Custom Home Furniture Market Size

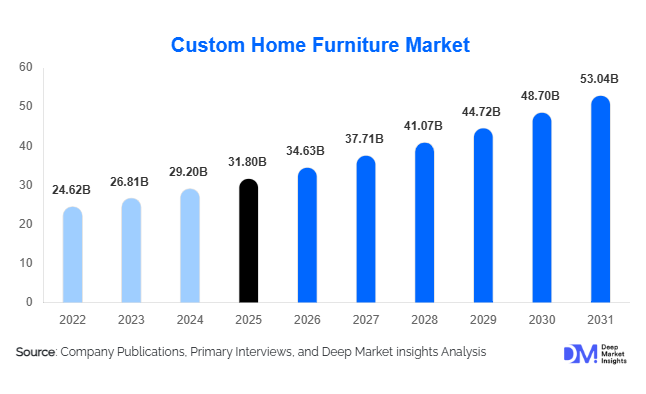

According to Deep Market Insights, the global custom home furniture market size was valued at USD 31.8 billion in 2025 and is projected to grow from USD 34.63 billion in 2026 to reach USD 53.04 billion by 2031, expanding at a CAGR of 8.9% during the forecast period (2026–2031). The market growth is primarily driven by rising consumer preference for personalized living spaces, increasing residential renovation activities, expanding urbanization, and growing demand for multifunctional furniture solutions. Advances in digital design technologies, CNC manufacturing, and AI-powered customization platforms are making personalized furniture more accessible across both premium and mid-market consumer segments.

Key Market Insights

- Customized living room and bedroom furniture account for the largest share of global demand, driven by consumers seeking personalized aesthetics and optimized space utilization.

- Sustainability has become a major purchasing criterion, with increasing adoption of FSC-certified wood, recycled materials, and low-emission manufacturing processes.

- Europe remains the largest regional market, supported by strong demand for premium craftsmanship, bespoke interior design, and high residential spending.

- Asia-Pacific is the fastest-growing region, fueled by rapid urbanization, rising disposable incomes, and increasing homeownership across China, India, and Southeast Asia.

- Digital furniture customization platforms are transforming customer engagement, enabling consumers to visualize designs before purchase through AR and AI-based room planning tools.

- Premium and luxury furniture segments continue to outperform mass-market categories, as consumers increasingly view customized furniture as a long-term lifestyle investment.

Custom Home Furniture Market Trends

Digital Design and Visualization Technologies Reshaping Consumer Purchases

Furniture manufacturers are increasingly integrating artificial intelligence, augmented reality, and virtual room visualization tools into the purchasing journey. Consumers can now customize dimensions, materials, finishes, and configurations while viewing furniture within simulated home environments. These technologies improve purchase confidence, reduce design errors, and accelerate decision-making. Direct-to-consumer brands are investing heavily in digital customization platforms to expand customer reach and improve conversion rates. The growing integration of AI-generated recommendations and immersive design tools is expected to further streamline the custom furniture buying process over the coming years.

Sustainable and Eco-Friendly Furniture Solutions Gaining Momentum

Sustainability is becoming a defining trend across the custom home furniture market. Consumers are increasingly demanding furniture manufactured using responsibly sourced wood, recycled materials, water-based finishes, and environmentally friendly production processes. Furniture companies are responding through investments in certified timber sourcing, circular economy initiatives, and low-carbon manufacturing facilities. Eco-conscious consumers, particularly in Europe and North America, are willing to pay premium prices for furniture that aligns with sustainability values. This trend is encouraging manufacturers to incorporate environmental certifications and transparent supply chain practices into their product offerings.

Custom Home Furniture Market Drivers

Growing Residential Renovation and Remodeling Activities

Home renovation expenditures have increased substantially across developed and emerging economies. Homeowners are investing in customized furniture to improve functionality, aesthetics, and property value. The trend toward home improvement has accelerated demand for bespoke wardrobes, entertainment units, modular kitchens, and storage systems that maximize available living space. As consumers increasingly personalize their homes, custom furniture solutions are becoming an integral component of renovation projects worldwide.

Urbanization and Demand for Space Optimization

Rapid urbanization and shrinking residential footprints are creating strong demand for customized furniture that optimizes space utilization. Multifunctional furniture, built-in storage systems, modular kitchens, and customized wardrobes allow consumers to maximize efficiency in compact apartments and urban homes. This trend is particularly prominent in major metropolitan markets across Asia-Pacific and Europe, where living spaces continue to become more compact.

Advancements in Manufacturing and Mass Customization Technologies

Technological advancements such as CNC machining, digital fabrication, robotics, and cloud-based design software have significantly improved manufacturing efficiency. These innovations enable manufacturers to deliver customized furniture at lower production costs while maintaining high levels of personalization. The ability to combine customization with scalable production capabilities is expanding the addressable market beyond traditional luxury consumers.

Custom Home Furniture Market Restraints

Higher Production Costs Compared to Standard Furniture

Custom furniture typically requires individualized design processes, specialized materials, and flexible manufacturing workflows. These factors increase production costs and often result in premium pricing. Cost-conscious consumers in emerging markets may continue to prefer standardized furniture products, limiting market penetration in certain customer segments.

Supply Chain Volatility and Raw Material Price Fluctuations

The custom home furniture industry remains vulnerable to fluctuations in timber, metal, upholstery materials, and logistics costs. Supply disruptions and raw material shortages can increase lead times and impact profitability. Manufacturers must continually optimize sourcing strategies and inventory management practices to mitigate supply chain risks and maintain competitive pricing.

Custom Home Furniture Market Opportunities

Expansion of AI-Driven Furniture Customization Platforms

The growing adoption of AI-powered room planners and virtual design tools presents significant opportunities for furniture manufacturers. Digital customization platforms can reduce consultation costs, improve customer engagement, and enable mass personalization. Companies investing in advanced digital experiences are expected to gain competitive advantages through higher customer satisfaction and improved operational efficiency.

Growth in Sustainable and Premium Furniture Categories

Consumer demand for sustainable products continues to rise globally. Manufacturers that invest in environmentally responsible sourcing, carbon-neutral production, and recyclable materials can capture premium market segments. Sustainability-focused product lines are increasingly becoming important differentiators in mature markets such as Europe and North America.

Rising Demand from Emerging Housing Markets

Rapid residential construction activity across India, Southeast Asia, the Middle East, and Latin America is generating new demand for customized furniture solutions. Government housing programs, expanding urban populations, and increasing middle-class spending power are creating long-term growth opportunities for both domestic and international furniture manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 31.8 Billion |

| Market Size in 2026 | USD 34.63 Billion |

| Market Size in 2031 | USD 53.04 Billion |

| CAGR | 8.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Living room furniture represents the largest product category, accounting for approximately 28% of global market revenue in 2025. Customized sofas, sectional seating systems, entertainment units, and coffee tables continue to drive demand due to their importance in defining residential aesthetics. Bedroom furniture remains the second-largest category, supported by strong demand for customized wardrobes, beds, and storage solutions. Modular kitchen furniture is among the fastest-growing segments as consumers increasingly seek integrated storage systems and optimized kitchen layouts. Home office furniture is also experiencing strong growth, supported by hybrid work models and rising investments in dedicated home workspace environments.

Material Insights

Solid wood remains the leading material segment, accounting for nearly 39% of global market demand. Consumers associate solid wood furniture with durability, craftsmanship, premium aesthetics, and long-term value. Engineered wood products such as MDF and plywood continue gaining market share due to affordability and design flexibility. Sustainable and recycled materials represent one of the fastest-growing material categories, supported by environmental regulations and growing consumer awareness regarding responsible sourcing practices. Metal and glass materials continue to gain traction in contemporary and industrial furniture designs, particularly within urban residential markets.

Customization Level Insights

Semi-custom furniture dominates the market, accounting for approximately 46% of global revenue. This segment balances affordability and personalization by allowing consumers to select finishes, materials, dimensions, and configurations from predefined options. Fully bespoke furniture continues to dominate luxury residential applications, where consumers prioritize exclusivity and craftsmanship. Made-to-order standardized designs remain popular among mid-market buyers seeking customization without the higher costs associated with bespoke manufacturing. The growing adoption of digital design technologies is making all customization categories more accessible to a broader customer base.

Distribution Channel Insights

Brand-owned showrooms remain the dominant sales channel, representing approximately 45% of market demand. Consumers continue to value the ability to physically evaluate furniture quality, materials, finishes, and comfort before making purchasing decisions. Omnichannel retail models are expanding rapidly as manufacturers integrate physical showrooms with digital design platforms and e-commerce capabilities. Direct-to-consumer online channels are experiencing strong growth, particularly among younger consumers who prefer digital customization and home delivery services. Interior design firms also remain influential distribution partners for premium and luxury furniture manufacturers.

End-Use Insights

Individual households account for approximately 62% of global custom home furniture demand, making residential consumers the largest end-use segment. Demand is driven by home renovation projects, new residential construction, and increasing investments in personalized interiors. Luxury residential developments represent the fastest-growing end-use category, supported by rising high-net-worth populations and premium real estate investments. Property developers are increasingly partnering with furniture manufacturers to provide customized furnishing packages as part of residential offerings. Hospitality residences and serviced apartments are also emerging as important demand generators for premium customized furniture solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Custom Home Furniture Market Segmentations

By Product Type

- Living Room Furniture

- Bedroom Furniture

- Dining Room Furniture

- Kitchen & Storage Furniture

- Home Office Furniture

- Children's Furniture

- Outdoor Residential Furniture

By Material

- Solid Wood

- Engineered Wood

- Metal

- Glass

- Composite Materials

- Sustainable/Recycled Materials

By Customization Level

- Made-to-Order Standard Designs

- Semi-Custom Furniture

- Fully Bespoke Furniture

By Distribution Channel

- Brand-Owned Showrooms

- Independent Furniture Retailers

- Interior Design Firms

- Direct-to-Consumer Online Platforms

- Omnichannel Retail

By End User

- Individual Households

- Luxury Residential Projects

- Hospitality Residences

- Property Developers & Builders

Regional Insights

North America

North America accounts for approximately 24% of global market demand, led primarily by the United States. High disposable incomes, strong home renovation activity, and growing consumer preference for premium interior furnishings support market growth. Customized living room furniture, home office furniture, and storage solutions remain particularly popular across the region. Canada also contributes significantly through sustained residential remodeling expenditures and increasing demand for sustainable furniture products.

Europe

Europe remains the largest regional market, accounting for approximately 33% of global revenue. Germany, Italy, France, and the United Kingdom represent the primary demand centers. Germany leads regional consumption due to strong demand for premium craftsmanship and customized home interiors. Italy benefits from its established furniture manufacturing ecosystem and luxury furniture heritage. Sustainability and design innovation remain key purchasing drivers throughout the European market.

Asia-Pacific

Asia-Pacific accounts for approximately 29% of global market demand and represents the fastest-growing region. China remains the largest market due to extensive residential construction and rising middle-class spending. India is emerging as the fastest-growing country market, supported by urbanization, increasing homeownership, and expanding residential development programs. Japan and South Korea continue to exhibit strong demand for space-efficient customized furniture solutions tailored to compact urban living environments.

Latin America

Latin America represents approximately 7% of global market revenue, led by Brazil and Mexico. Residential construction growth, rising urban populations, and expanding middle-class consumer spending continue to support furniture demand. Customized furniture adoption is increasing among affluent urban consumers seeking premium interior design solutions.

Middle East & Africa

The Middle East and Africa account for approximately 7% of global market demand. The UAE and Saudi Arabia remain key growth markets due to luxury residential developments and high-end interior design investments. South Africa continues to represent the largest furniture market in Africa, supported by residential renovation activities and growing urbanization trends. Increasing premium real estate investments across Gulf Cooperation Council countries are expected to further stimulate demand for customized home furniture solutions.

Key Players in the Custom Home Furniture Market

- IKEA

- MillerKnoll

- Ashley Furniture Industries

- Steelcase

- La-Z-Boy

- RH (Restoration Hardware)

- Williams-Sonoma

- Oppein Home Group

- Suofeiya Home Collection

- GoldenHome Living

- Hülsta

- Natuzzi

- Roche Bobois

- BoConcept

- Wren Kitchens