Baby Rice Cereal Market Size

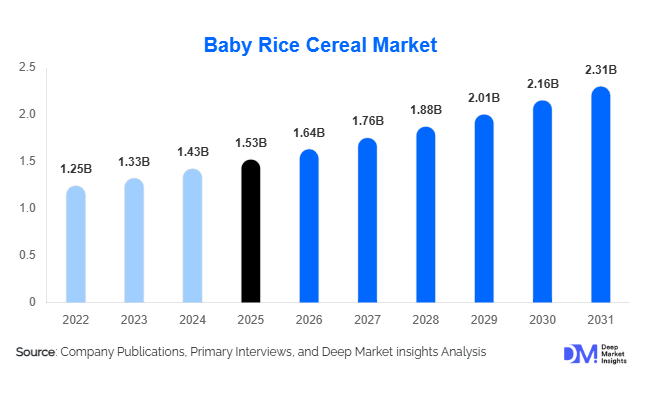

According to Deep Market Insights, the global baby rice cereal market size was valued at USD 1.53 billion in 2025 and is projected to grow from USD 1.64 billion in 2026 to reach USD 2.31 billion by 2031, expanding at a CAGR of 7.1% during the forecast period (2026–2031). The baby rice cereal market growth is primarily driven by increasing awareness regarding infant nutrition, rising demand for fortified complementary foods, expanding urban populations, and growing parental preference for convenient and scientifically formulated infant feeding products. The market continues to benefit from increasing adoption of premium infant nutrition products, particularly in Asia-Pacific and North America, where parents are actively seeking organic, clean-label, and micronutrient-enriched baby cereals that support healthy growth and development during infancy.

Key Market Insights

- Fortified baby rice cereals account for over 40% of global revenue, driven by increasing demand for iron-enriched and vitamin-fortified infant nutrition products.

- Asia-Pacific dominates the global market, supported by large infant populations, increasing disposable incomes, and growing penetration of branded baby foods.

- Organic baby rice cereals are among the fastest-growing product categories, benefiting from rising consumer preference for clean-label and chemical-free infant nutrition.

- Online retail channels continue gaining market share, enabling parents to access premium domestic and imported infant cereal products.

- Functional nutrition innovation is accelerating, with manufacturers introducing probiotics, prebiotics, DHA, and digestive health ingredients into cereal formulations.

- Food safety and traceability have become major purchasing criteria, encouraging investments in advanced sourcing, testing, and quality assurance systems.

Baby Rice Cereal Market Latest Trends

Premium and Organic Infant Nutrition Gaining Momentum

The baby rice cereal industry is experiencing substantial premiumization as parents increasingly prioritize product quality, ingredient transparency, and nutritional value. Organic rice cereals are witnessing strong demand across North America, Europe, China, Australia, and urban centers in emerging economies. Consumers are increasingly willing to pay premium prices for products carrying organic certifications, non-GMO claims, and clean-label positioning. Manufacturers are responding by investing in certified organic rice supply chains and introducing cereals with minimal ingredients, free from artificial preservatives, flavors, and sweeteners. Premium infant cereals are increasingly positioned around digestive health, immune support, and cognitive development, contributing to higher average selling prices and improved manufacturer margins.

Functional Fortification Transforming Product Innovation

Product innovation is increasingly centered on enhanced nutritional functionality. Baby rice cereal manufacturers are introducing products fortified with iron, zinc, calcium, vitamin D, omega-3 fatty acids, probiotics, and prebiotics to address infant nutritional deficiencies and support developmental outcomes. Iron-fortified cereals remain particularly important due to pediatric recommendations aimed at preventing iron deficiency during infancy. Companies are also investing in clinically supported ingredients that promote gut health and immune function. The trend toward personalized infant nutrition is encouraging manufacturers to develop age-specific formulations targeting distinct developmental stages from 4 months through 24 months of age.

Baby Rice Cereal Market Drivers

Growing Awareness of Infant Nutritional Requirements

Global awareness regarding infant nutrition has increased significantly over the past decade. Healthcare providers, pediatric associations, and public health agencies increasingly emphasize the importance of nutrient-rich complementary foods after six months of age. Baby rice cereals continue to serve as one of the most recommended introductory solid foods because of their digestibility, mild taste profile, and nutritional fortification potential. Rising educational campaigns focused on infant health are contributing to higher adoption rates of fortified cereal products globally.

Increasing Female Workforce Participation and Demand for Convenience

The increasing participation of women in the workforce has significantly influenced infant feeding patterns. Working parents increasingly seek convenient feeding solutions that reduce preparation time while maintaining nutritional quality. Baby rice cereals offer a practical solution through ease of preparation, consistent nutritional content, and portability. Urban households, dual-income families, and working professionals represent major consumer groups driving category expansion. The convenience factor remains particularly important in emerging economies undergoing rapid urbanization.

Expansion of Premium and Functional Baby Food Categories

The growth of premium infant nutrition segments has created strong demand for fortified and specialty baby rice cereals. Parents increasingly prefer products containing essential micronutrients, probiotics, DHA, and other developmental ingredients. Premium products addressing digestive health, immunity, and cognitive development are achieving higher growth rates than traditional cereal offerings. This trend is particularly visible in developed economies and upper-income households across emerging markets, supporting long-term value growth within the category.

Baby Rice Cereal Market Restraints

Arsenic and Heavy Metal Concerns in Rice-Based Products

Rice-based infant products periodically face scrutiny regarding arsenic and heavy metal content. Regulatory agencies across North America, Europe, and Asia have implemented stricter standards governing contaminant levels in infant foods. Compliance requires substantial investments in sourcing controls, laboratory testing, and quality assurance programs. Consumer concerns regarding product safety can temporarily affect purchasing behavior and increase operational costs for manufacturers.

Declining Birth Rates in Developed Economies

Several developed economies including Japan, South Korea, Germany, Italy, and parts of North America continue to experience declining birth rates. Lower infant populations directly impact category volume growth, forcing manufacturers to rely on premiumization and product innovation to sustain revenue expansion. The demographic challenge remains one of the most significant long-term constraints affecting mature infant nutrition markets.

Baby Rice Cereal Industry Key Opportunities

Expansion of Organic and Clean-Label Product Portfolios

Organic baby rice cereal remains underpenetrated across many developing economies despite growing consumer interest in chemical-free and sustainably sourced foods. Manufacturers capable of developing reliable organic supply chains and obtaining international certifications can capitalize on premium pricing opportunities. The organic segment is expected to outperform conventional products throughout the forecast period, supported by increasing awareness of food safety and ingredient transparency among millennial parents.

Rapid Growth Across Emerging Asia-Pacific Markets

Asia-Pacific presents the largest growth opportunity for market participants. Countries including India, Indonesia, Vietnam, Philippines, and China continue to witness rising spending on infant nutrition products. Growing middle-class populations, urbanization, increasing female employment, and improved retail infrastructure are creating favorable conditions for branded baby cereal adoption. Localized formulations, culturally relevant product positioning, and digital retail strategies will remain key success factors for market expansion.

Advanced Functional Nutrition and Clinical Positioning

Manufacturers have significant opportunities to develop clinically supported baby rice cereals targeting immunity, digestive health, brain development, and micronutrient supplementation. Products incorporating probiotics, prebiotics, omega fatty acids, and bioavailable minerals can command premium pricing and strengthen brand differentiation. As consumers increasingly seek scientifically validated infant nutrition products, evidence-based innovation is expected to become a major competitive advantage across global markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.53 Billion |

| Market Size in 2026 | USD 1.64 Billion |

| Market Size in 2031 | USD 2.31 Billion |

| CAGR | 7.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Fortified rice cereals remain the largest product segment in the global baby rice cereal market, accounting for approximately 41% of total market revenue in 2025. The segment’s leadership is primarily driven by growing pediatric recommendations emphasizing iron-fortified complementary foods to address infant micronutrient deficiencies, particularly iron deficiency anemia during the first year of life. Increasing awareness among parents regarding the importance of early-life nutrition, combined with government-backed nutritional guidelines in several countries, continues to strengthen demand for fortified formulations. Manufacturers are further enhancing product appeal through the incorporation of additional vitamins, minerals, probiotics, and functional ingredients that support immunity, cognitive development, and digestive health.Single-grain rice cereals continue to represent a foundational category within infant nutrition due to their high digestibility, mild taste profile, and low allergenic potential. These products are widely recommended as first complementary foods for infants transitioning from exclusive breastfeeding or formula feeding. Multi-grain variants are gaining momentum as infants progress through developmental feeding stages and parents seek broader nutritional diversity, improved texture experiences, and enhanced nutrient density. At the same time, specialty baby rice cereals, including organic, gluten-free, non-GMO, hypoallergenic, and clean-label formulations, are emerging as the fastest-growing product category. Rising premiumization trends, increasing demand for minimally processed foods, and heightened consumer scrutiny of ingredient sourcing continue to accelerate adoption across developed and emerging markets.

Ingredient Source Insights

Conventional baby rice cereals account for approximately 72% of global market revenue in 2025, maintaining a dominant position due to their affordability, extensive retail penetration, and broad consumer accessibility. The segment continues to benefit from established manufacturing infrastructure, large-scale agricultural supply chains, and strong brand recognition across both developed and developing economies. Conventional products remain particularly important in price-sensitive markets where affordability significantly influences purchasing decisions.Despite the dominance of conventional offerings, organic baby rice cereals are experiencing considerably faster growth and steadily increasing their market share. The primary driver supporting the organic segment is rising consumer concern regarding pesticide residues, artificial additives, genetically modified ingredients, and long-term environmental sustainability. Parents are increasingly seeking products perceived as safer, cleaner, and more natural for infant consumption. Demand is particularly strong in North America, Western Europe, Australia, Japan, and major metropolitan areas across China, where premium consumers demonstrate a greater willingness to pay for certified organic infant nutrition products. In response, manufacturers are expanding organic sourcing networks, investing in certification programs, and strengthening clean-label product portfolios to capitalize on evolving consumer preferences.

Age Group Insights

Stage 2 products targeting infants aged 6–12 months represent the largest age-group segment, accounting for approximately 49% of global market revenue in 2025. The segment’s dominance is primarily driven by the critical complementary feeding phase during which infant cereals become a major source of nutrition alongside breast milk or infant formula. During this developmental stage, infants require increased intake of iron, vitamins, minerals, and energy to support rapid physical growth, cognitive development, and immune system maturation. Consequently, demand for nutrient-dense fortified cereals remains particularly strong among caregivers and healthcare professionals.Stage 1 products designed for infants aged 4–6 months continue to play a vital role as introductory feeding solutions, benefiting from their simple formulations and suitability for first-time complementary feeding experiences. Meanwhile, Stage 3 products targeting toddlers aged 12–24 months are increasingly benefiting from premiumization trends and product innovation. Manufacturers are introducing age-specific formulations containing added proteins, fibers, probiotics, fruits, vegetables, and developmental nutrients to address evolving nutritional requirements. As parents increasingly seek personalized nutrition solutions throughout infancy and early childhood, companies continue expanding their stage-based product portfolios to support growth opportunities across all developmental categories.

Packaging Type Insights

Boxes and cartons remain the leading packaging format within the baby rice cereal market, accounting for approximately 44% of global sales in 2025. The segment's leadership is supported by cost efficiency, strong shelf visibility, ease of storage, and compatibility with dry cereal products. Manufacturers continue to favor carton-based packaging due to its ability to provide effective branding opportunities while maintaining competitive production costs. The widespread availability of carton-packaged products across supermarkets, hypermarkets, and convenience retail channels further reinforces segment dominance.Flexible pouches are witnessing accelerated adoption as modern consumers increasingly prioritize convenience, portability, and ease of use. These formats are particularly attractive for busy households seeking travel-friendly feeding solutions. Premium manufacturers are also investing in resealable packaging technologies that enhance product freshness, reduce food waste, and improve consumer convenience. In addition, sustainability considerations are becoming increasingly important across packaging decisions. Growing environmental awareness among consumers and tightening packaging regulations are encouraging manufacturers to incorporate recyclable materials, reduced-plastic designs, and environmentally responsible packaging innovations into their product strategies.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate global distribution, contributing approximately 38% of total market revenue in 2025. The segment’s leadership is primarily driven by extensive product assortments, strong consumer trust, competitive pricing strategies, and the ability to offer one-stop shopping convenience for families. Large retail chains provide manufacturers with significant shelf visibility, promotional opportunities, and broad geographic reach, making them the preferred channel for mass-market baby cereal distribution.Online retail represents the fastest-growing distribution channel, supported by the rapid expansion of e-commerce ecosystems, increasing digital literacy, and changing consumer purchasing behaviors. Parents increasingly value the convenience of home delivery, product comparisons, subscription-based purchasing programs, and access to premium or niche infant nutrition products unavailable in traditional retail stores. Pharmacies and specialty baby stores continue to maintain a strong market presence due to their association with healthcare credibility, expert guidance, and premium product offerings. At the same time, direct-to-consumer channels are gaining importance as manufacturers strengthen digital engagement strategies, leverage personalized marketing initiatives, and establish closer relationships with consumers.

Price Positioning Insights

The mid-priced segment leads the global baby rice cereal market, accounting for approximately 47% of total revenue in 2025. The segment’s dominance is primarily driven by growing consumer demand for products that effectively balance affordability, nutritional quality, and brand trust. Across both developed and emerging economies, middle-income households increasingly seek value-oriented infant nutrition products that provide essential fortification and quality assurance without premium-level pricing. This balance between accessibility and perceived quality continues to position the mid-priced category as the preferred choice among a broad consumer base.Premium and super-premium segments are expanding at a faster pace than the overall market, supported by increasing demand for organic ingredients, advanced fortification technologies, clean-label formulations, and specialized developmental health benefits. Consumers are increasingly willing to pay higher prices for products perceived to offer superior safety, transparency, and nutritional value. Meanwhile, economy-priced products remain essential in developing regions where affordability remains a key purchasing determinant. Manufacturers continue to optimize product portfolios across multiple price tiers to address diverse consumer income levels and evolving nutritional preferences.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Rice Cereal Market Segmentations

By Product Type

- Single-Grain Rice Cereal

- Multi-Grain Rice-Based Cereal

- Fortified Rice Cereal

- Specialty Rice Cereal

By Ingredient Source

- Conventional

- Organic

By Age Group

- Stage 1

- Stage 2

- Stage 3

By Packaging Type

- Boxes/Cartons

- Pouches

- Cans/Tins

- Cups & Ready-to-Eat Containers

By Form

- Dry Powder Cereal

- Instant Mix Cereal

- Ready-to-Eat Rice Cereal

Regional Insights

Asia-Pacific

Asia-Pacific represents the largest regional market, accounting for approximately 39% of global demand in 2025. The region’s leadership is supported by its large infant population, expanding middle-class consumer base, rising disposable incomes, and increasing awareness regarding infant nutrition and early childhood development. China contributes nearly 15% of global consumption and remains a key revenue-generating market due to strong demand for premium, imported, and scientifically formulated infant nutrition products. India accounts for approximately 9% of global demand and remains the fastest-growing national market, benefiting from improving maternal education levels, growing urbanization, expanding organized retail networks, and increasing government focus on child nutrition programs.Additional growth across the region is being supported by rising female workforce participation, growing adoption of packaged infant foods, expanding e-commerce penetration, and greater healthcare professional involvement in complementary feeding recommendations. Countries including Japan, South Korea, Indonesia, Vietnam, and Australia continue contributing significantly to regional growth through premium product adoption, innovation in infant nutrition, and expanding retail accessibility. Furthermore, increasing demand for fortified, organic, and clean-label baby cereals is creating substantial opportunities for manufacturers throughout the region.

North America

North America accounts for approximately 28% of global market revenue, led primarily by the United States. The region benefits from high consumer awareness regarding infant nutrition, strong purchasing power, and widespread adoption of premium baby food products. Demand remains concentrated in fortified, organic, non-GMO, and clean-label formulations as parents increasingly prioritize ingredient transparency, nutritional functionality, and stringent food safety standards.The primary growth drivers in North America include rising demand for premium infant nutrition, increasing preference for organic products, expanding e-commerce sales, and continuous product innovation focused on developmental health benefits. Strong healthcare guidance regarding complementary feeding practices, advanced retail infrastructure, and widespread availability of specialized infant nutrition products further support market expansion. In addition, growing consumer interest in sustainability, traceable ingredient sourcing, and environmentally responsible packaging continues to shape purchasing behavior across the region.

Europe

Europe represents approximately 22% of global demand, with Germany, the United Kingdom, France, Italy, and Spain serving as major consumption centers. The region remains one of the most mature infant nutrition markets globally, characterized by strict regulatory standards, strong consumer trust in premium products, and widespread adoption of organic infant food solutions. Organic baby rice cereals have achieved particularly strong market penetration throughout Western Europe, where consumers place significant emphasis on food quality and safety.Although declining birth rates continue to moderate volume growth across several European countries, market value expansion remains supported by premiumization trends and growing consumer willingness to invest in higher-quality infant nutrition products. Key growth drivers include increasing demand for organic and clean-label products, heightened focus on sustainability and traceability, expanding adoption of functional ingredients, and ongoing innovation in premium formulations. Environmental consciousness and stringent regulatory oversight continue to encourage manufacturers to develop products aligned with evolving consumer expectations.

Latin America

Latin America accounts for approximately 6% of global demand, with Brazil and Mexico representing the region’s largest markets. Demand is supported by growing urban populations, improving economic conditions, and increasing awareness regarding infant health and nutrition. Rising household incomes and the expansion of modern retail infrastructure are enabling greater accessibility to packaged baby food products across major urban centers.The region’s growth is being driven by increasing female workforce participation, rising adoption of convenient packaged nutrition products, expanding supermarket and e-commerce distribution networks, and greater consumer awareness of complementary feeding practices. While premium product penetration remains relatively lower than in developed markets, demand for fortified and premium baby cereals is gradually increasing among middle-income consumers seeking improved nutritional solutions for infants. Manufacturers continue to view the region as an important long-term growth opportunity due to favorable demographic fundamentals and ongoing retail modernization.

Middle East & Africa

The Middle East and Africa collectively contribute approximately 5% of global market revenue. Major markets include Saudi Arabia, the United Arab Emirates, South Africa, Egypt, and Nigeria. The region is characterized by a growing infant population, improving healthcare infrastructure, and increasing awareness regarding child nutrition. Demand for baby rice cereals continues to strengthen as parents increasingly recognize the importance of fortified complementary foods during early childhood development.Key growth drivers include rising household incomes, increasing healthcare expenditures, expanding urbanization, improving retail accessibility, and government initiatives focused on maternal and child health. Gulf Cooperation Council countries continue to demonstrate strong demand for imported premium infant nutrition products, supported by relatively high purchasing power and premium consumer preferences. Across Africa, gradual improvements in local manufacturing capabilities, expanding distribution networks, and growing awareness of infant nutritional requirements are creating favorable conditions for long-term market expansion.

Key Players in the Baby Rice Cereal Market

- Nestlé

- Danone

- Kraft Heinz

- HiPP

- Bellamy's Organic

- Abbott Laboratories

- Beingmate

- Yili Group

- Feihe International

- The Hain Celestial Group

- Hero Group

- Bubs Australia

- Little Freddie

- Holle Baby Food

- Plum Organics