Donuts Market Size

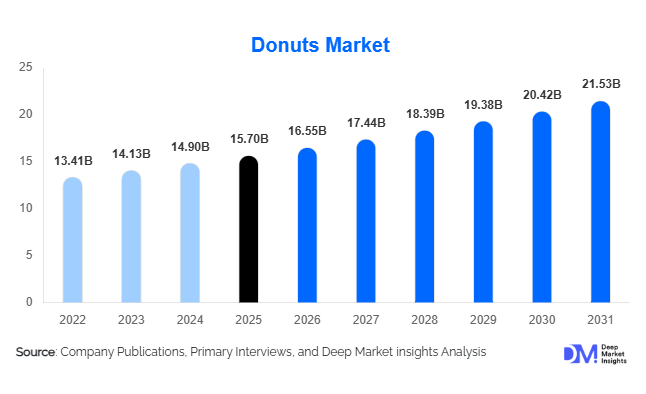

According to Deep Market Insights, the global donuts market size was valued at USD 15.7 billion in 2025 and is projected to grow from USD 16.55 billion in 2026 to reach USD 21.53 billion by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). The donuts market growth is primarily driven by rising demand for convenient snack foods, increasing café culture penetration, rapid expansion of quick-service restaurant chains, and growing consumer preference for premium and gourmet bakery products. Product innovation across health-oriented variants such as vegan, gluten-free, baked, and protein-enriched donuts is also supporting long-term market expansion globally.

Key Market Insights

- Premium and artisanal donuts are witnessing significant growth, supported by consumer demand for unique flavors, gourmet toppings, and limited-edition offerings.

- Quick-service restaurant chains and café outlets remain the dominant sales channels, benefiting from breakfast bundling and impulse snack purchases.

- North America dominates the global donuts market, accounting for the largest share due to high per capita bakery consumption and extensive franchise penetration.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization, rising disposable incomes, and westernized eating habits.

- Health-oriented donut categories are expanding rapidly, including vegan, low-sugar, gluten-free, baked, and protein-fortified products.

- Digital food delivery and cloud kitchen models are reshaping the market, improving accessibility and increasing repeat online bakery purchases.

donuts market latest trends

Premiumization and Gourmet Product Innovation

The global donuts market is increasingly shifting toward premium and artisanal product offerings. Consumers are seeking gourmet donuts featuring imported ingredients, handcrafted toppings, premium fillings, and fusion flavors inspired by global cuisines. Seasonal products, limited-edition launches, and visually appealing donuts designed for social-media engagement are becoming critical growth strategies for bakery chains and specialty cafés. Premium donuts are generating significantly higher margins compared to conventional offerings, encouraging operators to expand gourmet product portfolios. Urban consumers in the United States, Japan, South Korea, the United Kingdom, and the UAE are particularly driving this trend, with demand for dessert-style donuts and café-integrated bakery experiences continuing to rise. Brands are also collaborating with confectionery manufacturers, coffee brands, and entertainment franchises to create exclusive product launches that enhance consumer engagement and repeat purchases.

Health-Oriented and Functional Donuts Gaining Popularity

Growing health awareness among consumers is encouraging bakery manufacturers to develop healthier donut alternatives. Vegan donuts, baked donuts, gluten-free variants, low-sugar products, and protein-enriched formulations are becoming increasingly mainstream across developed markets. Functional bakery innovation is helping brands attract younger and health-conscious consumers who seek indulgent snacks with improved nutritional profiles. Ingredient reformulation using natural sweeteners, plant-based dairy alternatives, and high-fiber ingredients is expanding rapidly. This trend is particularly strong in Europe and North America, where regulatory pressure around sugar reduction and nutritional transparency continues to intensify. Companies are additionally focusing on clean-label product positioning, sustainable sourcing, and preservative-free recipes to differentiate themselves in an increasingly competitive bakery market.

donuts market drivers

Growing Demand for Convenient Snacking

Rising urbanization and fast-paced consumer lifestyles are significantly increasing demand for ready-to-eat snack products globally. Donuts remain highly attractive due to their affordability, portability, flavor diversity, and compatibility with coffee and beverage consumption. The increasing popularity of breakfast-on-the-go culture is driving strong sales through quick-service restaurants, convenience stores, and café chains. Working professionals and younger consumers are increasingly incorporating donuts into breakfast and mid-day snacking routines. Expanding retail availability across supermarkets, transit hubs, airports, and online delivery platforms is further supporting market growth.

Expansion of Organized Bakery and Café Chains

The rapid expansion of global and regional bakery café chains is accelerating donuts market growth across emerging economies. Franchise-driven expansion strategies are enabling brands to penetrate underdeveloped urban markets across Asia-Pacific, the Middle East, and Latin America. International bakery chains are increasingly localizing flavors and product assortments to match regional consumer preferences. Café culture growth, especially among millennials and Gen Z consumers, is also boosting donut consumption through bundled coffee-and-donut offerings. Investments in automated bakery production technologies and centralized commissary systems are improving scalability, consistency, and operational efficiency for large chains.

donuts market restraints

Health Concerns Related to Sugar and Fat Consumption

One of the major restraints impacting the donuts market is increasing consumer awareness regarding obesity, diabetes, and excessive sugar consumption. Donuts are commonly perceived as indulgent products with high calorie and fat content, causing some health-conscious consumers to reduce consumption frequency. Governments across several developed economies are also strengthening nutritional labeling regulations and encouraging sugar reduction initiatives, which may negatively impact traditional donut categories. The challenge for manufacturers lies in balancing indulgence with healthier ingredient formulations while maintaining taste and texture quality.

Raw Material Price Volatility

Fluctuations in the prices of wheat flour, edible oils, cocoa, dairy ingredients, sugar, and specialty fillings continue to create operational challenges for donut manufacturers and bakery chains. Geopolitical disruptions, agricultural supply shortages, and transportation cost inflation have increased ingredient price volatility globally. Smaller bakery operators are particularly vulnerable to rising input costs, as they often face difficulties passing higher prices onto consumers in competitive and price-sensitive markets. Energy costs associated with bakery operations and food manufacturing also remain an ongoing challenge for industry participants.

donuts industry key opportunities

Digital Bakery Retail and Cloud Kitchen Expansion

The rapid growth of digital food delivery ecosystems presents a major opportunity for donut brands globally. Online ordering platforms, mobile applications, and cloud kitchen models are transforming consumer purchasing behavior by improving accessibility and convenience. Donut brands are increasingly adopting hybrid operating models combining dine-in retail stores with delivery-focused kitchens to expand urban reach while reducing operational costs. Emerging markets such as India, Indonesia, Brazil, and the UAE are witnessing particularly strong growth in online bakery consumption. Subscription-based breakfast offerings and personalized digital promotions are also helping brands improve customer retention and increase average order values.

Growth of Health-Focused and Functional Bakery Products

The increasing consumer preference for healthier indulgence products is creating substantial opportunities for innovation within the donuts market. Vegan, low-calorie, baked, organic, gluten-free, and protein-fortified donuts are expected to outperform traditional categories in several developed markets over the forecast period. Companies investing in functional ingredients, natural sweeteners, and clean-label positioning are likely to gain competitive advantages among younger and health-conscious consumers. Fitness-oriented bakery products targeting active lifestyles and meal-replacement snacking are additionally creating new niche revenue streams for bakery operators and packaged food manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.70 Billion |

| Market Size in 2026 | USD 16.55 Billion |

| Market Size in 2031 | USD 21.53 Billion |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Yeast donuts dominate the global market and account for nearly 42% of total industry revenue due to their soft texture, strong compatibility with glazed and filled formats, and widespread adoption across quick-service restaurant chains. Cake donuts remain highly popular in North America and Europe because of their dense texture and versatility in flavored and old-fashioned varieties. Filled donuts, particularly chocolate-filled, custard-filled, and fruit-filled variants, continue to gain popularity in premium bakery segments due to higher consumer preference for indulgent products. Specialty and gourmet donuts are experiencing rapid growth, supported by artisanal toppings, imported ingredients, and visually distinctive product presentation. Health-oriented donut categories, including vegan and baked variants, are emerging strongly among younger urban consumers seeking healthier bakery alternatives.

Application Insights

Breakfast consumption remains the largest application segment in the donuts market, accounting for approximately 39% of global demand. Coffee-and-donut combinations offered by quick-service restaurants and café chains continue to reinforce breakfast-oriented purchasing patterns. Mid-day snacking represents another major application area, particularly among working professionals and students seeking convenient snack products. Dessert-oriented donut consumption is growing rapidly in premium bakery cafés and gourmet dessert outlets where donuts are increasingly positioned as indulgent specialty products. Celebration and gifting applications are also expanding through customized donuts, seasonal packaging, and premium assortments designed for festivals, birthdays, and corporate gifting. Demand from food delivery platforms is additionally increasing home-based donut consumption globally.

Distribution Channel Insights

Quick-service restaurants and bakery café chains collectively represent the leading distribution channel, accounting for nearly 46% of global market revenue. Strong brand visibility, standardized quality, and bundled beverage offerings continue to support dominance in this segment. Independent bakeries remain important in regional markets, particularly for artisanal and locally customized donut varieties. Supermarkets and convenience stores are witnessing strong growth in packaged ready-to-eat donuts targeted at impulse snack buyers. Online delivery platforms are among the fastest-growing channels globally, supported by mobile ordering applications, cloud kitchen expansion, and rising digital food consumption trends. Direct-to-consumer bakery websites and subscription-based delivery models are additionally emerging as new customer engagement channels.

Consumer Group Insights

Millennials and Gen Z consumers account for a major share of global donut consumption due to their preference for experiential food products, social-media-driven food trends, and café culture participation. Working professionals remain a critical consumer segment because of strong demand for convenient breakfast and snack options. Family consumers continue to drive significant demand through bulk purchases and value-oriented assortments sold through supermarkets and bakery chains. Premium consumers are increasingly supporting growth in gourmet and artisanal donut categories, particularly across developed urban markets. Health-conscious consumers are emerging as a rapidly growing demographic for vegan, gluten-free, baked, and reduced-sugar donut products.

Price Category Insights

Mid-range donuts dominate the global market and account for nearly 50% of industry revenue due to their affordability and broad consumer accessibility. Economy donuts continue to generate high-volume sales across developing markets and convenience retail channels where price sensitivity remains significant. Premium and gourmet donuts are witnessing the fastest growth rates globally, supported by consumer willingness to pay higher prices for artisanal toppings, imported ingredients, customized flavors, and premium presentation. Gourmet donut cafés are increasingly positioning products as affordable luxury desserts, enabling operators to achieve significantly higher profit margins compared to conventional bakery formats.

Explore more data points, trends and opportunities Download Free Sample Report

Donuts Market Segmentations

By Product Type

- Yeast Donuts

- Cake Donuts

- Filled Donuts

- Specialty & Gourmet Donuts

- Health-Oriented Donuts

By Flavor Profile

- Chocolate

- Vanilla

- Fruit-Based

- Coffee-Flavored

- Cinnamon & Spice

- Nut-Based

- Savory Donuts

By Preparation Method

- Fried Donuts

- Baked Donuts

- Air-Fried Donuts

By Distribution Channel

- Quick Service Restaurants (QSRs)

- Bakery Chains

- Independent Bakeries

- Cafés & Coffee Chains

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Delivery Platforms

- Direct-to-Consumer Online Stores

By Consumer Group

- Children

- Millennials & Gen Z Consumers

- Working Professionals

- Family Consumers

- Health-Conscious Consumers

- Premium Consumers

Regional Insights

North America

North America remains the largest regional market and accounted for approximately 38% of global donuts market revenue in 2025. The United States alone contributes nearly 31% of total global demand due to extensive franchise penetration, high per capita bakery consumption, and strong breakfast culture integration. Established quick-service restaurant chains, premium café networks, and convenience-oriented consumer behavior continue to support regional market leadership. Canada also demonstrates strong growth due to rising café culture and increasing demand for premium bakery products. Health-oriented donuts and gourmet artisanal varieties are increasingly gaining popularity across major metropolitan markets.

Europe

Europe accounts for approximately 24% of global market revenue, with the United Kingdom, Germany, France, Spain, and Italy representing the largest regional markets. European consumers increasingly prefer artisanal, organic, and baked donut variants due to strong health-awareness trends. Vegan and gluten-free donut categories are expanding rapidly across Western Europe, supported by growing demand for clean-label bakery products. Premium bakery cafés and dessert-focused retail formats are also contributing to regional market expansion. The United Kingdom remains one of the largest European markets due to strong café culture adoption and rising demand for gourmet bakery products.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is expected to record a CAGR exceeding 7% during the forecast period. China, Japan, South Korea, India, and Southeast Asia are driving strong regional demand due to urbanization, rising disposable income, and westernized eating habits. Japan and South Korea represent mature premium donut markets characterized by high demand for seasonal and gourmet offerings. India is witnessing rapid growth through organized bakery chains, shopping mall retail, and digital food delivery expansion. China continues to attract substantial international franchise investment due to increasing urban consumer spending and growing café culture penetration.

Latin America

Latin America represents a steadily expanding market led by Brazil and Mexico. Rising urban bakery consumption, growing middle-class income, and increasing franchise presence are supporting market growth across the region. Consumers increasingly prefer affordable snack products sold through convenience stores, supermarkets, and bakery cafés. International donut brands are also expanding through localized product offerings and franchise partnerships to strengthen regional market presence.

Middle East & Africa

The Middle East & Africa region is witnessing strong growth in premium donut consumption, particularly across GCC countries such as the UAE and Saudi Arabia. Expanding mall culture, café chains, tourism activity, and young consumer demographics are contributing significantly to regional demand. South Africa remains an important developing market for bakery chains and café operators. Rising disposable income and increasing exposure to westernized bakery products are supporting long-term market expansion across major urban centers within the region.

Key Players in the Donuts Market

- Dunkin’

- Krispy Kreme

- Tim Hortons

- Mister Donut

- J.CO Donuts & Coffee

- Daylight Donuts

- Shipley Do-Nuts

- Donut King

- Duck Donuts

- Mad Over Donuts

- Honey Dew Donuts

- Federal Donuts

- Round Rock Donuts

- Winchell’s Donut House

- Paris Baguette