Burritos Market Size

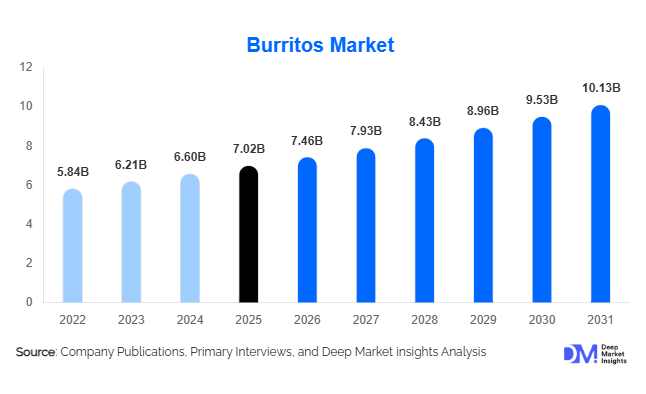

According to Deep Market Insights, the global burritos market size was valued at USD 7.02 billion in 2025 and is projected to grow from USD 7.46 billion in 2026 to reach USD 10.13 billion by 2031, expanding at a CAGR of 6.3% during the forecast period (2026–2031). The burritos market growth is primarily driven by increasing consumer demand for convenient meal solutions, rising popularity of Mexican-inspired cuisine worldwide, expansion of fast-casual restaurant chains, and growing penetration of frozen ready-to-eat food products across retail channels. Product innovation in plant-based proteins, premium ingredients, and healthier tortilla options is further supporting market expansion across both developed and emerging economies.

Key Market Insights

- Fresh prepared burritos remain the largest product category, accounting for nearly 38% of global market revenue due to strong demand from fast-casual restaurant chains.

- Chicken burritos dominate the filling segment, representing approximately 27% of global sales owing to broad consumer acceptance and favorable nutritional positioning.

- North America leads the global burritos market, accounting for nearly 57% of total market demand, supported by established consumption habits and extensive foodservice infrastructure.

- Asia-Pacific is the fastest-growing regional market, driven by increasing adoption of Western food formats and rapid expansion of food delivery platforms.

- Frozen burritos continue gaining popularity, fueled by rising household demand for convenient and protein-rich meal options.

- Plant-based, gluten-free, and high-protein burritos are emerging as key innovation areas, enabling manufacturers to capture premium consumer segments.

Burritos Market Latest Trends

Health-Oriented Burrito Innovation Accelerating

Health-conscious consumers are reshaping product development strategies across the global burritos market. Manufacturers are increasingly introducing high-protein burritos, low-carb tortilla formulations, gluten-free alternatives, and plant-based fillings to address changing dietary preferences. The demand for clean-label products with reduced sodium levels and organic ingredients has also increased significantly. Fast-casual chains and packaged food manufacturers are investing heavily in nutritional transparency and menu customization to appeal to fitness-focused consumers. Protein-rich formulations featuring grilled chicken, lean beef, legumes, and plant proteins are becoming standard offerings. These innovations are helping burritos evolve from indulgent convenience foods into balanced meal solutions that align with modern wellness trends.

Frozen Burritos Becoming a Mainstream Convenience Food

The frozen burrito segment is witnessing strong growth due to changing consumer lifestyles and increasing demand for quick meal preparation. Modern freezing technologies have significantly improved product quality, texture retention, and shelf life, making frozen burritos a preferred option for households seeking convenience without sacrificing taste. Retailers are expanding frozen Mexican food sections, while manufacturers are launching premium frozen burrito lines featuring gourmet ingredients and chef-inspired recipes. E-commerce grocery platforms are further strengthening market accessibility, allowing consumers to purchase frozen burritos through online channels with home delivery. This trend is particularly prominent in North America and Europe, where frozen food consumption continues to rise across urban households.

Burritos Market Drivers

Growing Demand for Convenient and Portable Meals

Busy lifestyles, increasing workforce participation, and urbanization have significantly increased demand for convenient meal formats. Burritos provide consumers with a complete meal containing proteins, carbohydrates, vegetables, and sauces in a portable format. This convenience factor makes burritos particularly attractive to working professionals, students, and commuters. The growth of grab-and-go foodservice formats and food delivery platforms has further accelerated market demand. As consumers continue prioritizing convenience without compromising meal quality, burritos are increasingly positioned as a practical solution for modern eating habits.

Expansion of Fast-Casual Restaurant Chains

The rapid expansion of fast-casual dining chains has been a major growth catalyst for the global burritos market. Operators such as Chipotle Mexican Grill, QDOBA Mexican Eats, Moe's Southwest Grill, and regional burrito chains have expanded their footprint across international markets. Fast-casual restaurants emphasize fresh ingredients, customization, and premium quality, aligning closely with consumer expectations. Digital ordering platforms, loyalty programs, and delivery integrations have further enhanced customer engagement and sales growth. The continued globalization of Mexican-inspired cuisine is expected to support further expansion of burrito-focused restaurant concepts.

Burritos Market Restraints

Raw Material Price Volatility

Fluctuating prices of key ingredients such as beef, chicken, cheese, wheat flour, avocados, and vegetables continue to impact profitability across the burritos value chain. Supply chain disruptions, climate-related agricultural challenges, and commodity inflation have increased procurement costs for both manufacturers and foodservice operators. Companies often face difficulties passing these increased costs directly to consumers in highly competitive markets, leading to margin pressures and pricing challenges.

Perceived Nutritional Concerns

Despite increasing product innovation, traditional burritos are often perceived as high-calorie, high-sodium meal options. Growing consumer awareness regarding obesity, cardiovascular health, and dietary quality may limit consumption among certain demographics. Manufacturers must continuously invest in healthier formulations, transparent labeling, and portion-controlled offerings to address these concerns. Failure to adapt to evolving health preferences could constrain long-term market growth potential.

Burritos Market Industry Key Opportunities

Expansion Across Emerging International Markets

Significant growth opportunities exist in emerging economies where Mexican-inspired cuisine remains underpenetrated. Countries such as India, China, South Korea, Saudi Arabia, and the United Arab Emirates are experiencing rising demand for international food concepts due to urbanization, higher disposable incomes, and increasing exposure to global dining trends. Localized menu adaptations incorporating regional flavors can help companies accelerate adoption while maintaining authentic burrito positioning. Food delivery ecosystems and shopping mall-based restaurant expansion are expected to create additional growth avenues in these markets.

Plant-Based and Premium Burrito Development

The global shift toward plant-based diets presents substantial opportunities for product innovation. Vegan burritos, meat-alternative fillings, organic ingredients, and functional nutrition products are attracting premium consumer segments willing to pay higher prices. Manufacturers that successfully combine convenience, taste, and nutritional value can differentiate themselves in an increasingly competitive market. Premium burritos featuring sustainably sourced ingredients, gourmet fillings, and artisanal tortillas are expected to generate higher margins while expanding the overall addressable market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7.02 Billion |

| Market Size in 2026 | USD 7.46 Billion |

| Market Size in 2031 | USD 10.13 Billion |

| CAGR | 6.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Format Insights

Fresh prepared burritos continue to account for the largest share of the global market, contributing approximately 38% of total revenue in 2025. This leadership is primarily driven by strong consumer preference for freshly assembled, customizable, and high-quality meal experiences that align with fast-casual dining culture. The expansion of urban foodservice outlets, increasing willingness to pay for premium freshness, and the growing perception of burritos as a complete, balanced meal further reinforce this dominance. Frozen burritos represent the fastest-growing product category, supported by rising demand for convenient, long-shelf-life meal solutions that align with busy lifestyles, dual-income households, and expanding retail freezer infrastructure. Breakfast burritos are gaining traction as on-the-go morning consumption increases, particularly among working professionals and students seeking portable and protein-rich options. Ready-to-eat shelf-stable burritos and snack-sized formats are gradually carving niche positions in convenience stores, travel retail, and vending ecosystems, where portability and quick consumption are key purchasing drivers. Across all formats, innovation in premium ingredients, plant-based alternatives, and health-focused formulations is strengthening category expansion and supporting long-term diversification.

Filling Type Insights

Chicken burritos dominate the global filling segment with approximately 27% share of total revenue, largely due to affordability, widespread consumer acceptance, and alignment with health-conscious protein preferences. Demand is further reinforced by the versatility of chicken in global flavor adaptations and its strong integration into quick-service restaurant menus. Beef burritos maintain significant popularity, particularly across North and Latin America, where traditional Mexican cuisine continues to influence mainstream consumption patterns and where consumers associate beef with richer taste profiles and indulgent eating occasions. Vegetarian and vegan burritos are experiencing the fastest growth, driven by accelerating flexitarian lifestyles, rising awareness of plant-based nutrition, and increasing environmental sustainability concerns among younger consumers. Pork burritos continue to hold steady regional relevance, especially in markets with strong culinary traditions tied to pork-based Mexican dishes, while seafood burritos are expanding in coastal regions and premium dining formats where consumers seek differentiated protein experiences. Mixed-protein burritos are also gaining momentum as manufacturers and foodservice operators innovate with higher-protein, flavor-rich combinations designed to meet evolving fitness-oriented and experiential eating trends.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, accounting for approximately 46% of global retail burrito sales. Their leadership is supported by extensive product assortment, strong promotional strategies, and well-developed frozen food infrastructure that enables consistent product availability. The primary growth driver within this channel is the increasing penetration of private-label frozen meal offerings and the expansion of premium ready-meal sections targeting urban households. Convenience stores play a critical role in supporting immediate consumption demand, particularly for ready-to-eat and snack-sized burritos, benefiting from high foot traffic, urban density, and impulse purchase behavior. Club stores and cash-and-carry formats are expanding due to increasing bulk purchasing behavior among families and foodservice operators seeking cost efficiency. Online grocery platforms represent the fastest-growing distribution channel, driven by digital adoption, subscription-based meal purchasing, and improved cold-chain logistics enabling reliable delivery of frozen and chilled products. Specialty food retailers also contribute meaningfully to market growth by focusing on artisanal, organic, and premium burrito variants that appeal to health-conscious and gourmet-oriented consumers.

End Use Insights

Household consumption remains the largest end-use segment, accounting for approximately 44% of global demand in 2025. This dominance is supported by the increasing integration of frozen and ready-to-eat burritos into everyday meal planning, driven by time constraints, dual-income households, and the need for convenient yet filling meal options. The availability of diverse product formats and improved nutritional positioning further strengthens household penetration. Foodservice operators, including quick-service restaurants and fast-casual chains, represent the fastest-growing end-use segment, fueled by strong consumer demand for customizable, globally inspired meals and rapid expansion of branded restaurant networks. Growth in this segment is further supported by menu innovation and operational efficiency benefits associated with standardized burrito preparation. Institutional catering across schools, hospitals, universities, and corporate cafeterias is steadily increasing adoption due to scalability, portion control, and ease of service. Travel-related foodservice environments such as airports, railway stations, and highway retail outlets are also contributing to incremental growth, supported by rising mobility, tourism recovery, and demand for portable meal solutions.

Consumer Demographic Insights

Millennials represent the largest consumer demographic, accounting for approximately 39% of global burrito consumption. This leadership is driven by their strong preference for convenience-oriented meals, openness to multicultural cuisines, and high engagement with fast-casual dining formats. Gen Z is the fastest-growing demographic segment, supported by digital-first food ordering behaviors, strong exposure to global food trends through social media, and increasing preference for customizable and visually appealing meals. Generation X maintains steady demand, particularly in household and family consumption contexts where frozen and ready-to-eat formats align with time-saving needs. Baby Boomers contribute stable demand, especially within premium and health-focused product categories that emphasize nutritional balance, portion control, and ease of preparation. Across all demographics, increasing demand for convenience, personalization, and health-oriented ingredients continues to shape consumption patterns and drive product innovation.

Explore more data points, trends and opportunities Download Free Sample Report

Burritos Market Segmentations

By Product Format

- Fresh Prepared Burritos

- Frozen Burritos

- Ready-to-Eat Shelf-Stable Burritos

- Breakfast Burritos

- Snack/Portable Mini Burritos

By Filling Type

- Chicken Burritos

- Beef Burritos

- Pork Burritos

- Seafood Burritos

- Vegetarian Burritos

- Vegan Burritos

- Mixed Protein Burritos

By Consumption Channel

- Quick Service Restaurants (QSR)

- Fast Casual Restaurants

- Full-Service Restaurants

- Institutional Foodservice

- Retail Consumption

By Retail Distribution

- Supermarkets & Hypermarkets

- Convenience Stores

- Club Stores & Cash-and-Carry

- Specialty Food Retailers

- Online Grocery Platforms

By Tortilla Type

- Flour Tortilla Burritos

- Whole Wheat Burritos

- Corn-Based Burritos

- Low-Carb/Keto Burritos

- Gluten-Free Burritos

Regional Insights

North America

North America remains the dominant regional market, accounting for approximately 57% of global burrito demand in 2025. This leadership is strongly supported by deeply rooted Mexican culinary influence, a highly developed fast-casual restaurant ecosystem, and extensive penetration of frozen convenience foods. The United States contributes the majority share of regional consumption, driven by widespread availability across foodservice and retail channels, strong brand presence, and continuous menu innovation. Mexico serves as both a high-consumption domestic market and a key production hub, reinforcing supply chain efficiency and cultural authenticity. Canada is experiencing steady expansion supported by multicultural population trends and increasing adoption of international cuisine. Regional growth is primarily driven by strong cold-chain infrastructure, rising demand for convenience foods, and continuous innovation in both premium and health-oriented burrito formats.

Europe

Europe accounts for approximately 18% of global demand, with growth concentrated in the United Kingdom, Germany, France, Spain, and the Netherlands. The primary growth driver in the region is the increasing consumer shift toward international cuisines combined with fast-paced urban lifestyles that favor convenient meal solutions. The United Kingdom remains the largest European market, supported by high fast-casual restaurant penetration, strong delivery ecosystem development, and increasing retail availability of ready-to-eat Mexican-inspired foods. Western Europe is also witnessing rising demand for premium, organic, and health-focused burrito options, driven by heightened nutritional awareness and demand for clean-label ingredients. Expansion of global food chains and increasing adoption of fusion-style menus further support sustained market penetration across the region.

Asia-Pacific

Asia-Pacific represents approximately 15% of global demand and is projected to be the fastest-growing region through 2031. Growth is primarily driven by rapid urbanization, rising disposable incomes, and increasing exposure to Western dining habits. China, India, Japan, South Korea, and Australia are the key contributing markets, with India expected to exhibit the highest growth rate due to rapid expansion of food delivery platforms and international restaurant chains. The region’s growth is strongly supported by localization strategies that adapt burrito flavors to regional taste preferences, including spice adjustments and ingredient substitutions. Expansion of organized retail, growing youth population, and increasing digital food ordering behavior further accelerate regional adoption of burrito-based meal formats.

Latin America

Latin America accounts for approximately 7% of global revenue, with Mexico serving as both the largest consumer and a key production center. The primary growth driver in the region is the increasing commercialization of Mexican cuisine through modern foodservice formats and rising cross-border culinary influence. Brazil, Chile, Colombia, and Argentina are witnessing steady growth as urban consumers increasingly adopt international fast-casual dining experiences. Expansion of retail infrastructure and growing exposure to global food trends are strengthening demand, while premiumization in urban restaurant segments is gradually reshaping consumption patterns. The region benefits from strong cultural familiarity with core ingredients, which supports sustained long-term growth potential.

Middle East & Africa

The Middle East and Africa region accounts for approximately 3% of global demand, with growth concentrated in the United Arab Emirates, Saudi Arabia, and South Africa. A key growth driver in this region is the high presence of expatriate populations, which supports strong demand for international cuisine, including Mexican-inspired offerings. Tourism development, expansion of modern retail infrastructure, and rapid growth of food delivery platforms further contribute to market expansion. South Africa is emerging as a key growth market due to increasing frozen food penetration and rising urban consumption. Across the region, Western dining influence, hospitality sector growth, and increasing investment in organized foodservice networks continue to support gradual but steady market development.

Key Players in the Burritos Market

- Chipotle Mexican Grill

- Ruiz Foods

- Taco Bell

- Amy's Kitchen

- QDOBA Mexican Eats

- Del Taco

- Freebirds World Burrito

- Barberitos

- Moe's Southwest Grill

- Taco John's

- El Monterey

- Ramona's Mexican Food Products

- Tina's Burritos

- Red's All Natural

- Jose Ole