Milk Powder Market Size

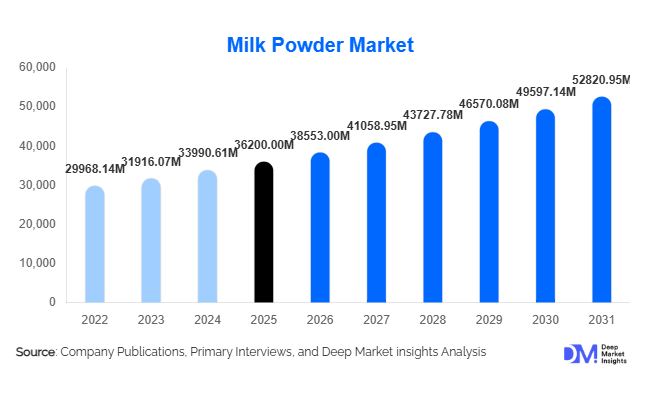

According to Deep Market Insights, the global milk powder market size was valued at USD 36,200 million in 2025 and is projected to grow from USD 38,553.00 million in 2026 to reach USD 52,820.95 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The milk powder market growth is primarily driven by increasing demand for shelf-stable dairy products, expanding food processing industries, and rising consumption of nutritional and fortified dairy products worldwide. The versatility of milk powder across applications such as bakery, confectionery, infant nutrition, and beverages continues to strengthen its global demand. Additionally, the growing need for long shelf-life dairy solutions in regions with limited cold-chain infrastructure further supports market expansion. Emerging economies in Asia-Pacific and Africa are witnessing rapid adoption due to urbanization, population growth, and increasing disposable incomes, positioning milk powder as a critical dairy commodity in global food supply chains.

Key Market Insights

- Milk powder demand is increasingly driven by food processing industries, particularly in bakery, confectionery, and ready-to-drink beverages.

- Infant nutrition and clinical nutrition segments are experiencing rapid growth, supported by rising health awareness and demographic shifts.

- Asia-Pacific dominates the global milk powder market due to high population and increasing dairy consumption in China and India.

- Middle East & Africa is the fastest-growing region, driven by import dependency and rising urban demand.

- Specialty milk powders, including lactose-free and protein-fortified variants, are gaining traction among health-conscious consumers.

- Technological advancements in spray drying and fortification are improving product quality and expanding application scope.

What are the latest trends in the milk powder market?

Rising Demand for Functional and Fortified Milk Powders

The global market is witnessing a strong shift toward functional dairy products, with consumers increasingly seeking milk powders enriched with vitamins, minerals, and protein. Products such as lactose-free, organic, and high-protein milk powders are gaining popularity among health-conscious consumers and individuals with dietary restrictions. This trend is particularly prominent in developed markets, where consumers prioritize nutritional benefits and clean-label products. Manufacturers are also introducing customized formulations targeting specific demographics such as children, athletes, and elderly populations, further expanding the market scope.

Expansion of Global Dairy Trade and Export-Oriented Production

Milk powder plays a central role in global dairy trade due to its ease of transport and extended shelf life. Export-oriented production hubs in regions such as Europe and Oceania are expanding capacity to meet rising demand from import-dependent countries in Asia and Africa. Countries like China, Algeria, and Indonesia are among the largest importers, driving international trade volumes. This trend is further supported by trade agreements, improved logistics, and investments in dairy infrastructure, enabling efficient cross-border supply chains.

What are the key drivers in the milk powder market?

Growth in Food Processing Industry

The increasing demand for processed and convenience foods is a major driver for milk powder consumption. It serves as a key ingredient in bakery, confectionery, and beverage applications due to its stability and functional properties. Rapid urbanization and changing lifestyles have significantly boosted the consumption of ready-to-eat and packaged foods globally.

Rising Demand for Infant and Nutritional Products

Infant formula and clinical nutrition products are key growth drivers, supported by increasing awareness of early-life nutrition and growing aging populations. Milk powder serves as a primary ingredient in these formulations, offering high nutritional value and ease of use. The premium pricing associated with these segments also enhances overall market profitability.

What are the restraints for the global market?

Volatility in Raw Milk Prices

Fluctuations in raw milk supply due to climatic conditions, feed costs, and seasonal variations significantly impact production costs. This volatility can lead to unstable pricing, affecting both manufacturers and consumers and creating uncertainty in the market.

Stringent Regulatory Compliance

The milk powder industry is subject to strict quality and safety regulations, particularly in infant nutrition. Compliance with international standards increases operational costs and complexity for manufacturers, posing challenges for market entry and expansion.

What are the key opportunities in the milk powder industry?

Expansion in Emerging Markets

Emerging economies such as India, China, and African nations present significant growth opportunities due to rising disposable incomes, population growth, and increasing demand for affordable dairy products. Government nutrition programs and urbanization further support market expansion in these regions.

Innovation in Specialty Milk Powders

The development of specialty products such as organic, lactose-free, and protein-enriched milk powders offers significant growth potential. These products cater to evolving consumer preferences and allow manufacturers to command premium pricing, improving profitability and market differentiation.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 36200.00 Million |

| Market Size in 2026 | USD 38553.00 Million |

| Market Size in 2031 | USD 52820.95 Million |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global milk powder market exhibits a diverse product landscape, with whole milk powder maintaining its leadership position by accounting for approximately 32% of the global market share in 2025. This dominance is primarily attributed to its superior nutritional profile, rich fat content, and versatile applicability across multiple food processing industries. Whole milk powder is extensively utilized in confectionery, bakery, dairy-based beverages, and reconstituted milk products, particularly in regions where cold chain infrastructure is underdeveloped. The leading driver for this segment is its ability to deliver enhanced taste, creaminess, and mouthfeel, which are critical attributes in premium food formulations. Additionally, the extended shelf life and ease of transportation make it a preferred choice among food manufacturers and exporters.Infant milk powder stands out as one of the fastest-growing segments, driven by strong demographic and socio-economic trends. The leading growth driver in this segment is the increasing emphasis on infant health and nutrition, particularly in emerging economies where urbanization and rising disposable incomes are reshaping consumption patterns. Working mothers are increasingly relying on high-quality infant formula products as a convenient and nutritionally balanced alternative to breastfeeding. Furthermore, advancements in formulation technologies, including the addition of probiotics, prebiotics, and essential micronutrients, are enhancing product efficacy and driving premiumization within this segment.Specialty milk powders, including fortified, lactose-free, organic, and high-protein variants, are gaining significant traction as consumers become more health-conscious and demand personalized nutrition solutions. The key driver for this segment is the growing demand for functional foods that offer targeted health benefits such as muscle recovery, immune support, and digestive health. Manufacturers are increasingly investing in research and development to introduce innovative products that align with evolving dietary trends, including plant-based blends and hybrid dairy formulations. This segment is also benefiting from rising awareness of sports nutrition and clinical dietary requirements.Dairy whiteners continue to maintain a stable presence in the market, particularly in developing regions across Asia and Africa. The leading driver for this segment is their affordability, convenience, and widespread use in tea and coffee applications. In regions where fresh milk supply is inconsistent or expensive, dairy whiteners serve as a reliable alternative, supporting consistent demand across both household and commercial segments. Their long shelf life and ease of storage further enhance their appeal in markets with limited refrigeration infrastructure.

Application Insights

The food and beverage industry remains the dominant application segment, contributing nearly 40% of the total market share in 2025. The leading driver for this segment is the extensive functional versatility of milk powder, which enables its use as a key ingredient in bakery products, confectionery, dairy beverages, sauces, and ready-to-eat meals. Its ability to enhance texture, flavor, and nutritional value makes it indispensable in large-scale food production. Additionally, the growing demand for convenience foods and packaged products is significantly boosting the utilization of milk powder in industrial food processing.The infant nutrition segment is witnessing the fastest growth, driven primarily by increasing parental awareness regarding early childhood nutrition and the importance of scientifically formulated dietary products. The rising number of working women, particularly in urban areas, is accelerating the adoption of infant formula as a practical feeding solution. Moreover, stringent quality standards and regulatory frameworks are encouraging manufacturers to develop premium, high-quality products, further fueling market expansion.Clinical and sports nutrition applications are also expanding rapidly, supported by a growing global focus on health, fitness, and preventive healthcare. The leading driver in this segment is the increasing demand for protein-rich and nutrient-dense formulations that support muscle development, recovery, and overall wellness. Milk powder, particularly in its high-protein and fortified forms, is widely used in dietary supplements, medical nutrition products, and functional beverages. The aging population in developed regions is also contributing to the growth of clinical nutrition applications.Household consumption remains a stable and essential segment, particularly in regions where access to fresh milk is limited or unreliable. The primary driver for this segment is the convenience and long shelf life of milk powder, which allows consumers to store and use it as needed without concerns about spoilage. In many developing countries, milk powder serves as a cost-effective and accessible source of nutrition, supporting consistent demand across diverse demographic groups.

Distribution Channel Insights

B2B distribution channels dominate the global milk powder market, accounting for approximately 65% of total sales. The leading driver for this segment is the substantial demand from food manufacturers, dairy processors, and industrial buyers who rely on milk powder as a key raw material. Large-scale procurement agreements, long-term supply contracts, and bulk purchasing practices further strengthen the dominance of B2B channels. Additionally, the globalization of food supply chains has increased cross-border trade, enabling manufacturers to source milk powder efficiently from major exporting regions.B2C distribution channels are experiencing steady growth, driven by rising consumer demand for packaged and branded milk powder products. Supermarkets and hypermarkets play a crucial role in this segment by offering a wide range of options, including premium and specialty products. Convenience stores are also contributing to growth by providing easy access to smaller packaging formats suitable for daily consumption.E-commerce platforms are emerging as a significant growth driver within the B2C segment, fueled by increasing internet penetration and changing consumer shopping behaviors. Online retail offers convenience, competitive pricing, and access to a broader product ассортимент, including imported and niche offerings. Subscription-based models and direct-to-consumer strategies are further enhancing the growth potential of this channel.Specialty stores continue to play an important role, particularly in the distribution of organic, fortified, and premium milk powder products. The leading driver for this channel is the growing consumer preference for high-quality, health-oriented products that require expert guidance and curated selection.

End-Use Industry Insights

The food processing industry remains the largest end-use segment, with a market size exceeding USD 15,000 million in 2026. The leading driver for this segment is the increasing global demand for processed and convenience foods, which rely heavily on milk powder as a functional and nutritional ingredient. Rapid urbanization, busy lifestyles, and changing dietary habits are further accelerating the growth of this industry.The infant nutrition industry is the fastest-growing end-use segment, with an estimated CAGR of around 8%. The primary growth driver is the rising focus on early-life nutrition and the increasing adoption of scientifically formulated infant products. Government initiatives promoting child health and nutrition are also supporting the expansion of this segment.Clinical nutrition and sports nutrition industries are witnessing strong growth, driven by increasing awareness of health and wellness, as well as the rising prevalence of lifestyle-related diseases. The aging population in developed regions is creating significant demand for clinical nutrition products, while the growing fitness culture among younger consumers is boosting the sports nutrition segment.Export-driven demand continues to play a critical role in shaping the market, with major dairy-producing regions supplying milk powder to import-dependent countries. This dynamic is particularly evident in regions with limited domestic dairy production, where reliance on imports is essential to meet consumption needs.

Explore more data points, trends and opportunities Download Free Sample Report

Milk Powder Market Segmentations

By Product Type

- Whole Milk Powder

- Skimmed Milk Powder

- Infant Milk Powder

- Specialty Milk Powders

By Source

- Cow Milk Powder

- Buffalo Milk Powder

- Goat Milk Powder

- Sheep Milk Powder

- Plant-Blended Milk Powder

By Application

- Food & Beverage Industry

- Infant Nutrition

- Clinical & Medical Nutrition

- Sports Nutrition

- Household Consumption

- Animal Feed & Pet Nutrition

By Distribution Channel

- B2B

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Stores

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global milk powder market, accounting for approximately 38% of the total market share in 2025. The region’s growth is primarily driven by its large and rapidly expanding population, coupled with rising urbanization and increasing disposable incomes. Countries such as China and India are at the forefront of demand, supported by strong consumption of dairy products and growing awareness of nutritional benefits. A key driver for regional growth is the increasing demand for infant nutrition products, fueled by rising birth rates and changing parental preferences. Additionally, the expansion of the food processing industry and the growing popularity of convenience foods are significantly boosting milk powder consumption. Southeast Asian countries are also experiencing strong growth due to improvements in retail infrastructure and increasing penetration of modern trade channels.

Europe

Europe holds around 25% of the global market share, supported by its well-established dairy industry and strong production capabilities. The region is characterized by advanced processing technologies, high-quality standards, and a strong focus on exports. The leading driver for growth in Europe is its role as a major exporter of milk powder, particularly to Asia and Africa. Countries such as Germany, France, and the Netherlands have developed robust supply chains that enable efficient production and distribution. Additionally, the growing demand for specialty and organic milk powders is driving innovation within the region, as consumers increasingly seek high-quality and sustainably produced dairy products.

North America

North America accounts for nearly 20% of the global market, with the United States leading demand. The region benefits from advanced dairy farming practices, technological innovation, and a highly developed food processing industry. The primary driver for regional growth is the increasing demand for protein-rich and functional food products, particularly in the sports and clinical nutrition segments. Additionally, the presence of major market players and strong investment in research and development are supporting the introduction of innovative milk powder formulations. The growing trend of health and wellness is further encouraging consumers to adopt fortified and specialty dairy products.

Middle East & Africa

The Middle East & Africa region is the fastest-growing market, with a CAGR of approximately 7.5%. The leading driver for growth is the high level of import dependency due to limited domestic dairy production. Rapid urbanization, population growth, and increasing disposable incomes are contributing to rising demand for milk powder across the region. Countries such as Saudi Arabia, the UAE, and Nigeria are key markets, where milk powder is widely used in both household consumption and food processing applications. Additionally, government initiatives aimed at improving food security and expanding dairy supply chains are supporting market growth. The increasing adoption of packaged and processed foods is also playing a significant role in driving demand.

Latin America

Latin America is experiencing moderate growth, with Brazil and Mexico emerging as the largest markets. The primary driver for regional growth is the increasing consumption of dairy products, supported by rising income levels and changing dietary habits. The expansion of the food processing industry is also contributing to higher demand for milk powder as a key ingredient. Additionally, improving distribution networks and growing retail penetration are enhancing product accessibility across the region. While local production exists, imports continue to play an important role in meeting demand, particularly for specialized and high-quality milk powder products.

Key Players in the Milk Powder Market

- Nestlé

- Danone

- Fonterra

- Lactalis

- FrieslandCampina

- Arla Foods

- Dairy Farmers of America

- Saputo Inc.

- Yili Group

- Mengniu Dairy

- Amul

- Glanbia plc

- Meiji Holdings

- Morinaga Milk Industry

- Royal A-ware