Chocolate Confectionery Market Size

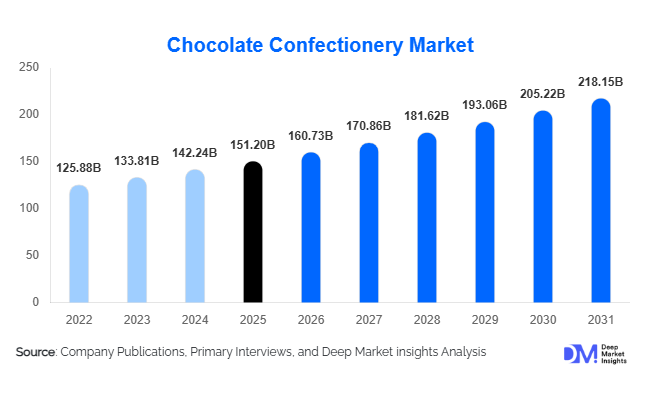

According to Deep Market Insights, the global chocolate confectionery market size was valued at USD 151.2 billion in 2025 and is projected to grow from USD 160.73 billion in 2026 to reach USD 218.15 billion by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The chocolate confectionery market growth is primarily driven by rising premium chocolate consumption, expanding gifting culture, increasing demand for indulgent snacks, and growing consumer preference for dark chocolate, organic products, and functional confectionery offerings. Rapid expansion of e-commerce channels, premium packaging innovations, and strong seasonal demand across developed and emerging economies are further supporting long-term market expansion.

Key Market Insights

- Premium and artisanal chocolate products are gaining strong traction globally, driven by rising consumer willingness to pay for higher cocoa content, ethical sourcing, and unique flavor experiences.

- Dark chocolate consumption is expanding rapidly, supported by increasing health awareness and demand for reduced-sugar confectionery products.

- Europe dominates the global chocolate confectionery market, led by strong per-capita consumption across Germany, Switzerland, the U.K., and France.

- Asia-Pacific remains the fastest-growing regional market, fueled by urbanization, rising disposable incomes, and expanding premium gifting culture in China and India.

- E-commerce and direct-to-consumer chocolate retailing are transforming purchasing behavior, particularly among younger and digitally connected consumers.

- Sustainable cocoa sourcing and recyclable packaging initiatives are becoming major competitive differentiators among global manufacturers.

Chocolate Confectionery Market Latest Trends

Premiumization and Gourmet Chocolate Expansion

Consumers are increasingly shifting toward premium chocolate confectionery products that emphasize superior ingredients, artisanal production methods, and elevated sensory experiences. Premium dark chocolate, single-origin cocoa products, handcrafted truffles, and gourmet chocolate assortments are witnessing robust growth across North America, Europe, Japan, and urban Asia-Pacific markets. Manufacturers are launching innovative flavor combinations involving sea salt, exotic fruits, nuts, spices, botanical infusions, and alcohol-inspired fillings to differentiate their premium portfolios. Seasonal gifting collections and personalized packaging are also contributing significantly to premium segment growth. Luxury chocolate boutiques and experiential retail formats are further enhancing consumer engagement by offering tasting sessions, limited-edition launches, and customizable chocolate products.

Health-Conscious and Functional Chocolate Innovation

Health and wellness trends are increasingly reshaping the global chocolate confectionery market. Consumers are seeking products with lower sugar content, higher cocoa percentages, clean-label ingredients, and functional benefits such as protein enrichment, probiotics, adaptogens, and antioxidant properties. Dark chocolate is particularly benefiting from consumer perception regarding cardiovascular and mood-enhancing benefits. Vegan, dairy-free, organic, and keto-friendly chocolate variants are expanding rapidly as manufacturers target health-conscious millennials and Gen Z consumers. Companies are also investing heavily in sugar-reduction technologies and alternative sweeteners to comply with evolving nutritional regulations while maintaining taste quality and texture consistency.

Chocolate Confectionery Market Drivers

Growing Demand for Premium Indulgence Products

The increasing global appetite for premium indulgent snacks remains one of the primary growth drivers for the chocolate confectionery market. Consumers across both developed and emerging economies are increasingly viewing chocolate as an affordable luxury product associated with emotional comfort, gifting, celebration, and self-reward behavior. Premium chocolate bars, artisanal pralines, luxury truffle collections, and seasonal assortments are experiencing significant demand growth. High-income consumers are particularly driving demand for ethically sourced cocoa, organic certifications, and handcrafted premium chocolate experiences. In addition, premiumization allows manufacturers to improve pricing power and profitability despite rising raw material costs.

Expansion of Modern Retail and Digital Commerce

The rapid expansion of supermarkets, hypermarkets, convenience retail chains, and e-commerce platforms has substantially improved chocolate accessibility globally. Digital retail channels are enabling consumers to access premium international brands, personalized gifting assortments, subscription boxes, and direct-to-consumer chocolate offerings. Online gifting during festivals and celebrations has emerged as a major revenue driver, particularly across Asia-Pacific and the Middle East. Social media campaigns, influencer partnerships, and digital advertising are also strengthening impulse purchasing and brand engagement among younger demographics.

Strong Seasonal and Festive Consumption Patterns

Seasonal celebrations and gifting traditions continue to generate recurring global demand for chocolate confectionery products. Occasions such as Christmas, Easter, Valentine’s Day, Halloween, Ramadan, Lunar New Year, and Diwali significantly boost sales volumes across retail and corporate gifting channels. Manufacturers increasingly launch region-specific festive collections, premium packaging formats, and limited-edition products to capitalize on seasonal purchasing behavior. Corporate gifting trends and travel retail expansion are additionally strengthening premium chocolate consumption globally.

Chocolate Confectionery Market Restraints

Volatility in Cocoa and Raw Material Prices

The chocolate confectionery industry remains highly vulnerable to fluctuations in cocoa prices, sugar costs, dairy prices, and packaging expenses. Cocoa production is heavily concentrated in West African nations such as Côte d’Ivoire and Ghana, making global supply chains susceptible to climate-related disruptions, crop disease outbreaks, geopolitical instability, and labor challenges. Rising raw material prices continue pressuring manufacturer margins and often force companies to adopt shrinkflation strategies, reformulate products, or implement retail price increases. Sustained cocoa price inflation may negatively impact affordability in price-sensitive emerging markets.

Rising Regulatory Pressure on Sugar Consumption

Governments and public health organizations worldwide are increasingly targeting high-sugar food categories through stricter labeling requirements, sugar taxes, and nutritional guidelines. Chocolate confectionery manufacturers face growing pressure to reduce sugar content while maintaining product taste, texture, and shelf stability. Health concerns related to obesity, diabetes, and excessive calorie consumption are encouraging some consumers to moderate confectionery intake, particularly in developed markets. Compliance with evolving food regulations and reformulation investments continues to increase operational complexity and R&D costs across the industry.

Chocolate Confectionery Industry Key Opportunities

Functional and Better-for-You Chocolate Products

The growing health and wellness industry presents substantial opportunities for chocolate confectionery manufacturers to expand into functional and better-for-you product categories. Consumers increasingly seek chocolate products offering nutritional value alongside indulgence, including protein-enriched bars, probiotic-infused chocolates, adaptogenic ingredients, and reduced-sugar formulations. Vegan and plant-based chocolate categories are also gaining strong traction globally as consumers prioritize sustainability and dietary flexibility. Functional chocolates targeted toward energy enhancement, mood improvement, stress reduction, and sports nutrition applications are expected to create high-margin niche opportunities for manufacturers over the forecast period.

Expansion Across Emerging Economies

Emerging markets across Asia-Pacific, Latin America, and the Middle East represent major untapped growth opportunities for global chocolate confectionery brands. Rising urbanization, increasing disposable incomes, westernized snacking habits, and expanding organized retail infrastructure are driving strong consumption growth in countries such as India, China, Indonesia, Vietnam, and Saudi Arabia. Manufacturers are increasingly localizing flavor profiles, introducing smaller affordable pack sizes, and expanding regional manufacturing capacity to penetrate middle-income consumer segments. Growing gifting culture and premium consumption trends across emerging economies are expected to significantly boost long-term market expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 151.20 Billion |

| Market Size in 2026 | USD 160.73 Billion |

| Market Size in 2031 | USD 218.15 Billion |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Chocolate bars continue to dominate the global chocolate confectionery market, accounting for nearly 34% of total market revenue in 2025. Their leadership position is supported by affordability, widespread retail availability, convenience, and strong impulse purchasing behavior. Filled chocolate bars, wafer-based bars, and nut-infused variants remain highly popular across both developed and emerging economies. Boxed chocolates and premium assortments are witnessing strong growth due to increasing gifting demand and seasonal purchases. Seasonal chocolates, including Easter eggs, Christmas assortments, and festive collections, generate substantial recurring revenues for leading manufacturers. Artisanal and gourmet chocolates are among the fastest-growing product categories as consumers increasingly seek premium sensory experiences and ethically sourced ingredients.

Chocolate Type Insights

Milk chocolate remains the leading segment within the chocolate confectionery market, representing approximately 48% of global demand in 2025 due to its broad consumer appeal and mass-market accessibility. However, dark chocolate is emerging as the fastest-growing category, supported by rising health consciousness and demand for higher cocoa content products. White chocolate maintains strong popularity in premium confectionery and bakery applications, while ruby chocolate and specialty cocoa formulations are gradually expanding within luxury product segments. Organic and vegan chocolate variants are also experiencing accelerated adoption as clean-label and plant-based consumption trends strengthen globally.

Distribution Channel Insights

Supermarkets and hypermarkets dominate chocolate confectionery distribution globally, accounting for nearly 41% of market revenue in 2025 due to extensive product assortment, promotional activities, and high consumer footfall. Convenience stores remain highly important for impulse chocolate purchases, particularly in urban markets. Specialty chocolate retailers and premium boutiques continue expanding in affluent regions, offering luxury gifting collections and artisanal experiences. E-commerce and direct-to-consumer channels are witnessing the fastest growth rates, driven by online gifting trends, subscription boxes, personalized assortments, and digital retail expansion. Social media marketing and influencer-driven campaigns are increasingly shaping online chocolate purchasing behavior among younger consumers.

Consumer Group Insights

Adult consumers account for the largest share of global chocolate confectionery consumption, driven by premium indulgence trends, gifting behavior, and rising interest in dark chocolate products. Teenagers and younger consumers remain major contributors to impulse purchasing and flavored chocolate innovation, particularly within countline and snack-size categories. Children continue driving demand for novelty chocolates, seasonal assortments, and cartoon-branded confectionery products. Geriatric consumers are increasingly adopting dark chocolate and reduced-sugar variants due to perceived wellness benefits and growing availability of health-oriented formulations.

Price Point Insights

Mid-range chocolate confectionery products account for the largest share of global market demand, representing nearly 44% of total revenue in 2025. These products balance affordability and quality while benefiting from mass-market retail penetration. Premium and super-premium chocolate segments are expanding significantly faster than economy products due to rising disposable income, gifting culture, and consumer willingness to pay for ethical sourcing, artisanal craftsmanship, and high cocoa percentages. Economy chocolate products continue maintaining strong demand across price-sensitive emerging markets, particularly through small-format packs and local retail channels.

Explore more data points, trends and opportunities Download Free Sample Report

Chocolate Confectionery Market Segmentations

By Product Type

- Chocolate Bars

- Countlines & Single-Serve Chocolates

- Boxed Chocolates

- Seasonal & Festive Chocolates

- Chocolate Pouches & Sharing Packs

- Compound Chocolate Confectionery

- Sugar-Free & Functional Chocolates

- Organic & Vegan Chocolates

- Artisanal & Gourmet Chocolates

By Chocolate Type

- Milk Chocolate

- Dark Chocolate

- White Chocolate

- Ruby Chocolate

- Compound Chocolate

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Stores

- Departmental Stores

- Online Retail/E-Commerce

- Direct-to-Consumer

- Foodservice & Institutional Sales

By Consumer Group

- Children

- Teenagers

- Adults

- Geriatric Consumers

By Price Point

- Economy

- Mid-Range

- Premium

- Super-Premium/Luxury

Regional Insights

Europe

Europe dominates the global chocolate confectionery market, accounting for approximately 39% of total global revenue in 2025. Germany, Switzerland, the U.K., France, Belgium, and Italy remain key consumption and manufacturing hubs due to strong chocolate traditions and high per-capita intake levels. Premium dark chocolate, artisanal products, and sustainably sourced cocoa-based confectionery are particularly popular across Western Europe. Switzerland continues leading premium chocolate exports globally, while Germany remains one of the largest manufacturing and processing centers within the industry.

North America

North America accounts for nearly 27% of global chocolate confectionery demand, led primarily by the United States. Strong seasonal purchasing behavior, premium gifting culture, and rising demand for organic and low-sugar chocolates are driving regional market growth. Consumers increasingly favor snack-size formats, dark chocolate products, and functional confectionery innovations. Canada also represents a significant premium chocolate market, while Mexico continues strengthening its role as both a manufacturing hub and growing consumer market.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market and is projected to expand at a CAGR exceeding 8% through 2031. China and India are emerging as major demand centers due to rising middle-class populations, urbanization, and westernized consumption habits. Premium gifting culture and e-commerce expansion are significantly accelerating chocolate demand across the region. Japan and South Korea remain highly innovation-driven markets characterized by premium seasonal launches and sophisticated packaging trends. Southeast Asian countries including Indonesia, Vietnam, and Thailand are also witnessing increasing chocolate penetration.

Latin America

Latin America represents a steadily expanding chocolate confectionery market led by Brazil, Argentina, and Chile. Brazil serves as both a major cocoa-producing nation and one of the region’s largest chocolate-consuming markets. Rising urbanization and affordable premiumization trends are supporting demand growth across the region. Manufacturers are increasingly introducing smaller pack formats and localized flavor variants to improve accessibility among middle-income consumers.

Middle East & Africa

The Middle East & Africa region is emerging as a high-potential growth market driven by luxury gifting culture, tourism expansion, and retail modernization. The UAE and Saudi Arabia are witnessing rising demand for premium imported chocolates, particularly during Ramadan and festive occasions. South Africa remains a major regional consumption hub, while cocoa-producing African countries are increasingly investing in domestic value-added chocolate manufacturing. Expanding organized retail infrastructure and premium gifting demand are expected to strengthen long-term regional growth.

Key Players in the Chocolate Confectionery Market

- Mars Incorporated

- Mondelez International

- Nestlé S.A.

- Ferrero Group

- The Hershey Company

- Lindt & Sprüngli

- Meiji Holdings Co., Ltd.

- Yildiz Holding

- Pladis Foods

- Lotte Wellfood

- Barry Callebaut

- August Storck KG

- Orion Corporation

- Ezaki Glico Co., Ltd.

- Ritter Sport