Butter Cookies Market Size

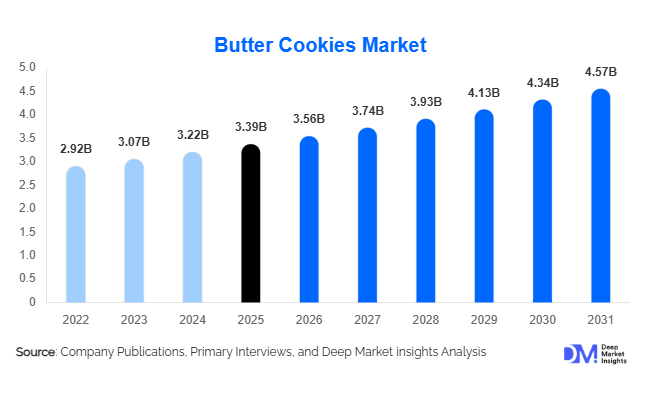

According to Deep Market Insights, the global butter cookies market size was valued at approximately USD 3.39 billion in 2025 and is projected to grow from USD 3.56 billion in 2026 to reach USD 4.57 billion by 2031, expanding at a CAGR of 5.1% during the forecast period (2026–2031). The butter cookies market growth is primarily driven by rising consumer preference for premium bakery products, increasing demand for indulgent snacking experiences, expansion of gifting-oriented food categories, and growing penetration of organized retail and e-commerce channels worldwide.

Butter cookies continue to occupy a premium position within the global sweet biscuits and baked snacks industry due to their rich taste, high butter content, premium perception, and strong association with festive gifting. While mature markets in Europe and North America maintain steady consumption, emerging economies across Asia-Pacific are witnessing significant demand growth fueled by rising disposable incomes, urbanization, and increasing exposure to Western-style bakery products. Product innovations focused on clean-label ingredients, premium packaging, artisanal formulations, and healthier variants are further supporting market expansion. Manufacturers are also investing heavily in digital retail channels and direct-to-consumer platforms to strengthen brand visibility and improve consumer reach. As premium snacking and food gifting continue to gain traction globally, butter cookies are expected to remain one of the most resilient and attractive categories within the packaged bakery products market.

Key Market Insights

- Traditional butter cookies account for the largest share of the market, representing nearly 58% of global revenues due to strong consumer familiarity and gifting demand.

- Metal tin packaging remains the preferred format globally, accounting for approximately 34% of sales due to its premium appearance and suitability for festive gifting.

- Europe dominates the global butter cookies market, holding nearly 35% market share owing to established consumption traditions and strong manufacturing capabilities.

- Asia-Pacific is the fastest-growing regional market, supported by rising middle-class incomes, premium snack adoption, and increasing retail penetration.

- Household consumers represent the largest end-user segment, contributing approximately 69% of overall demand worldwide.

- E-commerce and direct-to-consumer channels are rapidly transforming distribution, enabling premium and imported brands to expand their consumer reach globally.

- Premiumization remains the strongest industry trend, with consumers increasingly willing to pay higher prices for gourmet, imported, and artisanal butter cookie products.

Butter Cookies Market Latest Trends

Premiumization Driving Category Value Growth

Premiumization has emerged as one of the most influential trends shaping the global butter cookies market. Consumers increasingly seek authentic butter content, premium ingredients, artisanal recipes, and imported European-style products. Premium butter cookies command significantly higher average selling prices compared to conventional sweet biscuits, helping manufacturers improve margins despite raw material cost fluctuations. Luxury gifting packs, gourmet assortments, specialty flavors, and limited-edition seasonal launches are becoming major growth drivers across both developed and emerging markets. Companies are increasingly positioning butter cookies as affordable indulgences, appealing to consumers seeking premium experiences without substantial spending commitments.

Growth of Clean-Label and Better-for-You Butter Cookies

Health-conscious consumers are encouraging manufacturers to introduce clean-label, organic, reduced-sugar, and gluten-free butter cookie formulations. While indulgence remains central to category appeal, buyers increasingly scrutinize ingredient labels and prefer products made with natural ingredients and fewer artificial additives. Premium brands are responding through the introduction of organic butter, non-GMO ingredients, and transparent sourcing practices. This trend is particularly evident in North America and Europe, where consumers increasingly balance indulgence with wellness considerations. As a result, functional and specialty dietary butter cookies are expected to outperform traditional products in terms of growth rates during the forecast period.

Butter Cookies Market Drivers

Rising Demand for Premium Snacking Products

Consumers globally are increasingly gravitating toward premium snack products that offer superior taste, quality ingredients, and elevated consumption experiences. Butter cookies perfectly align with this trend due to their rich flavor profile and strong association with indulgence. Premium bakery products continue to outperform standard biscuit categories in value growth, particularly among urban consumers seeking high-quality packaged snacks. The expansion of gourmet food retailing and premium supermarket offerings is further supporting category growth.

Expansion of Organized Retail and E-Commerce

The rapid growth of organized retail formats, supermarkets, hypermarkets, specialty stores, and online grocery platforms has significantly improved product accessibility. Digital commerce enables consumers to access both domestic and imported butter cookie brands while providing manufacturers with direct engagement opportunities. Subscription services, gifting portals, and personalized packaging options are also contributing to rising sales through online channels. Increasing smartphone penetration and digital payment adoption in emerging economies further support e-commerce-driven market growth.

Growing Seasonal and Corporate Gifting Demand

Butter cookies have become an important category within global food gifting markets. Seasonal demand peaks during Christmas, Lunar New Year, Eid, Diwali, and other festive periods. Corporate gifting programs increasingly incorporate premium butter cookie assortments due to their universal appeal, premium presentation, and long shelf life. Manufacturers continue introducing decorative packaging and limited-edition product offerings specifically designed for gifting occasions, generating substantial revenue growth during festive periods.

Butter Cookies Market Restraints

Volatility in Butter and Dairy Prices

Butter represents one of the largest input costs in production. Global fluctuations in milk and dairy prices directly impact manufacturing costs and profitability. Rising butter prices often force manufacturers to increase retail prices, potentially reducing consumer demand in price-sensitive markets. Smaller manufacturers are particularly vulnerable to raw material price volatility due to limited procurement scale and lower bargaining power.

Increasing Health Concerns Regarding Sugar Consumption

Growing awareness surrounding obesity, diabetes, and excessive sugar consumption presents a challenge for traditional butter cookie manufacturers. Consumers are increasingly seeking healthier snack alternatives with lower sugar content and improved nutritional profiles. Regulatory initiatives aimed at reducing sugar consumption may also impact category growth over the long term. Manufacturers must therefore balance indulgence with evolving health and wellness preferences through product reformulation and innovation.

Butter Cookies Industry Key Opportunities

Expansion into High-Growth Asian Markets

Asia-Pacific represents the most attractive growth opportunity for butter cookie manufacturers. Rising disposable incomes, expanding middle-class populations, and increasing acceptance of Western-style bakery products are creating substantial demand across China, India, Indonesia, Vietnam, Thailand, and the Philippines. Premium imported products particularly benefit from strong gifting traditions across many Asian countries. Companies investing in regional manufacturing facilities, localized flavors, and strategic retail partnerships can capture significant growth opportunities over the coming decade.

Premium Gifting and Gourmet Product Innovation

The continued expansion of premium food gifting presents significant opportunities for both established players and new entrants. Luxury packaging, seasonal assortments, artisanal ingredients, and customized gifting solutions can command premium pricing while improving profitability. Corporate gifting, festive celebrations, and special occasions continue driving demand for premium butter cookie offerings. Manufacturers introducing gourmet flavors, premium imported butter, and handcrafted positioning are expected to capture increasing market share within the higher-margin segments of the industry.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.39 Billion |

| Market Size in 2026 | USD 3.56 Billion |

| Market Size in 2031 | USD 4.57 Billion |

| CAGR | 5.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Traditional butter cookies continue to dominate the global butter cookies market, accounting for approximately 58% of total revenue in 2025. Their leadership is supported by strong consumer familiarity, widespread retail availability, established brand loyalty, and enduring demand across both everyday snacking and gifting occasions. Danish-style butter cookies, classic butter assortments, and shortbread varieties remain particularly popular due to their association with premium quality, heritage baking traditions, and festive consumption. The segment also benefits from its broad appeal across age groups and geographic markets, making it the preferred product category among both household consumers and institutional buyers.Premium and gourmet butter cookies represent the fastest-growing product category, driven by increasing consumer willingness to pay for superior ingredients, artisanal production methods, authentic recipes, and differentiated taste profiles. Growing demand for indulgent snacks, premium gifting products, and imported bakery items is encouraging manufacturers to expand their premium portfolios. At the same time, organic, clean-label, preservative-free, and non-GMO butter cookies are gaining traction among health-conscious consumers seeking greater ingredient transparency. Gluten-free, reduced-sugar, vegan, and other specialty dietary variants are also expanding market opportunities, particularly across North America and Western Europe where dietary preferences continue to evolve. Product innovation remains centered on premium butter content, natural flavorings, limited-edition seasonal offerings, regional recipe adaptations, and texture enhancements that allow brands to strengthen differentiation within the broader sweet biscuits and bakery products industry.

Flavor Insights

Original butter flavor remains the largest flavor category, representing approximately 47% of global sales in 2025. The segment benefits from consumers’ strong association between authentic butter taste and traditional baking craftsmanship, premium quality, and product authenticity. The enduring popularity of classic butter flavor is further reinforced by its suitability for both everyday consumption and gifting occasions, enabling manufacturers to maintain consistent demand across multiple distribution channels and geographic regions.Chocolate-flavored butter cookies constitute the second-largest segment, supported by broad consumer acceptance, successful premium product introductions, and growing demand for indulgent snacking experiences. Manufacturers are increasingly combining chocolate with premium ingredients such as dark cocoa, chocolate chips, and filled centers to enhance product appeal. Beyond traditional offerings, nut-based, fruit-infused, vanilla, caramel, coffee, and seasonal flavors continue gaining popularity among younger consumers seeking variety and novelty. Limited-edition festive flavors introduced during holidays and special celebrations are becoming an important growth strategy, helping brands increase consumer engagement, drive repeat purchases, and strengthen seasonal sales performance. The ongoing diversification of flavor portfolios is enabling manufacturers to target evolving consumer preferences while expanding their customer base across both mature and emerging markets.

Packaging Format Insights

Metal tins remain the leading packaging format globally, accounting for nearly 34% of market revenues in 2025. Their dominance is primarily driven by strong demand for premium gifting products, enhanced product protection, extended shelf life, and the premium visual appeal associated with traditional butter cookie packaging. Metal tins are particularly popular during festive seasons and special occasions, where presentation and gift suitability significantly influence purchasing decisions. The reusable nature of tins also contributes to consumer preference, supporting perceived value and brand recognition.Rigid cartons continue to maintain a significant market presence due to their cost-effectiveness, strong shelf visibility, and suitability for mass retail distribution. Flexible pouches are gaining popularity among value-oriented consumers because of their affordability, portability, and convenience. Single-serve packs and multipacks are witnessing increasing demand from busy consumers seeking portion-controlled snacking options, while institutional buyers favor individually wrapped products for hygiene and convenience purposes. Sustainability is becoming a key packaging innovation driver across the industry, with manufacturers investing in recyclable materials, lightweight packaging formats, reduced plastic usage, and environmentally responsible packaging solutions to align with evolving regulatory requirements and consumer sustainability expectations.

Distribution Channel Insights

Hypermarkets and supermarkets remain the dominant distribution channel, accounting for approximately 50% of global butter cookie sales in 2025. Their leadership is supported by extensive product assortments, strong promotional capabilities, attractive in-store merchandising, and widespread consumer accessibility. Large-format retail stores continue to serve as important purchasing destinations for both everyday consumption and seasonal gifting purchases, enabling brands to achieve significant market visibility and volume sales.Traditional grocery stores continue to play a critical role in emerging economies where neighborhood retail formats remain highly influential in consumer purchasing behavior. Specialty food retailers support premium, imported, and gourmet butter cookie sales by catering to consumers seeking differentiated products and premium experiences. Online retail is emerging as one of the fastest-growing channels, driven by rising internet penetration, expanding digital payment adoption, growing consumer preference for convenience, and increasing direct-to-consumer sales strategies. E-commerce platforms are enabling manufacturers to broaden geographic reach, offer personalized gifting solutions, launch exclusive product variants, and implement subscription-based purchasing models that enhance customer retention and long-term revenue growth.

End-Use Insights

Household consumers represent the largest end-use segment, accounting for approximately 69% of global butter cookie demand in 2025. The segment's dominance is driven by the widespread consumption of butter cookies as convenient snacks, desserts, and accompaniments to tea, coffee, and other beverages. Consistent household demand is further supported by family-oriented purchasing patterns, festive celebrations, and the product’s strong appeal across multiple age groups. The increasing availability of premium, flavored, and specialty variants is also encouraging greater household consumption and product experimentation.The foodservice segment is expanding steadily as cafés, bakeries, hotels, restaurants, and catering operators increasingly incorporate butter cookies into their product offerings. Premium hospitality establishments frequently utilize butter cookies as complementary items alongside beverages and desserts, supporting growth in commercial consumption. Institutional demand is also rising among airlines, educational institutions, healthcare facilities, and corporate offices that require individually packaged products for convenience, hygiene, and customer satisfaction purposes. In addition, corporate gifting programs, premium gift baskets, and specialty retail applications continue to create incremental demand, particularly during holiday seasons, cultural celebrations, and business events.

Explore more data points, trends and opportunities Download Free Sample Report

Butter Cookies Market Segmentations

By Product Type

- Traditional Butter Cookies

- Premium & Gourmet Butter Cookies

- Functional & Better-for-You Butter Cookies

- Organic & Clean-Label Butter Cookies

- Specialty Dietary Butter Cookies

By Flavor Category

- Original/Classic Butter

- Chocolate-Based

- Vanilla-Based

- Nut-Based

- Fruit-Based

- Caramel & Toffee

- Seasonal & Limited Edition Flavors

By Packaging Format

- Metal Tins

- Rigid Boxes/Cartons

- Flexible Pouches

- Multipacks

- Single-Serve Packs

By Distribution Channel

- Hypermarkets & Supermarkets

- Convenience Stores

- Traditional Grocery Retail

- Specialty Food Stores

- Online Retail/E-Commerce

- Direct-to-Consumer (DTC)

By Price Positioning

- Economy

- Mid-Range

- Premium

- Luxury/Gifting

Regional Insights

Europe

Europe remains the largest regional market, accounting for approximately 35% of global butter cookie revenues in 2025. The region benefits from a deeply rooted bakery culture, strong consumer preference for premium baked goods, and longstanding traditions associated with butter-based confectionery products. Germany, the United Kingdom, France, Denmark, Belgium, Italy, and the Netherlands represent major consumption centers, supported by high per-capita bakery consumption and mature retail infrastructure. Denmark continues to serve as a major production and export hub due to the global recognition of Danish butter cookies and the presence of well-established manufacturers.Regional growth is supported by increasing demand for premium and artisanal bakery products, rising consumer preference for authentic and heritage recipes, strong seasonal gifting traditions, and continuous product innovation focused on premium ingredients and clean-label formulations. The expansion of specialty retail channels, growing demand for organic and sustainable food products, and the increasing popularity of gourmet snack offerings are further contributing to market development across the region.

Asia-Pacific

Asia-Pacific accounts for approximately 32% of global market share and represents the fastest-growing regional market, with a projected CAGR of nearly 6.8% during the forecast period. China remains the largest market within the region, benefiting from strong gifting traditions, growing middle-class spending, and increasing demand for premium imported bakery products. India is emerging as one of the most attractive growth markets, supported by rapid urbanization, rising disposable incomes, expanding organized retail networks, and increasing exposure to international food brands. Japan, South Korea, Australia, Indonesia, Thailand, and Vietnam continue to contribute significantly to regional demand growth.The region’s growth is being driven by expanding middle-class populations, increasing westernization of dietary habits, rising premiumization trends in packaged foods, rapid e-commerce expansion, and growing demand for gift-oriented confectionery products. The development of modern retail infrastructure, increasing consumer spending on indulgent snacks, and strong adoption of premium packaged bakery products among younger consumers are expected to sustain robust market expansion throughout the forecast period.

North America

North America accounts for approximately 22% of global butter cookie revenues. The United States represents the largest market in the region, supported by strong demand for premium bakery products, imported European cookies, and indulgent snack offerings. Seasonal consumption patterns, particularly during holiday periods, continue to generate significant category sales, while Canada contributes stable demand through premium retail, specialty food stores, and gourmet gifting segments.Regional growth is supported by increasing consumer preference for premium and specialty snacks, rising demand for clean-label and natural ingredient products, growing popularity of international bakery brands, and expanding online grocery sales. Product innovation focused on healthier formulations, premium ingredients, and unique flavor combinations is attracting a broader consumer base. Additionally, strong gifting culture, increasing demand for convenient packaged snacks, and ongoing premiumization across the bakery sector continue to strengthen market prospects throughout North America.

Latin America

Latin America represents approximately 6% of global butter cookie demand. Brazil remains the largest market in the region, benefiting from growing consumer interest in premium packaged snacks, expanding middle-income populations, and increasing availability of imported bakery products. Mexico, Argentina, Colombia, and Chile are also witnessing steady growth in demand for packaged bakery products, supported by evolving consumer lifestyles and expanding retail distribution networks.Regional growth is being driven by rising disposable incomes, increasing urbanization, expanding supermarket and hypermarket penetration, and growing consumer awareness of premium snack products. The gradual development of modern retail channels, improving access to international brands, and increasing demand for convenient ready-to-eat bakery products are creating favorable conditions for long-term market expansion. Seasonal gifting trends and the growing influence of western consumption patterns are also contributing to rising butter cookie sales across the region.

Middle East & Africa

The Middle East and Africa account for approximately 5% of global butter cookie revenues. Demand is concentrated primarily in the Gulf Cooperation Council (GCC) countries, particularly Saudi Arabia and the United Arab Emirates, where premium gifting traditions, strong purchasing power, and high consumer spending on imported food products support market growth. South Africa remains the leading market within Africa due to its relatively developed retail infrastructure and growing consumer demand for premium packaged snacks.Growth across the region is being driven by rising disposable incomes, expanding modern retail networks, increasing tourism and hospitality sector activity, and growing demand for premium confectionery and bakery products. Cultural gifting traditions, particularly during religious festivals and celebrations, continue to support strong demand for premium packaged butter cookies. Furthermore, increasing urbanization, greater exposure to international food brands, and the expansion of organized retail channels are expected to create additional growth opportunities across both Middle Eastern and African markets over the forecast period.

Key Players in the Butter Cookies Market

- Mondelez International

- Lotus Bakeries

- Bahlsen GmbH

- Campbell Soup Company (Pepperidge Farm)

- Walkers Shortbread

- Kelsen Group

- Yildiz Holding

- Burton's Biscuit Company

- pladis Global

- Arnott's Group

- Meiji Holdings

- Bourbon Corporation

- Griesson-de Beukelaer

- Grupo Bimbo

- Danish Speciality Foods