Global Canned Pears Market Size

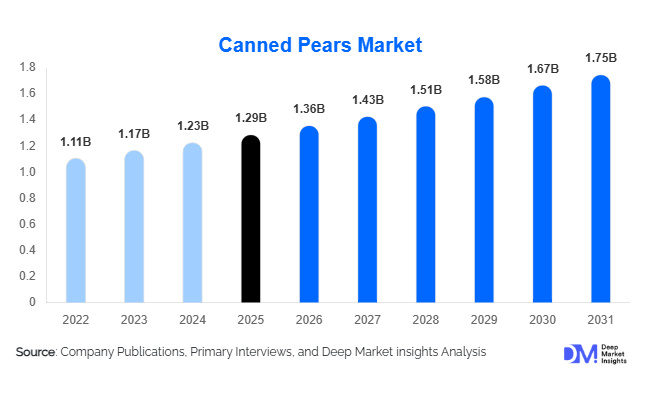

According to Deep Market Insights, the global canned pears market size was valued at USD 1.29 billion in 2025 and is projected to grow from USD 1.36 billion in 2026 to reach USD 1.75 billion by 2031, expanding at a CAGR of 5.2% during the forecast period (2026–2031). Market growth is being supported by rising demand for convenient and shelf-stable fruit products, increasing utilization of canned fruits in food processing applications, and growing consumer preference for affordable fruit options with extended shelf life. The market is also benefiting from the expansion of organized retail channels, increasing demand for no-added-sugar fruit products, and ongoing innovations in sustainable packaging and premium fruit preservation technologies.

Key Market Insights

- Pear halves remain the leading product form, accounting for approximately 34% of global canned pears demand due to their versatility across retail and foodservice applications.

- Light syrup-packed pears dominate packing formats, representing nearly 38% of the market as consumers shift toward lower-sugar fruit preservation options.

- North America leads the global market, accounting for approximately 31% of worldwide revenue owing to high canned fruit consumption and established retail distribution networks.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization, modern retail expansion, and rising processed food consumption across China, India, and Southeast Asia.

- Food processing applications are expanding rapidly, particularly in bakery, dairy, dessert, and ready-to-eat meal manufacturing industries.

- Organic, clean-label, and no-added-sugar canned pears are emerging as premium growth segments, supported by evolving consumer health preferences.

Global Canned Pears Market Latest Trends

Growing Demand for Clean-Label and Reduced-Sugar Products

Consumer awareness regarding sugar intake and food ingredient transparency is reshaping the canned pears industry. Manufacturers are increasingly introducing products packed in natural fruit juice, water, and extra-light syrup formulations to appeal to health-conscious consumers. Organic-certified and non-GMO canned pears are gaining traction across North America and Europe, where retailers are expanding shelf space for clean-label products. Brands are also reducing preservatives and artificial additives while highlighting fruit origin and sustainability credentials on packaging. These developments are allowing producers to command premium pricing while strengthening brand differentiation in mature markets.

Sustainable Packaging and Processing Innovations

Sustainability has become a major focus area across the canned fruit industry. Manufacturers are investing in recyclable metal cans, BPA-free packaging materials, lightweight containers, and energy-efficient production systems. Advanced sterilization and preservation technologies are helping processors maintain fruit texture, flavor, and nutritional value while reducing waste and operational costs. Automated grading systems, AI-powered quality inspection technologies, and digital traceability platforms are increasingly being deployed to improve production efficiency and strengthen consumer trust. Sustainability-focused investments are expected to remain a defining trend throughout the forecast period.

Global Canned Pears Market Drivers

Rising Demand for Convenient and Shelf-Stable Food Products

Busy lifestyles and increasing demand for convenience foods continue to drive canned pears consumption globally. Canned pears provide year-round availability, extended shelf life, affordability, and reduced food waste compared with fresh fruits. Consumers increasingly value ready-to-eat fruit products that can be easily incorporated into meals, snacks, desserts, and breakfast preparations. This convenience factor is particularly important in urban markets where food storage efficiency and accessibility influence purchasing decisions.

Expansion of Foodservice and Industrial Food Processing Sectors

The growing use of canned pears by restaurants, hotels, catering providers, bakeries, dairy manufacturers, and ready-meal producers is significantly supporting market growth. Food processors benefit from the consistency, availability, and stable pricing of canned fruit ingredients compared with fresh alternatives. Bakery fillings, yogurt preparations, fruit desserts, smoothies, and fruit-based snacks increasingly incorporate canned pears, creating substantial demand from industrial customers worldwide.

Global Canned Pears Market Restraints

Competition from Fresh and Frozen Fruit Alternatives

Despite their convenience, canned pears face increasing competition from fresh, frozen, and minimally processed fruit products. Many consumers continue to perceive fresh fruit as healthier and more natural than canned alternatives, particularly among younger demographics focused on clean eating and minimally processed foods. This perception creates ongoing challenges for manufacturers seeking to expand penetration in health-conscious consumer segments.

Raw Material Supply and Agricultural Volatility

Pear production is highly dependent on climatic conditions, water availability, labor resources, and orchard productivity. Weather-related disruptions, pest outbreaks, and fluctuations in harvest yields can significantly affect raw material availability and pricing. Such volatility impacts processor margins and creates supply chain uncertainties, particularly for companies dependent on specific pear-growing regions for sourcing.

Global Canned Pears Industry Key Opportunities

Expansion into Emerging Asian Markets

Asia-Pacific presents substantial untapped growth potential for canned pear manufacturers. Rising disposable incomes, urbanization, changing dietary patterns, and expansion of organized retail networks are increasing consumer exposure to shelf-stable fruit products. Countries such as India, Indonesia, Vietnam, Thailand, and the Philippines remain significantly underpenetrated compared with North American and European markets. Companies investing in localized distribution, marketing, and product customization can capitalize on long-term demand growth opportunities throughout the region.

Industrial Ingredient Applications Across Processed Foods

The growing global processed food industry offers significant opportunities for canned pear suppliers. Food manufacturers increasingly utilize canned pears as ingredients in bakery fillings, fruit desserts, dairy products, fruit preparations, confectionery products, and ready-to-eat meals. Industrial customers value the consistency, quality control, and year-round availability of canned fruit ingredients. Strategic partnerships with food manufacturers can help producers diversify beyond traditional retail channels while generating stable long-term demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.29 Billion |

| Market Size in 2026 | USD 1.36 Billion |

| Market Size in 2031 | USD 1.75 Billion |

| CAGR | 5.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

Pear halves continue to dominate the global canned pears market, contributing approximately 34% of total revenue in 2025. This leadership is primarily driven by their strong consumer acceptance, visually appealing presentation, and high versatility across both household consumption and foodservice applications. Their structural integrity after processing makes them particularly suitable for desserts, fruit cocktails, and ready-to-serve retail formats, which has reinforced their position as the preferred product form across mainstream retail channels. Demand is further supported by manufacturers prioritizing standardized sizing and consistent quality, which enhances operational efficiency in large-scale canning operations.Pear slices represent a highly significant secondary segment, benefiting from widespread usage in bakery fillings, desserts, salads, and institutional catering programs where ease of portioning and uniform distribution are essential. The segment’s growth is strongly supported by the expanding bakery and confectionery industries, where canned fruit is increasingly used as a cost-efficient and stable ingredient that maintains flavor consistency throughout the year. Diced and cubed pears are emerging as a high-growth sub-segment, primarily driven by industrial food processors and manufacturers of yogurt, dairy mixes, and ready-to-eat meals, where smaller cut formats enable easier integration and product innovation. Whole canned pears maintain a niche but stable demand in premium retail categories, where visual appeal and luxury positioning influence purchasing decisions. Crushed and industrial-grade pear formats are primarily driven by large-scale food manufacturing, where the key growth driver is cost optimization and functional usage in fillings, purees, and blended fruit preparations.

Pear Variety Insights

Bartlett and Williams pears lead the global canned pears market, accounting for approximately 42% of total production. Their dominance is strongly supported by superior sweetness levels, excellent texture retention during thermal processing, and high juice content, which collectively ensure consistent product quality across industrial canning applications. The leading segment driver for Bartlett/Williams varieties is their processing efficiency and ability to maintain flavor integrity after sterilization, making them the most economically viable option for large-scale manufacturers.Anjou and Bosc pears hold a substantial share in premium product categories, where demand is driven by their firmer texture, longer shelf stability, and suitability for specialty retail and gourmet food applications. Their adoption is increasingly supported by the premiumization trend in developed markets, where consumers are willing to pay higher prices for differentiated fruit varieties. Asian pear varieties are experiencing rising traction in the Asia-Pacific region, driven by strong cultural familiarity, preference for crisp texture profiles, and integration into regional dessert and snack formulations. This diversification of pear varieties is further supported by manufacturers’ strategic focus on product differentiation and expansion into value-added fruit offerings.

Packing Medium Insights

Light syrup remains the leading packing medium, representing nearly 38% of global market revenue. Its dominance is driven by its ability to balance sweetness with reduced sugar intensity, aligning with evolving consumer preferences for moderately healthier indulgent food products. The key driver supporting this segment is the rising demand for better-for-you canned fruit options that maintain traditional taste profiles while reducing overall sugar consumption.Heavy syrup continues to serve legacy consumer segments, particularly in traditional retail markets and dessert-oriented applications; however, its share is gradually declining due to growing health consciousness. In contrast, pears packed in natural fruit juice are witnessing strong growth momentum, driven by clean-label trends and increasing demand for minimally processed food products. Water-packed and no-added-sugar variants are also expanding rapidly, supported by calorie-conscious consumers, institutional buyers, and foodservice operators seeking healthier ingredient alternatives. The overarching driver across all emerging packing mediums is the global shift toward health-oriented consumption and transparency in food labeling.

Distribution Channel Insights

Supermarkets and hypermarkets dominate global canned pear distribution, accounting for approximately 45% of total sales. Their leadership is driven by strong product visibility, extensive assortment availability, and aggressive promotional strategies that influence impulse purchasing behavior. The key growth driver in this channel is organized retail expansion, particularly in emerging economies where modern trade infrastructure continues to replace traditional retail formats.Grocery stores and discount retailers continue to maintain a strong presence, especially in price-sensitive markets where affordability remains a critical purchasing factor. Online retail is emerging as one of the fastest-growing distribution channels, driven by rapid digitalization, increasing penetration of e-commerce grocery platforms, and consumer preference for home delivery convenience. The growth of online grocery ecosystems and subscription-based food delivery models is further accelerating this shift. Foodservice distributors play a vital role in supplying bulk quantities to restaurants, hotels, educational institutions, and catering services, with demand driven by the recovery and expansion of the global hospitality sector and increasing reliance on standardized, shelf-stable ingredients.

End-Use Insights

Household consumption remains the dominant end-use segment, accounting for approximately 58% of global demand. The leading driver of this segment is the rising preference for convenient, ready-to-eat fruit options that require minimal preparation while offering consistent taste and year-round availability. Canned pears are widely used in home baking, desserts, snacks, breakfast meals, and fruit salads, reinforcing their position as a staple pantry product.Foodservice applications represent a growing end-use segment, supported by expanding hospitality infrastructure and the increasing use of standardized ingredients that reduce preparation time and ensure consistency across large-scale operations. Industrial food processing is emerging as one of the fastest-growing segments, driven by rising demand from bakery manufacturers, dairy processors, and ready-meal producers, where canned pears serve as functional ingredients in fillings, toppings, and blended formulations. Beverage applications are also expanding steadily, particularly in smoothies and fruit-based drinks, where demand is fueled by health and wellness trends and increasing consumption of natural fruit ingredients in functional beverages.

Explore more data points, trends and opportunities Download Free Sample Report

Canned Pears Market Segmentations

By Product Form

- Pear Halves

- Pear Slices

- Diced / Cubed Pears

- Whole Pears

- Crushed Pears

- Industrial Fruit Pieces

By Pear Variety

- Bartlett / Williams Pears

- Anjou Pears

- Bosc Pears

- Asian / Snow Pears

- Mixed Pear Varieties

By Packing Medium

- Light Syrup

- Heavy Syrup

- Extra Light Syrup

- Natural Fruit Juice

- No-Added-Sugar / Water Packed

By Packaging Type

- Metal Cans

- Glass Jars

- Retort Pouches

- Bulk Foodservice Containers

By Distribution Channel

- Supermarkets & Hypermarkets

- Grocery & Convenience Stores

- Online Retail / E-commerce

- Foodservice Distributors

- Specialty Food Stores

Regional Insights

North America

North America accounted for approximately 31% of the global canned pears market in 2025, making it the leading regional market. The United States alone contributes nearly 24% of global demand, driven by strong consumption of packaged fruit products, well-established retail infrastructure, and significant foodservice penetration. The primary growth driver in the region is the increasing shift toward convenient, shelf-stable, and health-positioned food products, particularly those with no-added-sugar or organic positioning. Canada also supports regional demand through steady retail and institutional consumption, with growing emphasis on premium and health-oriented canned fruit offerings.

Europe

Europe represented approximately 28% of global market revenue in 2025, with strong contributions from Germany, France, the United Kingdom, Italy, Spain, and the Netherlands. Regional growth is primarily driven by the extensive use of canned fruits in bakery, dessert, and institutional foodservice applications, where consistency and year-round availability are essential. A major growth driver across Europe is the increasing consumer shift toward organic, sustainably sourced, and environmentally friendly packaging solutions, particularly in Western European countries where sustainability strongly influences purchasing decisions. This has encouraged manufacturers to innovate in clean-label formulations and eco-friendly packaging formats.

Asia-Pacific

Asia-Pacific accounted for approximately 26% of global demand and is recognized as the fastest-growing regional market. China leads regional consumption and production, supported by strong domestic fruit processing capacity and rising urban consumption of packaged foods. The primary growth driver in the region is rapid urbanization combined with expanding modern retail infrastructure, which is increasing accessibility to processed and convenience food products. India represents the fastest-growing national market, driven by rising disposable incomes, evolving dietary habits, and rapid expansion of organized retail. Additional contributions from Japan, South Korea, Indonesia, Vietnam, and Thailand are supported by strong food manufacturing industries and increasing adoption of Western-style desserts and convenience foods.

Latin America

Latin America accounted for approximately 8% of global demand in 2025. Brazil and Mexico lead regional consumption, supported by increasing penetration of supermarkets and growing consumer acceptance of packaged and processed fruit products. The key driver in this region is the expansion of modern retail infrastructure combined with the growth of the processed food industry, which is increasing demand for stable, cost-effective fruit ingredients. Rising urbanization and improving distribution networks are further strengthening market accessibility across secondary cities and semi-urban areas.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7% of global market revenue. Key markets include the United Arab Emirates, Saudi Arabia, South Africa, Egypt, and Qatar. Growth is primarily driven by rising food import dependency, expanding hospitality and tourism sectors, and increasing demand for long shelf-life food products suitable for arid climates. The hospitality industry, particularly in Gulf Cooperation Council countries, is a major demand driver, supported by large-scale tourism development and high reliance on imported processed food products. Additionally, improving retail infrastructure and rising expatriate populations are further contributing to sustained market expansion across the region.

Key Players in the Global Canned Pears Market

- Del Monte Foods

- Dole Food Company

- Seneca Foods Corporation

- Rhodes Food Group

- Kraft Heinz

- Princes Group

- CHB Group

- Pacific Coast Producers

- Golden Circle

- Conserve Italia

- Ardo Foods

- Tropical Food Industries

- Gulong Food

- Delicia Foods India

- Shandong Wanlilai Food