Candy Toys Market Size

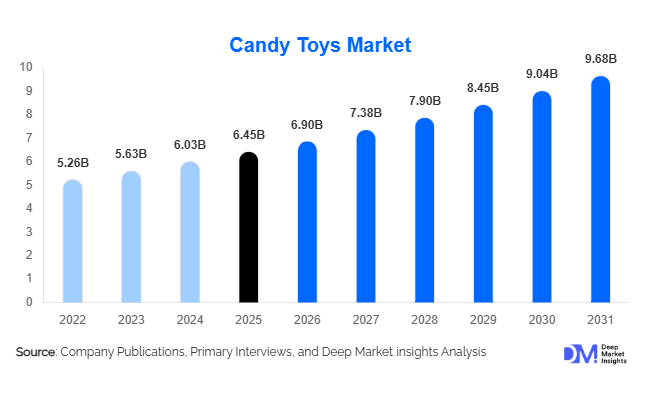

According to Deep Market Insights, the global candy toys market size was valued at approximately USD 6.45 billion in 2025 and is projected to grow from USD 6.90 billion in 2026 to reach USD 9.68 billion by 2031, expanding at a CAGR of 7.0% during the forecast period (2026–2031). The candy toys market growth is being driven by rising consumer demand for novelty confectionery products, increasing popularity of collectible and surprise-based toys, expansion of licensed entertainment merchandise, and growing penetration of organized retail and e-commerce channels. Manufacturers are increasingly combining confectionery products with entertainment experiences, character licensing, and digital engagement strategies to create differentiated offerings that appeal to both children and adult collectors. The convergence of confectionery, toys, collectibles, and entertainment franchises continues to create new growth opportunities across global markets.

Key Market Insights

- Collectible and surprise-based candy toys are becoming the primary growth engine, encouraging repeat purchases through limited-edition releases and blind-box concepts.

- Licensed entertainment properties are transforming product development strategies, with movie, gaming, anime, and streaming franchises driving premium demand.

- Asia-Pacific dominates the global candy toys market, supported by large child populations, strong manufacturing capabilities, and growing consumer spending.

- India is emerging as one of the fastest-growing national markets, fueled by expanding retail infrastructure and increasing disposable incomes.

- E-commerce and direct-to-consumer channels are reshaping distribution models, enabling manufacturers to launch exclusive collectibles and regional product variants.

- Adult collectors are becoming an increasingly important customer segment, creating demand for premium, nostalgic, and limited-edition candy toy products.

Candy Toys Market Latest Trends

Collectible and Blind-Box Candy Toys Driving Consumer Engagement

The candy toys market is increasingly influenced by collectible product formats that encourage repeat purchases and long-term consumer engagement. Blind-box concepts, surprise capsules, mystery packs, and limited-edition collectibles have transformed candy toys from simple novelty products into highly engaging consumer experiences. Manufacturers are leveraging scarcity-driven marketing strategies, seasonal launches, and collectible series to stimulate demand. Consumers, particularly children and young adults, are increasingly motivated by the desire to complete collections rather than solely consume the confectionery component. This trend has significantly improved customer retention rates and average transaction values across key global markets.

Entertainment Licensing and Cross-Media Collaborations Expanding

Strategic partnerships between candy toy manufacturers and entertainment companies are becoming increasingly common. Global franchises from movies, television, gaming, anime, and streaming platforms are being integrated into product designs to enhance consumer appeal. Licensed products typically command premium pricing and generate stronger retail performance than non-licensed alternatives. The rapid expansion of digital entertainment ecosystems has created continuous opportunities for new product launches tied to blockbuster releases, gaming events, and viral content. Companies are also integrating digital collectibles, QR-code experiences, and online reward systems into candy toy offerings to strengthen consumer engagement beyond physical purchases.

Candy Toys Market Drivers

Growing Demand for Experiential and Interactive Products

Modern consumers increasingly seek products that provide experiences beyond traditional consumption. Candy toys combine confectionery, entertainment, collectability, and surprise elements into a single purchase, creating a unique value proposition. This trend is particularly strong among younger consumers who prioritize novelty and engagement. The popularity of unboxing content across social media platforms has further amplified demand for surprise-based candy toys, driving higher product visibility and purchase frequency.

Expansion of Licensed Intellectual Property Partnerships

Licensing agreements with major entertainment brands have become a significant driver of market growth. Candy toy manufacturers are partnering with movie studios, gaming companies, sports organizations, and animation producers to launch character-themed products that attract highly engaged fan communities. Licensed products benefit from established brand recognition and often generate stronger sales performance than generic alternatives. The growing global popularity of anime, gaming, and streaming content is creating additional opportunities for franchise-based candy toy launches.

Rapid Growth of Organized Retail and E-Commerce

The expansion of supermarkets, hypermarkets, convenience chains, and digital commerce platforms has significantly improved product accessibility. Online channels allow manufacturers to introduce exclusive product variants, subscription-based collectible programs, and direct-to-consumer sales strategies. E-commerce platforms also facilitate global distribution of niche collectible products that may not achieve sufficient shelf space in traditional retail environments. Increasing smartphone penetration and digital payment adoption are further supporting online sales growth worldwide.

Candy Toys Market Restraints

Stringent Regulatory Requirements for Children's Products

Candy toys face extensive regulatory oversight due to their dual nature as both food and toy products. Manufacturers must comply with food safety standards, toy safety regulations, labeling requirements, packaging restrictions, and child protection guidelines. Regulatory complexity increases compliance costs and can delay product launches, particularly for multinational companies operating across multiple jurisdictions. Product recalls and safety concerns can also negatively impact brand reputation and consumer trust.

Volatility in Raw Material and Packaging Costs

Fluctuations in sugar, cocoa, packaging materials, plastics, paperboard, and transportation costs continue to create challenges for manufacturers. Rising commodity prices directly affect production economics and profit margins. Smaller market participants often face greater difficulty absorbing cost increases, leading to pricing pressures and competitive disadvantages. Supply chain disruptions and global logistics challenges have further contributed to uncertainty across the industry.

Candy Toys Industry Key Opportunities

Premiumization Through Adult Collector Segments

The emergence of adult collectors represents one of the most attractive opportunities within the candy toys market. Consumers who grew up with novelty confectionery products are increasingly purchasing premium editions linked to nostalgic brands, gaming franchises, anime properties, and entertainment collectibles. This segment typically exhibits higher spending power and stronger willingness to purchase limited-edition products. Manufacturers can capitalize on this trend through premium packaging, exclusive releases, subscription models, and direct-to-consumer engagement strategies.

Expansion into Emerging Consumer Markets

Emerging economies across Asia-Pacific, Latin America, and the Middle East present significant untapped growth potential. Rising disposable incomes, urbanization, expanding retail infrastructure, and growing youth populations are creating favorable conditions for candy toy consumption. Countries such as India, Indonesia, Vietnam, Saudi Arabia, and Brazil are witnessing increased demand for novelty confectionery products. Localized product development, affordable pricing strategies, and regional licensing partnerships can help companies establish stronger market positions in these high-growth regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.45 Billion |

| Market Size in 2026 | USD 6.90 Billion |

| Market Size in 2031 | USD 9.68 Billion |

| CAGR | 7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Collectible candy toys represent the largest product category, accounting for approximately 31% of global market revenue in 2025. Their leadership is primarily driven by the accelerating global trend toward licensed character merchandise, gamified consumption experiences, and the rapid expansion of blind-box and surprise-based retail formats that enhance repeat purchase behavior. The integration of limited-edition drops and seasonal exclusivity has further strengthened consumer engagement, particularly among younger demographics and collectors who actively seek rarity-driven value. Candy with embedded toys continues to maintain strong mainstream appeal due to its combination of confectionery consumption and interactive play, making it highly effective in impulse-driven retail environments. Interactive candy toys, including DIY candy-making kits and assembly-based formats, are experiencing increasing adoption as parents prioritize educational and experiential play that combines entertainment with skill development. Electronic and mechanically enhanced candy toys are gaining traction through improved product innovation that extends play value beyond consumption, while attached-toy formats such as ring candies, dispenser-based products, and novelty packaging solutions remain consistently relevant within convenience-driven and impulse purchase channels supported by high retail visibility.

Candy Format Insights

Chocolate candy toys dominate the market with approximately 38% share of global revenue, supported by deeply entrenched consumer familiarity, strong gifting traditions, and premium positioning opportunities that allow manufacturers to combine indulgence with collectible appeal. The leading growth driver in this segment is the increasing premiumization of chocolate-based confectionery, where brands leverage high-quality ingredients, character licensing, and seasonal editions to strengthen emotional consumer engagement and justify higher price points. Gummy candy toys are witnessing robust growth as a result of continuous flavor innovation, texture experimentation, and broad demographic acceptance across children, teenagers, and adult consumers. Hard candy and compressed candy toys continue to play a stable role within value-oriented segments, where affordability and long shelf life remain key purchasing considerations. Jelly and marshmallow-based novelty products are increasingly being introduced as part of limited-edition and themed product lines that emphasize sensory experience and playful consumption. Mixed-confectionery formats are also gaining momentum by offering multi-texture and multi-flavor experiences within a single package, which enhances perceived value and supports cross-category appeal in both retail and gifting environments.

Distribution Channel Insights

Supermarkets and hypermarkets account for approximately 41% of global candy toy sales, maintaining their position as the dominant distribution channel due to high consumer traffic, strong shelf visibility, and the effectiveness of impulse purchasing behavior at checkout zones. The primary growth driver for this channel is the strategic placement of novelty confectionery products in high-traffic retail zones, where visual merchandising and promotional bundling significantly increase conversion rates. Convenience stores continue to play a critical role in urban and semi-urban markets, particularly for single-unit and on-the-go purchases, supported by their accessibility and extended operating hours. E-commerce is emerging as the fastest-growing distribution channel, driven by direct-to-consumer strategies, subscription-based collectible models, influencer-led product discovery, and the availability of exclusive online-only launches that enhance scarcity value. Toy specialty stores and dedicated confectionery retailers remain essential for premium, licensed, and collector-focused product lines, offering curated assortments and experiential retail environments. Vending machines continue to contribute steady sales in transportation hubs, entertainment venues, and educational institutions, where accessibility and instant purchase convenience remain key demand drivers.

Age Group Insights

Children aged 6–12 years represent the largest consumer segment, accounting for approximately 55% of global demand, driven primarily by their strong engagement with novelty-based products, surprise elements, and collectible toy integrations that reinforce repeat purchase behavior. The leading driver within this segment is the psychological appeal of reward-based consumption combined with character-driven storytelling and interactive product formats that enhance entertainment value. Preschool consumers also contribute significantly to overall demand, with purchasing decisions largely influenced by parents seeking safe, educational, and portion-controlled confectionery options. Teenagers are increasingly participating in the market through licensed gaming, anime, and entertainment-themed products that align with their digital media consumption habits and identity-driven purchasing preferences. Young adults and adult collectors represent the fastest-growing demographic segment, fueled by nostalgia marketing, pop culture licensing, anime fandom, gaming communities, and the growing perception of candy toys as collectible lifestyle artifacts. Manufacturers are increasingly responding to this shift by developing premium, display-oriented, and limited-edition product lines tailored specifically for older consumers seeking exclusivity and long-term collectible value.

End-Use Insights

Household consumption remains the dominant end-use segment, contributing approximately 63% of total market demand, primarily driven by routine household purchasing behavior where candy toys are used as rewards, treats, and entertainment products for children. The leading growth driver in this segment is the increasing emphasis on at-home experiential consumption, where parents seek products that combine indulgence with engagement and interactive play. Gifting and celebrations represent a rapidly expanding application area, supported by strong demand during holidays, birthdays, festivals, and seasonal events where novelty confectionery products serve as affordable yet emotionally engaging gifts. Promotional usage is also expanding, as brands increasingly incorporate candy toys into marketing campaigns to enhance consumer engagement, product sampling, and brand recall. Educational and activity-based applications are emerging through DIY kits and structured play formats that combine learning with confectionery consumption, aligning with broader trends in edutainment. The collectible hobby segment is experiencing notable expansion as adult consumers increasingly integrate candy toy products into memorabilia collections, driven by fandom culture, limited-edition scarcity strategies, and the rising influence of digital communities that reinforce collectible value perception.

Explore more data points, trends and opportunities Download Free Sample Report

Candy Toys Market Segmentations

By Product Type

- Collectible Candy Toys

- Candy with Embedded Toys

- Candy with Attached Toys

- Interactive Candy Toys

- Electronic Candy Toys

- Mechanical Candy Toys

By Candy Format

- Chocolate Candy Toys

- Gummy Candy Toys

- Hard Candy Toys

- Chewing Candy Toys

- Jelly & Marshmallow Candy Toys

- Compressed Candy Toys

- Mixed Confectionery Candy Toys

By Licensing Category

- Entertainment Licensed Products

- Gaming Licensed Products

- Anime & Manga Licensed Products

- Sports Licensed Products

- Non-Licensed Products

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- E-commerce Platforms

- Toy Specialty Stores

- Confectionery Specialty Stores

- Vending Machines

- Direct-to-Consumer Channels

By End Use

- Household Consumption

- Gifting & Celebrations

- Promotional & Marketing Campaigns

- Entertainment & Theme Parks

- Educational & Activity-Based Use

- Collectible Hobby Market

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 35% of global candy toys market revenue, making it the largest and most influential regional market. The region’s growth is primarily driven by rapid urbanization, rising disposable incomes, and the strong cultural integration of confectionery novelty products into both daily consumption and gifting traditions. China plays a dual role as both the largest production hub and a major consumption market, supported by extensive manufacturing capabilities, efficient supply chains, and strong domestic demand for licensed and collectible products. Japan’s growth is fueled by continuous innovation in novelty confectionery, high consumer acceptance of character-driven merchandising, and a deeply embedded culture of collectible toy consumption that supports premium pricing. India is emerging as one of the fastest-growing markets due to expanding middle-class populations, increasing retail penetration in Tier II and Tier III cities, and growing exposure to global entertainment franchises. South Korea’s expansion is strongly influenced by the global reach of K-pop, anime culture, gaming ecosystems, and entertainment licensing, which collectively drive high engagement with themed candy toy products and limited-edition collaborations.

North America

North America holds approximately 28% of global market share, with the United States accounting for nearly 23% of worldwide demand. The region’s growth is driven by strong consumer purchasing power, well-established licensing ecosystems, and a mature retail infrastructure that effectively supports premium and collectible product distribution. A key driver in this region is the high penetration of entertainment-driven licensing agreements across major media franchises, which significantly enhances product visibility and consumer demand. Collectible candy toys and premium limited-edition releases perform particularly well due to strong collector communities and high engagement with pop culture merchandising. Canada contributes steady demand through stable household consumption patterns and growing interest in novelty confectionery products that align with seasonal and gifting occasions. The region is also a leader in the adoption of digitally integrated and experience-enhanced candy toy products, where online engagement and physical collectibles are increasingly merged through promotional ecosystems and loyalty-based campaigns.

Europe

Europe represents approximately 24% of global market revenue, supported by a strong confectionery heritage, well-developed retail networks, and high consumer preference for premium and quality-oriented products. Germany leads regional demand, driven by high per-capita confectionery consumption, robust retail distribution systems, and strong demand for novelty and seasonal product variations. The United Kingdom exhibits significant demand for licensed and collectible products, supported by strong entertainment franchise penetration and a well-established gifting culture. France and Italy are experiencing steady growth in premium and artisanal candy toy segments, where product aesthetics, packaging innovation, and ingredient quality play a key role in purchasing decisions. A major regional driver is the increasing emphasis on sustainability, including recyclable packaging, reduced sugar formulations, and environmentally conscious production practices, which are significantly shaping consumer preferences and influencing brand positioning strategies across European markets.

Latin America

Brazil and Mexico dominate regional demand in Latin America, supported by large youth populations, increasing urbanization, and the ongoing modernization of retail infrastructure. The primary growth driver in this region is the rising accessibility of branded confectionery products through expanding supermarket chains and convenience retail formats. Consumers in Latin America demonstrate strong preference for affordable, entertainment-oriented confectionery that combines value pricing with engaging product formats. Economic development and the gradual expansion of middle-class households are further supporting increased discretionary spending on novelty and impulse-driven products. Manufacturers are increasingly focusing on localization strategies, including culturally relevant licensing, flavor adaptation, and price-optimized product offerings to strengthen market penetration across diverse socioeconomic segments.

Middle East & Africa

The Middle East and Africa region is experiencing steady and sustained growth, led by key markets such as Saudi Arabia, the United Arab Emirates, South Africa, and Egypt. Growth in the region is primarily driven by rising youth populations, increasing urbanization, and the expansion of modern retail formats that improve product accessibility. In Gulf countries, strong disposable incomes and high demand for imported premium brands support the performance of licensed and collectible candy toy products. A significant driver is the growing influence of international entertainment content, including animation and gaming franchises, which directly enhances demand for themed confectionery products. South Africa and North African markets are benefiting from improving retail penetration and expanding consumer awareness of novelty confectionery formats. Additionally, increasing tourism activity and rapid development of entertainment and leisure infrastructure are further accelerating demand for experiential and novelty-based confectionery products across the region.

Key Players in the Candy Toys Market

- Ferrero Group

- Perfetti Van Melle

- The Hershey Company

- Nestlé

- Mondelez International

- Haribo

- Meiji Holdings

- Ezaki Glico

- Lotte Wellfood

- Orion Corporation

- Yildiz Holding

- August Storck

- Tohato

- Jelly Belly Candy Company

- PEZ International