Fried Chicken Market Size

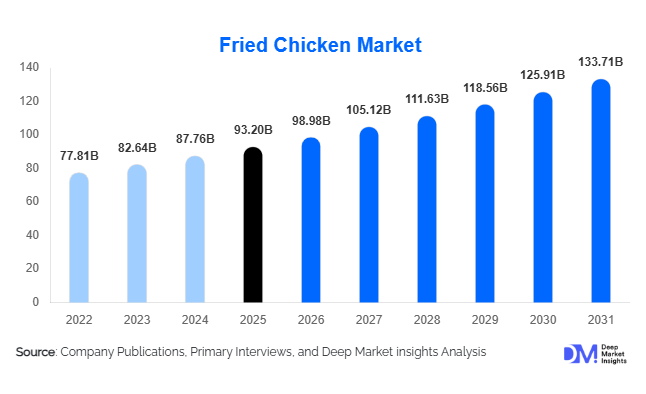

According to Deep Market Insights, the global fried chicken market size was valued at USD 93.2 billion in 2025 and is projected to grow from USD 98.98 billion in 2026 to reach USD 133.71 billion by 2031, expanding at a CAGR of 6.2% during the forecast period (2026–2031). The fried chicken market growth is primarily driven by expanding quick-service restaurant (QSR) networks, rising global poultry consumption, rapid adoption of food delivery platforms, and increasing consumer preference for convenient protein-rich meals. The category continues to benefit from menu innovation, premium flavor introductions, digital ordering ecosystems, and strong demand across both developed and emerging economies. Growth is particularly pronounced in Asia-Pacific, where urbanization, rising disposable incomes, and increasing penetration of international foodservice brands are creating substantial opportunities for market participants.

Key Market Insights

- Quick-service restaurants remain the dominant sales channel, accounting for nearly half of global fried chicken revenues through extensive franchise networks and digital ordering capabilities.

- Asia-Pacific is the fastest-growing regional market, supported by strong demand in China, India, Indonesia, South Korea, and the Philippines.

- Bone-in fried chicken continues to lead product demand, representing the largest product segment due to value perception and consumer preference for traditional offerings.

- Food delivery and cloud kitchen models are transforming industry economics, enabling rapid market penetration with lower capital investments.

- Premiumization trends are accelerating globally, driven by Korean fried chicken, gourmet chicken sandwiches, specialty seasonings, and artisanal preparation methods.

- Automation and AI-powered restaurant technologies are improving operational efficiency, inventory management, customer engagement, and order fulfillment.

Fried Chicken Market Latest Trends

Premium and Regional Flavor Innovation Accelerating Growth

The fried chicken market is experiencing significant product diversification through premium menu offerings and regional flavor innovations. Korean fried chicken, Nashville hot chicken, Cajun-inspired recipes, Japanese karaage, and Southeast Asian flavor profiles are rapidly expanding beyond their domestic markets. Consumers increasingly seek unique culinary experiences while maintaining familiarity with chicken-based meals. Restaurant operators are responding through limited-time offers, premium sauces, specialty coatings, and customized seasoning blends that support higher margins. Premium chicken sandwich categories continue to gain momentum globally, creating a new avenue for differentiation among major chains. This trend is particularly strong among younger consumers seeking social-media-friendly food experiences and premium dining options at accessible price points.

Digital Ordering and Delivery-Led Expansion

The rapid growth of online food delivery platforms has fundamentally transformed the fried chicken industry. Mobile ordering, loyalty applications, third-party delivery aggregators, and cloud kitchen concepts have expanded customer reach and improved transaction frequency. Digital channels now account for a growing share of fried chicken sales in major metropolitan markets. Artificial intelligence is increasingly being deployed to optimize pricing, inventory planning, demand forecasting, and personalized promotions. Delivery-only brands are leveraging lower operating costs to enter highly competitive urban markets, while established chains continue investing in omnichannel customer engagement strategies. The integration of predictive analytics and automated kitchen technologies is expected to further enhance operational efficiency over the forecast period.

Fried Chicken Market Drivers

Growing Global Consumption of Poultry Protein

Chicken remains one of the most widely consumed proteins globally due to its affordability, versatility, and broad cultural acceptance. Compared with beef and pork, poultry faces fewer dietary and religious restrictions, making it accessible across diverse consumer populations. Rising disposable incomes, expanding urban populations, and increasing protein consumption in emerging economies continue to strengthen demand for fried chicken products. Poultry production growth across major producing nations such as the United States, Brazil, China, and Thailand is further supporting long-term market expansion.

Rapid Expansion of Quick-Service Restaurant Chains

The continued expansion of international and regional QSR operators remains a major growth driver. Franchising models allow companies to scale rapidly while maintaining operational consistency and brand recognition. Major fried chicken chains are aggressively expanding across Asia-Pacific, the Middle East, and Africa to capitalize on rising urbanization and changing dining habits. The ability to combine dine-in, takeaway, drive-thru, and delivery services enhances market accessibility and supports higher customer acquisition rates.

Food Delivery Ecosystem Development

The proliferation of food delivery applications and digital payment systems has significantly increased fried chicken consumption frequency. Consumers increasingly prioritize convenience, leading to strong growth in delivery-driven orders. Delivery platforms allow brands to expand beyond traditional trade areas and efficiently serve densely populated urban markets. The emergence of cloud kitchens and delivery-only brands further enhances scalability while reducing capital expenditure requirements.

Fried Chicken Market Restraints

Volatility in Poultry and Edible Oil Prices

Raw material costs remain one of the largest operational challenges for fried chicken producers and restaurant operators. Chicken meat, edible oils, flour, seasonings, and packaging materials account for a significant share of total costs. Price volatility driven by supply chain disruptions, feed costs, disease outbreaks, and geopolitical factors can significantly impact profitability. Operators often face challenges in passing these costs directly to consumers without affecting demand.

Increasing Health and Nutrition Concerns

Consumers are becoming more conscious of calorie intake, fat content, sodium levels, and overall nutritional quality. Fried foods are frequently scrutinized within public health discussions, particularly in developed markets. Regulatory requirements related to nutritional labeling and ingredient transparency are increasing globally. These trends require companies to invest in healthier cooking methods, improved ingredient quality, and alternative preparation technologies such as air-frying and reduced-oil processing.

Fried Chicken Industry Key Opportunities

Expansion Across Emerging Markets

Emerging economies present significant growth opportunities due to increasing disposable incomes, urbanization, and changing dietary habits. Markets such as India, Indonesia, Vietnam, Saudi Arabia, Egypt, and Nigeria remain underpenetrated relative to developed economies. International and regional brands can capitalize on these opportunities through localized menu offerings, franchise partnerships, and affordable pricing strategies. As modern retail and foodservice infrastructure continues to develop, demand for fried chicken is expected to increase substantially.

Health-Focused Product Innovation

The growing consumer focus on wellness creates opportunities for healthier fried chicken alternatives. Air-fried products, antibiotic-free poultry, clean-label ingredients, organic chicken, and lower-sodium formulations are gaining traction among health-conscious consumers. Brands capable of balancing taste, convenience, and nutrition can capture premium customer segments while improving long-term brand perception. Product innovation in healthier preparation methods is expected to become a key competitive differentiator.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 93.20 Billion |

| Market Size in 2026 | USD 98.98 Billion |

| Market Size in 2031 | USD 133.71 Billion |

| CAGR | 6.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Bone-in fried chicken continues to dominate the global market, accounting for approximately 43% of total revenues, largely driven by its strong association with traditional consumption formats, perceived authenticity, and superior flavor retention during frying. Its leadership is reinforced by long-established quick-service restaurant (QSR) bucket meals and value-driven sharing formats, which continue to resonate strongly across both developed and emerging markets. Drumsticks, thighs, wings, and mixed buckets remain central to menu architectures, particularly where affordability and portion-based pricing strategies are critical to demand generation. Boneless fried chicken products, including tenders, strips, and popcorn chicken, are expanding at a faster pace, supported by rising demand for convenience-oriented eating, on-the-go snacking, and delivery-optimized menu items that offer ease of consumption without compromise on taste experience. Fried chicken sandwiches and burgers have emerged as one of the most dynamic growth categories globally, fueled by aggressive premiumization strategies, limited-time offerings, and competitive menu innovation among leading QSR and fast-casual operators. Value-added fried chicken products featuring specialty coatings, stuffed formats, and regionally inspired flavor infusions are increasingly driving premium segment expansion as consumers seek differentiated and experiential dining options.

Preparation Method Insights

Pressure-fried chicken remains the leading preparation method globally, contributing approximately 38% of market revenues, with its dominance primarily driven by its ability to deliver consistent product quality, improved moisture retention, reduced oil absorption, and high operational efficiency in high-volume QSR environments. This method is particularly favored by large franchise networks seeking standardization, faster throughput, and improved kitchen productivity. Deep-fried chicken continues to hold a substantial share due to its low equipment barrier, widespread culinary familiarity, and adaptability across both formal and informal foodservice settings. Double-fried chicken is gaining strong traction in premium and specialty restaurant formats, particularly within Korean fried chicken concepts, where its defining driver is the pursuit of superior crisp texture, extended crunch retention, and differentiated sensory experience. Air-fried chicken is emerging as a fast-growing niche segment, primarily driven by rising health consciousness, demand for lower-fat alternatives, and increasing adoption of modern kitchen technologies in both home consumption and select foodservice applications.

Flavor Profile Insights

Classic or original flavor profiles continue to lead the global fried chicken market with approximately 36% share, supported by their universal acceptance, broad demographic appeal, and strong alignment with traditional QSR offerings where consistency and familiarity drive repeat purchases. Spicy and extra-spicy variants are experiencing accelerated growth, primarily driven by younger consumer cohorts, social media-influenced food trends, and the rising global appetite for bold, sensory-intensive flavor experiences. Regional flavor innovation is emerging as a key growth engine for category expansion, with Korean, Japanese, Cajun, Nashville hot, and Southeast Asian-inspired profiles increasingly integrated into mainstream menus, driven by globalization of taste preferences and cross-cultural culinary adoption. Sweet-and-savory flavor combinations are also gaining momentum in premium and limited-time offerings, where operators leverage flavor novelty and experimentation as strategic tools to enhance differentiation, drive trial, and increase consumer engagement in highly competitive markets.

Service Channel Insights

Quick-service restaurants dominate the fried chicken market with approximately 49% share of global revenues, a leadership position primarily driven by extensive franchise penetration, strong brand equity, standardized operating models, and robust omnichannel integration across dine-in, takeaway, and delivery platforms. The segment’s growth is further reinforced by continuous menu innovation and aggressive expansion strategies in both urban and suburban markets. Casual dining and fast-casual restaurants maintain a strong position in the competitive landscape by emphasizing premium ingredients, experiential dining environments, and higher-margin menu offerings that cater to evolving consumer expectations for quality and ambiance. Cloud kitchens and ghost kitchens represent the fastest-growing service channel, with growth driven by the rapid expansion of food delivery ecosystems, reduced real estate costs, and data-driven menu optimization strategies that prioritize delivery-friendly product formats. Independent outlets and street food vendors continue to play a vital role in emerging economies, where affordability, localized taste preferences, and informal food distribution networks remain key demand drivers.

Customer Group Insights

Individual consumers account for approximately 54% of global fried chicken consumption, with growth primarily driven by urbanization, increasing single-person households, busy lifestyles, and the rising prevalence of convenience-based meal consumption patterns. This segment benefits significantly from expanding delivery platforms and ready-to-eat food availability. Family consumers represent a substantial and stable demand base, with growth supported by sharing-oriented meal formats such as bucket meals, combo packs, and value bundles that emphasize affordability and collective consumption occasions. Institutional buyers, including hotels, restaurants, catering services, airlines, educational institutions, healthcare facilities, and corporate cafeterias, continue to generate significant volume demand, driven by large-scale procurement needs, standardized meal programs, and expanding organized foodservice infrastructure. Growth in global travel, tourism recovery, and outsourcing of foodservice operations is further strengthening institutional demand across both developed and emerging regions.

Explore more data points, trends and opportunities Download Free Sample Report

Fried Chicken Market Segmentations

By Product Type

- Bone-In Fried Chicken

- Boneless Fried Chicken

- Fried Chicken Sandwiches & Burgers

- Value-Added Fried Chicken Products

By Preparation Method

- Deep-Fried

- Pressure-Fried

- Air-Fried Commercial Products

- Double-Fried Premium Products

By Flavor Profile

- Original/Classic

- Spicy

- Extra Spicy/Hot

- Sweet & Savory

- Regional Flavors

By Consumption Format

- Ready-to-Eat (RTE)

- Ready-to-Heat (RTH)

- Ready-to-Cook (RTC)

By Service Channel

- Quick Service Restaurants (QSR)

- Casual Dining Restaurants

- Fast Casual Restaurants

- Cloud Kitchens/Ghost Kitchens

- Street Food & Independent Outlets

Regional Insights

North America

North America accounted for approximately 37% of global fried chicken market revenues in 2025, making it the most mature and largest regional market, with growth primarily driven by high per-capita consumption, deep QSR penetration, and strong franchise-led expansion across urban and suburban areas. The United States remains the core growth engine due to continuous menu innovation, premium sandwich offerings, and strong integration of digital ordering and delivery ecosystems that enhance accessibility and convenience. Canada is experiencing steady growth supported by premium fried chicken concepts and increasing adoption of international flavors, while Mexico benefits from rapid urbanization, expanding middle-class consumption, and the continued penetration of global restaurant chains. The region’s growth is further reinforced by advanced logistics infrastructure, high digital ordering adoption, and strong consumer responsiveness to product innovation and limited-time offerings.

Asia-Pacific

Asia-Pacific accounts for approximately 31% of global market revenues and represents the fastest-growing regional market, with growth exceeding 8% annually, driven by rapid urbanization, rising disposable incomes, and expanding middle-class populations. China leads regional demand due to its large urban consumer base, sophisticated food delivery ecosystems, and strong penetration of both domestic and international QSR brands. India is emerging as one of the fastest-growing markets globally, supported by rapid expansion of organized foodservice chains, increasing youth population, and rising preference for Western-style fast food formats. South Korea plays a pivotal role in global product innovation, particularly through the worldwide influence of Korean fried chicken, while Southeast Asian markets such as Indonesia, Thailand, Vietnam, and the Philippines are witnessing strong demand growth driven by digital food delivery platforms, street food culture evolution, and increasing urban consumer spending. The primary regional growth drivers include expanding digital ecosystems, rising affordability of QSR meals, and strong cultural acceptance of fried chicken as a mainstream protein choice.

Europe

Europe represents approximately 18% of global market revenues, with growth primarily driven by increasing demand for premium fast food experiences, rising adoption of food delivery services, and evolving consumer preferences toward protein-rich and convenient meal options. The United Kingdom leads the regional market, supported by strong QSR penetration, multicultural food influences, and rapid expansion of fried chicken-focused restaurant chains. Germany, France, Spain, and Italy are experiencing steady growth fueled by menu diversification, premium product positioning, and increasing openness to international flavor profiles. A key regional driver is the growing consumer emphasis on quality sourcing, sustainability, and healthier preparation methods, which is encouraging innovation in product formulation and cooking techniques. Additionally, the expansion of fast-casual dining formats and delivery-first restaurant models is accelerating market penetration across major European cities.

Latin America

Latin America accounts for approximately 6% of global fried chicken revenues, with Brazil emerging as the dominant market due to its strong poultry production base, established foodservice culture, and high domestic consumption levels. The region’s growth is primarily driven by rising urbanization, increasing penetration of international QSR brands, and improving restaurant infrastructure across major cities. Mexico and Argentina are also witnessing steady expansion supported by franchise development and growing middle-class food expenditure. A key growth driver in the region is the strong alignment between fried chicken offerings and affordability-focused consumer behavior, making it a preferred protein option across income segments. Additionally, expanding delivery services and increasing investment in organized retail food outlets are further supporting long-term market development.

Middle East & Africa

The Middle East and Africa region contributes approximately 8% of global fried chicken demand, with growth concentrated in urban centers and tourism-driven economies. The Gulf Cooperation Council (GCC) countries, particularly Saudi Arabia and the United Arab Emirates, represent the largest and most dynamic markets, driven by high disposable incomes, strong international franchise penetration, and a strong preference for convenient dining experiences. South Africa remains the most developed market in Sub-Saharan Africa, supported by established QSR networks and growing urban middle-class consumption. Meanwhile, Egypt and Nigeria are emerging as high-potential markets due to rapid population growth, increasing urbanization, and expanding investments in organized foodservice infrastructure. Regional growth is further supported by tourism inflows, youth-dominated demographics, and rising adoption of Western fast-food concepts across major metropolitan areas.