Coconut Gel Market Size

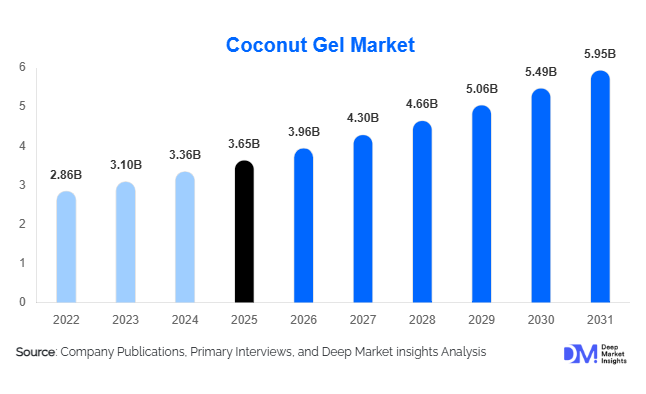

According to Deep Market Insights, the global coconut gel market size was valued at approximately USD 3.65 billion in 2025 and is projected to grow from USD 3.96 billion in 2026 to reach USD 5.95 billion by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The coconut gel market growth is primarily driven by increasing demand for functional food ingredients, rising consumption of Asian-inspired desserts and beverages, growing adoption of plant-based dietary products, and expanding applications of bacterial cellulose in food, nutraceutical, personal care, and biomedical industries. Coconut gel, commonly known as nata de coco, is increasingly being utilized as a low-calorie, high-fiber ingredient that aligns with consumer preferences for clean-label and natural food products.

Key Market Insights

- Coconut gel consumption is increasingly shifting toward functional food and beverage applications, supported by growing awareness of digestive health and dietary fiber benefits.

- Asia-Pacific dominates global production and consumption, with the Philippines, Indonesia, Thailand, and Vietnam serving as major manufacturing and export hubs.

- Ready-to-drink beverages and bubble tea applications represent one of the fastest-growing demand segments, driven by consumer preference for textured beverage experiences.

- North America and Europe are witnessing rising demand for clean-label dessert ingredients, supporting imports of flavored and premium coconut gel products.

- Nutraceutical and bacterial cellulose applications are emerging as high-growth opportunities, expanding coconut gel usage beyond traditional food categories.

- Product innovation through organic, fortified, and specialty-flavored coconut gel formulations is enhancing market penetration across developed economies.

Coconut Gel Market Latest Trends

Growing Demand for Functional and Fiber-Rich Ingredients

Consumers worldwide are increasingly seeking food products that provide both nutritional and functional benefits. Coconut gel contains significant amounts of dietary fiber while remaining low in fat and calories, making it attractive to health-conscious consumers. Food manufacturers are incorporating coconut gel into yogurt products, fruit cups, plant-based desserts, and functional snacks to improve texture and nutritional profiles. The trend toward digestive wellness and gut-health-focused diets has further accelerated adoption across developed and emerging markets. Manufacturers are also launching fortified variants containing vitamins, minerals, and prebiotic ingredients to cater to premium wellness segments.

Expansion of Bubble Tea and Specialty Beverage Applications

The rapid global growth of bubble tea chains and specialty beverage outlets has created substantial demand for coconut gel inclusions. Coconut gel cubes and strips are increasingly used as alternatives to tapioca pearls due to their lower caloric content and unique texture. Beverage manufacturers are also introducing ready-to-drink products containing nata de coco pieces, particularly across Asia-Pacific, North America, and Europe. The popularity of experiential beverages among younger consumers is encouraging innovation in flavor combinations, packaging formats, and premium beverage offerings that incorporate coconut gel as a key ingredient.

Coconut Gel Market Drivers

Rising Popularity of Plant-Based and Natural Foods

The global shift toward plant-based diets has significantly strengthened demand for coconut-derived ingredients. Coconut gel is entirely plant-based and fits within vegan, vegetarian, and clean-label product portfolios. Food manufacturers are increasingly utilizing coconut gel as a natural texture enhancer and low-calorie ingredient in dairy alternatives, desserts, and functional foods. Growing consumer scrutiny of artificial additives and synthetic ingredients further supports demand for naturally fermented coconut gel products.

Expansion of Processed Food and Beverage Industries

Rapid growth in processed food consumption across Asia-Pacific, North America, and Europe continues to create new opportunities for coconut gel suppliers. Manufacturers are incorporating nata de coco into fruit preparations, dessert cups, ice creams, frozen desserts, bakery fillings, and beverage products. The increasing popularity of convenience foods and ready-to-consume snacks is driving steady volume demand from industrial food processors globally.

Growing Export Demand from Asian Producing Countries

The Philippines, Indonesia, Thailand, and Vietnam have established robust coconut processing industries and continue to expand exports of value-added coconut products. Improved processing technologies, greater production efficiency, and increasing global awareness of Asian dessert ingredients are supporting export growth. Strong international demand from North America, Europe, and the Middle East has encouraged investments in large-scale production facilities dedicated to coconut gel manufacturing.

Coconut Gel Market Restraints

Dependence on Coconut Supply and Agricultural Variability

Coconut gel production relies heavily on coconut water availability, making the industry susceptible to fluctuations in coconut harvests. Weather disruptions, climate change impacts, pest outbreaks, and agricultural productivity challenges can influence raw material availability and pricing. Supply chain disruptions in major producing countries may create temporary shortages and affect production costs for manufacturers.

Limited Consumer Awareness in Developed Markets

Although coconut gel enjoys widespread popularity across Asia, consumer awareness remains relatively limited in several Western markets. Many consumers remain unfamiliar with nata de coco applications and nutritional benefits. Manufacturers must invest in education, marketing campaigns, and product innovation to expand adoption beyond ethnic food channels and mainstream retail segments.

Coconut Gel Industry Key Opportunities

Expansion into Nutraceutical and Functional Food Products

The nutraceutical industry presents a significant growth avenue for coconut gel manufacturers. High dietary fiber content and bacterial cellulose properties support applications in digestive health products, weight-management foods, and functional nutrition formulations. Manufacturers can develop premium products targeting wellness-focused consumers while commanding higher profit margins than conventional food applications. As global preventive healthcare spending continues to increase, coconut gel-based functional ingredients are expected to gain wider commercial acceptance.

Growth of Organic and Premium Product Categories

Consumer willingness to pay premium prices for organic and sustainably sourced products is creating opportunities for differentiation. Organic coconut gel products remain a relatively underpenetrated segment globally. Producers capable of obtaining organic certifications, traceability standards, and sustainability credentials can access premium retail channels across North America, Europe, Japan, and Australia. Premium flavored variants also provide opportunities for higher-margin product portfolios.

Industrial Applications of Bacterial Cellulose

Beyond food applications, bacterial cellulose derived from coconut gel fermentation is attracting interest from pharmaceutical, wound care, biomedical, and cosmetic industries. Research into advanced cellulose materials for medical dressings, tissue engineering, and cosmetic formulations continues to expand. These emerging applications offer manufacturers diversification opportunities and access to higher-value specialty markets with stronger long-term growth potential.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.65 Billion |

| Market Size in 2026 | USD 3.96 Billion |

| Market Size in 2031 | USD 5.95 Billion |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Processing clarifiers represent the largest product category in the global beer clarifiers market, with silica gel clarifiers accounting for approximately 28% of total market revenue in 2025. The segment’s leadership is primarily driven by the increasing emphasis on beer clarity, colloidal stability, and extended shelf life across both commercial and craft brewing operations. Silica gel clarifiers are extensively used due to their effectiveness in selectively adsorbing haze-forming proteins while preserving beer flavor, aroma, color, and foam characteristics. As breweries continue to focus on delivering visually appealing and quality-consistent products, demand for silica gel-based clarification solutions remains strong. The growing international trade of beer and rising consumer expectations for premium-quality beverages are further supporting the adoption of advanced protein stabilization technologies.PVPP clarifiers continue to account for a substantial share of the market owing to their superior capability to remove polyphenols responsible for oxidative instability and chill haze formation. Their importance has increased as breweries seek to improve product freshness and maintain flavor stability throughout extended storage and distribution periods. Enzyme-based clarifiers are emerging as one of the fastest-growing product categories, supported by the brewing industry's shift toward process optimization, sustainability, and production efficiency. These solutions help reduce maturation times, improve filtration performance, lower energy consumption, and minimize production bottlenecks. Clarification equipment, including membrane filtration systems, centrifuges, and crossflow filtration technologies, is also witnessing growing demand among large breweries seeking automation, reduced product losses, enhanced throughput, and improved operational consistency.

Source Insights

Synthetic clarifiers dominated the global beer clarifiers market in 2025, accounting for approximately 36% of total revenue. The segment’s leading position is driven by their reliable performance, high process consistency, scalability, and compatibility with large-scale brewing operations. Industrial breweries continue to prefer synthetic clarifiers because they provide predictable clarification outcomes, facilitate quality control, and support high-volume production requirements. Their ability to deliver uniform results across multiple production batches remains a key factor supporting widespread adoption.Mineral-based clarifiers maintain a notable share of the market due to their cost-effectiveness, widespread availability, and long-standing use within brewing applications. Their ability to efficiently remove suspended particles while maintaining economical processing costs makes them particularly attractive among regional and value-focused breweries. Plant-based clarifiers are experiencing rapid growth as breweries increasingly align their production processes with consumer demand for vegan-certified, clean-label, and naturally sourced products. Growing awareness regarding ingredient transparency and sustainable brewing practices is encouraging greater adoption of botanical clarification solutions. Enzyme-based clarifiers are also gaining traction due to their ability to reduce processing times, improve filtration efficiency, lower resource consumption, and support environmental sustainability goals, positioning them as a key growth area within the market.

Brewing Stage Insights

Final beer stabilization and clarification account for the largest share of market demand, representing approximately 33% of total revenue in 2025. The dominance of this segment is primarily attributed to the critical role clarification plays in ensuring visual clarity, flavor consistency, microbiological stability, and shelf-life performance before packaging. As breweries compete to deliver premium-quality products and strengthen brand differentiation, investments in final-stage clarification technologies continue to increase. The ability to maintain product appearance and stability throughout storage and transportation remains a major priority for breweries globally.Fermentation clarification and maturation-stage clarification also contribute significantly to market demand as breweries increasingly focus on improving production efficiency and reducing process timelines. Clarification during fermentation helps minimize suspended solids and enhances downstream processing performance, while maturation-stage clarification supports flavor development and long-term product stability. Growing investments in brewery modernization, process optimization, and advanced filtration technologies are encouraging breweries to implement clarification solutions throughout multiple stages of production. This trend is particularly evident among large commercial brewers seeking to maximize throughput, reduce waste, and maintain consistent product quality.

Brewery Scale Insights

Macro breweries remain the largest consumers of beer clarifiers, accounting for nearly 52% of global market demand in 2025. The leading position of this segment is driven by large production volumes, stringent quality control requirements, and the need to ensure product consistency across extensive distribution networks. Global beer manufacturers continue to invest heavily in clarification technologies to maintain product stability, optimize operational efficiency, and comply with increasingly demanding quality standards. The growing scale of international beer exports and premium product offerings further supports sustained demand from macro breweries.Regional breweries represent an important customer segment as premium beer consumption continues to expand across developed and emerging markets. These breweries increasingly adopt advanced clarification solutions to enhance product quality while maintaining production flexibility. Craft breweries and microbreweries are among the fastest-growing end users of beer clarifiers, supported by rising consumer interest in specialty, artisanal, and premium beer products. The need to preserve flavor authenticity while achieving desired clarity standards is driving investment in innovative clarification technologies within the craft brewing sector. Brewpubs are also adopting specialized clarification products to improve consistency and support premium small-batch beer production.

Function Insights

Haze removal remains the leading functional application in the beer clarifiers market, accounting for approximately 39% of total demand in 2025. The segment’s dominance is driven by growing consumer preference for visually clear and aesthetically appealing beer products, particularly within premium lager, pilsner, and export beer categories. Beer clarity continues to serve as a key quality indicator for consumers, making haze prevention a critical objective for breweries worldwide. Increasing competition within the premium beer segment and heightened focus on product presentation are further accelerating investments in haze-removal technologies.Shelf-life enhancement and flavor stability improvement are becoming increasingly important functions as breweries expand export operations and establish broader distribution networks. Clarification technologies help reduce oxidation-related quality degradation, maintain freshness, and support longer storage durations, making them essential for export-oriented producers. Polyphenol reduction and protein stabilization applications also contribute significantly to market growth by preventing haze formation and improving colloidal stability. As breweries continue to prioritize product quality, consistency, and customer satisfaction, demand for multifunctional clarification solutions is expected to increase steadily.

Explore more data points, trends and opportunities Download Free Sample Report

Coconut Gel Market Segmentations

By Product Type

- Plain Coconut Gel

- Flavored Coconut Gel

- Fortified Coconut Gel

- Organic Coconut Gel

- Conventional Coconut Gel

By Physical Form

- Cubes

- Strips

- Pearls

- Sheets

- Powdered Coconut Gel Ingredients

By Application

- Desserts

- Bakery Fillings & Toppings

- Dairy Products

- Frozen Desserts

- Fruit Preparations

- Bubble Tea & Specialty Beverages

- Ready-to-Drink Beverages

- Nutraceuticals & Functional Foods

- Cosmetics & Personal Care

- Pharmaceutical & Biomedical Applications

- Industrial Bacterial Cellulose Applications

By Distribution Channel

- Food & Beverage Manufacturers (B2B)

- Foodservice & Hospitality (B2B)

- Hypermarkets & Supermarkets

- Convenience Stores

- Specialty Stores

- Online Retail

By End-Use Industry

- Food Manufacturing

- Beverage Manufacturing

- Foodservice & Hospitality

- Retail Consumer Products

- Personal Care & Cosmetics

- Pharmaceutical & Healthcare

Regional Insights

Europe

Europe accounted for approximately 34% of the global beer clarifiers market in 2025, making it the largest regional market. Germany leads regional demand with nearly 11% of global market revenue, supported by its extensive brewing industry, strong export performance, and deep-rooted brewing heritage. Other major contributors include the United Kingdom, Belgium, France, the Netherlands, Italy, and Spain, all of which maintain mature beer industries and strong premium beer consumption patterns. The region benefits from highly developed brewing infrastructure, stringent quality regulations, and widespread adoption of advanced beer processing technologies.Regional growth is primarily driven by the strong presence of premium and specialty beer segments, increasing demand for export-quality products, ongoing investments in brewery modernization, and the adoption of advanced filtration and stabilization technologies. Additionally, growing consumer preference for clean-label products, rising demand for vegan-certified beer, and increasing implementation of sustainable brewing practices are encouraging breweries to adopt innovative clarification solutions. Continuous product innovation and a strong focus on maintaining beer quality standards further reinforce Europe’s leadership position in the global market.

North America

North America represented approximately 28% of global beer clarifiers market revenue in 2025. The United States accounted for nearly 23% of worldwide demand, supported by its large brewing sector, extensive network of craft breweries, and strong demand for premium and specialty beer products. Canada contributes steadily through investments in brewing innovation, premium beer production, and modernization of processing facilities.Market growth in the region is being driven by the continued expansion of craft brewing, increasing premiumization trends, rising consumer expectations regarding beer quality and consistency, and growing investments in sustainable production technologies. The increasing adoption of vegan-friendly and environmentally responsible clarification agents is further supporting demand. Breweries across North America are also investing in automation, advanced filtration systems, and process optimization technologies to improve operational efficiency and maintain competitive differentiation, creating favorable conditions for continued clarifier adoption.

Asia-Pacific

Asia-Pacific accounted for approximately 24% of the global beer clarifiers market in 2025 and is expected to register the fastest growth during the forecast period. China remains the largest regional market due to its substantial brewing capacity, large consumer base, and growing demand for premium beer products. India is emerging as the fastest-growing national market, supported by brewery expansion projects, rising disposable incomes, rapid urbanization, and increasing acceptance of premium alcoholic beverages. Japan, South Korea, Vietnam, Thailand, and Australia continue to invest in advanced brewing technologies and quality-enhancement initiatives.The region’s growth is being fueled by rising beer consumption, rapid expansion of brewing infrastructure, increasing penetration of international beer brands, and growing consumer preference for premium and craft beer products. Expanding middle-class populations, changing lifestyle preferences, and increasing spending on alcoholic beverages are further contributing to market development. Additionally, ongoing investments in brewery modernization, foreign direct investment in beverage manufacturing, and greater adoption of advanced processing technologies are accelerating demand for beer clarification solutions across Asia-Pacific.

Latin America

Latin America accounted for approximately 8% of global market revenue in 2025. Brazil leads regional demand due to its large beer production industry, substantial domestic consumption, and expanding premium beer segment. Mexico and Argentina also contribute significantly to regional revenue, supported by growing export activity, modernization initiatives, and increasing investments in brewing technology.Regional growth is being driven by rising disposable incomes, expansion of the middle-class population, increasing demand for premium and flavored beer products, and ongoing improvements in brewing infrastructure. Breweries across the region are adopting advanced clarification technologies to enhance product quality, improve shelf-life performance, and meet export-quality requirements. The gradual development of craft beer industries and the growing popularity of premium beer experiences are creating additional opportunities for clarification solution providers throughout Latin America.

Middle East & Africa

The Middle East and Africa accounted for approximately 6% of global beer clarifiers market revenue in 2025. South Africa remains the largest market in the region, supported by established brewing operations, growing adoption of modern processing technologies, and increasing demand for quality-focused beer production. The United Arab Emirates and Saudi Arabia are emerging growth markets, particularly within the non-alcoholic malt beverage segment, where clarification technologies play a crucial role in ensuring product stability, appearance, and flavor consistency.Growth across the region is being supported by rising investments in beverage manufacturing infrastructure, increasing consumption of malt-based and non-alcoholic beverages, expanding food and beverage industries, and greater adoption of advanced processing equipment. Rapid urbanization, improving retail distribution networks, and increasing consumer preference for premium-quality beverages are further encouraging manufacturers to invest in modern clarification technologies. In addition, government-led industrial diversification initiatives and growing investments in food processing capabilities are expected to create long-term opportunities for market expansion across the Middle East and Africa.

Key Players in the Coconut Gel Market

- Century Pacific Food Inc.

- Axelum Resources Corp.

- Franklin Baker Company

- PT Pulau Sambu Group

- Viet Delta Corporation

- Theppadungporn Coconut Co., Ltd.

- Coco Asenso Philippines Inc.

- Happy Alliance (M) Sdn. Bhd.

- Schmecken Agro Food Products

- Nata de Coco Manufacturing Sdn. Bhd.

- Celebes Coconut Corporation

- Peter Paul Philippine Corporation

- Celebes Canning Corporation

- Primex Coco Products Inc.

- Thai Coconut Public Company Limited