Cut Flower Packaging Market Size

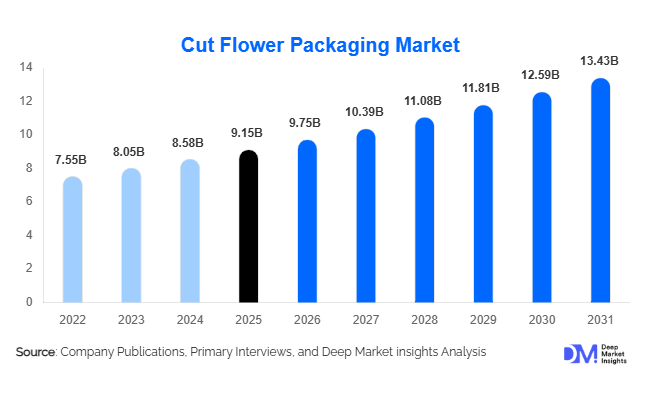

According to Deep Market Insights, the global cut flower packaging market size was valued at USD 9.15 billion in 2025 and is projected to grow from USD 9.75 billion in 2026 to reach USD 13.43 billion by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The cut flower packaging market growth is primarily driven by rising global floriculture trade, increasing demand for premium floral presentation, rapid expansion of e-commerce flower delivery services, and growing adoption of sustainable packaging materials. Packaging has become a strategic component of the floriculture supply chain as producers, exporters, retailers, and online flower delivery companies seek solutions that extend freshness, reduce transportation losses, and enhance visual appeal.

Key Market Insights

- Sustainable paper-based and biodegradable packaging solutions are increasingly replacing conventional plastic packaging due to stricter environmental regulations and changing consumer preferences.

- E-commerce flower delivery companies are becoming major packaging consumers, driving demand for protective transport packaging, moisture-control systems, and customized branding solutions.

- Asia-Pacific dominates the global market, supported by large-scale flower production, expanding exports, and strong domestic consumption in China and India.

- India is emerging as one of the fastest-growing markets, driven by floriculture exports, wedding demand, and investments in cold-chain infrastructure.

- Paper and paperboard packaging account for the largest material share, benefiting from recyclability, cost efficiency, and compatibility with sustainability initiatives.

- Packaging innovation is increasingly focused on freshness preservation, incorporating ventilation systems, moisture-retention technologies, and export-grade protective structures.

Cut Flower Packaging Market Trends

Growing Adoption of Sustainable Packaging Materials

The floral industry is rapidly transitioning toward environmentally responsible packaging formats. Retailers, florists, and exporters are increasingly replacing conventional plastic sleeves and wraps with recyclable paper, molded fiber, biodegradable films, and compostable materials. Sustainability commitments from major retail chains, coupled with government restrictions on single-use plastics, are accelerating this transition globally. Packaging manufacturers are investing in eco-friendly product development while maintaining moisture retention and structural performance. The trend is particularly pronounced across Europe and North America, where consumers increasingly prefer floral products packaged using sustainable materials. Premium flower brands are also leveraging environmentally friendly packaging as a key differentiator in the market.

Expansion of E-Commerce Flower Delivery Packaging

The rapid growth of online flower ordering has transformed packaging requirements across the industry. Unlike traditional retail channels, e-commerce deliveries require packaging capable of withstanding multiple handling stages while maintaining flower freshness and presentation quality. Packaging suppliers are developing reinforced corrugated cartons, moisture-control liners, protective inserts, and temperature-resistant packaging systems specifically designed for direct-to-consumer flower shipments. Personalized packaging, branded unboxing experiences, and digital printing capabilities are becoming increasingly important as online flower delivery companies seek to improve customer satisfaction and strengthen brand recognition. This trend is expected to remain a significant growth driver throughout the forecast period.

Cut Flower Packaging Market Drivers

Expansion of Global Floriculture Trade

The growing international trade of fresh-cut flowers continues to stimulate demand for advanced packaging solutions. Major flower-exporting countries including the Netherlands, Colombia, Ecuador, Kenya, Ethiopia, China, and India rely heavily on protective packaging to maintain flower quality during long-distance transportation. Packaging solutions that reduce physical damage, moisture loss, and spoilage are becoming critical for exporters seeking to improve profitability and reduce post-harvest losses. As export volumes continue to increase, demand for specialized packaging products is expected to grow accordingly.

Increasing Demand for Premium Floral Presentation

Consumer spending on floral gifts, weddings, corporate events, and decorative arrangements has increased demand for aesthetically appealing packaging formats. Florists and retailers are investing in decorative sleeves, luxury wrapping materials, bouquet holders, and customized packaging solutions to enhance product value and customer experience. Premium packaging is increasingly viewed as an extension of the floral product itself, enabling suppliers to command higher pricing and differentiate their offerings in competitive markets.

Growth of Online Flower Delivery Platforms

The expansion of digital flower marketplaces and direct-to-consumer delivery services has significantly increased packaging consumption. Online flower retailers require packaging solutions that combine transportation protection, freshness preservation, branding, and sustainability. As flower e-commerce penetration continues to increase globally, demand for specialized packaging products is expected to rise at a faster pace than traditional retail packaging segments.

Cut Flower Packaging Market Restraints

Volatility in Raw Material Prices

Packaging manufacturers remain highly exposed to fluctuations in raw material costs, particularly paper pulp, polymers, adhesives, inks, and specialty coatings. Sudden increases in material prices can reduce profit margins and limit pricing flexibility, particularly for suppliers operating under long-term contracts. Ongoing volatility in global commodity markets continues to create uncertainty for packaging producers.

Performance Requirements for Perishable Products

Fresh-cut flowers require highly specialized packaging capable of maintaining product quality throughout the supply chain. Packaging failures can result in moisture loss, stem damage, reduced shelf life, and increased product returns. Meeting these technical requirements often requires significant investment in research, testing, and product development, creating barriers for new market entrants and increasing operational costs for manufacturers.

Cut Flower Packaging Market Opportunities

Development of Advanced Sustainable Packaging Solutions

As governments and retailers accelerate sustainability initiatives, significant opportunities exist for packaging manufacturers capable of delivering environmentally friendly alternatives to conventional plastics. Compostable sleeves, biodegradable films, recyclable wraps, and molded fiber packaging formats are expected to experience strong adoption over the next decade. Companies that successfully balance sustainability with freshness preservation and cost efficiency are likely to capture substantial market share.

Growth of Export-Oriented Floriculture Markets

Emerging flower-exporting countries such as India, Kenya, Ethiopia, and Vietnam are expanding production capacities and strengthening export infrastructure. These markets require specialized export packaging solutions that comply with international transportation standards and phytosanitary regulations. Establishing manufacturing operations near major floriculture clusters provides packaging suppliers with opportunities to secure long-term partnerships and recurring revenue streams.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.15 Billion |

| Market Size in 2026 | USD 9.75 Billion |

| Market Size in 2031 | USD 13.43 Billion |

| CAGR | 6.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

Paper and paperboard packaging dominate the global cut flower packaging market, accounting for approximately 45.2% of total revenue in 2025. Their leadership is supported by strong recyclability credentials, cost competitiveness, and widespread acceptance among retailers and consumers. Plastic packaging remains important for moisture retention and transportation applications, particularly in export-oriented supply chains. However, growing environmental concerns are gradually reducing dependence on conventional plastics. Bioplastics, molded fiber packaging, natural fiber wraps, and textile-based decorative packaging are gaining momentum as sustainability requirements increase across developed markets. Manufacturers are increasingly focusing on hybrid packaging solutions that combine structural strength, freshness preservation, and environmental performance.

Packaging Format Insights

Sleeves represent the largest packaging format segment, accounting for nearly 31% of global market revenue. Their popularity stems from affordability, ease of customization, and widespread use across florists, supermarkets, and retail chains. Wrapping sheets remain highly utilized for bouquet presentation and premium floral arrangements. Corrugated boxes and cartons are experiencing strong growth due to rising flower exports and e-commerce deliveries, where transportation protection is critical. Bouquet holders, floral trays, and display containers also contribute significantly to market demand, particularly within organized retail environments. Decorative gift packaging sets are gaining traction among premium flower brands seeking differentiation and enhanced customer experiences.

End-Use Insights

Florists and flower shops remain the largest end-user segment, accounting for approximately 31% of global packaging demand. Their consistent requirement for sleeves, decorative wraps, bouquet holders, and presentation packaging supports segment leadership. Flower exporters represent a rapidly growing segment due to increasing international trade volumes and stricter quality preservation requirements. Online flower delivery companies are emerging as the fastest-growing end-user category, supported by expanding digital commerce and direct-to-consumer delivery models. Supermarkets and hypermarkets continue to increase floral product offerings, while wedding planners, event management companies, and hospitality providers are creating additional demand for premium packaging solutions. Export-oriented floriculture businesses are expected to remain a key growth engine for the industry over the forecast period.

Distribution Channel Insights

Floral packaging distributors account for the largest share of global sales, representing nearly 39% of market revenue. Distributors play a critical role by aggregating inventory, offering product variety, and ensuring rapid fulfillment for florists and retailers. Direct sales to growers and exporters remain significant, particularly among large commercial flower producers. E-commerce procurement platforms are gaining popularity as packaging buyers increasingly seek streamlined sourcing processes, transparent pricing, and broader product selections. Organized retail procurement channels are also expanding as supermarkets and retail flower chains centralize packaging purchasing activities across multiple locations.

Explore more data points, trends and opportunities Download Free Sample Report

Cut Flower Packaging Market Segmentations

By Material Type

- Paper & Paperboard Packaging

- Plastic Packaging

- Jute & Natural Fiber Packaging

- Fabric & Textile Packaging

- Metal-Based Packaging

By Packaging Format

- Sleeves

- Wrapping Sheets

- Boxes & Cartons

- Bags & Pouches

- Bouquet Holders

- Flower Transport Trays

- Display Buckets & Containers

- Floral Gift Packaging Sets

By Packaging Function

- Transport & Export Packaging

- Retail Display Packaging

- Bouquet Presentation Packaging

- Gift Packaging

- Cold Chain Compatible Packaging

By Sustainability Type

- Conventional Packaging

- Recyclable Packaging

- Compostable Packaging

- Biodegradable Packaging

- Reusable Packaging

By End User

- Flower Growers & Farms

- Flower Exporters

- Floral Wholesalers

- Florists & Flower Shops

- Supermarkets & Hypermarkets

- Online Flower Delivery Companies

- Event & Wedding Decorators

Regional Insights

Asia-Pacific

Asia-Pacific represents the largest regional market, accounting for approximately 35% of global revenue in 2025. China leads regional demand due to extensive flower cultivation, growing domestic consumption, and expanding online flower delivery services. India is emerging as one of the fastest-growing markets, supported by increasing floriculture exports, wedding-related floral demand, and government initiatives promoting agricultural exports. Japan and South Korea contribute significantly through premium flower consumption and high-value packaging demand. Australia also represents a stable market characterized by organized retail distribution and growing sustainability adoption.

Europe

Europe accounts for approximately 28% of the global market and remains a key center for floriculture trade. The Netherlands serves as the world's largest flower trading hub and drives substantial packaging demand through export and distribution activities. Germany, the United Kingdom, France, and Italy represent major consumption markets characterized by strong demand for sustainable packaging solutions. Regulatory initiatives targeting plastic reduction continue to support growth in paper-based and biodegradable packaging formats across the region.

North America

North America accounts for roughly 22% of global market revenue. The United States dominates regional demand due to high flower consumption, significant import volumes from Latin America, and strong adoption of online flower delivery services. Canada contributes through premium floral retail channels and increasing demand for sustainable packaging products. Continued growth in gifting occasions and e-commerce sales is expected to support long-term market expansion across the region.

Latin America

Latin America contributes approximately 9% of global demand and is heavily influenced by export-oriented flower production. Colombia and Ecuador are among the world's leading flower exporters and require sophisticated packaging solutions capable of preserving product quality during international transportation. Investments in logistics infrastructure and export capacity continue to strengthen regional demand.

Middle East & Africa

The Middle East & Africa region accounts for approximately 6% of global market revenue. Kenya and Ethiopia serve as major flower-exporting nations, generating substantial demand for export-grade packaging solutions. Meanwhile, countries such as the UAE and Saudi Arabia are experiencing growing demand for premium floral products driven by hospitality, gifting, and luxury event sectors. Increasing investment in floriculture infrastructure is expected to support future growth across the region.

Key Players in the Cut Flower Packaging Market

- Smurfit Westrock

- Stora Enso

- DS Smith

- Mondi Group

- UFlex Limited

- Koen Pack

- Flamingo Holland

- A-ROO Company

- Broekhof Verpakkingen

- Sirane Group

- Dilpack Kenya

- Packman Packaging

- Nature-Pack

- GleePackaging

- FloraPack Solutions