Bagasse Products Market Size

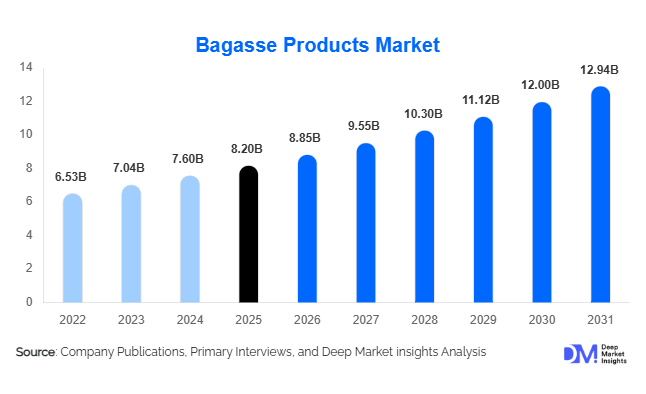

According to Deep Market Insights, the global bagasse products market size was valued at USD 8.2 billion in 2025 and is projected to grow from USD 8.85 billion in 2026 to reach USD 12.94 billion by 2031, expanding at a CAGR of 7.9% during the forecast period (2026–2031). The bagasse products market growth is primarily driven by increasing restrictions on single-use plastics, growing consumer preference for biodegradable packaging materials, and expanding adoption of sustainable foodservice packaging solutions across restaurants, catering services, retail chains, and food delivery platforms. Derived from sugarcane fiber residue, bagasse has emerged as one of the most commercially viable alternatives to petroleum-based packaging materials due to its compostability, renewable sourcing, and favorable environmental profile.

Key Market Insights

- Global regulations restricting single-use plastics are accelerating bagasse product adoption across foodservice, retail packaging, and institutional applications.

- Foodservice and restaurant applications account for the largest share of demand, supported by rapid expansion of food delivery and takeaway services.

- Asia-Pacific dominates the global market, benefiting from abundant sugarcane production, low manufacturing costs, and growing domestic consumption.

- North America represents the largest importing region, driven by stringent sustainability regulations and corporate ESG commitments.

- Molded fiber technology advancements are improving product quality, enabling superior moisture resistance, durability, and heat tolerance.

- Industrial packaging applications are emerging as a high-growth segment, replacing EPS foam and plastic protective packaging across consumer goods industries.

Bagasse Products Market Trends

Transition Toward Sustainable Packaging Solutions

The global packaging industry is undergoing a significant transformation as businesses increasingly replace conventional plastics with biodegradable alternatives. Bagasse-based packaging products are benefiting from this trend due to their renewable origin, compostability, and compatibility with circular economy objectives. Major restaurant chains, retailers, and food manufacturers are incorporating bagasse containers, trays, bowls, and plates into their sustainability programs. Governments worldwide are further supporting adoption through bans on plastic cutlery, foam containers, and single-use packaging materials. As environmental awareness continues to rise among consumers, demand for eco-friendly packaging is expected to remain a key growth driver throughout the forecast period.

Technological Advancements in Molded Fiber Manufacturing

Manufacturers are investing heavily in advanced molded fiber technologies to improve product functionality and production efficiency. Modern thermoforming processes enable the production of premium-quality bagasse products with enhanced strength, improved aesthetics, and better resistance to heat, grease, and moisture. Automation technologies are also helping manufacturers increase production capacity while reducing operating costs. Innovations in bio-based coatings and PFAS-free barrier technologies are further expanding the application scope of bagasse products into premium food packaging and industrial protective packaging segments.

Bagasse Products Market Drivers

Global Plastic Ban Regulations

One of the strongest growth drivers for the bagasse products market is the implementation of regulations restricting single-use plastics. Countries across Europe, North America, Asia-Pacific, and Latin America have introduced legislation aimed at reducing plastic waste generation. These regulations are creating substantial opportunities for biodegradable alternatives such as bagasse packaging. Public institutions, educational facilities, airports, and government agencies are increasingly adopting compostable foodservice products, creating stable long-term demand for manufacturers.

Growth of Food Delivery and Takeaway Services

The rapid expansion of food delivery platforms and takeaway dining models has significantly increased demand for sustainable packaging solutions. Restaurants require containers capable of maintaining food quality while complying with evolving environmental standards. Bagasse products offer excellent thermal insulation, durability, and grease resistance, making them particularly suitable for meal delivery applications. The continued growth of online food ordering platforms is expected to generate substantial demand for bagasse containers and clamshell packaging throughout the forecast period.

Bagasse Products Market Restraints

Feedstock Supply Volatility

The availability of bagasse raw material is closely linked to sugarcane production cycles and agricultural output. Weather-related disruptions, changing sugar production economics, and regional crop variations can affect feedstock availability and pricing. These fluctuations create challenges for manufacturers seeking stable production costs and long-term supply agreements.

Price Competition from Conventional Packaging Materials

Although bagasse products have become increasingly cost competitive, they generally remain more expensive than conventional plastic alternatives. In price-sensitive markets, adoption can be constrained by higher upfront costs, particularly where environmental regulations remain limited. Manufacturers must continue improving production efficiency and economies of scale to narrow the cost gap and support broader market penetration.

Bagasse Products Market Opportunities

Expansion into Industrial Packaging Applications

Industrial packaging represents one of the most promising growth opportunities for bagasse product manufacturers. Electronics companies, cosmetics brands, pharmaceutical manufacturers, and consumer appliance producers are increasingly replacing plastic and EPS foam inserts with molded fiber packaging solutions. These applications offer higher value-added opportunities compared to traditional foodservice products while aligning with corporate sustainability objectives.

Vertical Integration with Sugar Industry Operations

Sugar-producing countries such as India, Brazil, Thailand, China, and Pakistan generate significant quantities of bagasse annually. Manufacturers that establish vertically integrated operations near sugar mills can reduce raw material costs, improve supply chain security, and strengthen profitability. This model also supports circular economy initiatives and attracts government incentives focused on agricultural waste utilization.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.2 Billion |

| Market Size in 2026 | USD 8.85 Billion |

| Market Size in 2031 | USD 12.94 Billion |

| CAGR | 7.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Plates represent the largest product segment, accounting for approximately 24% of the global market in 2025. Their widespread use across restaurants, catering services, institutional foodservice facilities, and event management applications continues to support strong demand. Compartment plates have experienced particularly strong growth due to increasing adoption in meal delivery and cafeteria services. Clamshell containers represent one of the fastest-growing product categories, benefiting from rising food delivery demand and growing adoption among quick-service restaurants. Bowls and food containers are also witnessing significant growth as operators seek sustainable alternatives for takeaway meals, soups, and ready-to-eat food packaging.

Manufacturing Process Insights

Molded fiber thermoforming dominates the market with an estimated 42% share of global revenues. The technology provides superior product quality, smooth surface finishes, and enhanced structural integrity compared to traditional pulp molding methods. Wet press molding continues to gain traction in premium packaging applications due to its ability to produce aesthetically appealing products with improved strength characteristics. Dry press molding remains widely used in cost-sensitive markets because of its lower capital investment requirements and high-volume production capabilities.

End-Use Industry Insights

Foodservice and restaurant applications account for approximately 39% of total market demand, making them the largest end-use segment globally. Quick-service restaurant chains, institutional cafeterias, catering providers, and hospitality operators continue to drive consumption. Food delivery platforms are emerging as the fastest-growing end-use category due to increasing consumer preference for convenient dining solutions. Industrial packaging applications are gaining momentum as manufacturers seek environmentally friendly protective packaging materials. Agriculture and horticulture sectors are also increasingly adopting bagasse trays and biodegradable packaging solutions for produce handling and plant cultivation applications.

Distribution Channel Insights

Direct B2B sales account for more than 50% of global market revenues, reflecting the importance of large procurement contracts with restaurant chains, institutional buyers, and packaging distributors. Foodservice wholesalers remain important distribution partners, particularly in North America and Europe. E-commerce channels are experiencing rapid growth as small businesses and independent foodservice operators increasingly purchase sustainable packaging products through digital platforms. Retail channels continue to expand as consumer awareness of compostable tableware products increases.

Explore more data points, trends and opportunities Download Free Sample Report

Bagasse Products Market Segmentations

By Product Type

- Plates

- Bowls

- Trays

- Clamshell Containers

- Food Containers

- Cups & Drinkware

- Cutlery

- Packaging Products

- Others

By Manufacturing Process

- Molded Fiber Thermoforming

- Wet Press Molding

- Dry Press Molding

- Pulp Molding

- Hybrid Fiber Processing

By Coating Type

- Uncoated Bagasse Products

- Water-Based Coated Products

- Bio-Polymer Coated Products

- Oil & Grease Resistant Coated Products

By End-Use Industry

- Foodservice & Restaurants

- Quick Service Restaurants (QSRs)

- Catering Services

- Hotels & Hospitality

- Institutional Food Services

- Retail & Supermarkets

- Food Delivery Platforms

- Consumer Household Use

- Industrial Packaging

- Agriculture & Horticulture

By Distribution Channel

- Direct B2B Sales

- Packaging Distributors

- Foodservice Wholesalers

- Retail Stores

- E-Commerce Platforms

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 41% of the global bagasse products market in 2025, making it the largest regional market and the primary manufacturing hub for bagasse-based packaging products worldwide. China and India collectively account for the majority of regional production and consumption, supported by abundant sugarcane availability, low-cost manufacturing infrastructure, and favorable government policies promoting sustainable packaging alternatives. China remains the largest producer of molded fiber packaging products, benefiting from large-scale manufacturing ecosystems, strong export capabilities, and increasing domestic demand following restrictions on single-use plastics. India has emerged as one of the fastest-growing markets globally, driven by nationwide bans on selected plastic products, government initiatives promoting biodegradable materials, and the availability of substantial sugarcane feedstock from the country's extensive sugar industry.

Regional growth is further supported by rapid expansion of food delivery services, quick-service restaurant chains, and organized retail sectors across China, India, Indonesia, Vietnam, Thailand, and the Philippines. Increasing urbanization and rising middle-class consumption are accelerating demand for eco-friendly takeaway packaging solutions. Thailand and Vietnam are strengthening their positions as major export-oriented manufacturing hubs, supplying sustainable packaging products to North America and Europe. Additionally, growing investments in molded fiber production facilities, automation technologies, and circular economy initiatives are expected to reinforce Asia-Pacific's leadership position throughout the forecast period. The region is projected to remain the fastest-growing market globally, supported by a CAGR exceeding the global average.

North America

North America represented approximately 28% of global bagasse products market revenues in 2025, making it the second-largest regional market. The United States accounts for the majority of regional demand and remains the largest country-level consumer globally. Market growth is being driven by aggressive sustainability commitments from multinational foodservice operators, retail chains, educational institutions, healthcare facilities, and corporate campuses. Increasing adoption of compostable food packaging across airports, universities, stadiums, and government facilities continues to create substantial demand for bagasse products.

A key growth driver in North America is the strengthening regulatory landscape surrounding plastic waste reduction. Several U.S. states, including California, New York, Washington, and Colorado, have implemented restrictions on single-use plastics and expanded producer responsibility programs, encouraging businesses to transition toward compostable alternatives. Canada is also witnessing strong growth due to nationwide initiatives targeting plastic pollution and increasing corporate ESG compliance requirements. The rapid expansion of food delivery platforms and meal-preparation services has further accelerated demand for compostable containers, bowls, and clamshell packaging. Growing consumer willingness to pay a premium for sustainable products, coupled with rising investments in composting infrastructure, is expected to support long-term market expansion across the region.

Europe

Europe accounted for approximately 22% of global demand in 2025 and represents one of the most regulation-driven markets for bagasse products. The implementation of the European Union Single-Use Plastics Directive has significantly accelerated the transition toward biodegradable and compostable packaging materials. Germany, France, the United Kingdom, Italy, Spain, and the Netherlands are among the leading consumers of bagasse-based foodservice and retail packaging products. Strong environmental awareness among consumers and businesses continues to drive adoption across multiple end-use industries.

The primary growth driver for the European market is the region's commitment to circular economy objectives and carbon reduction targets. Governments are actively encouraging the use of renewable and compostable materials through regulatory mandates, taxation of plastic packaging, and sustainable procurement policies. Major restaurant chains, supermarkets, coffee chains, and food manufacturers are increasingly replacing plastic packaging with bagasse alternatives to meet sustainability commitments and comply with evolving regulations. Growth is also supported by expanding organic food sectors, rising demand for sustainable takeaway packaging, and increasing investments in industrial composting infrastructure. Germany remains the largest market within Europe due to its advanced waste management systems and strong environmental regulations, while France and the United Kingdom continue to witness rapid adoption among foodservice operators and retailers.

Latin America

Latin America contributes approximately 6% of global market revenues, with Brazil representing the largest market within the region. The region benefits from significant sugarcane production, providing abundant availability of bagasse feedstock for manufacturing applications. Brazil's well-established sugar and ethanol industries create favorable conditions for the development of integrated bagasse packaging production facilities. The country is increasingly utilizing agricultural waste streams to support sustainable manufacturing and circular economy initiatives.

Market growth across Latin America is being driven by rising environmental awareness, gradual implementation of plastic reduction policies, and increasing investments in sustainable packaging solutions by multinational foodservice and consumer goods companies. Mexico is witnessing growing demand from restaurant chains, food delivery providers, and retail packaging applications, while Chile and Colombia continue to strengthen environmental regulations aimed at reducing plastic waste. Export opportunities also represent a significant growth driver, as regional manufacturers seek to supply sustainable packaging products to North American and European markets. Although adoption rates remain lower than in developed regions, increasing regulatory support and expanding foodservice industries are expected to accelerate market growth over the coming years.

Middle East & Africa

The Middle East & Africa region accounted for approximately 3% of global market demand in 2025. While currently representing the smallest regional market, it is emerging as a promising growth area due to increasing sustainability initiatives and expanding hospitality sectors. The United Arab Emirates, Saudi Arabia, South Africa, and Qatar are among the leading markets within the region. Growing investments in tourism infrastructure, hospitality developments, and large-scale events are generating increasing demand for environmentally friendly foodservice packaging products.

A major driver for regional growth is the implementation of sustainability agendas across Gulf Cooperation Council (GCC) countries. Government-led environmental programs, including Saudi Vision 2031 and the UAE's sustainability initiatives, are encouraging businesses to reduce dependence on single-use plastics and adopt biodegradable alternatives. The hospitality, aviation, catering, and quick-service restaurant sectors are increasingly incorporating compostable packaging into their operations. In Africa, South Africa remains the most developed market, supported by growing consumer awareness and increasing adoption of sustainable packaging across retail and foodservice industries. Rising urbanization, expanding tourism activities, and infrastructure investments across the Middle East are expected to create substantial long-term growth opportunities for bagasse product manufacturers throughout the forecast period.

Key Players in the Bagasse Products Market

- Huhtamaki

- Duni Group

- Pactiv Evergreen

- Genpak

- World Centric

- Eco-Products

- Dart Container Corporation

- Vegware

- Sabert Corporation

- GreenGood USA

- BioPak

- Ecoware

- Pappco Greenware

- Pakka Limited

- Detpak