Canned Food Market Size

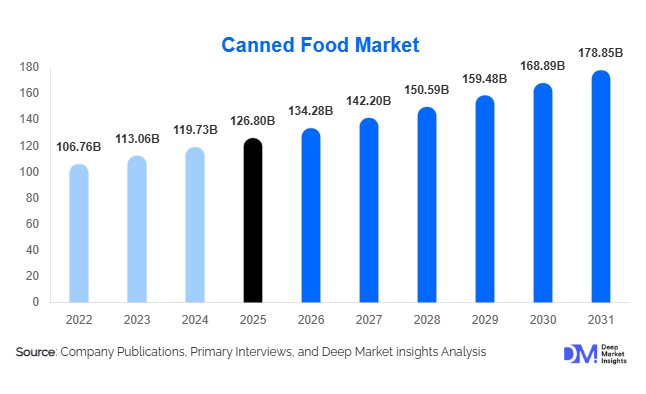

According to Deep Market Insights, the global canned food market size was valued at USD 126.8 billion in 2025 and is projected to grow from USD 134.28 billion in 2026 to reach USD 178.85 billion by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The canned food market growth is primarily driven by increasing demand for convenient and shelf-stable food products, rising urbanization, expanding organized retail penetration, and growing consumer preference for ready-to-eat and easy-to-store meal solutions. Technological advancements in food preservation, sustainable packaging innovations, and rising demand for premium canned seafood and organic canned vegetables are further supporting market expansion globally.

Key Market Insights

- Canned vegetables remain the dominant product category, accounting for nearly 26% of the global canned food market due to broad household consumption and extensive foodservice applications.

- Asia-Pacific is the fastest-growing regional market, driven by urbanization, expanding middle-class populations, and rising adoption of packaged convenience foods across China, India, Indonesia, and Vietnam.

- Metal cans continue to dominate packaging demand, holding nearly 78% market share globally owing to durability, recyclability, and extended shelf-life performance.

- Premium and clean-label canned foods are gaining strong traction, particularly in North America and Europe where consumers increasingly prioritize organic, BPA-free, and low-sodium food products.

- Online grocery retail channels are rapidly expanding, enabling canned food manufacturers to penetrate emerging urban and semi-urban consumer markets more effectively.

- Technological adoption across manufacturing facilities, including AI-based quality inspection systems, automated filling lines, and smart packaging technologies, is improving operational efficiency and sustainability compliance.

Canned Food Market Latest Trends

Growing Demand for Premium and Clean-Label Canned Foods

Consumer preferences are shifting toward healthier and premium canned food offerings, creating strong momentum for clean-label product innovation. Manufacturers are increasingly launching organic canned vegetables, preservative-free soups, low-sodium ready meals, and sustainably sourced seafood products to cater to evolving dietary preferences. BPA-free packaging and recyclable aluminum cans are becoming standard across premium product categories as environmental awareness and food safety concerns intensify globally. Consumers are also demanding greater transparency in ingredient sourcing, nutritional labeling, and sustainability certifications, encouraging brands to strengthen traceability systems and ethical sourcing practices. Premium canned seafood products such as tuna, salmon, and sardines are witnessing particularly strong growth due to rising protein consumption trends and increasing awareness regarding omega-3 nutritional benefits.

E-Commerce and Digital Grocery Expansion Reshaping Distribution

The rapid expansion of online grocery retail platforms is transforming canned food distribution globally. Shelf-stable canned foods are highly compatible with e-commerce logistics due to lower spoilage risks and ease of transportation compared to fresh or frozen products. Major retailers and packaged food companies are strengthening direct-to-consumer strategies, subscription-based meal delivery models, and digital promotional campaigns to capture growing online demand. Emerging economies such as India, Indonesia, Brazil, and Mexico are witnessing rapid growth in grocery delivery adoption, creating new opportunities for canned food manufacturers to penetrate underserved urban and semi-urban markets. AI-driven inventory management systems, smart warehousing technologies, and predictive consumer analytics are further improving supply chain efficiency and product availability across digital retail ecosystems.

Canned Food Market Drivers

Rising Demand for Convenience and Shelf-Stable Foods

Rapid urbanization, changing lifestyles, and increasing workforce participation are significantly driving global demand for convenient packaged food products. Consumers increasingly seek ready-to-eat and easy-to-store foods that require minimal preparation while maintaining nutritional stability. Canned foods offer long shelf life, affordability, and reduced food waste, making them attractive across both developed and emerging economies. Working professionals, students, and dual-income households particularly contribute to growing consumption of canned soups, vegetables, seafood, and ready meals. The rising popularity of quick meal preparation and pantry stocking behavior continues to strengthen long-term market demand globally.

Growing Focus on Food Security and Emergency Preparedness

Governments, humanitarian organizations, and households are increasingly investing in shelf-stable food inventories to improve resilience against geopolitical disruptions, natural disasters, pandemics, and supply chain instability. Canned foods are widely utilized in emergency preparedness systems due to their durability, long shelf life, and logistical efficiency. Military procurement programs, disaster relief agencies, and institutional food reserve programs are driving substantial demand for canned meat, seafood, vegetables, and ready meals globally. Climate-related uncertainties and inflationary pressures are further encouraging consumers to maintain larger inventories of packaged food products.

Global Market Restraints

Health Concerns Related to Processed Foods

Despite growing demand, consumer concerns regarding sodium content, preservatives, and processed food consumption continue to challenge the canned food market. Health-conscious consumers increasingly prefer fresh and minimally processed food alternatives, particularly in developed economies. Regulatory scrutiny surrounding additives, preservatives, and packaging chemicals such as BPA is intensifying globally, forcing manufacturers to invest heavily in reformulation, clean-label innovation, and sustainable packaging upgrades. Failure to address changing nutritional expectations may limit market penetration among younger health-focused consumers.

Raw Material and Packaging Cost Volatility

Fluctuations in agricultural commodities, seafood supply, steel, aluminum, and transportation costs create substantial operational challenges for canned food manufacturers. Rising metal packaging costs directly impact production margins, particularly for smaller regional players with limited procurement scale advantages. Supply chain disruptions and energy price volatility further increase manufacturing and logistics expenses. Maintaining competitive pricing while preserving profitability remains a key challenge within highly price-sensitive mass-market product categories such as canned vegetables and soups.

Canned Food Industry Key Opportunities

Expansion of Premium Seafood and Functional Nutrition Products

The growing global demand for protein-rich and functional nutrition products presents substantial opportunities for canned food manufacturers. Premium canned tuna, salmon, sardines, and fortified ready meals are gaining popularity among health-conscious consumers seeking convenient nutritional solutions. Functional canned foods enriched with vitamins, minerals, plant proteins, and omega-3 ingredients are expected to gain strong traction over the forecast period. Manufacturers investing in premiumization strategies, gourmet meal offerings, and organic seafood sourcing are likely to achieve higher profit margins and stronger brand differentiation globally.

Emerging Market Retail Expansion

Rapid retail modernization and grocery infrastructure development across emerging economies are creating significant growth opportunities for canned food companies. Expanding supermarket chains, convenience stores, and online grocery platforms across Asia-Pacific, Latin America, and the Middle East are improving accessibility to packaged food products. Countries such as India, Vietnam, Indonesia, and Saudi Arabia are witnessing rising demand for affordable and shelf-stable meal solutions due to urban population growth and evolving consumer lifestyles. Manufacturers entering these high-growth markets through localized product portfolios and regional production facilities are expected to benefit from strong long-term volume expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 126.80 Billion |

| Market Size in 2026 | USD 134.28 Billion |

| Market Size in 2031 | USD 178.85 Billion |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Canned vegetables dominate the global canned food market, accounting for nearly 26% of total market revenue in 2025. Tomatoes, sweet corn, peas, and mixed vegetables remain highly consumed across households and foodservice industries due to affordability and broad culinary applications. Canned seafood represents one of the fastest-growing product categories, led by strong global demand for tuna and salmon products driven by rising protein consumption trends and health awareness. Ready meals, soups, and ethnic canned foods are witnessing increasing adoption among urban consumers seeking convenience and time-saving meal solutions. Premium canned dairy desserts and organic canned fruit products are also gaining popularity in developed economies where clean-label and natural ingredient preferences continue to strengthen. Canned pet food is emerging as a high-growth niche category due to rising pet ownership and increasing expenditure on premium animal nutrition products.

Packaging Type Insights

Metal cans remain the dominant packaging format within the canned food industry, accounting for approximately 78% of global packaging demand in 2025. Aluminum cans are increasingly preferred due to lightweight properties, high recyclability, corrosion resistance, and transportation efficiency. Easy-open pull-tab packaging solutions are gaining popularity among consumers due to enhanced convenience and accessibility. BPA-free can linings are becoming increasingly important across premium product categories as manufacturers respond to tightening food safety regulations and consumer concerns regarding chemical exposure. Sustainable packaging innovations including lightweight containers, recyclable materials, and low-carbon manufacturing technologies are becoming critical competitive differentiators globally.

Distribution Channel Insights

Supermarkets and hypermarkets dominate canned food distribution globally, contributing nearly 46% of total market revenue in 2025. Large retail chains offer broad product visibility, promotional pricing strategies, and extensive shelf space allocation for packaged food brands. Convenience stores continue to play an important role in urban markets where on-the-go purchasing behavior remains strong. Online grocery retail is emerging as the fastest-growing distribution channel, expanding at more than 8% CAGR due to rapid adoption of digital grocery shopping and home delivery services. Foodservice distribution channels are also witnessing rising demand from restaurants, institutional catering providers, hotels, and airline catering operators that increasingly rely on canned ingredients for operational consistency and reduced spoilage risk.

End-Use Insights

Household consumers account for the largest share of the canned food market, representing approximately 63% of global consumption in 2025. Retail demand remains strong due to convenience, affordability, and long-term storage benefits. Foodservice establishments including restaurants, hotels, and institutional catering operators represent one of the fastest-growing end-use segments as operators seek cost-efficient and shelf-stable ingredient solutions. Industrial food processors also contribute significantly to demand through the utilization of canned vegetables, seafood, and fruit products within frozen foods, sauces, snacks, and ready meals. Emergency food supply programs, military procurement systems, and humanitarian aid organizations are emerging as increasingly important institutional buyers due to growing focus on food security preparedness globally.

Explore more data points, trends and opportunities Download Free Sample Report

Canned Food Market Segmentations

By Product Type

- Canned Fruits

- Canned Vegetables

- Canned Seafood

- Canned Meat & Poultry

- Canned Ready Meals

- Canned Dairy & Desserts

- Canned Pet Food

By Packaging Type

- Metal Cans

- BPA-Free Cans

- Easy-Open / Pull-Tab Cans

- Retort Cans & Shelf-Stable Packaging

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Food Stores

- Online Retail / E-Commerce

- Wholesale & Bulk Retail

- Foodservice Distribution

By End User

- Household/Retail Consumers

- Foodservice Industry

- Industrial Food Processing

- Military & Emergency Food Supply

Regional Insights

North America

North America accounted for approximately 31% of the global canned food market in 2025, making it the largest regional market. The United States dominates regional demand due to strong consumption of canned soups, vegetables, seafood, and ready meals. High urbanization levels, busy consumer lifestyles, and extensive retail infrastructure continue to support market expansion. Canada also demonstrates strong demand for premium canned seafood and organic packaged foods. Consumer preference for low-sodium, BPA-free, and clean-label products is reshaping product innovation strategies across the region.

Europe

Europe represented nearly 27% of global canned food revenue in 2025. Germany, the United Kingdom, France, Italy, and Spain remain major consumption markets for canned vegetables, seafood, and prepared meals. The region demonstrates strong demand for organic, sustainable, and recyclable packaged food products due to stringent environmental regulations and increasing health consciousness. Spain and Portugal remain key seafood processing and export hubs supporting regional canned seafood supply chains. Premiumization trends continue to drive strong growth within gourmet canned foods and specialty meal categories across Western Europe.

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing regional market during the forecast period, expanding at over 7% CAGR through 2031. China leads regional demand due to rapid urbanization, increasing middle-class income, and expanding organized retail penetration. India is emerging as a major high-growth market supported by rising convenience food consumption and rapid e-commerce grocery adoption. Japan and South Korea continue to demonstrate strong demand for canned seafood, soups, and premium ready meals. Southeast Asian countries including Indonesia, Vietnam, and Thailand are witnessing rising packaged food demand driven by demographic expansion and changing dietary preferences.

Latin America

Latin America continues to experience steady growth in canned food consumption led by Brazil, Mexico, Argentina, and Chile. Affordability, shelf stability, and improving retail infrastructure support rising market penetration across the region. Brazil remains a major producer and exporter of canned meat products while Mexico demonstrates strong domestic demand for canned beans, vegetables, and ethnic ready meals. Economic volatility in some regional markets continues to encourage consumers to prioritize shelf-stable and cost-efficient food products.

Middle East & Africa

The Middle East & Africa region is witnessing increasing demand for canned foods due to rapid urbanization, food import dependency, and expanding modern retail networks. Saudi Arabia and the UAE represent key consumption centers supported by strong foodservice growth and rising packaged food demand among expatriate populations. South Africa remains the largest canned food market within Africa due to its advanced food processing industry and retail infrastructure. Governments across the region are increasingly investing in food security programs and strategic food reserves, supporting long-term demand for canned products.

Key Players in the Canned Food Market

- Conagra Brands

- Del Monte Foods

- Nestlé

- Kraft Heinz

- Campbell Soup Company

- Thai Union Group

- Hormel Foods

- Bolton Group

- Bonduelle

- Ayam Brand

- Bumble Bee Foods

- Danish Crown

- Princes Group

- Dongwon Industries

- General Mills