Filled Pasta Market Size

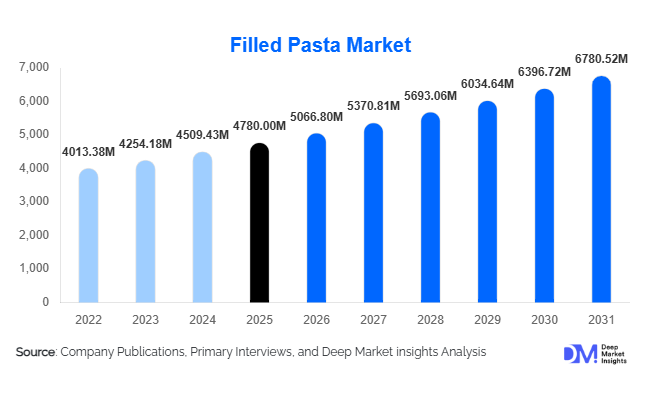

According to Deep Market Insights, the global filled pasta market size was valued at USD 4,780 million in 2025 and is projected to grow from USD 5,066.80 million in 2026 to reach USD 6,780.52 million by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The filled pasta market growth is primarily driven by increasing demand for premium convenience foods, rising global adoption of Italian cuisine, and continuous product innovations in fresh, frozen, and plant-based stuffed pasta products. Growing consumer preference for restaurant-quality meals at home, coupled with expanding retail distribution and cold-chain infrastructure, is supporting the penetration of filled pasta products across both developed and emerging economies.

Key Market Insights

- Fresh and refrigerated filled pasta remains the largest category, accounting for approximately 45% of global market revenues due to premium positioning and superior taste perception.

- Cheese-filled pasta dominates product demand, representing nearly 37% of total market consumption owing to its widespread consumer acceptance across vegetarian and mainstream diets.

- Europe leads the global market, accounting for nearly 43% of global revenues, supported by strong culinary traditions and extensive manufacturing capabilities.

- Asia-Pacific is the fastest-growing regional market, with demand increasing due to westernization of food habits and rising disposable incomes in China and India.

- Household consumers account for the majority of demand, representing approximately 58% of total consumption as consumers increasingly seek convenient meal solutions.

- Plant-based and functional filled pasta products are gaining traction, creating opportunities for premium product development and category expansion.

- E-commerce and meal-kit platforms are becoming increasingly important distribution channels, improving product accessibility and boosting premium product sales globally.

Filled Pasta Market Latest Trends

Plant-Based and Functional Filled Pasta Gaining Momentum

Consumer preferences are shifting toward healthier and sustainable food choices, driving demand for plant-based and functional filled pasta products. Manufacturers are introducing vegan cheese alternatives, legume-based proteins, and nutrient-enriched fillings to attract health-conscious consumers. Gluten-free and high-protein stuffed pasta varieties are also witnessing strong adoption among consumers seeking healthier convenience foods. Premium retailers and specialty stores are increasingly allocating shelf space to these products, while foodservice operators are expanding their menus with vegan and flexitarian filled pasta options. This trend is expected to significantly reshape product development strategies across the industry.

Premiumization and Gourmet Fillings Driving Product Innovation

The market is witnessing a strong shift toward premium and artisanal filled pasta products featuring gourmet ingredients such as truffles, specialty cheeses, seafood, and organic vegetables. Consumers increasingly perceive filled pasta as a premium meal solution that offers restaurant-quality dining experiences at home. Manufacturers are investing in innovative fillings, sustainable packaging, and clean-label formulations to differentiate their offerings. The trend toward premiumization has enabled companies to command higher margins while appealing to affluent consumers willing to pay more for unique culinary experiences.

Filled Pasta Market Drivers

Rising Demand for Convenience and Ready-to-Cook Foods

Busy lifestyles, urbanization, and increasing workforce participation have significantly increased demand for convenient meal solutions worldwide. Filled pasta products require minimal preparation and provide consumers with restaurant-quality meals within a short preparation time. The growing convenience food industry, particularly in North America and Europe, has become a major demand driver for fresh, frozen, and shelf-stable stuffed pasta products.

Global Popularity of Italian Cuisine

Italian cuisine remains one of the most widely consumed international cuisines globally. Increased travel, globalization, social media influence, and the expansion of Italian restaurant chains have improved consumer awareness and acceptance of filled pasta products in emerging markets. Countries across Asia-Pacific and Latin America are increasingly adopting premium Italian food products, creating substantial long-term growth opportunities for market participants.

Premiumization and Product Diversification

Consumers are increasingly willing to spend on premium convenience foods featuring organic ingredients, authentic recipes, and gourmet fillings. Manufacturers are introducing artisanal recipes, plant-based options, and premium packaging formats to capture higher-value consumer segments. Premiumization has significantly enhanced revenue growth and profitability across the filled pasta industry.

Filled Pasta Market Restraints

Raw Material Price Volatility

The industry remains highly exposed to fluctuations in the prices of wheat, cheese, dairy products, meat, and vegetables. Rising agricultural commodity prices can significantly impact production costs and profit margins, particularly for manufacturers operating in the premium segment where ingredient quality is critical.

Cold Chain and Distribution Challenges

Fresh and refrigerated filled pasta products require advanced cold-chain infrastructure to maintain product quality and shelf life. In many developing markets, limited refrigerated logistics capabilities and higher transportation costs continue to restrict market expansion and increase operational complexities.

Filled Pasta Industry Key Opportunities

Expansion into Emerging Markets

Emerging economies such as China, India, Indonesia, Vietnam, and Brazil are witnessing rapid growth in premium packaged food consumption. Increasing disposable incomes, urbanization, and exposure to international cuisines are creating significant opportunities for filled pasta manufacturers. Modern retail expansion and rising penetration of organized foodservice channels further support long-term demand growth in these markets.

Growth of Meal Kits and Ready Meals

The increasing popularity of meal kits and ready-to-eat meals is creating substantial opportunities for filled pasta manufacturers. Meal-kit providers and frozen meal producers are increasingly incorporating stuffed pasta products due to their convenience, premium appeal, and versatility. Manufacturers capable of developing portion-controlled and microwave-ready products are expected to benefit considerably from this trend.

Development of Plant-Based and Functional Products

The global shift toward healthier and sustainable food consumption presents substantial opportunities for product innovation. Vegan fillings, gluten-free products, fortified pasta, and high-protein formulations are attracting health-conscious consumers and allowing manufacturers to command premium pricing.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4780.00 Million |

| Market Size in 2026 | USD 5066.80 Million |

| Market Size in 2031 | USD 6780.52 Million |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The ravioli segment dominated the global filled pasta market and accounted for approximately 33% of total market revenues in 2025. The segment's leadership is primarily driven by its widespread consumer familiarity, extensive product availability across retail and foodservice channels, and the versatility of fillings that cater to diverse taste preferences and dietary requirements. Ravioli products are available in fresh, frozen, refrigerated, and shelf-stable formats, making them highly accessible to both household and commercial consumers. In addition, manufacturers continue to introduce premium and gourmet variants featuring artisanal ingredients, organic formulations, and innovative fillings, further strengthening the segment's market position. The increasing demand for convenient meal solutions and the expansion of ready-to-cook food categories have also significantly contributed to the segment's growth.Tortellini represents the second-largest product category, supported by its strong consumption base in Europe and North America where Italian cuisine enjoys widespread popularity. The segment benefits from increasing demand for authentic and premium pasta offerings, particularly among consumers seeking restaurant-quality meals at home. Meanwhile, specialty products such as cappelletti, agnolotti, girasoli, and other regional Italian filled pasta varieties are gaining significant traction in premium and artisanal food segments. These products are increasingly favored by consumers seeking unique culinary experiences, premium ingredients, and authentic Italian flavors. Frozen and gourmet ravioli products continue to witness robust demand growth, particularly through modern retail formats and e-commerce platforms, where premium convenience foods are experiencing strong consumer acceptance.

Filling Type Insights

Cheese-based fillings represent the largest filling category, accounting for approximately 37% of global demand in 2025. The segment's dominance is largely attributable to the broad consumer acceptance of cheese-filled products, their compatibility with vegetarian diets, and the growing preference for comfort foods featuring familiar flavors. Ricotta, mozzarella, parmesan, and mixed cheese combinations remain the preferred options due to their versatility and ability to appeal to diverse demographic groups. Furthermore, the increasing popularity of premium and indulgent food products has encouraged manufacturers to introduce gourmet cheese blends and specialty formulations, supporting continued segment growth.Meat-based fillings continue to perform strongly across North America and Europe, supported by high consumption of traditional Italian dishes and increasing demand for protein-rich meal options. Fillings containing beef, chicken, pork, and cured meats remain particularly popular among consumers seeking hearty and satiating meal experiences. Meanwhile, vegetable-based and plant-based fillings are projected to register the fastest growth during the forecast period owing to rising health consciousness, growing vegan and flexitarian populations, and increasing consumer demand for clean-label and sustainable food products. The expansion of plant-based food innovation and the incorporation of ingredients such as spinach, mushrooms, pumpkin, and legumes are further accelerating growth within this segment. Seafood-filled products continue to occupy a niche but premium position in the market, particularly in developed economies where consumers are willing to pay higher prices for gourmet and specialty offerings.

Distribution Channel Insights

Supermarkets and hypermarkets account for nearly 48% of global sales, making them the leading distribution channel for filled pasta products. The segment's dominance is primarily driven by extensive product assortments, well-developed refrigerated and frozen storage infrastructure, and strong penetration of private-label offerings that enhance product affordability and accessibility. Large retail chains also provide significant shelf visibility and promotional opportunities, enabling manufacturers to introduce new product variants and premium offerings to a broad consumer base. The increasing consumer preference for one-stop shopping destinations and the expansion of organized retail networks across emerging economies continue to strengthen the market position of this distribution channel.Specialty food retailers and gourmet stores maintain strong performance within premium product categories by offering artisanal, imported, and organic filled pasta products that cater to discerning consumers. Meanwhile, online retail and direct-to-consumer channels are witnessing rapid growth due to increasing digital grocery adoption, rising internet penetration, and the convenience associated with home delivery services. The emergence of meal-kit providers and subscription-based food services is further creating new avenues for premium and specialty filled pasta products, particularly among urban consumers seeking convenient meal preparation solutions and restaurant-quality dining experiences at home.

End User Insights

Household consumers account for approximately 58% of global filled pasta demand, making them the largest end-user segment in the market. The segment's leadership is driven by increasing at-home meal preparation, rising consumer preference for premium convenience foods, and growing demand for quick and easy meal solutions that require minimal preparation time. The expansion of dual-income households, busy lifestyles, and increasing availability of premium frozen and refrigerated pasta products have further accelerated household consumption. In addition, growing interest in international cuisines and authentic Italian dishes has contributed significantly to rising demand among home consumers.Restaurants and quick-service establishments represent rapidly growing end-user categories, benefiting from increasing global consumption of Italian cuisine and the operational efficiencies associated with pre-prepared filled pasta products. Filled pasta products enable foodservice operators to maintain consistency, reduce preparation times, and offer premium menu options while optimizing labor costs. Industrial food processors are also becoming increasingly important customers as demand for ready meals, frozen dinners, and convenience food products continues to rise globally. The incorporation of filled pasta into packaged meal solutions and premium frozen food offerings is expected to create additional growth opportunities for manufacturers over the forecast period.

Explore more data points, trends and opportunities Download Free Sample Report

Filled Pasta Market Segmentations

By Product Type

- Ravioli

- Tortellini

- Cappelletti

- Agnolotti

- Cannelloni

- Mezzelune

- Girasoli

- Sacchettini/Fagottini

- Other Specialty Filled Pasta

By Filling Type

- Cheese-Based Fillings

- Meat-Based Fillings

- Seafood-Based Fillings

- Vegetable-Based Fillings

- Plant-Based/Vegan Fillings

By Product Form

- Fresh/Refrigerated Filled Pasta

- Frozen Filled Pasta

- Shelf-Stable/Ambient Filled Pasta

- Dried Filled Pasta

By Ingredient Composition

- Conventional Wheat-Based

- Whole Wheat

- Gluten-Free

- Organic

- High-Protein/Enriched

- Functional & Fortified

By Packaging Format

- Bags/Pouches

- Trays

- Boxes/Cartons

- Vacuum Packs

- Family-Size Multipacks

Regional Insights

North America

North America accounted for approximately 27% of global market revenues in 2025, with the United States representing nearly 22% of global demand. The region's growth is supported by strong consumer preference for premium convenience foods, increasing demand for refrigerated and frozen meal solutions, and growing adoption of gourmet and restaurant-inspired products. Rising consumption of Italian cuisine, expanding premium private-label offerings, and the increasing popularity of clean-label and organic food products are further contributing to market expansion. The rapid growth of e-commerce grocery platforms and meal-kit delivery services has also improved product accessibility and consumer penetration. Canada represents a significant market due to high consumption of frozen and premium pasta products, supported by strong retail infrastructure and increasing demand for convenient meal solutions.

Europe

Europe dominates the global filled pasta market with approximately 43% market share in 2025. Italy remains the largest producer and consumer globally, accounting for nearly 15% of worldwide demand, followed by Germany, France, and the United Kingdom. The region's leadership is underpinned by deeply rooted culinary traditions, high per capita pasta consumption, and extensive manufacturing capabilities. Regional growth is further driven by increasing demand for authentic Italian products, rising premiumization trends, growing consumer preference for artisanal and organic food products, and continuous product innovation by leading manufacturers. The expansion of premium retail channels and increasing export demand for high-quality Italian filled pasta products continue to reinforce Europe's dominant market position.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, with projected growth exceeding 8% annually during the forecast period. China and India are emerging as key demand centers due to rapid urbanization, expanding middle-class populations, increasing disposable incomes, and greater exposure to Western food products and international cuisines. The proliferation of organized retail, growing penetration of frozen and convenience food categories, and rising adoption of premium packaged foods are creating substantial opportunities for market participants. In addition, changing dietary habits among younger consumers and the rapid expansion of foodservice chains offering international cuisines are accelerating market growth. Japan and Australia remain established markets characterized by premium product demand, sophisticated retail infrastructure, and strong consumer willingness to spend on high-quality imported and gourmet food products.

Latin America

Brazil and Mexico dominate the regional market due to increasing consumption of international cuisines and the growing presence of modern retail chains. Rising disposable incomes, urbanization, and changing dietary preferences are creating favorable conditions for market expansion across the region. The increasing penetration of supermarkets and hypermarkets, coupled with growing demand for premium and convenience food products, is further supporting market growth. Additionally, expanding foodservice sectors, increasing tourism activities, and rising exposure to European and North American culinary trends are contributing to higher consumption of filled pasta products. Long-term opportunities are also emerging from the increasing adoption of frozen foods and premium packaged meal solutions.

Middle East & Africa

The UAE, Saudi Arabia, and South Africa represent the largest markets within the Middle East & Africa region. Market growth is primarily supported by increasing tourism activities, rising premium food consumption, and the rapid expansion of hospitality and foodservice sectors. The region is also benefiting from growing imports of premium Italian food products and increasing consumer exposure to international cuisines through travel and global restaurant chains. Rising disposable incomes, expanding expatriate populations, and increasing demand for convenience-oriented premium food products are further driving market development. Additionally, the ongoing expansion of modern retail infrastructure and premium grocery formats is improving product availability and supporting the long-term growth prospects of the filled pasta market across the region.

Key Players in the Filled Pasta Market

- Barilla Group

- Giovanni Rana

- Nestlé S.A.

- Ebro Foods S.A.

- Newlat Food S.p.A.

- Pastificio Lucio Garofalo S.p.A.

- Ugo Foods Group

- Voltan S.p.A.

- RP's Pasta Company

- Pappardelle's Pasta

- Armanino Foods of Distinction Inc.

- Lilly's Fresh Pasta

- Pasta Evangelists

- BRE.MA.A Group

- Fresh Pasta Company