Global Citrus Fruits Market Size

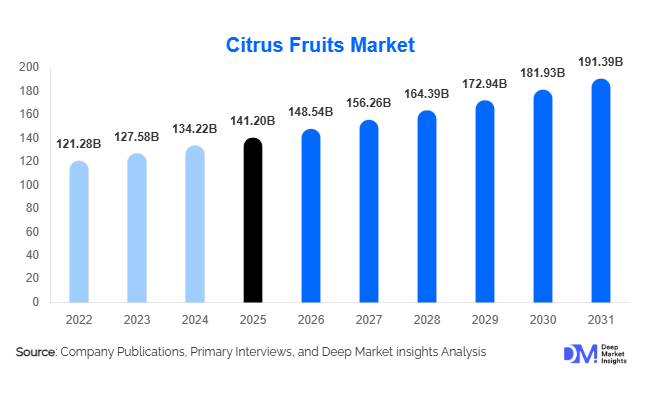

According to Deep Market Insights, the global citrus fruits market size was valued at USD 141.2 billion in 2025 and is projected to grow from USD 148.54 billion in 2026 to reach USD 191.39 billion by 2031, expanding at a CAGR of 5.2% during the forecast period (2026–2031). The citrus fruits market growth is primarily driven by increasing consumer demand for vitamin-rich foods, rising health awareness, expanding global fruit trade, growing utilization of citrus fruits in food processing and beverage manufacturing, and the increasing adoption of citrus-derived ingredients in nutraceutical and pharmaceutical applications. The market continues to benefit from improvements in cold-chain infrastructure, export-oriented cultivation, and technological advancements in citrus farming, enabling producers to serve both domestic and international markets more efficiently.

Key Market Insights

- Oranges remain the dominant citrus fruit category, accounting for nearly 48% of global market revenue due to their extensive use in fresh consumption and juice processing.

- Fresh citrus fruits account for over 70% of total market demand, supported by growing consumer preference for natural and minimally processed foods.

- Asia-Pacific dominates the global citrus fruits market, led by strong consumption and production in China and India.

- Organic citrus fruits are growing faster than conventional varieties, driven by increasing consumer demand for pesticide-free and sustainably cultivated produce.

- Export-oriented citrus production is expanding rapidly in Egypt, South Africa, Turkey, Peru, and India.

- Precision agriculture, disease-resistant varieties, and smart irrigation technologies are improving citrus yields and farm profitability globally.

Global Citrus Fruits Market Latest Trends

Rapid Growth of Organic and Sustainable Citrus Production

Organic citrus fruits are emerging as one of the fastest-growing segments within the global citrus fruits market. Consumers across North America, Europe, Japan, South Korea, and urban Asia are increasingly demanding fruits produced without synthetic pesticides and fertilizers. Retailers are expanding shelf space dedicated to organic produce, while governments continue supporting sustainable agricultural practices through certification and incentive programs. Citrus growers are adopting regenerative agriculture techniques, biological pest control solutions, precision irrigation systems, and carbon footprint reduction initiatives to meet evolving consumer expectations. Sustainability certifications are becoming critical purchasing criteria among premium retailers and international importers, creating long-term opportunities for producers capable of demonstrating environmentally responsible farming practices.

Expansion of Citrus-Based Functional Foods and Beverages

The use of citrus fruits in functional food and beverage applications is increasing significantly. Manufacturers are incorporating citrus extracts, vitamin C concentrates, flavonoids, and citrus bioactive compounds into fortified beverages, dietary supplements, sports nutrition products, and wellness-focused food formulations. Consumers increasingly associate citrus fruits with immunity enhancement, digestive health, and antioxidant benefits, driving demand beyond traditional fresh fruit consumption. Food processors are also developing citrus-infused snacks, low-sugar beverages, plant-based products, and nutraceutical formulations that leverage the health attributes of citrus ingredients. This trend is expanding revenue opportunities throughout the citrus value chain while supporting long-term market growth.

Global Citrus Fruits Market Drivers

Increasing Consumer Focus on Health and Immunity

The growing emphasis on preventive healthcare and nutritional wellness is significantly increasing citrus fruit consumption worldwide. Citrus fruits remain among the most recognized natural sources of vitamin C, antioxidants, flavonoids, and dietary fiber. Consumers are increasingly incorporating oranges, lemons, mandarins, grapefruits, and limes into their daily diets to support immunity and overall health. The long-term behavioral shift toward healthier eating habits continues to strengthen demand across both developed and emerging economies.

Growing Demand from Juice and Food Processing Industries

The expansion of juice manufacturing, beverage production, food ingredient processing, and nutraceutical applications is creating substantial demand for citrus fruits. Citrus fruits serve as key raw materials for juice concentrates, flavor ingredients, confectionery products, bakery applications, dietary supplements, and functional beverages. Industrial demand provides stable procurement volumes and supports market growth beyond retail fresh fruit consumption. Increasing investments in citrus processing infrastructure are further strengthening the industry's growth trajectory.

Expansion of Global Citrus Trade Networks

International citrus trade continues to grow as importing nations seek year-round fruit availability. Major exporters including Spain, Egypt, South Africa, Turkey, Mexico, Brazil, and China are expanding shipments to Europe, Asia-Pacific, and Middle Eastern markets. Improved cold storage facilities, containerized transportation systems, and advanced post-harvest technologies are enabling producers to access distant markets while maintaining product quality. Trade diversification is creating new revenue streams for citrus-producing countries and supporting global market expansion.

Global Citrus Fruits Market Restraints

Climate Variability and Citrus Disease Outbreaks

The citrus industry remains vulnerable to weather-related disruptions such as droughts, floods, heat waves, and unpredictable rainfall patterns. Climate change is affecting citrus productivity in several key growing regions. Additionally, citrus greening disease (HLB), citrus canker, and other plant health challenges continue to threaten orchard productivity and fruit quality. These factors contribute to supply fluctuations and increased production risks.

Rising Production and Logistics Costs

Increasing labor costs, fertilizer expenses, irrigation investments, packaging costs, and transportation charges are putting pressure on producer margins. Water scarcity in several citrus-producing regions has further increased cultivation costs. Exporters also face higher logistics expenses due to global shipping volatility, which can affect competitiveness in international markets and limit profitability for smaller producers.

Global Citrus Fruits Industry Key Opportunities

Nutraceutical and Functional Ingredient Expansion

The nutraceutical industry presents a major opportunity for citrus producers and processors. Citrus-derived compounds such as vitamin C, hesperidin, limonene, pectin, and bioflavonoids are increasingly used in dietary supplements, immunity products, pharmaceutical formulations, and wellness beverages. Companies capable of integrating citrus cultivation with ingredient extraction operations can capture significantly higher margins than those focused solely on fresh fruit sales. The growing global wellness industry is expected to create sustained demand for citrus-derived functional ingredients over the coming decade.

Export-Oriented Citrus Production and Trade Growth

Rising import demand from Europe, East Asia, Southeast Asia, and the Middle East continues to create substantial opportunities for citrus-exporting countries. Egypt, South Africa, Turkey, Peru, and India are expanding export-oriented citrus cultivation to capitalize on growing international demand. Investments in grading facilities, cold storage infrastructure, traceability systems, and logistics networks are enabling producers to access premium overseas markets. Export diversification strategies are expected to generate significant revenue growth opportunities for both existing participants and new entrants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 141.20 Billion |

| Market Size in 2026 | USD 148.54 Billion |

| Market Size in 2031 | USD 191.39 Billion |

| CAGR | 5.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Fruit Type Insights

Oranges dominate the global citrus fruits market, accounting for approximately 48% of total market revenue in 2025. Their leadership position is supported by widespread consumption in both fresh and processed forms, particularly within juice manufacturing. Mandarins and tangerines represent the second-largest category, benefiting from increasing consumer preference for easy-to-peel and convenient fruit varieties. Lemons and limes continue experiencing strong demand from foodservice, beverage manufacturing, and flavor ingredient industries. Grapefruits maintain a stable market position, particularly in North America and select European countries. Specialty citrus varieties including pomelos, yuzu, and kumquats are gaining popularity among premium consumers seeking differentiated fruit experiences and exotic flavor profiles.

Application Insights

Direct fresh consumption remains the largest application segment, accounting for approximately 56% of total citrus fruit demand globally. Consumers continue prioritizing fresh fruits as part of healthy dietary routines, supporting strong retail sales across major markets. Juice processing represents the second-largest application segment, driven by growing demand for natural fruit beverages and concentrates. Food processing applications including bakery products, confectionery, sauces, and prepared foods continue expanding. Nutraceutical and dietary supplement applications are among the fastest-growing segments, benefiting from rising demand for immunity-supporting ingredients. Flavor and fragrance manufacturers are increasingly utilizing citrus oils and extracts in cosmetics, personal care products, and household cleaning formulations.

Distribution Channel Insights

Supermarkets and hypermarkets dominate citrus fruit distribution, accounting for approximately 41% of global sales. Organized retail chains offer extensive product variety, quality assurance, and convenient access to consumers. Traditional grocery stores continue maintaining significant market share, particularly in developing economies where informal retail channels remain important. Online retail platforms are emerging as one of the fastest-growing distribution channels, supported by increasing adoption of grocery delivery services and digital commerce platforms. Wholesale markets remain essential for foodservice operators, processors, and institutional buyers, while direct farm-to-business sales are gaining traction among large-scale commercial customers seeking supply chain efficiencies.

End-Use Insights

Household consumers represent the largest end-use segment, accounting for approximately 53% of global citrus fruit demand. Daily consumption patterns and growing health consciousness continue supporting strong retail demand. Food and beverage manufacturers constitute the largest industrial end-use segment, utilizing citrus fruits in juices, concentrates, confectionery products, dairy applications, and ready-to-drink beverages. Nutraceutical and pharmaceutical companies are increasingly incorporating citrus-derived ingredients into supplements and wellness formulations. Flavor and fragrance manufacturers continue expanding their use of citrus oils and extracts, while foodservice operators remain important buyers due to growing demand for citrus-based menu offerings and beverages.

Trade Type Insights

Domestic consumption remains the largest trade category, accounting for approximately 68% of total citrus fruit market revenue. Large producing countries such as China, India, Brazil, and the United States consume substantial portions of domestic production. However, export markets are growing faster than domestic consumption in several producing regions. International citrus trade continues to expand due to increasing demand for year-round fruit availability, premium imported varieties, and processed citrus products. Export-oriented production models are becoming increasingly important in countries such as Egypt, South Africa, Turkey, Peru, and Spain, which have established strong positions within global citrus trade networks.

Explore more data points, trends and opportunities Download Free Sample Report

Citrus Fruits Market Segmentations

By Fruit Type

- Oranges

- Mandarins & Tangerines

- Lemons

- Limes

- Grapefruits

- Pomelos

- Kumquats

- Yuzu

- Other Specialty Citrus Fruits

By Product Form

- Fresh Citrus Fruits

- Frozen Citrus Fruits

- Dried/Dehydrated Citrus Fruits

- Citrus Purees

- Citrus Pulp

- Citrus Concentrates

By Cultivation Method

- Conventional Citrus Fruits

- Organic Citrus Fruits

- Integrated Pest Management (IPM) Citrus Fruits

- Regenerative Agriculture Citrus Fruits

By Application

- Direct Fresh Consumption

- Juice Processing

- Food Processing

- Beverage Manufacturing

- Nutraceuticals & Dietary Supplements

- Flavors & Fragrances

- Essential Oils Extraction

- Animal Feed & By-products

- Pharmaceutical Ingredients

By Distribution Channel

- Supermarkets & Hypermarkets

- Traditional Grocery Stores

- Wholesale Markets

- Convenience Stores

- Specialty Fruit Retailers

- Foodservice Distributors

- Online Retail

Regional Insights

Asia-Pacific

Asia-Pacific is the largest regional market, accounting for approximately 38% of global citrus fruits market revenue in 2025. China represents the largest citrus-consuming and producing country globally, supported by extensive cultivation acreage and rising household demand. India is emerging as one of the fastest-growing markets due to increasing health awareness, urbanization, and expanding fruit consumption. Japan and South Korea remain important premium markets characterized by strong demand for high-quality citrus varieties. Australia continues to strengthen its export position through premium citrus production and growing shipments to Asian markets.

Europe

Europe accounts for approximately 24% of the global market and remains a major citrus-importing region. Spain dominates European production and export activities, serving as the region’s primary citrus supplier. Germany, France, the United Kingdom, Italy, and the Netherlands represent major consumption centers. European consumers continue driving demand for organic, sustainably sourced, and premium-quality citrus fruits. Strict quality standards and sustainability requirements are shaping sourcing decisions across the region.

North America

North America accounts for nearly 20% of global citrus fruit demand. The United States remains the dominant market due to strong fresh fruit consumption and extensive juice processing activities. Florida and California continue serving as key production hubs, despite challenges associated with citrus greening disease. Mexico plays a dual role as both a major producer and exporter, while Canada remains heavily dependent on imports due to limited domestic production capabilities.

Latin America

Latin America represents approximately 11% of the global market. Brazil remains the region's largest producer and a leading global supplier of orange juice concentrates. Argentina, Chile, and Peru continue expanding export-oriented citrus production, supported by favorable climatic conditions and growing international demand. The region benefits from strong agricultural expertise and increasing investments in export infrastructure.

Middle East & Africa

The Middle East and Africa account for approximately 7% of global citrus fruit demand. Egypt has emerged as one of the world's fastest-growing citrus exporters, leveraging competitive production costs and strong export infrastructure. South Africa remains a critical supplier to European and Asian markets. Gulf countries including Saudi Arabia and the UAE continue increasing imports due to limited domestic production and growing consumer demand for fresh fruit. The region is expected to experience robust growth as export-oriented citrus production continues expanding.

Key Players in the Global Citrus Fruits Market

- Sunkist Growers

- Fresh Del Monte Produce

- Dole plc

- Wonderful Citrus

- T&G Global

- San Miguel Corporation

- AMC Group

- Citrosuco

- Louis Dreyfus Company

- Cutrale Group

- Limoneira Company

- Seeka Limited

- Costa Group

- Rio Grande Valley Citrus

- Bama Citrus Operations