Chicken Wings Market Size

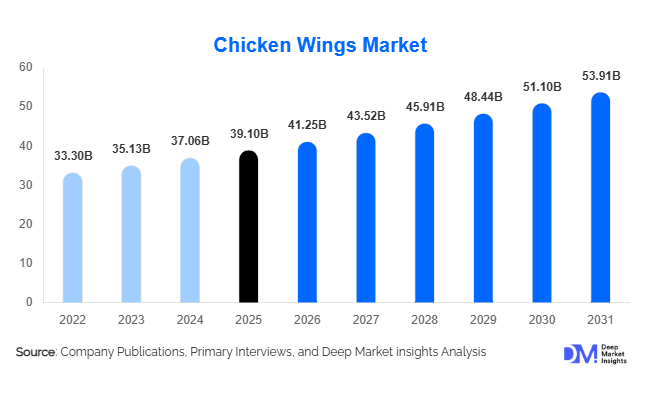

According to Deep Market Insights, the global chicken wings market size was valued at USD 39.1 billion in 2025 and is projected to grow from USD 41.25 billion in 2026 to reach USD 53.91 billion by 2031, expanding at a CAGR of 5.5% during the forecast period (2026–2031). The chicken wings market growth is primarily driven by increasing demand for protein-rich convenience foods, expansion of quick-service restaurant (QSR) chains, rising consumption of frozen and ready-to-cook poultry products, and continued menu innovation across foodservice establishments. The growing popularity of flavored wings, increasing penetration of food delivery platforms, and investments in poultry processing infrastructure are further supporting global market expansion.

Key Market Insights

- Foodservice remains the largest consumption channel, accounting for nearly 58% of global chicken wings demand, driven by restaurants, sports bars, pubs, and QSR chains.

- Frozen chicken wings dominate product demand, representing approximately 38% of the global market due to longer shelf life, efficient logistics, and retail penetration.

- North America leads the global market, supported by strong consumer preference for chicken wings and extensive restaurant networks.

- Asia-Pacific is the fastest-growing region, driven by urbanization, rising disposable income, and expansion of western-style dining concepts.

- Premium flavored and value-added chicken wings are experiencing strong growth as consumers seek differentiated taste experiences.

- Automation and advanced poultry processing technologies are improving production efficiency, yield optimization, and supply chain management across the industry.

Chicken Wings Market Latest Trends

Premium and International Flavor Innovation Accelerating Growth

Flavor innovation has become a major competitive differentiator within the chicken wings market. While traditional Buffalo and BBQ flavors continue to dominate global sales, manufacturers and restaurant operators are increasingly introducing international flavor profiles such as Korean spicy, Nashville hot, peri-peri, teriyaki, honey garlic, and Asian fusion variants. Premium flavored wings command higher margins and encourage repeat purchases, particularly among younger consumers seeking unique dining experiences. Limited-time offers and seasonal flavor launches are also becoming common strategies among major restaurant chains, contributing to increased consumer engagement and higher average order values.

Retail and E-Commerce Expansion Supporting Household Consumption

The retail segment is witnessing significant growth as consumers increasingly purchase frozen and ready-to-cook chicken wings for home consumption. Improvements in freezing technology, packaging solutions, and cold-chain logistics have enabled manufacturers to offer restaurant-quality products through supermarkets and online grocery platforms. Direct-to-consumer channels and online food retailing are creating additional growth opportunities, particularly in developed markets where convenience and at-home meal preparation continue to influence purchasing decisions. Retailers are also expanding premium and organic chicken wing offerings to cater to health-conscious consumers.

Chicken Wings Market Drivers

Expansion of Quick-Service Restaurants and Wing-Focused Chains

The global expansion of quick-service restaurants, sports bars, and wing-focused restaurant chains continues to drive substantial demand for chicken wings. Major restaurant operators are expanding into emerging markets while introducing innovative menu offerings that increase consumption frequency. Chicken wings remain one of the most profitable menu items for many foodservice establishments due to their popularity and versatility. Sporting events, social gatherings, and promotional campaigns further stimulate demand throughout the year, supporting steady market growth.

Growing Demand for High-Protein Convenience Foods

Consumers worldwide are increasingly prioritizing protein-rich foods as part of healthier lifestyles and active dietary habits. Chicken wings benefit from this trend by offering a convenient and flavorful source of animal protein. The growing popularity of snacking occasions, meal replacements, and shareable food formats has increased demand across both retail and foodservice channels. Younger demographics in particular are driving growth as they seek convenient, protein-based meal options that can be easily consumed at home or on-the-go.

Chicken Wings Market Restraints

Volatility in Poultry and Feed Costs

The chicken wings market remains highly sensitive to fluctuations in feed costs, particularly corn and soybean meal prices, which account for a significant portion of poultry production expenses. Rising energy, transportation, and labor costs further impact processor profitability. Since each chicken produces a limited number of wings, supply-demand imbalances can quickly lead to price volatility, affecting both manufacturers and foodservice operators.

Disease Outbreaks and Supply Chain Disruptions

Avian influenza outbreaks and other poultry diseases continue to pose risks to global supply chains. Production disruptions, trade restrictions, and biosecurity concerns can temporarily reduce supply availability and increase market prices. Export-oriented producers are particularly vulnerable to regulatory restrictions and disease-related trade barriers, creating challenges for maintaining consistent global supply.

Chicken Wings Industry Key Opportunities

Growth of Premium and Value-Added Products

Premium chicken wings represent one of the most attractive opportunities for market participants. Consumers increasingly seek restaurant-quality products featuring unique seasonings, marinades, smoking techniques, and gourmet flavor combinations. Premium wings often generate significantly higher margins compared to standard frozen products. Manufacturers investing in product innovation and flavor development can differentiate themselves in an increasingly competitive market while expanding revenue per unit sold.

Rapid Expansion Across Asia-Pacific Markets

Asia-Pacific presents substantial long-term growth opportunities due to rising poultry consumption, growing disposable incomes, and expanding foodservice infrastructure. Countries such as China, India, Indonesia, Vietnam, and the Philippines are witnessing strong demand growth as western-style dining concepts become more popular. Localized flavor development and investments in regional processing capacity can help companies capture emerging demand and establish long-term market positions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 39.10 Billion |

| Market Size in 2026 | USD 41.25 Billion |

| Market Size in 2031 | USD 53.91 Billion |

| CAGR | 5.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

Frozen chicken wings remain the leading product form segment, accounting for approximately 38% of global market revenue in 2025. Their dominance is supported by extended shelf life, lower product wastage, ease of storage, and efficient transportation across domestic and international supply chains. Frozen products are extensively utilized by quick-service restaurants, casual dining establishments, sports bars, institutional foodservice operators, and retail consumers due to their consistent quality and year-round availability. The expansion of cold-chain logistics networks and advancements in freezing technologies have further strengthened the position of frozen chicken wings across both developed and emerging markets.Value-added product categories, including marinated, seasoned, breaded, and fully cooked chicken wings, are among the fastest-growing segments within the market. The growth of these categories is primarily driven by rising demand for convenience-oriented food products, changing consumer lifestyles, and increasing preference for ready-to-cook and ready-to-eat meal solutions. Manufacturers are actively expanding processing capabilities and introducing innovative flavor profiles to differentiate products and capture premium pricing opportunities. The growing popularity of air fryers, meal kits, and home-delivered food products is further accelerating demand for processed and convenience-focused chicken wing offerings. As consumers increasingly prioritize convenience without compromising taste, value-added chicken wing products are expected to experience sustained growth throughout the forecast period.

Wing Type Insights

Traditional bone-in wings continue to dominate the global chicken wings market, accounting for approximately 61% of total market revenue. Their leadership position is largely attributed to consumer preference for authentic wing consumption experiences, superior flavor retention, and long-standing popularity across restaurants, sports bars, and social dining occasions. Drumettes and wingettes remain staple menu items across foodservice establishments, particularly in North America, where chicken wings have become deeply embedded in sports-viewing culture and casual dining habits.Boneless wings represent the fastest-growing wing type category and are gaining widespread acceptance among younger consumers, families, and convenience-oriented buyers. The primary growth driver for the boneless segment is ease of consumption, as consumers increasingly seek portable, mess-free, and easy-to-share food options. Foodservice operators are also expanding boneless wing offerings due to operational efficiencies, broader customer appeal, and opportunities for menu innovation through diverse sauces and flavor combinations. Growing demand for delivery-friendly food products and increasing participation in digital food ordering platforms are expected to further accelerate growth within the boneless wing segment over the coming years.

Distribution Channel Insights

Foodservice remains the largest distribution channel for chicken wings, accounting for nearly 58% of global consumption. The segment's leadership is primarily driven by the widespread popularity of chicken wings across quick-service restaurants, casual dining chains, sports bars, pubs, entertainment venues, and catering operations. Chicken wings have become a staple menu item due to their versatility, strong profit margins, and ability to attract consumers during sporting events, social gatherings, and promotional campaigns.Retail distribution channels, including supermarkets, hypermarkets, convenience stores, specialty meat retailers, and online grocery platforms, continue to gain market share as consumers increasingly prepare chicken wings at home. Growth in the retail segment is being supported by greater availability of frozen, marinated, and ready-to-cook products, along with rising consumer interest in home entertaining and quick meal preparation. E-commerce has emerged as an increasingly important channel, allowing manufacturers to directly engage consumers while offering broader product variety and premium selections. The growing adoption of subscription meal kits and direct-to-consumer sales models is expected to create additional opportunities for market participants seeking to diversify distribution strategies and improve customer engagement.

End-Use Insights

Restaurants represent the largest end-use segment, accounting for approximately 44% of global chicken wing demand. The segment benefits from the widespread popularity of wing-focused restaurant chains, sports bars, casual dining establishments, and quick-service restaurants where chicken wings serve as a core menu offering. Consistent consumer demand for shareable appetizers, game-day foods, and flavored protein snacks continues to support high consumption volumes across the restaurant industry.Hotels, pubs, catering providers, educational institutions, healthcare facilities, and corporate foodservice operators also contribute significantly to market demand. Household consumption is emerging as one of the fastest-growing end-use categories due to increasing availability of frozen and ready-to-cook products through retail channels. Consumers are increasingly replicating restaurant-style experiences at home, supported by growing ownership of air fryers and home cooking appliances. The food processing industry is also expanding utilization of chicken wings in prepared meals, snack products, and value-added convenience foods. Additionally, recovery in global tourism and air travel is contributing to rising demand from airline catering and travel-related foodservice applications.

Pricing Tier Insights

Mid-priced chicken wings account for the largest share of global sales, reflecting a balance between affordability, quality, and accessibility across both retail and foodservice channels. This segment appeals to a broad consumer base and remains the preferred choice among restaurants, supermarkets, and mass-market foodservice operators. The leading driver for the mid-priced segment is growing consumer demand for value-oriented protein products that offer quality without significant price premiums.Premium and gourmet chicken wings are among the fastest-growing pricing categories, driven by ongoing premiumization trends across the global food industry. Consumers are increasingly willing to pay higher prices for organic products, specialty marinades, clean-label ingredients, unique flavor profiles, and restaurant-quality eating experiences. Artisanal and specialty offerings featuring regional seasonings, premium ingredients, and sustainable sourcing claims are gaining visibility across retail shelves and foodservice menus. As disposable incomes continue to rise and consumer preferences shift toward higher-quality food experiences, premium products are expected to contribute disproportionately to value growth within the market.

Explore more data points, trends and opportunities Download Free Sample Report

Chicken Wings Market Segmentations

By Product Form

- Fresh Chicken Wings

- Chilled Chicken Wings

- Frozen Chicken Wings

- Marinated Chicken Wings

- Breaded/Battered Chicken Wings

- Fully Cooked Chicken Wings

- Ready-to-Cook Chicken Wings

- Ready-to-Eat Chicken Wings

By Wing Type

- Traditional Bone-In Wings

- Wingettes (Flats)

- Drumettes

- Boneless Wings

By Flavor Profile

- Buffalo

- Barbecue (BBQ)

- Spicy/Hot

- Honey-Based

- Garlic-Based

- Teriyaki

- Lemon Pepper

- Asian-Inspired Flavors

- Dry Rub Flavors

- Unseasoned/Plain

By Distribution Channel

- Quick Service Restaurants (QSRs)

- Casual Dining Restaurants

- Sports Bars & Pubs

- Cloud Kitchens

- Catering Services

- Hotels & Resorts

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Meat Stores

- Online Grocery Platforms

By End Use

- Restaurants

- Hotels

- Bars & Pubs

- Catering Companies

- Institutional Foodservice

- Household Consumption

- Food Processing Industry

- Airline & Travel Catering

Regional Insights

North America

North America remains the largest regional market, accounting for approximately 39% of global chicken wing demand in 2025. The United States alone contributes nearly 34% of worldwide consumption, supported by a strong cultural affinity for chicken wings, extensive restaurant penetration, and year-round demand associated with sporting events, social gatherings, and entertainment occasions. Canada continues to contribute stable growth through expanding retail and foodservice sales, while Mexico is witnessing increasing adoption of western-style dining concepts and poultry-based convenience foods.Regional market growth is primarily driven by the widespread popularity of sports-viewing culture, the strong presence of wing-focused restaurant chains, increasing food delivery penetration, and continuous menu innovation across the foodservice sector. Advanced poultry production capabilities, highly efficient processing infrastructure, sophisticated cold-chain networks, and high consumer spending on dining and convenience foods further strengthen North America's leadership position within the global market.

Europe

Europe accounts for approximately 18% of global market demand, with major consumption concentrated in the United Kingdom, Germany, France, Spain, Italy, and Poland. The market benefits from increasing popularity of casual dining formats, growing consumption during sporting and social occasions, and rising demand for frozen convenience foods. Retailers continue to expand product assortments, while foodservice operators increasingly incorporate flavored and premium chicken wing offerings into menus.The primary drivers supporting regional growth include rising demand for convenience-oriented meal solutions, increasing penetration of international quick-service restaurant brands, and growing consumer interest in premium poultry products. Additionally, expanding e-commerce grocery platforms, innovation in ready-to-cook products, and growing preference for high-quality protein sources continue to support market expansion. Sustainability initiatives, animal welfare standards, and demand for traceable poultry products are also influencing purchasing behavior and encouraging premium product adoption across the region.

Asia-Pacific

Asia-Pacific accounts for nearly 29% of global demand and represents the fastest-growing regional market. China remains the largest market within the region, supported by rapid urbanization, rising disposable incomes, expanding middle-class populations, and increasing foodservice penetration. India is emerging as one of the fastest-growing markets globally due to rapid quick-service restaurant expansion, growing acceptance of western-style foods, and rising poultry consumption. Japan and South Korea continue to demonstrate strong demand for premium and flavored chicken wing products, while Southeast Asian countries including Indonesia, Vietnam, Thailand, and the Philippines benefit from expanding modern retail networks and digital food delivery ecosystems.The region's growth is primarily driven by rising urbanization, increasing disposable incomes, expanding organized foodservice industries, and changing dietary preferences toward protein-rich foods. Rapid growth in online food delivery platforms, increasing youth populations, and continuous investment in cold-chain infrastructure are further accelerating market development. The expansion of international restaurant chains and growing demand for convenient ready-to-cook products are expected to sustain strong regional growth throughout the forecast period.

Latin America

Latin America represents approximately 9% of global market demand, led by Brazil, Mexico, and Argentina. Brazil serves as both a major poultry producer and consumer, benefiting from a highly developed poultry industry, abundant feed availability, and strong export competitiveness. Regional consumption continues to rise as poultry remains one of the most affordable and accessible protein sources for consumers.Market growth across Latin America is being driven by increasing urbanization, rising consumption of affordable animal proteins, expanding quick-service restaurant networks, and improving retail distribution infrastructure. Growing middle-class populations and increasing demand for convenient food products are supporting higher consumption levels across both retail and foodservice channels. Additionally, investments in poultry production capacity and processing technologies are enhancing product availability and supporting long-term market expansion.

Middle East & Africa

The Middle East & Africa region accounts for approximately 5% of global market demand. Saudi Arabia and the United Arab Emirates represent the largest import-driven markets, supported by tourism growth, hospitality sector expansion, and rising consumption of western-style food products. South Africa remains an important regional market due to its relatively developed foodservice industry and growing retail penetration.Regional growth is primarily supported by expanding tourism activity, rising disposable incomes, increasing urbanization, and growing demand for convenience foods among younger consumers. Investments in cold-chain infrastructure, food processing facilities, modern retail development, and foodservice expansion are improving product accessibility across several markets. The increasing presence of international restaurant chains and growing popularity of western dining formats are expected to create additional growth opportunities for chicken wing suppliers throughout the region.

Key Players in the Chicken Wings Market

- Tyson Foods

- JBS S.A.

- BRF S.A.

- Cargill Incorporated

- Charoen Pokphand Foods (CP Foods)

- Perdue Farms

- Koch Foods

- Wayne-Sanderson Farms

- Mountaire Farms

- Plukon Food Group

- Industrias Bachoco

- Wens Foodstuff Group

- New Hope Liuhe

- Fujian Sunner Development

- Suguna Foods