Commodity Plastics Market Size

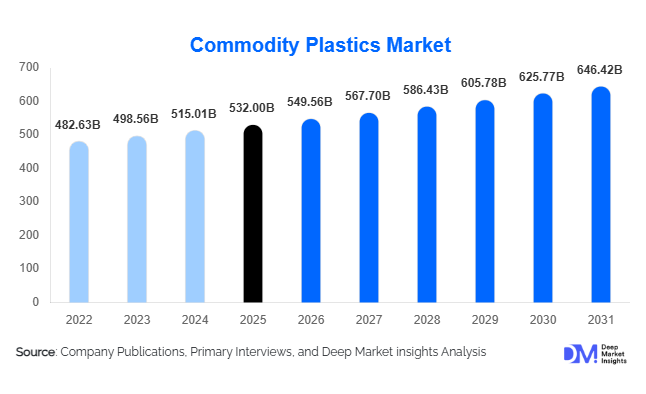

According to Deep Market Insights, the global commodity plastics market size was valued at USD 532.0 billion in 2025 and is projected to grow from USD 549.56 billion in 2026 to reach USD 646.42 billion by 2031, expanding at a CAGR of 3.3% during the forecast period (2026–2031). The commodity plastics market growth is primarily driven by rising demand from packaging, construction, automotive, consumer goods, and healthcare industries. Increasing urbanization, industrialization in emerging economies, and growing investments in manufacturing infrastructure continue to support demand for polyethylene (PE), polypropylene (PP), polyvinyl chloride (PVC), polyethylene terephthalate (PET), and polystyrene (PS). Furthermore, advancements in recycling technologies and circular economy initiatives are reshaping industry dynamics while ensuring sustained long-term demand for commodity plastics across global value chains.

Key Market Insights

- Packaging remains the largest application segment, accounting for nearly 39% of global commodity plastics consumption due to strong demand from food, beverage, pharmaceutical, and e-commerce sectors.

- Polyethylene (PE) dominates resin demand, representing approximately 35% of the global market owing to its extensive use in flexible packaging, films, containers, and infrastructure applications.

- Asia-Pacific leads the global market, holding approximately 48% of total demand, supported by large-scale manufacturing activities in China, India, Japan, and Southeast Asia.

- India is emerging as the fastest-growing country market, driven by infrastructure development, industrial expansion, and increasing domestic polymer consumption.

- Recycling and circular economy investments are accelerating, with governments and corporations investing heavily in mechanical and chemical recycling technologies.

- Automotive lightweighting and electric vehicle production are creating new demand opportunities for polypropylene, ABS, and other commodity plastics used in vehicle components.

Commodity Plastics Market Trends

Circular Economy and Recycled Plastics Adoption Accelerating

The commodity plastics industry is undergoing a significant transformation as sustainability becomes a strategic priority across global supply chains. Brand owners, retailers, and packaging manufacturers are increasingly committing to recycled-content targets and plastic waste reduction initiatives. This trend is driving investments in advanced mechanical recycling, chemical recycling, and closed-loop collection systems. Governments across Europe, North America, and Asia are implementing recycled-content mandates and extended producer responsibility (EPR) regulations that encourage greater utilization of recycled polymers. As a result, recycled polyethylene, polypropylene, and PET are witnessing increasing adoption across packaging, consumer goods, and automotive applications. Companies are also investing in traceability technologies and digital waste management platforms to improve recycled material recovery rates and support circular economy objectives.

Infrastructure Expansion Driving Construction Plastics Demand

Infrastructure development programs worldwide are increasing demand for commodity plastics used in construction applications. PVC pipes, insulation systems, roofing membranes, drainage systems, and geomembranes continue to gain traction due to their durability, lightweight properties, and cost efficiency. Major government investments in housing, transportation, water management, and smart city projects across India, China, Southeast Asia, and the Middle East are supporting sustained growth. Urbanization and population growth are further driving demand for modern infrastructure, while innovations in polymer formulations are improving product performance and lifecycle costs. Construction-grade commodity plastics are increasingly replacing traditional materials in water distribution networks, electrical conduits, and building systems, creating long-term opportunities for resin producers.

Commodity Plastics Market Drivers

Growing Global Packaging Industry

Packaging continues to be the largest demand center for commodity plastics worldwide. Rapid growth in e-commerce, food delivery services, consumer packaged goods, and pharmaceutical products is driving substantial demand for polyethylene films, polypropylene packaging solutions, PET bottles, and rigid plastic containers. Flexible packaging formats offer cost advantages, improved shelf life, and reduced transportation costs, making them increasingly attractive to manufacturers. Rising urban populations and changing consumer lifestyles are further contributing to packaging consumption across developed and emerging economies.

Expansion of Infrastructure and Construction Activities

Large-scale infrastructure investments are fueling demand for commodity plastics in residential, commercial, and industrial construction projects. PVC and polyethylene products are extensively used in water distribution, sewage systems, cable insulation, flooring, and roofing applications. Government-led infrastructure initiatives, particularly in Asia-Pacific and the Middle East, continue to stimulate demand. Increasing emphasis on affordable housing and urban infrastructure development is expected to maintain strong consumption growth throughout the forecast period.

Commodity Plastics Market Restraints

Environmental Regulations on Single-Use Plastics

Growing environmental concerns surrounding plastic waste are resulting in stricter regulations across multiple regions. Restrictions on single-use plastics, recycling mandates, and producer responsibility frameworks are increasing compliance costs for manufacturers. Regulatory uncertainty in some markets may also affect investment decisions and demand growth for virgin commodity plastics.

Volatility in Petrochemical Feedstock Prices

Commodity plastics are highly dependent on crude oil and natural gas derivatives such as ethylene and propylene. Fluctuations in feedstock prices directly influence production costs and profitability across the value chain. Geopolitical tensions, supply disruptions, and energy market volatility can create pricing uncertainty for manufacturers and downstream users, impacting market stability and investment planning.

Commodity Plastics Market Opportunities

Advanced Recycling and Sustainable Material Development

The growing focus on sustainability presents significant opportunities for both established participants and new entrants. Investments in chemical recycling technologies, waste-to-polymer conversion systems, and high-quality recycled resins are opening new revenue streams. Consumer brands increasingly seek suppliers capable of delivering recycled-content materials that meet performance requirements while supporting sustainability goals. Companies investing early in advanced recycling infrastructure are likely to benefit from premium pricing and long-term customer contracts.

Rapid Industrialization in Emerging Economies

Emerging economies such as India, Vietnam, Indonesia, Saudi Arabia, and Brazil are experiencing increasing demand for commodity plastics across packaging, construction, consumer goods, and automotive industries. Government initiatives including "Make in India," industrial corridor developments, and manufacturing localization programs are encouraging domestic production and consumption of plastics. These regions offer significant growth potential due to rising disposable incomes, urbanization, and expanding manufacturing sectors.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 532.0 Billion |

| Market Size in 2026 | USD 549.56 Billion |

| Market Size in 2031 | USD 646.42 Billion |

| CAGR | 3.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Resin Type Insights

Polyethylene (PE) accounted for approximately 35% of the global commodity plastics market in 2025, making it the largest resin segment. The segment's dominance is primarily driven by its unmatched versatility, cost-effectiveness, chemical resistance, and ease of processing across high-volume applications. PE remains the preferred material for flexible packaging, films, industrial liners, agricultural applications, bottles, containers, and water infrastructure systems. The rapid expansion of global flexible packaging demand, particularly from food, beverage, personal care, and e-commerce industries, continues to drive consumption growth.

Among polyethylene grades, HDPE leads demand within rigid packaging and piping applications due to its superior strength-to-weight ratio, durability, and resistance to moisture and chemicals. Growing investments in water management infrastructure, municipal pipeline projects, and industrial fluid transportation systems are further supporting HDPE demand globally. Meanwhile, LDPE and LLDPE are benefiting from rising consumption of stretch films, shrink films, agricultural films, and protective packaging solutions, particularly across Asia-Pacific and North America.

Polypropylene (PP) remains the second-largest resin category, supported by growing adoption in automotive lightweighting initiatives, reusable packaging solutions, consumer appliances, and industrial products. The automotive industry's focus on fuel efficiency and electric vehicle range optimization continues to increase polypropylene usage in interior and exterior vehicle components. PVC maintains a strong position due to sustained investments in construction and infrastructure projects, while PET demand continues to benefit from growth in bottled beverages, food packaging, and increasing recycled PET (rPET) utilization driven by sustainability regulations worldwide.

Processing Technology Insights

Extrusion represented approximately 31% of global commodity plastics consumption in 2025 and remains the leading processing technology segment. Its market leadership is largely attributed to the widespread use of extruded products across packaging, construction, agriculture, and industrial manufacturing applications. The process enables cost-efficient, high-volume production of films, sheets, pipes, tubing, insulation materials, and profiles, making it indispensable for commodity plastics processing.

The primary growth driver for the extrusion segment is the continued expansion of the flexible packaging industry, which accounts for a substantial share of polyethylene and polypropylene demand globally. Rising demand for food packaging, e-commerce packaging, protective films, and agricultural films has significantly increased extrusion-based production volumes. Furthermore, growing investments in water infrastructure and urban utility networks continue to support extrusion demand through large-scale production of PVC and HDPE piping systems.

Injection molding remains the second-largest processing technology, benefiting from strong demand for automotive components, packaging closures, household products, medical devices, and electrical equipment. Blow molding continues to play a critical role in bottle and container manufacturing, particularly for beverage, pharmaceutical, and personal care industries. Thermoforming is gaining momentum in healthcare and food-service packaging applications, while rotational molding maintains importance in industrial storage tanks, agricultural equipment, and large hollow plastic products.

Application Insights

Films and sheets constituted approximately 28% of the global commodity plastics market in 2025, making them the largest application segment. The segment's leadership is directly linked to rising demand for flexible packaging solutions, which have become the preferred packaging format across food, beverage, pharmaceutical, consumer goods, and logistics industries. Flexible packaging offers advantages including lower material consumption, reduced transportation costs, improved shelf life, and enhanced sustainability performance compared to rigid alternatives. The continued growth of e-commerce, online grocery delivery, and global retail distribution networks has significantly increased demand for protective films, stretch wraps, shrink films, and industrial packaging materials. Additionally, agricultural modernization initiatives across developing economies are boosting consumption of greenhouse films, mulch films, and silage wraps.

Bottles and containers represent another major application area, supported by expanding beverage production, personal care products, and pharmaceutical packaging requirements. Pipes and fittings continue to benefit from increasing investments in water treatment facilities, wastewater infrastructure, irrigation networks, and urban development projects. Automotive parts, electrical components, medical consumables, consumer goods, and textile fibers further demonstrate the extensive application diversity of commodity plastics across global industries.

End-Use Industry Insights

Packaging accounted for approximately 39% of global commodity plastics demand in 2025 and remains the dominant end-use industry. The segment's leadership is supported by continuous growth in food and beverage consumption, pharmaceutical product distribution, consumer packaged goods production, and global e-commerce activities. Increasing urbanization, changing lifestyles, and rising demand for convenience products continue to accelerate packaging consumption across both developed and emerging economies. The packaging industry's transition toward lightweight, cost-efficient, and recyclable materials further strengthens demand for polyethylene, polypropylene, and PET resins. Flexible packaging formats are increasingly replacing traditional packaging materials due to their superior logistics efficiency and lower carbon footprint.

Construction remains the second-largest end-use segment, driven by global investments in residential housing, commercial buildings, transportation infrastructure, and utility networks. PVC pipes, insulation systems, roofing membranes, flooring materials, and cable protection products continue to generate significant demand. Meanwhile, automotive and transportation applications are expanding due to vehicle lightweighting trends and growing electric vehicle production. Healthcare and pharmaceutical applications represent one of the fastest-growing end-use sectors, supported by increasing healthcare expenditures, aging populations, and rising demand for disposable medical products. Agriculture is also emerging as a key growth market, driven by adoption of modern irrigation systems, protected cultivation technologies, greenhouse farming, and crop-yield enhancement initiatives.

Explore more data points, trends and opportunities Download Free Sample Report

Commodity Plastics Market Segmentations

By Resin Type

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polyethylene Terephthalate (PET)

- Polystyrene (PS)

- Acrylonitrile Butadiene Styrene (ABS)

- Polymethyl Methacrylate (PMMA)

By Processing Technology

- Extrusion

- Injection Molding

- Blow Molding

- Thermoforming

- Rotational Molding

- Calendering

- Others

By Application

- Films & Sheets

- Bottles & Containers

- Pipes & Fittings

- Packaging Components

- Consumer Goods

- Electrical Components

- Automotive Parts

- Building Materials

- Medical Consumables

- Fibers & Textiles

By End-Use Industry

- Packaging

- Building & Construction

- Automotive & Transportation

- Electrical & Electronics

- Consumer Goods

- Medical & Pharmaceutical

- Textile & Fibers

- Agriculture

- Industrial Manufacturing

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 48% of global commodity plastics demand in 2025, making it the largest regional market. The region's dominance is driven by its position as the world's largest manufacturing hub, extensive packaging industry, expanding middle-class population, and rapid urbanization. China alone contributes nearly 29% of global demand due to its massive consumer goods, electronics, automotive, construction, and packaging industries. Government investments in industrial modernization, infrastructure expansion, and domestic manufacturing continue to support long-term plastics consumption.

India represents the fastest-growing country market globally, supported by strong GDP growth, infrastructure spending, urban development projects, and initiatives such as Make in India. Rising demand for packaged food, healthcare products, construction materials, and consumer goods is accelerating plastics consumption. Meanwhile, Japan and South Korea maintain strong demand through advanced automotive, semiconductor, and electronics manufacturing sectors. Southeast Asian countries including Vietnam, Indonesia, and Thailand are emerging as key production hubs as manufacturers diversify supply chains beyond China, creating substantial incremental demand for commodity plastics.

North America

North America accounted for approximately 19% of global market demand in 2025. The region's growth is largely supported by abundant shale gas resources, which provide a significant feedstock cost advantage for polyethylene and polypropylene production. The United States remains the dominant market, contributing nearly 16% of global consumption through strong demand from packaging, healthcare, construction, and consumer goods industries.

The region also benefits from advanced recycling infrastructure, increasing adoption of sustainable packaging solutions, and strong investments in medical and pharmaceutical manufacturing. Mexico is emerging as an important growth market due to expanding automotive production, nearshoring trends, and increasing foreign direct investment in manufacturing facilities serving North American supply chains.

Europe

Europe represents approximately 18% of global commodity plastics demand. Germany remains the largest regional market due to its strong automotive manufacturing base, industrial production capabilities, and advanced packaging sector. France, Italy, the United Kingdom, and Spain continue to generate substantial demand across consumer goods, healthcare, food processing, and industrial manufacturing industries.

The primary growth driver in Europe is the region's transition toward a circular economy. Regulatory mandates promoting recycled content, sustainable packaging, and carbon reduction are accelerating investments in recycling infrastructure and advanced polymer technologies. Additionally, increasing demand for lightweight materials in electric vehicles and renewable energy infrastructure is creating new opportunities for commodity plastics manufacturers throughout the region.

Latin America

Latin America accounted for approximately 7% of global commodity plastics demand in 2025. Brazil remains the largest market due to its extensive consumer goods, food processing, packaging, and agricultural sectors. Rising urbanization and growing middle-class consumption continue to support plastics demand across household products, packaged food, and personal care applications.

The region's growth is increasingly driven by agricultural modernization, infrastructure investments, and industrial expansion. Demand for irrigation systems, greenhouse films, water management solutions, and flexible packaging continues to rise. Mexico also serves as a strategic manufacturing hub linked to North American automotive and industrial supply chains, further strengthening regional plastics consumption.

Middle East & Africa

The Middle East & Africa region represented approximately 8% of global demand in 2025 and is expected to witness above-average growth during the forecast period. The Middle East benefits from abundant hydrocarbon feedstocks and large-scale petrochemical investments, particularly in Saudi Arabia, the UAE, and Qatar. Government-led industrial diversification programs such as Saudi Vision 2031 are encouraging downstream plastics manufacturing and value-added industrial production.

Across Africa, rapid population growth, urbanization, and infrastructure development are driving increasing demand for commodity plastics in packaging, construction, healthcare, and agriculture. Investments in water distribution systems, sanitation infrastructure, housing projects, and food packaging industries are expected to create significant long-term growth opportunities. Furthermore, rising consumer goods manufacturing and retail sector expansion across countries such as South Africa, Nigeria, Egypt, and Kenya are contributing to increasing regional plastics consumption.

Key Players in the Commodity Plastics Market

- Exxon Mobil Corporation

- LyondellBasell Industries

- SABIC

- Dow Inc.

- INEOS

- Chevron Phillips Chemical

- Formosa Plastics Corporation

- Sinopec

- BASF SE

- LG Chem

- Sumitomo Chemical

- Braskem

- Reliance Industries Limited

- Borealis AG

- TotalEnergies Petrochemicals