Canned Chickpeas Market Size

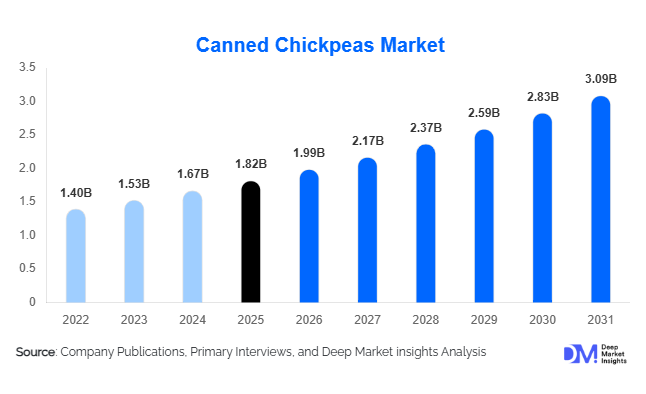

According to Deep Market Insights, the global canned chickpeas market size was valued at USD 1.82 billion in 2025 and is projected to grow from USD 1.99 billion in 2026 to reach USD 3.09 billion by 2031, expanding at a CAGR of 9.2% during the forecast period (2026–2031). The canned chickpeas market growth is primarily driven by increasing consumer preference for plant-based protein sources, rising adoption of healthy convenience foods, and expanding global demand for Mediterranean and vegan cuisine applications.

Key Market Insights

- Canned chickpeas are increasingly becoming a mainstream pantry staple, supported by growing demand for convenient, protein-rich, and shelf-stable food products.

- Plant-based and flexitarian diets are accelerating global chickpea consumption, particularly across North America and Europe where vegan food penetration is rapidly increasing.

- Organic and low-sodium canned chickpeas are witnessing strong premiumization trends, driven by clean-label and health-conscious consumer preferences.

- North America dominates the canned chickpeas market, supported by high hummus consumption, strong retail infrastructure, and increasing adoption of Mediterranean diets.

- Asia-Pacific is the fastest-growing region, led by rising packaged food demand, urbanization, and growing awareness regarding plant-based nutrition.

- Technological innovations in BPA-free packaging, automated canning systems, and sustainable food processing are reshaping competitive dynamics within the global canned chickpeas industry.

canned chickpeas market latest trends

Rising Demand for Plant-Based Protein Products

The global shift toward plant-based nutrition is significantly transforming the canned chickpeas market. Consumers are increasingly replacing animal-based proteins with legumes due to health, environmental, and ethical considerations. Chickpeas are widely recognized for their high protein, fiber, iron, and folate content, making them an ideal ingredient in vegan and flexitarian diets. Food manufacturers are increasingly integrating canned chickpeas into plant-based ready meals, salads, hummus, wraps, soups, and snack products. The rising popularity of Mediterranean cuisine and clean-eating trends is further accelerating chickpea consumption globally. Retailers are also expanding private-label canned chickpea offerings to capitalize on the growing demand for affordable and nutritious pantry staples.

Premiumization and Sustainable Packaging Innovations

Manufacturers are increasingly introducing premium canned chickpea products including organic, non-GMO, low-sodium, and preservative-free variants. Consumers are willing to pay higher prices for clean-label food products that align with wellness and sustainability goals. In parallel, packaging innovation is becoming a major market trend. BPA-free cans, recyclable packaging materials, and lightweight retort pouch formats are gaining traction, particularly across North America and Europe. Companies are also investing in energy-efficient processing technologies and supply chain optimization to reduce environmental impact. E-commerce platforms and subscription-based grocery delivery services are further supporting the premium canned chickpeas segment by improving accessibility to specialty products globally.

canned chickpeas market drivers

Growing Popularity of Healthy Convenience Foods

The increasing consumer preference for healthy convenience foods is a major driver of the canned chickpeas market. Urban consumers are increasingly seeking food products that combine nutritional value with ease of preparation. Canned chickpeas offer extended shelf life, ready-to-use convenience, and versatility across multiple cuisines and meal formats. Rising work-from-home trends, meal-prep culture, and quick cooking preferences are further supporting retail demand. Consumers increasingly incorporate canned chickpeas into salads, grain bowls, soups, curries, and snacks, strengthening overall market expansion.

Expansion of Vegan and Flexitarian Diets

The global expansion of vegan and flexitarian dietary habits is accelerating demand for chickpea-based products. Consumers are increasingly reducing meat consumption due to sustainability concerns and rising awareness regarding cardiovascular health and obesity management. Chickpeas serve as a highly affordable and functional protein alternative for both households and food manufacturers. The rapid expansion of vegan restaurants, healthy fast-casual dining chains, and plant-based food innovation is positively influencing industrial procurement of canned chickpeas. Major food brands are increasingly introducing chickpea-based snacks, dips, and meat substitutes to capitalize on this trend.

canned chickpeas market restraints

Raw Material Price Volatility

The canned chickpeas market remains vulnerable to fluctuations in chickpea crop production and agricultural commodity prices. Climatic disruptions, drought conditions, and water scarcity in major chickpea-producing countries such as India, Turkey, Australia, and Canada can significantly impact supply availability and pricing stability. Rising input costs related to farming, transportation, and packaging materials also create operational challenges for processors and exporters. Such volatility can compress manufacturer profit margins and increase retail pricing pressure.

Health Concerns Regarding Sodium and Processed Foods

Growing consumer concerns regarding sodium content and preservatives in canned foods may restrain market growth in premium health-conscious segments. Some consumers continue to perceive canned products as overly processed compared to fresh or dried legumes. Increasing regulatory scrutiny around food labeling transparency and sodium reduction standards is encouraging manufacturers to reformulate products and adopt clean-label positioning strategies. Companies unable to adapt to changing nutritional preferences may face reduced competitiveness in developed markets.

canned chickpeas industry key opportunities

Expansion of Organic and Functional Chickpea Products

The growing global demand for organic and functional foods presents significant opportunities for canned chickpea manufacturers. Consumers increasingly seek pesticide-free, non-GMO, and high-protein packaged foods that support wellness-oriented lifestyles. Manufacturers are capitalizing on this trend by introducing fortified chickpea products enriched with additional nutrients, reduced sodium formulations, and flavored ready-to-eat variants. Premium product positioning allows companies to achieve higher margins while attracting health-conscious consumers in developed economies. Organic canned chickpeas are particularly gaining traction across specialty retail and online grocery channels.

Growing Demand from Foodservice and Ready Meal Industries

The rapid expansion of healthy fast-casual restaurants, cloud kitchens, and ready meal manufacturers is creating strong procurement demand for canned chickpeas globally. Foodservice operators increasingly utilize chickpeas in hummus, salads, vegan bowls, wraps, soups, and Mediterranean dishes due to their affordability and versatility. The growth of plant-based ready-to-eat meals and meal-kit delivery services is also expanding industrial applications for canned chickpeas. Emerging economies across Asia-Pacific and the Middle East offer substantial whitespace opportunities for new entrants seeking to supply foodservice chains and institutional catering operations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.82 Billion |

| Market Size in 2026 | USD 1.99 Billion |

| Market Size in 2031 | USD 3.09 Billion |

| CAGR | 9.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Conventional canned chickpeas dominate the global market, accounting for the largest revenue share due to affordability, widespread retail penetration, and established consumer familiarity. These products are extensively used in household cooking, foodservice applications, and industrial food manufacturing. Organic canned chickpeas represent the fastest-growing segment as consumers increasingly prioritize clean-label and pesticide-free food products. Low-sodium and flavored variants are also witnessing increasing adoption among health-conscious consumers seeking convenient but nutritionally balanced meal solutions. Ready-to-eat chickpea mixes and seasoned chickpea products are gaining popularity among younger urban consumers who prefer convenient snack and meal-preparation options.

Application Insights

Hummus and dip preparation remains the leading application segment within the canned chickpeas market, supported by strong global demand for Mediterranean cuisine and healthy snack alternatives. Salad and ready-meal applications are also witnessing rapid growth as consumers increasingly integrate chickpeas into protein-rich meal routines. Soups, stews, curries, and ethnic cuisine preparations continue to drive stable demand across retail and foodservice channels. The plant-based food industry is emerging as a major application area, with chickpeas increasingly utilized in vegan meat substitutes, dairy alternatives, and protein-enriched packaged foods. Snack-based applications including roasted chickpea preparations and healthy convenience foods are also expanding globally.

Distribution Channel Insights

Supermarkets and hypermarkets dominate canned chickpeas distribution globally due to extensive shelf visibility, bulk purchasing patterns, and strong private-label penetration. Organized retail chains continue to expand premium organic and specialty canned chickpea offerings to address rising health-conscious demand. Online grocery platforms are the fastest-growing distribution channel, driven by increasing digital grocery adoption, subscription meal services, and direct-to-consumer food brands. Specialty food stores also play a critical role in premium product sales, particularly for organic, low-sodium, and non-GMO variants. Wholesale and institutional supply channels remain important for restaurants, caterers, and food processing companies requiring bulk procurement.

End-Use Insights

Household consumption accounts for the largest share of the canned chickpeas market, supported by rising home cooking trends, convenience food demand, and increasing awareness regarding plant-based nutrition. Consumers increasingly use canned chickpeas in salads, curries, wraps, soups, and healthy snack preparations. The foodservice segment is witnessing the fastest growth due to expanding Mediterranean restaurants, vegan dining concepts, and healthy fast-casual chains globally. Industrial food processing applications are also increasing significantly as manufacturers integrate chickpeas into ready meals, soups, snacks, and plant-based food formulations. Institutional consumption from schools, hospitals, and corporate cafeterias is gradually expanding as organizations promote healthier meal standards and sustainable protein alternatives.

Explore more data points, trends and opportunities Download Free Sample Report

Canned Chickpeas Market Segmentations

By Product Type

- Organic Canned Chickpeas

- Conventional Canned Chickpeas

- Low-Sodium Canned Chickpeas

- Flavored/Seasoned Canned Chickpeas

- Ready-to-Eat Chickpea Mixes

- Chickpeas in Brine

- Chickpeas in Water

- Chickpeas in Sauce-Based Preparations

By Packaging Type

- Metal Cans

- Glass Jars

- Retort Pouches

- Multi-Pack Formats

- Bulk Foodservice Packaging

By Chickpea Variety

- Kabuli Chickpeas

- Desi Chickpeas

- Mixed Chickpea Blends

By Application

- Salads

- Hummus & Dips

- Ready Meals

- Soups & Stews

- Snack Preparations

- Vegan & Plant-Based Recipes

- Ethnic Cuisine Preparations

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Specialty Food Stores

- Online Retail & E-commerce

- Wholesale & Cash-and-Carry

- Direct Institutional Supply

Regional Insights

North America

North America remains the largest regional market for canned chickpeas, accounting for nearly 32% of global market share in 2025. The United States dominates regional demand due to rising adoption of vegan diets, strong hummus consumption, and increasing demand for healthy convenience foods. Retail penetration of organic and premium canned chickpeas continues to expand across supermarkets and online grocery channels. Canada also represents a major market due to its strong chickpea cultivation industry and increasing exports of processed pulse products. Growing demand for clean-label packaged foods is further strengthening regional market growth.

Europe

Europe accounted for approximately 29% of the global canned chickpeas market in 2025, supported by widespread adoption of Mediterranean dietary habits and strong consumer preference for sustainable food products. Germany, the United Kingdom, France, Italy, and Spain represent key regional markets. The UK market benefits from expanding private-label packaged foods and vegan product penetration, while Southern European countries maintain strong traditional chickpea consumption patterns. European consumers increasingly prefer organic, BPA-free, and low-sodium canned products, driving premiumization trends throughout the region.

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing regional market during the forecast period, supported by rising urbanization, expanding packaged food demand, and increasing disposable incomes. India remains one of the world’s largest chickpea producers and consumers, while China is witnessing increasing adoption of westernized healthy eating trends. Australia plays a major role in global chickpea exports and processed food supply chains. Rising middle-class populations, rapid retail modernization, and growth in e-commerce grocery platforms are further accelerating regional canned chickpeas demand.

Latin America

Latin America is gradually emerging as a promising market for canned chickpeas, led by Brazil, Mexico, Argentina, and Chile. Consumers in the region are increasingly adopting plant-based and protein-rich food products as health awareness improves. Retail modernization and expansion of international packaged food brands are contributing to market penetration. Brazil is witnessing rising demand for healthy convenience foods, while Mexico benefits from expanding processed food infrastructure and foodservice growth.

Middle East & Africa

The Middle East & Africa region continues to demonstrate stable demand due to the strong cultural integration of chickpeas in traditional cuisines including hummus, falafel, soups, and stews. Countries such as Saudi Arabia, UAE, Turkey, and Israel represent major demand centers for processed chickpea products. UAE is emerging as an important import-driven packaged food market supported by tourism and expatriate populations. In Africa, rising urbanization and increasing packaged food accessibility are gradually supporting canned food consumption growth across key metropolitan markets.

Key Players in the Canned Chickpeas Market

- Conagra Brands

- Bonduelle Group

- Del Monte Foods

- B&G Foods

- Goya Foods

- Bush Brothers & Company

- Princes Group

- The Kraft Heinz Company

- Ayam Brand

- Eden Foods

- AGT Food and Ingredients

- Riviana Foods

- Roland Foods

- La Costeña

- SunOpta Inc.