Global Fried Puffed Food Market Size

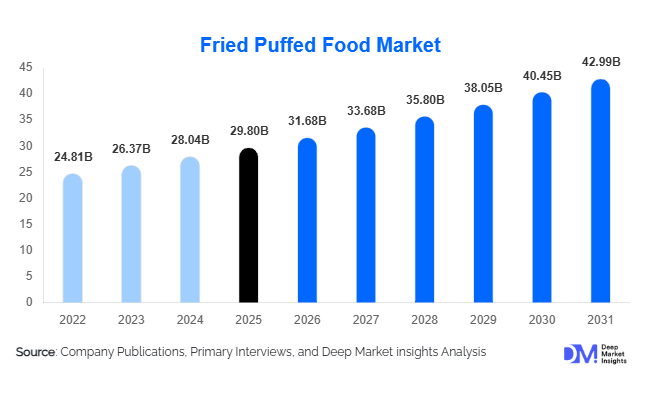

According to Deep Market Insights, the global fried puffed food market size was valued at USD 29.8 billion in 2025 and is projected to grow from USD 31.68 billion in 2026 to reach USD 42.99 billion by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The market growth is primarily driven by increasing global snack consumption, expanding urban populations, rising demand for convenient ready-to-eat foods, and continuous innovation in flavors, ingredients, and processing technologies. Fried puffed foods remain one of the most consumed snack categories worldwide, benefiting from strong consumer acceptance across both developed and emerging markets.

Key Market Insights

- Corn-based fried puffed snacks dominate the global market, accounting for approximately 31% of total industry revenue due to their affordability, scalability, and widespread consumer acceptance.

- Asia-Pacific leads global consumption, representing nearly 42% of worldwide demand, supported by strong snack penetration in China, India, Indonesia, Thailand, and Japan.

- Health-oriented product innovation is reshaping product development, with manufacturers introducing high-protein, multigrain, low-sodium, and clean-label puffed snacks.

- E-commerce is emerging as one of the fastest-growing distribution channels, enabling brands to directly engage consumers and launch premium snack portfolios.

- Advanced extrusion technologies are improving production efficiency, reducing manufacturing costs while enabling innovative shapes, textures, and formulations.

- Sustainable packaging adoption is accelerating globally, driven by regulatory requirements and increasing consumer preference for environmentally responsible products.

Global Fried Puffed Food Market Latest Trends

Health-Focused Puffed Snacks Gaining Momentum

The fried puffed food industry is experiencing a significant shift toward healthier product formulations. Consumers increasingly seek snacks containing whole grains, plant proteins, natural seasonings, reduced sodium, and lower oil content. Manufacturers are responding by launching chickpea puffs, lentil puffs, millet-based snacks, and protein-enriched products targeting health-conscious consumers. The clean-label movement is also influencing purchasing decisions, encouraging companies to eliminate artificial additives and preservatives. Premium snack brands are increasingly positioning fried puffed products as permissible indulgences, balancing taste with nutritional benefits. This trend is particularly prominent across North America and Western Europe, where consumers are willing to pay premium prices for healthier snack alternatives.

Regional Flavor Innovation Driving Consumer Engagement

Flavor innovation remains one of the most powerful growth drivers within the fried puffed food market. Manufacturers are continuously introducing region-specific flavors inspired by local cuisines, including spicy chili variants in Asia, barbecue flavors in North America, peri-peri seasonings in Africa, and Mediterranean-inspired flavors in Europe. Fusion flavors combining sweet, savory, and spicy elements are attracting younger consumers seeking unique snacking experiences. Limited-edition launches and seasonal flavor introductions are increasingly being used to drive repeat purchases and strengthen brand differentiation. Artificial intelligence and consumer analytics are also helping manufacturers identify emerging taste preferences and accelerate product development cycles.

Global Fried Puffed Food Market Drivers

Growing Global Snacking Culture

Changing lifestyles, increasing urbanization, and busier work schedules have fundamentally transformed eating habits worldwide. Consumers increasingly prefer multiple snacking occasions throughout the day rather than traditional meal patterns. Fried puffed snacks benefit significantly from this trend due to their convenience, portability, affordability, and widespread availability. The growing prevalence of work-from-home arrangements and hybrid work environments has further increased at-home snack consumption. Emerging economies continue to witness rising snack penetration as disposable incomes increase and modern retail infrastructure expands.

Expansion of Organized Retail and Modern Trade Channels

The rapid growth of supermarkets, hypermarkets, convenience stores, and online retail platforms has significantly improved product accessibility and visibility. Modern retail environments provide manufacturers with opportunities to showcase premium product offerings, launch new flavors, and execute promotional campaigns effectively. Organized retail expansion across India, Southeast Asia, Latin America, and Africa is particularly supporting volume growth. Additionally, the emergence of quick-commerce platforms is creating new distribution opportunities for snack manufacturers, enabling faster product delivery and increased impulse purchases.

Continuous Product Innovation and Premiumization

Innovation remains a key driver of market expansion. Manufacturers are investing heavily in new ingredients, advanced extrusion technologies, flavor development, and packaging solutions. Premium fried puffed snacks featuring gourmet seasonings, international flavors, and functional ingredients are attracting higher-income consumers. Product diversification enables brands to address multiple consumer segments simultaneously, ranging from value-oriented consumers to premium snack purchasers. Companies are also leveraging limited-edition launches and collaborative product development to maintain consumer interest and drive market growth.

Global Fried Puffed Food Market Restraints

Growing Health Concerns Related to Fried Snacks

Increasing awareness regarding obesity, cardiovascular diseases, and dietary health is creating challenges for traditional fried puffed food manufacturers. Regulatory authorities across multiple countries are introducing stricter nutritional labeling requirements and encouraging sodium and fat reduction initiatives. Health-conscious consumers are increasingly evaluating ingredient lists and nutritional profiles before making purchasing decisions. These factors are encouraging manufacturers to invest in healthier formulations while maintaining product taste and texture.

Volatility in Raw Material Prices

The industry remains highly dependent on agricultural commodities such as corn, potatoes, rice, vegetable oils, and seasonings. Fluctuations in commodity prices caused by adverse weather conditions, geopolitical tensions, transportation disruptions, and supply chain constraints can significantly impact manufacturing costs. Rising packaging material prices further contribute to cost pressures. Companies must continuously optimize procurement strategies and production efficiency to maintain profitability amid volatile input costs.

Global Fried Puffed Food Industry Key Opportunities

Expansion in Emerging Consumer Markets

Emerging economies present substantial growth opportunities for fried puffed food manufacturers. Countries including India, Indonesia, Vietnam, Nigeria, Brazil, and Mexico continue to experience rising disposable incomes, urbanization, and increasing demand for packaged food products. Affordable pack sizes, localized flavors, and expanding retail infrastructure provide favorable conditions for market penetration. Companies capable of tailoring products to regional preferences can establish strong market positions while benefiting from relatively low per-capita snack consumption compared to mature markets.

Premium and Functional Snack Development

The growing demand for healthier and value-added snacks creates significant opportunities for innovation. High-protein puffs, multigrain snacks, gluten-free products, organic variants, and fortified formulations are gaining traction globally. Functional ingredients such as plant proteins, probiotics, and dietary fibers are increasingly being incorporated into snack products. Premium positioning allows manufacturers to achieve higher profit margins while addressing evolving consumer expectations regarding health and wellness.

E-Commerce and Direct-to-Consumer Expansion

Digital retail channels are transforming the snack industry by enabling direct consumer engagement and reducing reliance on traditional intermediaries. Online platforms provide opportunities to launch niche products, test new flavors, and gather valuable consumer insights. Subscription snack services, customized product bundles, and social media-driven marketing campaigns are creating new revenue streams. Younger consumers increasingly discover and purchase snack products through digital channels, making e-commerce a critical growth opportunity for industry participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 29.80 Billion |

| Market Size in 2026 | USD 31.68 Billion |

| Market Size in 2031 | USD 42.99 Billion |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Corn-based fried puffed snacks continue to represent the largest product category in the global fried puffed food market, accounting for approximately 31% of total market revenue in 2025. The segment maintains its leadership due to the widespread availability of corn as a cost-effective raw material, high production scalability, and exceptional versatility in flavor application and product formulation. Manufacturers favor corn-based products because extrusion and frying processes can efficiently produce a broad range of textures, shapes, and taste profiles while maintaining competitive pricing. The segment also benefits from strong consumer familiarity across both developed and emerging markets, making it a preferred choice for mass-market snack brands and private-label manufacturers.Multigrain and legume-based puffed snacks are emerging as some of the fastest-growing product categories as consumers increasingly seek products perceived as healthier, more nutritious, and protein-rich. Growing awareness regarding balanced diets, functional ingredients, and better-for-you snacking is encouraging manufacturers to expand product portfolios featuring lentils, chickpeas, peas, quinoa, and mixed grains. Meanwhile, tapioca and cassava-based puffed snacks continue gaining popularity across Southeast Asia and Latin America due to abundant local raw material availability, established consumption habits, and increasing commercialization of traditional snack formats. The growing emphasis on ingredient diversification and nutritional enhancement is expected to further support innovation across all product categories during the forecast period.

Processing Technology Insights

Extrusion-fried snacks dominate the global fried puffed food industry, representing approximately 63% of total market value in 2025. The segment's leadership is primarily driven by the superior production efficiency, scalability, and product consistency offered by extrusion technology. Extrusion enables manufacturers to produce large volumes while maintaining uniform texture, shape, and expansion characteristics, making it highly suitable for commercial snack manufacturing. The technology also supports extensive product customization, allowing companies to rapidly develop new shapes, flavors, and formulations that cater to evolving consumer preferences.Advancements in extrusion systems are further strengthening segment growth. Twin-screw extrusion technologies are witnessing increased adoption among leading manufacturers due to their ability to process complex ingredient blends, improve product quality, and enhance operational flexibility. These systems facilitate the incorporation of functional ingredients, alternative grains, legumes, and protein-enriched formulations, supporting the industry's shift toward premium and health-oriented snack products.Pellet-based expanded snacks continue to hold an important position within the market, particularly in value-oriented product categories and price-sensitive emerging economies. Pellet technologies offer manufacturers production flexibility and lower distribution costs while enabling localized flavor customization. Continued investments in process optimization, automation, and energy-efficient manufacturing technologies are expected to further enhance productivity and profitability across both extrusion-based and pellet-based snack production systems.

Flavor Category Insights

Plain and salted products account for nearly 28% of global market demand, making them the largest flavor category within the fried puffed food market. The segment's dominance is primarily driven by its broad consumer appeal, universal acceptance across age groups, and compatibility with diverse dietary preferences. Plain and salted variants also benefit from their affordability, wide retail availability, and suitability as everyday snack options, supporting consistent demand across both developed and emerging markets.Cheese-based flavors continue to maintain strong popularity throughout North America and Europe, where consumers increasingly seek indulgent and savory snacking experiences. At the same time, spicy, chili-based, and regionally inspired flavors are gaining significant traction across Asia-Pacific, Latin America, and parts of the Middle East as manufacturers capitalize on growing demand for bold and culturally relevant taste profiles. Localized flavor development has become a key competitive strategy, enabling brands to strengthen regional market penetration and improve consumer engagement.Fusion flavors that combine sweet, savory, spicy, and umami characteristics are increasingly attracting younger consumers seeking novel and differentiated snacking experiences. As consumer preferences become more diverse and experimental, manufacturers continue investing heavily in flavor innovation, sensory research, and limited-edition product launches. The increasing importance of flavor differentiation as a purchasing factor is expected to remain a major driver of market competitiveness and product innovation throughout the forecast period.

Distribution Channel Insights

Hypermarkets and supermarkets remain the leading distribution channel, contributing approximately 38% of global fried puffed food sales in 2025. The segment's leadership is primarily driven by extensive product visibility, broad brand assortment, strong promotional capabilities, and convenient one-stop shopping experiences. Large retail chains enable manufacturers to achieve substantial product reach while providing consumers with access to a diverse range of snack formats, flavors, and packaging options.Convenience stores continue to represent an important distribution channel, particularly in densely populated urban markets where impulse purchases account for a significant share of snack consumption. Their strategic locations, extended operating hours, and focus on ready-to-consume products support consistent demand for fried puffed snacks among commuters, students, and working professionals.Online retail is emerging as one of the fastest-growing channels, supported by rising internet penetration, increasing smartphone adoption, expanding e-commerce ecosystems, and growing consumer preference for home delivery services. Direct-to-consumer strategies, subscription snack programs, and digital marketing initiatives are further strengthening online sales performance. Specialty food stores are also expanding their market presence, particularly within premium, organic, clean-label, and health-focused snack categories, reflecting broader consumer interest in differentiated and value-added products.

End-Use Insights

Household consumers account for approximately 81% of global fried puffed food consumption, making them the dominant end-use segment. The segment's leadership is primarily driven by rising at-home snacking occasions, increasing demand for convenient packaged foods, and the growing popularity of family-sized and multipack snack formats. Busy lifestyles, expanding urban populations, and changing eating habits continue to encourage frequent snack consumption across both developed and emerging economies.The growing integration of snacks into daily routines, including between-meal consumption, entertainment activities, social gatherings, and work-from-home lifestyles, continues to strengthen household demand. Manufacturers are increasingly introducing innovative packaging formats, portion-controlled offerings, and value packs to address evolving consumer preferences and maximize household penetration.Foodservice operators represent a rapidly expanding end-use segment, supported by growing demand across cinemas, quick-service restaurants, entertainment venues, sports facilities, and travel hubs. Institutional demand from schools, universities, hospitals, and corporate cafeterias is also increasing, particularly across Asia-Pacific and other developing regions where organized foodservice infrastructure continues to expand. Furthermore, airlines, railway catering providers, tourism operators, and hospitality establishments are creating additional opportunities for packaged snack suppliers as travel activity and tourism-related consumption continue to recover and grow globally.

Explore more data points, trends and opportunities Download Free Sample Report

Fried Puffed Food Market Segmentations

By Product Type

- Potato-Based Fried Puffed Snacks

- Corn-Based Fried Puffed Snacks

- Rice-Based Fried Puffed Snacks

- Multigrain Fried Puffed Snacks

- Legume-Based Fried Puffed Snacks

- Tapioca & Cassava-Based Fried Puffed Snacks

By Processing Technology

- Extrusion-Fried Puffed Snacks

- Pellet-Based Fried Expanded Snacks

- Pressure-Puffed Fried Snacks

- Twin-Screw Extruded Fried Snacks

- Single-Screw Extruded Fried Snacks

By Flavor Category

- Plain/Salty

- Cheese-Based

- Barbecue & Smoke

- Spicy/Hot

- Sweet

- Fusion & Regional Flavors

By Distribution Channel

- Hypermarkets & Supermarkets

- Convenience Stores

- Traditional Grocery Retail

- Specialty Food Stores

- Online Retail & E-Commerce

- Foodservice & Vending

By End User

- Household Consumers

- Foodservice Operators

- Institutional Buyers

- Travel & Leisure Channels

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global fried puffed food market, accounting for approximately 42% of total market revenue in 2025. The region's leadership is supported by its large population base, rapid urbanization, expanding middle-class population, increasing disposable incomes, and strong cultural acceptance of packaged snack foods. Growing modernization of retail channels, rising penetration of convenience stores, and the rapid expansion of e-commerce platforms are further accelerating market development across the region.China represents the largest individual market globally, accounting for nearly 16% of worldwide demand. Strong consumer spending, widespread snack consumption habits, and continuous product innovation by domestic and international manufacturers continue to support market growth. India contributes approximately 9% of global revenue and remains one of the fastest-growing markets, driven by rising urban populations, increasing household incomes, expanding organized retail infrastructure, and growing demand for affordable convenience foods. Japan continues to drive premiumization and product innovation through advanced flavor development and high-quality snack offerings, while Indonesia, Thailand, and Vietnam benefit from favorable demographics, increasing retail penetration, rising youth populations, and growing consumption of modern packaged food products. The region also benefits from strong local agricultural production of corn, rice, cassava, and tapioca, ensuring stable raw material availability and supporting large-scale manufacturing activities.

North America

North America accounts for approximately 24% of global market revenue, led predominantly by the United States. The region benefits from some of the highest per-capita snack consumption levels globally, well-established distribution networks, strong brand recognition, and continuous investments in product innovation. Consumers increasingly incorporate snacks into daily meal occasions, supporting sustained demand across multiple product categories.Market growth is being driven by premiumization trends, increasing demand for clean-label products, flavor experimentation, convenience-oriented consumption patterns, and the growing popularity of protein-enriched and better-for-you snack alternatives. Manufacturers continue introducing innovative formulations that address evolving consumer preferences for healthier ingredients while maintaining indulgent taste experiences. Canada remains an important contributor to regional growth, particularly within premium, natural, and health-focused snack segments. Strong retail infrastructure, advanced marketing capabilities, and high consumer purchasing power continue to reinforce North America's position as a mature yet innovative market.

Europe

Europe represents approximately 20% of global market demand, with Germany, the United Kingdom, France, Italy, and Spain serving as the region's primary consumption centers. The market is characterized by sophisticated consumer preferences, strong regulatory standards, and growing demand for high-quality packaged food products.Regional growth is primarily driven by increasing consumer preference for clean-label ingredients, reduced-fat formulations, natural flavorings, and environmentally sustainable packaging solutions. Rising health consciousness is encouraging manufacturers to reformulate products and introduce innovative snack options that align with evolving nutritional expectations. Premium snack categories continue to gain momentum, supported by consumer willingness to pay higher prices for perceived quality, transparency, and sustainability. Western Europe remains highly competitive due to strong private-label participation, while Eastern European markets are benefiting from rising disposable incomes, urbanization, and expanding modern retail infrastructure.

Latin America

Latin America accounts for approximately 8% of global market revenue, with Brazil and Mexico representing the largest contributors to regional demand. Growing urban populations, increasing workforce participation, and changing dietary habits are contributing to higher consumption of convenient packaged snack products across the region.Regional growth is supported by improving retail infrastructure, rising household incomes, expanding supermarket penetration, and increasing availability of affordable snack products. Manufacturers are actively introducing localized flavors and culturally relevant product innovations to cater to diverse consumer preferences and strengthen brand loyalty. Growing investments in domestic food processing capabilities, combined with abundant agricultural resources such as corn and cassava, are further supporting market expansion. The increasing influence of modern retail formats and digital commerce channels is expected to create additional growth opportunities throughout the forecast period.

Middle East & Africa

The Middle East & Africa region contributes nearly 6% of global demand and continues to offer significant long-term growth potential. Market expansion is supported by favorable demographic trends, rapid population growth, increasing urbanization, and rising consumer spending on packaged food products.Saudi Arabia, the UAE, South Africa, Egypt, and Nigeria represent the region's major markets, benefiting from expanding retail networks, growing youth populations, and increasing adoption of modern snacking habits. Rising disposable incomes, greater exposure to international food brands, and ongoing development of organized retail channels are accelerating demand for fried puffed snack products. In addition, increasing investments in food manufacturing, improvements in distribution infrastructure, and the expansion of convenience retail formats are supporting broader market accessibility. The region's young demographic profile and growing preference for on-the-go food consumption are expected to remain key growth drivers over the forecast period.

Key Players in the Global Fried Puffed Food Market

- PepsiCo

- Kellanova

- Intersnack Group

- Calbee Inc.

- Mondelez International

- Orkla ASA

- Want Want China Holdings

- Universal Robina Corporation

- ITC Limited

- Bikaji Foods International

- Balaji Wafers

- Grupo Bimbo

- Meiji Holdings

- Nongshim

- Arca Continental