Body Armor Market Size

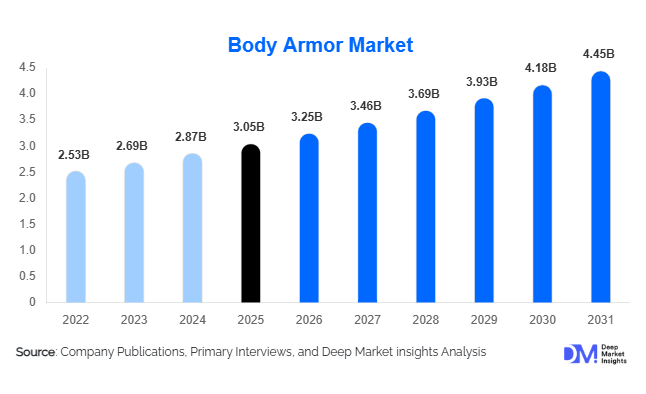

According to Deep Market Insights, the global body armor market size was valued at USD 3.05 billion in 2025 and is projected to grow from USD 3.24 billion in 2026 to reach USD 4.45 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The body armor market growth is primarily driven by rising global defense expenditures, increasing military modernization initiatives, growing demand for lightweight ballistic protection systems, and expanding adoption among law enforcement, homeland security, and private security organizations. Escalating geopolitical tensions, cross-border conflicts, and growing emphasis on soldier survivability are encouraging governments worldwide to invest in advanced personal protective equipment, further supporting market expansion.

Key Market Insights

- Military applications account for more than 50% of global demand, supported by extensive modernization programs and rising defense procurement budgets.

- Hard body armor remains the largest product category, driven by increasing demand for Level III and Level IV ballistic protection against rifle threats.

- North America dominates the global market, led by the United States' substantial investments in military and law enforcement protective equipment.

- Asia-Pacific is the fastest-growing regional market, supported by rising defense spending in China, India, South Korea, Australia, and Japan.

- Advanced materials such as UHMWPE and ceramic composites are transforming product development, enabling lighter and more effective armor solutions.

- Government procurement channels account for the majority of sales, with defense ministries and law enforcement agencies representing the primary customer base.

Body Armor Market Trends

Transition Toward Lightweight Composite Armor Systems

Modern armed forces increasingly prioritize mobility alongside protection, leading to widespread adoption of lightweight body armor solutions. Advanced materials including ultra-high molecular weight polyethylene (UHMWPE), boron carbide ceramics, silicon carbide composites, and hybrid armor systems are replacing traditional steel-based protection. These materials offer superior ballistic resistance while reducing weight, allowing soldiers and tactical personnel to maintain agility during extended operations. Manufacturers are investing heavily in material science innovations to improve protection-to-weight ratios and enhance wearer comfort. The trend is particularly evident in future soldier modernization programs across North America, Europe, and Asia-Pacific, where lightweight armor systems are becoming standard equipment.

Growing Demand for Modular and Mission-Adaptive Protection

Military and law enforcement agencies increasingly seek modular armor platforms that can be configured based on mission requirements. Modular systems allow operators to add or remove armor components, protection plates, and load-bearing equipment according to threat levels and operational environments. This flexibility improves tactical effectiveness while reducing unnecessary weight burdens. Manufacturers are integrating communication systems, power management technologies, and load carriage solutions into body armor platforms, creating multifunctional protection systems. The growing preference for mission-adaptive armor is expected to remain a key product development trend throughout the forecast period.

Body Armor Market Drivers

Increasing Global Defense Expenditure

Growing geopolitical tensions and military modernization initiatives continue to drive body armor procurement worldwide. NATO member countries, the United States, China, India, and Middle Eastern nations have significantly increased defense budgets, with soldier survivability emerging as a strategic priority. Procurement programs focused on upgrading infantry equipment are generating sustained demand for advanced body armor systems. Governments are increasingly allocating funds toward personal protective equipment as part of broader force modernization efforts, creating long-term growth opportunities for manufacturers.

Rising Law Enforcement and Homeland Security Requirements

Law enforcement agencies globally are upgrading protective equipment standards in response to evolving security threats. Increasing incidents involving active shooters, organized crime networks, terrorism, and civil unrest have accelerated adoption of advanced ballistic protection solutions. Tactical response units, border security agencies, and special operations teams require higher levels of protection while maintaining operational mobility. This trend is driving procurement of modern body armor systems across both developed and emerging economies.

Body Armor Market Restraints

High Manufacturing and Certification Costs

The development and production of advanced body armor involve substantial investments in specialized materials, manufacturing processes, and ballistic testing procedures. Compliance with NIJ standards, military specifications, and international certification requirements increases development costs and creates barriers to entry for smaller manufacturers. These high costs can limit market participation and place pressure on procurement budgets, particularly in cost-sensitive regions.

Raw Material Supply Chain Challenges

The body armor industry relies heavily on specialized materials such as aramid fibers, ceramic composites, and UHMWPE. Supply chain disruptions, geopolitical uncertainties, and fluctuations in raw material pricing can affect production schedules and profitability. Limited supplier concentration for critical materials also increases procurement risks for manufacturers, potentially impacting long-term supply stability and pricing competitiveness.

Body Armor Market Opportunities

Expansion of Soldier Modernization Programs

Future soldier programs represent one of the most significant growth opportunities within the body armor market. Governments worldwide are investing in integrated soldier systems that combine protection, communication, situational awareness, and mobility enhancements. Body armor manufacturers capable of supplying lightweight, modular, and technologically advanced systems are well positioned to secure long-term procurement contracts. Emerging defense modernization initiatives in Asia-Pacific, Eastern Europe, and the Middle East are expected to create substantial demand over the next decade.

Growing Demand Beyond Military Applications

The use of body armor is expanding into non-military sectors including private security, critical infrastructure protection, journalism, humanitarian operations, and corporate security services. Rising concerns regarding workplace violence, terrorism, and civil unrest are increasing demand for personal ballistic protection among civilian users. This diversification of end-user demand provides manufacturers with opportunities to develop specialized products tailored to different threat environments and customer requirements.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.05 Billion |

| Market Size in 2026 | USD 3.25 Billion |

| Market Size in 2031 | USD 4.45 Billion |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Hard body armor represents the largest segment of the global market, accounting for approximately 38% of total revenue in 2025. The segment's dominance is attributed to growing demand for protection against high-velocity rifle rounds and armor-piercing threats encountered in modern combat environments. Soft body armor continues to maintain strong adoption among law enforcement agencies due to its flexibility and concealability. Modular body armor systems are experiencing rapid growth as military organizations seek scalable protection platforms capable of adapting to different operational requirements. The increasing integration of hard armor plates with lightweight tactical vests is further supporting product innovation across the industry.

Protection Level Insights

Level IV armor remains the leading protection category, accounting for approximately 26% of the global market in 2025. The segment benefits from increasing military requirements for enhanced protection against armor-piercing ammunition. Level III armor also maintains significant demand among military personnel and tactical law enforcement units due to its balance of protection and weight efficiency. Meanwhile, Level IIIA armor remains widely adopted for concealed law enforcement applications where flexibility and comfort are critical. Rising threat levels across operational environments continue to drive demand for higher-rated ballistic protection systems.

Material Insights

Composite ceramic materials account for nearly 34% of the global body armor market and remain the preferred material category for advanced ballistic protection systems. Boron carbide and silicon carbide ceramics provide exceptional hardness and ballistic resistance while maintaining relatively low weight. UHMWPE materials are witnessing rapid adoption due to their superior strength-to-weight characteristics and increasing use in next-generation armor systems. Aramid fibers continue to play a critical role in soft armor applications, offering durability, flexibility, and proven ballistic performance. Ongoing material innovations are focused on improving survivability while reducing overall equipment burden.

End-User Insights

Defense forces remain the largest end-user segment, accounting for approximately 55% of total market demand in 2025. Military procurement programs continue to drive large-scale adoption of advanced armor systems worldwide. Law enforcement agencies represent the second-largest customer group, supported by ongoing modernization initiatives and evolving operational requirements. Homeland security agencies and border protection forces are increasingly investing in upgraded protective equipment to address emerging security threats. Private security organizations are also contributing to market growth as demand for personal protection expands across commercial and critical infrastructure sectors.

Procurement Channel Insights

Government procurement remains the dominant sales channel, representing approximately 72% of global market revenue. Defense ministries, military organizations, and law enforcement agencies account for the majority of procurement activity through long-term contracts and framework agreements. Direct OEM contracts are becoming increasingly common as governments seek customized solutions tailored to specific operational requirements. Commercial and civilian sales channels continue to expand, particularly in North America, where private security professionals and qualified civilian users contribute to market demand. Strategic partnerships between manufacturers and defense integrators are further strengthening market access opportunities.

Explore more data points, trends and opportunities Download Free Sample Report

Body Armor Market Segmentations

By Product Type

- Soft Body Armor

- Hard Body Armor

- Modular Body Armor Systems

- Load-Bearing Integrated Armor Systems

By Protection Level

- Level IIA

- Level II

- Level IIIA

- Level III

- Level IV

By Material

- Aramid Fiber

- Ultra-High Molecular Weight Polyethylene (UHMWPE)

- Composite Ceramic

- Steel Armor

- Hybrid Composite Materials

By Application

- Military Combat Protection

- Law Enforcement Protection

- Homeland Security & Border Security

- Private Security Services

- Civilian Protection

Regional Insights

North America

North America accounted for approximately 32% of the global body armor market in 2025, making it the largest regional market. The United States dominates regional demand due to its substantial military budget, advanced law enforcement infrastructure, and ongoing investments in soldier modernization programs. Procurement initiatives across the U.S. Department of Defense and federal law enforcement agencies continue to support long-term market growth. Canada also contributes to regional demand through military equipment modernization and homeland security investments.

Europe

Europe represents approximately 24% of the global market, supported by increasing defense expenditures among NATO member states. Germany, France, the United Kingdom, Poland, and Italy are major contributors to regional demand. Ongoing military modernization efforts and heightened security concerns have accelerated procurement of advanced ballistic protection systems. The region is also witnessing growing investment in indigenous defense manufacturing capabilities and next-generation soldier equipment programs.

Asia-Pacific

Asia-Pacific accounted for nearly 30% of global demand in 2025 and is projected to be the fastest-growing regional market through 2031. China and India are driving substantial procurement activity through large-scale military modernization programs and domestic defense manufacturing initiatives. Japan, South Korea, and Australia are also investing heavily in advanced personal protective equipment for military personnel. Increasing regional security concerns and defense budget expansion continue to create favorable growth conditions across the region.

Latin America

Latin America represents a smaller but steadily growing market, led by Brazil and Mexico. Demand is primarily driven by law enforcement modernization, border security requirements, and increasing adoption of ballistic protection among security personnel. Government efforts to combat organized crime and improve public safety are supporting continued investment in protective equipment.

Middle East & Africa

The Middle East & Africa region accounts for approximately 9% of global demand, with Saudi Arabia, the United Arab Emirates, Israel, and South Africa representing key markets. Regional defense modernization programs, border security initiatives, and geopolitical tensions continue to drive procurement of advanced body armor systems. Israel remains a significant technology innovator within the sector, while Gulf Cooperation Council countries continue investing heavily in military modernization efforts.

Key Players in the Body Armor Market

- Point Blank Enterprises

- BAE Systems

- Safariland Group

- ArmorSource

- MKU Limited

- Avon Technologies

- Rheinmetall AG

- Elmon SA

- US Armor Corporation

- Craig International Ballistics

- Mehler Systems

- Protection Group Danmark

- VestGuard UK

- Survitec Group

- Sarkar Tactical