Cricket Bat Market Size

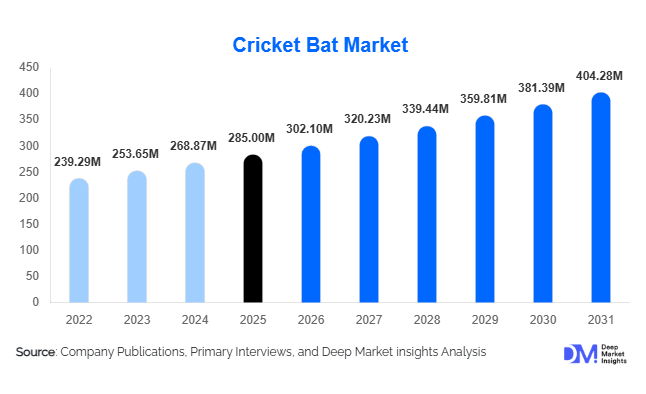

According to Deep Market Insights, the global cricket bat market size was valued at USD 285 million in 2026 and is projected to grow from USD 302.10 million in 2026 to reach USD 404.28 million by 2031, expanding at a CAGR of 6.0% during the forecast period (2026–2031). The cricket bat market growth is primarily driven by the increasing popularity of cricket across emerging geographies, expansion of professional franchise leagues, rising participation in grassroots and academy cricket, and growing consumer demand for premium-performance sporting equipment. The continued commercialization of the sport through tournaments such as the Indian Premier League (IPL), The Hundred, Pakistan Super League (PSL), SA20, and Major League Cricket (MLC) has significantly increased brand visibility and equipment purchases globally.

Cricket bats remain the highest-value product segment within the cricket equipment industry due to their premium pricing, technological differentiation, and recurring replacement requirements. Manufacturers are increasingly investing in superior willow processing technologies, advanced bat profiling techniques, customized manufacturing, and direct-to-consumer sales channels. The market is also witnessing growing adoption of premium English willow bats among semi-professional and amateur players, while Kashmir willow products continue to drive affordability and penetration across emerging cricket markets. As cricket gains traction in North America, the Middle East, and continental Europe, demand for professional-grade and academy-level cricket bats is expected to increase substantially during the forecast period.

Key Market Insights

- English willow cricket bats account for approximately 62% of global market revenue, supported by strong demand from professional and competitive players worldwide.

- Asia-Pacific dominates the global cricket bat market with nearly 48% market share, driven primarily by India, Pakistan, Australia, Bangladesh, and Sri Lanka.

- India represents approximately 32% of global cricket bat demand, making it the largest individual country market.

- North America is the fastest-growing regional market, expanding at an estimated CAGR of over 8% through 2031 due to rising participation and league development.

- Cricket academies are emerging as the fastest-growing end-use segment, supported by increasing investments in youth cricket development programs globally.

- Customization and premiumization trends are reshaping consumer purchasing behavior, with players increasingly seeking personalized bat profiles, handle designs, and weight distributions.

What are the latest trends in the cricket bat market?

Premiumization of Cricket Equipment

The global cricket bat market is experiencing significant premiumization as players increasingly prioritize performance-enhancing equipment over standard recreational products. Demand for Grade 1 and Grade 2 English willow bats continues to rise among club cricketers and academy trainees seeking professional-grade performance. Manufacturers are introducing thicker edges, enlarged sweet spots, improved pickup characteristics, and advanced pressing technologies to differentiate their offerings. Premium cricket bats priced above USD 300 are witnessing faster revenue growth than lower-priced categories, contributing disproportionately to overall market expansion. Brand endorsements by international cricketers are further accelerating adoption of premium products across amateur and semi-professional segments.

Rise of Customized and Direct-to-Consumer Cricket Bats

Customization has emerged as a major trend across the cricket bat industry. Players increasingly demand personalized bat specifications, including blade profile, weight distribution, handle shape, grip configuration, and toe protection. Manufacturers are leveraging digital tools and e-commerce platforms to provide customized ordering experiences directly to consumers. Direct-to-consumer sales channels are expanding rapidly, allowing brands to improve margins while building stronger relationships with players. Online fitting consultations, bat profiling software, and virtual product demonstrations are becoming important differentiators among leading cricket bat manufacturers.

What are the key drivers in the cricket bat market?

Expansion of Global Cricket Participation

The growing popularity of cricket beyond traditional markets is a major driver for cricket bat demand. Countries such as the United States, Canada, Germany, Netherlands, UAE, and Saudi Arabia are investing in cricket infrastructure, coaching academies, and domestic competitions. Youth participation programs and school-level cricket initiatives continue to create new equipment buyers annually. Increased accessibility to coaching and organized competitions is strengthening long-term demand fundamentals across both established and emerging cricket nations.

Growth of Franchise Cricket Leagues

The rapid expansion of franchise-based cricket leagues has significantly increased global visibility for the sport. High-profile tournaments including IPL, PSL, Big Bash League, SA20, ILT20, and Major League Cricket have expanded cricket's commercial footprint while influencing equipment purchasing decisions among aspiring players. Professional endorsements remain one of the strongest demand catalysts within the cricket bat industry. Young players frequently emulate international stars by purchasing branded bat models used by professional cricketers.

What are the restraints for the global market?

Limited Availability of Premium Willow

English willow remains the preferred raw material for premium cricket bats; however, supply remains constrained due to long cultivation cycles and limited production regions. Variability in weather conditions, agricultural yields, and land availability can significantly affect willow production volumes. Raw material shortages frequently lead to higher manufacturing costs and retail prices, impacting accessibility for price-sensitive consumers.

Increasing Product Costs

The average selling price of premium cricket bats has risen substantially over the past decade due to increasing raw material costs, labor expenses, and manufacturing complexity. Professional-grade bats often retail above USD 500, while elite-grade products can exceed USD 1,000. These elevated prices may limit market penetration among youth players and recreational participants, particularly in developing economies where disposable incomes remain constrained.

What are the key opportunities in the cricket bat industry?

Expansion into Emerging Cricket Markets

Emerging cricket nations present significant growth opportunities for manufacturers seeking geographic diversification. North America, the Middle East, and continental Europe are witnessing increased participation rates supported by immigration trends, league investments, and government-backed sports development programs. Early market entry into these regions provides manufacturers with opportunities to establish brand leadership before competitive intensity increases. Local partnerships, academy sponsorships, and direct distribution networks are expected to play crucial roles in capturing these growth opportunities.

Technology-Enabled Manufacturing and Customization

Advancements in bat manufacturing technologies are creating opportunities for product innovation and operational efficiency. Automated profiling systems, precision pressing equipment, moisture management technologies, and digital customization platforms allow manufacturers to improve consistency while addressing increasingly sophisticated consumer preferences. Companies investing in smart manufacturing and personalized production capabilities are expected to achieve superior margins and stronger customer loyalty over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 285 Million |

| Market Size in 2026 | USD 302.10 Million |

| Market Size in 2031 | USD 404.28 Million |

| CAGR | 6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Material Type Insights

English willow bats dominate the cricket bat market, accounting for approximately 62% of global revenue in 2026. The segment benefits from superior performance characteristics, lightweight construction, larger sweet spots, and widespread adoption by professional players. Grade 1 and Grade 2 English willow products represent the premium end of the market and command the highest average selling prices. Kashmir willow bats represent the second-largest material segment and remain particularly popular in South Asia due to affordability advantages. Composite and hybrid bats continue to occupy niche applications, primarily in training environments and recreational cricket. Ongoing innovations in willow treatment, pressing techniques, and blade profiling are expected to reinforce the dominance of English willow products throughout the forecast period.

Player Category Insights

Amateur club players represent the largest consumer segment, accounting for approximately 34% of global cricket bat revenues. The segment benefits from extensive participation across established cricket nations and rising engagement in emerging markets. Professional players constitute a relatively small volume segment but significantly influence purchasing trends through endorsements and sponsorship agreements. School and youth players represent one of the fastest-growing categories due to increasing investments in grassroots cricket development and academy-based training programs. Recreational players continue to drive demand for economy and mid-range bat categories, supporting market penetration across developing regions.

Distribution Channel Insights

Specialty sports stores account for approximately 38% of global cricket bat sales and remain the preferred channel for premium bat purchases. Consumers often prefer physical inspection of bat weight, balance, and pickup characteristics before making purchasing decisions. E-commerce channels are rapidly expanding, supported by direct-to-consumer business models, digital customization platforms, and broader product availability. Brand-owned retail stores continue to gain traction in major cricket markets, while institutional procurement channels serve academies, schools, and professional organizations through bulk purchasing agreements. The integration of omnichannel retail strategies is increasingly shaping competitive differentiation among leading manufacturers.

End-Use Insights

Individual consumers account for approximately 56% of global cricket bat demand and remain the largest end-use segment. Purchases are driven by recreational players, club cricketers, and academy participants seeking performance-oriented equipment. Cricket academies represent the fastest-growing end-use category, supported by rising enrollment levels and increased investments in structured coaching programs. Schools and colleges continue to expand cricket infrastructure and equipment procurement budgets, particularly across the Asia-Pacific and emerging cricket nations. Professional teams and franchise organizations contribute disproportionately to premium bat sales while also influencing broader market demand through player endorsements and equipment partnerships.

Explore more data points, trends and opportunities Download Free Sample Report

Cricket Bat Market Segmentations

By Material Type

- English Willow Cricket Bats

- Kashmir Willow Cricket Bats

- Composite & Hybrid Cricket Bats

By Player Category

- Professional Players

- Semi-Professional Players

- Amateur Club Players

- School & Youth Players

- Recreational Players

By Bat Size

- Senior/Adult Bats

- Youth Bats

- Junior Bats

- Mini & Training Bats

By Distribution Channel

- Specialty Sports Stores

- Multi-Sport Retail Chains

- Brand-Owned Stores

- E-Commerce Platforms

- Cricket Academy & Club Sales

- Institutional Procurement

By End User

- Individual Consumers

- Cricket Academies

- Schools & Colleges

- Professional Teams & Franchises

- Sports Retailers

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global cricket bat market, accounting for approximately 48% of total market revenue in 2026, making it the largest and most influential regional market globally. The region's leadership is underpinned by cricket's deep-rooted cultural significance, large player base, strong manufacturing ecosystem, and continuous investments in grassroots sports development. India represents the single largest market worldwide, contributing nearly 32% of global cricket bat revenues. The country's dominance is supported by over a century of cricket tradition, extensive school and academy participation, a rapidly expanding sports economy, and the commercial success of tournaments such as the Indian Premier League (IPL). Beyond India, Pakistan, Bangladesh, Sri Lanka, and Australia collectively contribute a substantial share of regional demand. Pakistan remains one of the largest producers and consumers of cricket equipment, while Bangladesh continues to benefit from increasing youth participation and government-backed sports development initiatives. Australia represents the premium segment leader in the region, characterized by high per-player spending on professional-grade equipment and strong demand from organized club cricket. Sri Lanka continues to generate steady demand through school-level cricket programs and national talent development pathways.

The primary growth drivers across Asia-Pacific include rising disposable incomes, increasing enrollment in cricket academies, growing female participation in cricket, expansion of franchise-based leagues, and continued investments in sports infrastructure. Additionally, the region serves as a major manufacturing hub for cricket bats, particularly in India and Pakistan, providing cost advantages and supporting export growth. As cricket continues to expand into new demographics and age groups, Asia-Pacific is expected to maintain its dominant position throughout the forecast period.

Europe

Europe accounts for approximately 22% of global cricket bat demand, with the United Kingdom representing the largest and most mature market within the region. England serves a dual role as both a major consumer of cricket bats and the world's leading source of premium English willow, the preferred raw material for high-performance cricket bats. The country's extensive cricket ecosystem, encompassing county cricket, club competitions, school programs, and professional tournaments such as The Hundred, creates sustained demand across all bat categories. The United Kingdom continues to lead premium bat consumption due to strong participation among club cricketers and semi-professional players who prioritize performance-oriented equipment. Demand for customized and handcrafted English willow bats remains particularly strong among competitive players. Meanwhile, European countries such as the Netherlands, Germany, Ireland, and Italy are witnessing increased cricket participation driven by immigrant populations from South Asia, the Caribbean, and Africa. Cricket federations across these countries are investing in youth development programs and grassroots leagues, gradually expanding the consumer base for cricket equipment.

Key growth drivers in Europe include increasing multicultural demographics, rising popularity of T20 cricket formats, expansion of community-based cricket clubs, and growing investments by national cricket boards. Additionally, the region benefits from strong e-commerce penetration, enabling consumers to access a broader range of premium cricket bat brands. The increasing visibility of international tournaments and cricket's inclusion in major sporting events is expected to further stimulate market growth across continental Europe.

North America

North America represents approximately 12% of the global cricket bat market and is projected to record the fastest growth rate globally, with an estimated CAGR exceeding 8% through 2031. The region's rapid expansion is being driven primarily by the United States, where cricket is transitioning from a niche sport into a commercially organized industry. The launch of Major League Cricket (MLC), investments in dedicated cricket stadiums, and increasing media coverage have significantly enhanced awareness and participation levels across the country. The United States is benefiting from a large South Asian diaspora population, which has created a strong foundation for grassroots cricket participation. Simultaneously, schools, universities, and private academies are increasingly introducing structured cricket programs, generating new demand for cricket bats and related equipment. Canada is also experiencing strong market growth, particularly in provinces with high immigrant populations such as Ontario and British Columbia. Organized leagues, youth development programs, and community-based cricket associations continue to support demand expansion.

Major growth drivers include increasing infrastructure investments, rising sponsorship activity, growing youth participation, professional league development, and enhanced accessibility through online retail channels. Furthermore, the inclusion of cricket in the 2028 Los Angeles Olympic Games is expected to significantly accelerate interest and participation across North America, creating substantial opportunities for cricket bat manufacturers and distributors over the next decade.

Latin America

Latin America accounts for approximately 8% of global cricket bat demand and remains an emerging market with significant long-term growth potential. While cricket participation remains relatively limited compared to traditional cricket-playing nations, several countries are actively investing in the sport through development programs, international partnerships, and grassroots initiatives. The Caribbean region continues to serve as the primary demand center due to its strong cricketing heritage and historical contributions to international cricket. Countries such as Brazil, Argentina, and Mexico are gradually expanding cricket participation through school programs, expatriate communities, and local cricket associations. Brazil, in particular, has demonstrated promising growth as cricket development initiatives target youth participation and women's cricket programs. Argentina continues to benefit from established cricket clubs and a growing interest in international cricket competitions.

The region's growth is being supported by increasing awareness through digital media, international cricket tournaments, and development funding from global cricket organizations. Additional drivers include expanding sports infrastructure investments, growing middle-class populations, and increasing availability of affordable cricket equipment through online channels. Although Latin America currently represents a relatively small share of global revenues, the region offers attractive long-term opportunities for manufacturers seeking geographic diversification and first-mover advantages.

Middle East & Africa

The Middle East & Africa region contributes approximately 10% of global cricket bat market revenues and has emerged as one of the most strategically important growth regions for the industry. The United Arab Emirates serves as the regional hub for international cricket, hosting major tournaments, franchise leagues, and training facilities that drive significant equipment demand. The country's large expatriate population from cricket-playing nations further strengthens participation and consumption levels. Saudi Arabia is increasingly investing in sports diversification initiatives as part of broader economic transformation programs, creating opportunities for cricket infrastructure development and participation growth. Qatar and Oman are also witnessing increasing cricket activity, supported by expatriate communities and regional tournament hosting. In Africa, South Africa remains the largest and most mature cricket market, characterized by strong domestic competitions, professional player development systems, and widespread participation at school and club levels.

Key growth drivers across the region include government investments in sports infrastructure, rising franchise cricket activity, increasing youth participation, and expanding academy networks. The growth of T20 leagues across the Gulf region has further strengthened consumer interest in cricket equipment. Additionally, improving retail distribution networks and rising disposable incomes are making premium cricket bats more accessible to a broader consumer base. As governments continue to prioritize sports development and international sporting events, the Middle East & Africa region is expected to deliver above-average growth throughout the forecast period.

Key Players in the Cricket Bat Market

- Gray-Nicolls

- Kookaburra

- Gunn & Moore

- SG (Sanspareils Greenlands)

- SS (Sareen Sports Industries)

- BAS (Beat All Sports)

- Spartan Sports

- Salix Cricket Bats

- Kippax Willow

- New Balance Cricket

- MRF Sports Goods

- TON Cricket

- Slazenger

- Aldred Cricket

- BDM Sports