothie, Beverage, and Dairy Industries

The expansion of smoothie chains, functional beverage manufacturers, yogurt producers, and frozen dessert companies is creating substantial demand for frozen berries. Food processors prefer frozen berries because they provide consistent quality, year-round availability, and reduced spoilage compared to fresh fruit. Blueberries and strawberries remain particularly important ingredients within premium dairy products, protein beverages, and meal replacement formulations. Increasing consumer preference for convenient yet nutritious products continues to support industrial demand.

Frozen Berries Market Restraints

Volatility in Berry Production and Raw Material Availability

Berry cultivation remains highly dependent on weather conditions, making supply vulnerable to droughts, frost events, excessive rainfall, and pest infestations. Climate-related disruptions can significantly affect harvest yields and raw material pricing, creating procurement challenges for processors. Supply fluctuations often lead to temporary pricing volatility and pressure profit margins throughout the frozen berry value chain.

High Energy and Cold Storage Costs

The frozen berries industry requires continuous refrigeration throughout harvesting, processing, transportation, warehousing, and retail distribution. Rising electricity prices and increasing sustainability requirements have elevated operational costs for manufacturers and distributors. Small and medium-sized processors face particular challenges in maintaining profitability while investing in energy-efficient cold-chain infrastructure and environmentally compliant freezing technologies.

Frozen Berries Industry Key Opportunities

Expansion into Functional Nutrition and Nutraceutical Markets

The growing global nutraceutical industry presents significant opportunities for frozen berry processors to diversify beyond traditional food applications. Berry-derived powders, concentrates, extracts, and freeze-dried ingredients are increasingly utilized in dietary supplements, sports nutrition products, immunity formulations, and functional beverages. High concentrations of anthocyanins, polyphenols, and natural antioxidants provide opportunities for manufacturers to develop premium, value-added products with substantially higher margins than conventional frozen fruit offerings. Companies investing in ingredient innovation and clinical validation are likely to benefit from growing consumer demand for natural wellness solutions.

Emerging Demand Across Asia-Pacific Markets

Asia-Pacific represents the largest untapped growth opportunity for frozen berry suppliers. Rising disposable incomes, expanding organized retail networks, westernization of dietary habits, and rapid growth of online grocery platforms are accelerating frozen fruit consumption across China, India, South Korea, Thailand, and Vietnam. Foodservice operators, beverage chains, dairy manufacturers, and bakery processors are increasingly incorporating berries into product offerings. Companies establishing early supply chain infrastructure and strategic partnerships within Asia-Pacific are expected to capture significant long-term growth opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.35 Billion |

| Market Size in 2026 | USD 8.95 Billion |

| Market Size in 2031 | USD 12.67 Billion |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Berry Type Insights

Strawberries emerged as the leading berry type segment in the global frozen berries market, accounting for approximately 36% of total revenue in 2025. The segment’s dominance is primarily driven by the widespread utilization of strawberries across multiple food and beverage applications, including smoothies, yogurts, ice creams, bakery fillings, confectionery products, frozen desserts, and direct retail consumption. Their broad consumer acceptance, attractive flavor profile, year-round availability through freezing technologies, and cost-effectiveness compared to certain specialty berries continue to strengthen their market position. In addition, food manufacturers increasingly prefer frozen strawberries due to their consistent quality, extended shelf life, and ease of incorporation into processed food formulations.Raspberries and blackberries are witnessing steady expansion owing to their increasing use in premium bakery products, gourmet desserts, specialty beverages, and nutraceutical formulations. Their distinctive flavor characteristics and high concentrations of vitamins, minerals, and bioactive compounds make them attractive ingredients for value-added food products. Cranberries continue to maintain an important position within beverage, wellness, and functional food applications due to their strong association with urinary tract health and antioxidant benefits. Meanwhile, mixed berry blends are among the fastest-growing product categories, driven by consumer demand for convenience, diversified nutritional profiles, enhanced flavor combinations, and ready-to-use smoothie ingredients. The increasing popularity of blended fruit products among health-conscious consumers is expected to support continued growth across this segment throughout the forecast period.

Application Insights

Dairy products constitute the largest application segment in the frozen berries market, accounting for approximately 22% of global demand in 2025. The segment’s leadership is primarily driven by the growing incorporation of frozen berries into yogurts, probiotic products, flavored milk beverages, dairy desserts, ice creams, and cultured dairy formulations. Manufacturers increasingly utilize frozen berries to enhance product flavor, natural color, nutritional value, and consumer appeal while ensuring year-round ingredient availability and supply consistency. Rising consumer preference for healthy dairy products enriched with natural fruit ingredients continues to support segment expansion globally.Nutraceutical applications are among the fastest-growing segments within the market. Growth is fueled by increasing consumer awareness regarding immunity support, antioxidant supplementation, healthy aging, and plant-based nutrition. Frozen berries serve as important raw materials for dietary supplements, functional foods, nutraceutical beverages, and botanical extracts due to their rich content of polyphenols, vitamins, and other bioactive compounds. The continued convergence of food and healthcare trends is expected to create substantial growth opportunities for berry-based nutraceutical products over the coming years.

Distribution Channel Insights

Retail stores remain the dominant distribution channel, accounting for approximately 47% of global market revenue in 2025. The segment’s leadership is driven by the extensive availability of frozen berries across supermarkets, hypermarkets, convenience stores, and specialty food retailers. Retailers continue expanding frozen fruit offerings as consumers increasingly seek healthy, convenient, and minimally processed food products. Improved freezer infrastructure, broader product assortments, and growing demand for ready-to-use ingredients continue to strengthen retail channel performance worldwide.Foodservice distribution remains an important channel, supplying restaurants, smoothie chains, cafés, hotels, bakeries, and institutional food providers with frozen berry ingredients. Growing demand for fruit-based menu offerings, healthy beverages, and premium desserts is driving procurement volumes within the foodservice sector. Industrial ingredient suppliers also represent a significant distribution segment, serving large-scale food manufacturers operating across dairy, bakery, beverage, confectionery, and nutritional product industries where frozen berries are utilized as key production inputs.

End User Insights

The food processing industry represents the largest end-user segment, accounting for approximately 41% of global frozen berry consumption in 2025. The segment’s dominance is primarily attributed to the extensive use of frozen berries in the production of dairy products, bakery items, beverages, desserts, snacks, and functional foods. Food manufacturers increasingly rely on frozen berries because they provide consistent quality, reliable year-round availability, stable pricing, and reduced raw material wastage compared to fresh fruit alternatives. These operational advantages enable manufacturers to maintain production efficiency and supply chain reliability.Retail consumers are also contributing significantly to market growth as frozen berries gain popularity for home consumption. Consumers increasingly appreciate frozen berries for their convenience, long shelf life, reduced food waste, and ability to provide year-round access to nutritious fruit. Nutraceutical manufacturers represent the fastest-growing end-user segment, driven by rising demand for berry-derived extracts, powders, concentrates, supplements, and functional beverage ingredients that support wellness, immunity, and preventive health objectives.

Packaging Type Insights

Flexible pouches dominate the frozen berries market and account for approximately 48% of global revenue in 2025. The leading position of this segment is primarily driven by the growing preference for lightweight, cost-efficient, and convenient packaging solutions that enhance product handling and storage efficiency. Flexible packaging reduces transportation costs, optimizes shelf utilization, improves product visibility, and helps maintain product freshness throughout the distribution process. These advantages have made flexible pouches the preferred packaging format among both manufacturers and consumers.Sustainability considerations are becoming increasingly important across the packaging landscape. Retailers, food manufacturers, and consumers are placing greater emphasis on recyclable, reusable, and environmentally responsible packaging solutions. Consequently, investments in sustainable packaging innovations are expected to increase significantly as market participants seek to align with evolving environmental regulations and consumer preferences.

Explore more data points, trends and opportunities Download Free Sample Report

Frozen Berries Market Segmentations

By Berry Type

- Strawberries

- Blueberries

- Raspberries

- Blackberries

- Cranberries

- Mixed Berry Blends

- Other Berries

By Freezing Technology

- Individual Quick Frozen (IQF)

- Block Frozen

- Freeze-Dried Frozen Berries

- Cryogenic Frozen Berries

By Product Form

- Whole Berries

- Sliced/Cut Berries

- Crushed Berries

- Berry Purees

- Berry Concentrates

- Berry Powders

- Berry Mixes/Blends

By Application

- Dairy Products

- Bakery & Confectionery

- Beverages

- Breakfast Foods & Cereals

- Frozen Desserts & Ice Cream

- Smoothies & Functional Nutrition

- Jams, Preserves & Spreads

- Nutraceuticals & Dietary Supplements

- Infant Nutrition

- Direct Consumption

By Distribution Channel

- Retail Stores

- Online Retail/E-Commerce

- Foodservice Distribution

- Industrial Ingredient Suppliers

Regional Insights

North America

North America accounted for approximately 32% of global frozen berries market revenue in 2025, making it the largest regional market. The United States dominates regional consumption owing to strong demand from food processors, dairy manufacturers, beverage producers, smoothie chains, and retail consumers. Frozen berries are widely incorporated into health-conscious dietary patterns, supporting sustained demand across multiple application categories. Canada also represents a significant market, benefiting from increasing consumer preference for nutritious frozen foods and expanding foodservice utilization.Regional growth is supported by several structural factors, including highly developed cold-chain infrastructure, widespread penetration of organized retail networks, strong consumer awareness regarding healthy eating habits, growing demand for functional and antioxidant-rich foods, and increasing consumption of smoothies and plant-based nutritional products. The presence of leading frozen food manufacturers, advanced food processing capabilities, and continuous product innovation further contribute to North America's market leadership.

Europe

Europe represented approximately 30% of global frozen berries demand in 2025 and remains one of the most mature and well-established markets worldwide. Germany, the United Kingdom, France, Italy, and Spain serve as major consumption centers, while Poland plays a critical role as a leading producer and exporter supplying frozen berries across the region. Demand for frozen berries continues to benefit from the region’s strong culture of fruit consumption and widespread adoption of frozen food products.Market growth in Europe is driven by increasing demand for organic and clean-label products, growing emphasis on sustainable sourcing practices, rising popularity of premium frozen fruit offerings, and strong consumer preference for traceable food products. Additionally, expanding applications in bakery, dairy, beverage, and functional food sectors continue to generate demand. Regulatory support for food quality standards, coupled with increasing environmental consciousness and investments in sustainable packaging solutions, further strengthens long-term market development across the region.

Asia-Pacific

Asia-Pacific accounted for approximately 22% of global market revenue in 2025 and is projected to be the fastest-growing regional market through 2031. China remains the largest contributor to regional growth due to rapid urbanization, expanding middle-class populations, rising disposable incomes, and increasing adoption of frozen food products. India is emerging as one of the fastest-growing country markets, supported by expanding modern retail infrastructure, growing health awareness, increasing smoothie consumption, and changing dietary preferences among younger consumers. Japan and South Korea continue to generate stable demand through their mature frozen food industries and preference for premium fruit products.The region's growth is further supported by rising investments in cold-chain logistics, rapid expansion of e-commerce grocery platforms, increasing demand for convenience foods, growing participation of women in the workforce, and greater awareness regarding the nutritional benefits of berries. The rising popularity of functional foods, wellness beverages, and western-style dietary habits is also accelerating frozen berry consumption across key Asia-Pacific economies.

Latin America

Latin America accounted for approximately 9% of global market revenue in 2025. Brazil and Mexico represent the largest consuming markets, while Chile serves as a major production and export hub supplying frozen berries to North America, Europe, and other international markets. The region continues to benefit from improving consumer access to frozen food products and expanding food processing activities.Key growth drivers include increasing urbanization, rising disposable incomes, expanding penetration of supermarkets and hypermarkets, growing consumer awareness regarding healthy eating, and greater adoption of convenience-oriented food products. Furthermore, rising demand from beverage manufacturers, foodservice operators, and dairy producers is creating new opportunities for frozen berry suppliers. Export-oriented berry cultivation and investments in food processing infrastructure are also supporting regional market expansion.

Middle East & Africa

The Middle East & Africa accounted for approximately 7% of global frozen berries market demand in 2025. The United Arab Emirates, Saudi Arabia, South Africa, and Israel represent the primary consumption markets within the region. Demand is largely concentrated in urban centers where consumers exhibit increasing interest in premium imported food products and healthy lifestyle choices.Regional growth is driven by the expansion of modern retail formats, increasing tourism-related foodservice demand, rising disposable incomes, growing awareness of nutrition and wellness, and improving accessibility of imported frozen food products. Investments in cold storage facilities, refrigerated transportation networks, and food distribution infrastructure are enhancing product availability across multiple countries. In addition, the growing popularity of smoothies, functional beverages, and premium dessert offerings is supporting frozen berry demand throughout the region. Among all countries globally, India is expected to register one of the highest growth rates during the forecast period, reflecting the significant growth potential emerging across developing economies.

Key Players in the Frozen Berries Market

- SunOpta

- Nature's Touch

- Polarica Group

- Euroberry

- Sicoly

- Dirafrost

- Ardo

- Agrana Fruit

- Milne Fruit Products

- Fruveco

- Polproduct

- Frulact

- I.Q.F. Foods

- Valio

- Greenyard