Global Bone Broth Market Size

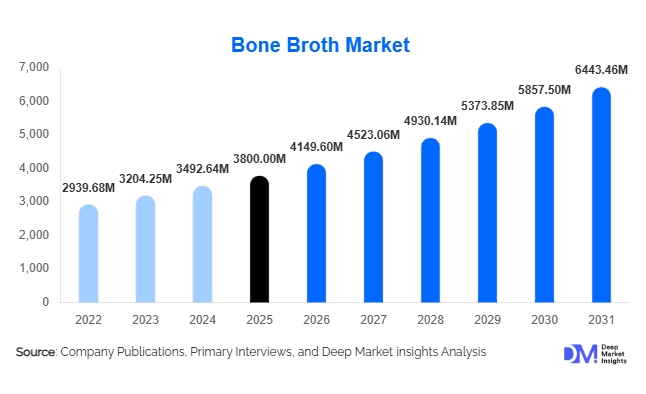

According to Deep Market Insights, the global bone broth market size was valued at USD 3,800 million in 2026 and is projected to grow from USD 4,149.60 million in 2026 to reach USD 6,443.46 million by 2031, expanding at a CAGR of 9.2% during the forecast period (2026–2031). The bone broth market growth is primarily driven by rising consumer demand for gut health and collagen-rich nutrition, increasing adoption of clean-label and functional foods, and the growing popularity of protein-focused dietary lifestyles such as keto and paleo.

Key Market Insights

- Functional nutrition positioning is redefining bone broth, shifting it from a traditional food product to a wellness and dietary supplement category.

- Collagen-rich formulations are driving premium product demand, especially in sports nutrition and anti-aging dietary applications.

- North America dominates global consumption, driven by strong wellness culture and high adoption of keto and paleo diets.

- Asia-Pacific is the fastest-growing region, supported by rising health awareness and expanding middle-class dietary shifts.

- E-commerce and DTC channels are expanding rapidly, enabling subscription-based wellness consumption models.

- RTD and powdered formats are gaining traction due to convenience, shelf stability, and portability.

Bone Broth Market Latest Trends

Functional Food Transformation of Bone Broth

Bone broth is increasingly transitioning from a traditional culinary ingredient to a functional health product. Manufacturers are fortifying broths with collagen peptides, electrolytes, amino acids, and adaptogens to target gut health, immunity, and joint support. This transformation is aligning bone broth with the broader functional food and nutraceutical industries. Ready-to-drink (RTD) bone broth beverages are gaining popularity among urban consumers seeking convenient nutrition, especially in fitness and wellness communities. Premium positioning and clean-label claims are further enhancing product value perception.

Expansion of Clean-Label and Organic Product Demand

Consumers are increasingly prioritizing transparency, sustainability, and ingredient purity. Organic, grass-fed, and antibiotic-free bone broth variants are witnessing strong demand growth. Brands are investing in ethical sourcing and regenerative agriculture practices to appeal to environmentally conscious consumers. This trend is particularly strong in North America and Europe, where regulatory frameworks and consumer awareness are pushing manufacturers toward higher product standards and certification-based marketing strategies.

Bone Broth Market Drivers

Rising Focus on Gut Health and Immunity

The growing awareness of gut health has significantly increased demand for bone broth due to its natural collagen, gelatin, and amino acid content. Consumers are increasingly shifting toward natural remedies that support digestion, inflammation reduction, and immune system strengthening. This trend has been amplified by rising post-pandemic health consciousness and preventive nutrition behavior globally.

Growth of High-Protein and Functional Diets

The increasing adoption of keto, paleo, and low-carb diets has accelerated bone broth consumption as a natural protein source. Fitness enthusiasts and health-conscious consumers are integrating bone broth into daily nutrition routines due to its low-calorie, high-nutrient profile. The sports nutrition industry is also incorporating bone broth into recovery and performance-enhancing formulations.

Expansion of Clean-Label and Natural Food Trends

The global clean-label movement is driving demand for minimally processed foods with simple ingredients. Bone broth aligns strongly with this trend as it is traditionally slow-cooked and free from artificial additives. Consumers increasingly prefer recognizable ingredients, which is strengthening market penetration across premium food and beverage segments.

Global Market Restraints

High Production Costs and Supply Constraints

Bone broth production requires significant time, raw materials, and processing costs due to slow simmering and extraction methods. Dependence on animal bones and quality sourcing increases production complexity and cost volatility, limiting scalability in price-sensitive markets.

Limited Shelf Life of Traditional Products

Traditional liquid bone broth has a short shelf life, creating challenges in global distribution and retail expansion. Although powdered and concentrated forms are addressing this issue, they require additional processing investments and may alter taste profiles, affecting consumer acceptance.

Bone Broth Industry Key Opportunities

Expansion into Nutraceutical and Clinical Nutrition

Bone broth is increasingly being adopted in clinical nutrition, elderly care, and sports recovery applications due to its digestibility and amino acid profile. Hospitals and wellness clinics are incorporating bone broth-based supplements for recovery diets and gut health programs, creating high-margin institutional demand opportunities.

Growth of RTD Functional Beverage Segment

The transformation of bone broth into ready-to-drink functional beverages presents a major growth opportunity. These products are being positioned alongside protein shakes and wellness drinks, targeting urban consumers seeking convenient nutrition solutions. Innovation in packaging and flavor profiles is further expanding consumer acceptance.

E-commerce and Subscription-Based Wellness Models

Direct-to-consumer and subscription models are rapidly expanding, allowing brands to build recurring revenue streams. Online wellness platforms, personalized nutrition plans, and influencer-driven marketing are significantly boosting product visibility and consumer engagement globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3800.00 Million |

| Market Size in 2026 | USD 4149.60 Million |

| Market Size in 2031 | USD 6443.46 Million |

| CAGR | 9..2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Liquid bone broth continues to dominate the global market, accounting for approximately 45% of total demand in 2025. Its leadership is primarily driven by strong culinary integration, long-standing traditional usage in home-cooked meals, and its perceived nutritional authenticity as a minimally processed food format. Consumers value liquid bone broth for its rich flavor profile, natural collagen content, and its ease of incorporation into soups, sauces, and everyday diets, which collectively sustain its widespread household and foodservice adoption.Powdered bone broth is emerging as the fastest-growing product type, supported by increasing consumer demand for convenience-oriented nutrition solutions. Its growth is strongly driven by portability, extended shelf life, and ease of storage, making it highly attractive for urban populations and working professionals with active lifestyles. Additionally, advancements in dehydration and flavor retention technologies have improved product quality, further accelerating adoption across wellness-focused consumers and fitness communities.Concentrated and cube formats maintain steady demand, particularly within foodservice and institutional cooking environments where portion control, cost efficiency, and standardized flavor delivery are important operational drivers. These formats benefit from their versatility and reduced preparation time, making them a practical choice for restaurants and catering services. Meanwhile, ready-to-drink (RTD) bone broth beverages represent an emerging premium segment, gaining traction among fitness-conscious and urban consumers seeking functional, on-the-go nutrition aligned with protein-rich and gut-health-oriented diets.

End-Use Insights

Household consumption remains the largest end-use segment in the bone broth market, driven by the increasing global shift toward home-based wellness, preventive nutrition, and functional eating habits. The rising influence of clean-label diets and natural food consumption patterns has reinforced bone broth’s role as a staple ingredient in daily household nutrition, particularly among health-conscious consumers seeking minimally processed protein sources.Nutraceutical applications are witnessing rapid expansion, fueled by the integration of bone broth into collagen supplements, gut health formulations, and recovery-focused nutritional products. The key driver for this segment is the growing consumer preference for natural bioactive ingredients that support joint health, digestion, and overall wellness, positioning bone broth as a preferred alternative to synthetic protein additives in supplement formulations.The sports nutrition segment is increasingly incorporating bone broth as a natural protein alternative to whey-based products, driven by demand for cleaner, dairy-free, and easily digestible protein sources. Its high amino acid profile and perceived anti-inflammatory benefits are encouraging adoption among athletes and fitness enthusiasts. Additionally, foodservice and clinical nutrition sectors are contributing to steady demand growth, supported by rising use in therapeutic diets, patient recovery programs, and institutional meal planning focused on functional nutrition delivery.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate distribution, supported by strong consumer trust, broad product visibility, and the ability to offer multiple brand comparisons under one roof. These retail formats remain essential for driving mainstream adoption, particularly among first-time buyers and household consumers who prefer in-person product evaluation.Online retail is expanding at a significantly faster pace, driven by the rise of subscription-based wellness services, direct-to-consumer functional food brands, and increasing digital penetration across both developed and emerging markets. The convenience of doorstep delivery, personalized nutrition offerings, and targeted digital marketing campaigns are key factors accelerating e-commerce growth in this segment.Specialty health stores and pharmacies are also gaining importance as consumers increasingly prioritize functional, therapeutic, and clinically positioned nutrition products. These channels benefit from professional guidance, curated product assortments, and heightened consumer trust in health-focused purchasing environments, further supporting premiumization trends in the bone broth market.

Explore more data points, trends and opportunities Download Free Sample Report

Bone Broth Market Segmentations

By Product Type

- Liquid Bone Broth

- Powdered Bone Broth

- Concentrated Bone Broth

- Bone Broth Cubes / Bouillon

- Ready-to-Drink (RTD) Bone Broth Beverages

By Source

- Chicken Bone Broth

- Beef Bone Broth

- Turkey Bone Broth

- Fish Bone Broth

- Mixed / Blended Animal Sources

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail & E-commerce

- Specialty Health & Organic Stores

- Pharmacies & Nutritional Supplement Stores

- Foodservice (HoReCa: Hotels, Restaurants, Cafés)

By End Use

- Household Consumption

- Foodservice Industry

- Nutraceutical & Dietary Supplements

- Sports Nutrition & Fitness Applications

- Clinical Nutrition & Elderly Care

Regional Insights

North America

North America leads the global bone broth market, primarily driven by strong demand in the United States and Canada. The region’s growth is supported by widespread adoption of ketogenic, paleo, and high-protein diets, along with a deeply rooted wellness culture that emphasizes functional and natural nutrition. A mature functional food industry, advanced retail infrastructure, and strong presence of premium health brands further reinforce market leadership. Additionally, increasing consumer awareness regarding gut health, collagen benefits, and clean-label diets continues to drive sustained demand across both household and nutraceutical applications.

Europe

Europe represents a significant and steadily growing market, with key contributions from Germany, the United Kingdom, and France. Growth in the region is strongly influenced by clean-label consumption patterns, high demand for organic food products, and sustainability-driven dietary preferences. Consumers in Europe increasingly favor minimally processed nutrition products with transparent sourcing, which aligns well with bone broth offerings. Regulatory support for natural food ingredients and rising interest in traditional, functional foods further enhance market expansion across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, led by China, India, Japan, and Australia. The region’s rapid expansion is driven by rising disposable incomes, growing awareness of preventive healthcare, and increasing adoption of Western dietary habits. Urbanization and lifestyle changes are also contributing to higher demand for convenient and nutrient-dense food products. Furthermore, the strong growth of e-commerce platforms and digital health food ecosystems is significantly improving product accessibility, accelerating adoption of bone broth across younger and health-conscious consumer groups.

Latin America

Latin America is an emerging market, with Brazil and Mexico at the forefront of consumption growth. The region’s expansion is supported by increasing urbanization, a growing middle-class population, and rising awareness of wellness-oriented diets. Consumers are gradually shifting toward functional and imported health foods as accessibility improves through modern retail and online channels. Additionally, exposure to global nutrition trends and increasing focus on preventive health are driving steady market penetration in the region.

Middle East & Africa

The Middle East & Africa region is experiencing growing demand, particularly in high-income markets such as the UAE and Saudi Arabia, along with emerging interest in South Africa. The primary growth driver is rising health consciousness among affluent consumers, who are increasingly adopting premium, protein-rich, and functional nutrition products. In addition, expanding retail modernization and the growing presence of international health food brands are improving product availability. Africa also plays an important role in raw material sourcing, contributing to regional supply chain integration and long-term market development.

Key Players in the Global Bone Broth Market

- Nestlé S.A.

- Kraft Heinz Company

- Campbell Soup Company

- General Mills Inc.

- Kettle & Fire

- Ancient Nutrition

- Vital Proteins

- Epic Provisions

- Bonafide Provisions

- Osso Good Co.

- Broth Masters

- Unilever

- Tyson Foods Inc.

- The Stock Merchant

- Bare Bones Broth Co.