Air Taxi Market Size

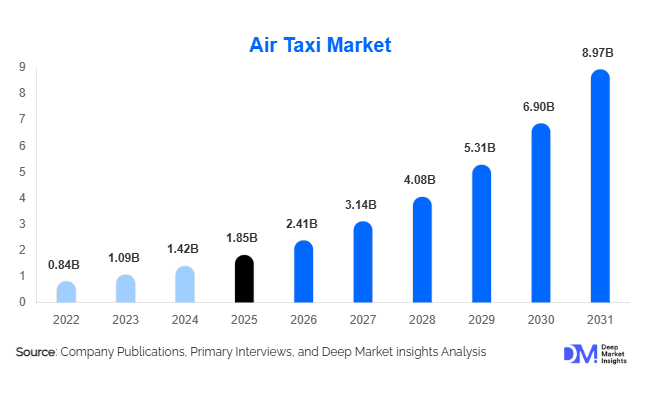

According to Deep Market Insights, the global air taxi market size was valued at USD 1.85 billion in 2025 and is projected to grow from USD 2.41 billion in 2026 to reach USD 8.97 billion by 2031, expanding at a CAGR of 30.1% during the forecast period (2026–2031). The air taxi market growth is primarily driven by rapid advancements in electric vertical take-off and landing (eVTOL) aircraft technology, increasing investments in advanced air mobility infrastructure, and growing demand for sustainable urban transportation solutions. Governments, aerospace manufacturers, and private investors are accelerating commercialization efforts to reduce urban congestion, improve regional connectivity, and support decarbonization objectives within the transportation sector.

Key Market Insights

- Electric air taxis are becoming the preferred urban mobility solution, supported by lower operating costs, reduced emissions, and growing regulatory support for sustainable transportation.

- Urban passenger transportation remains the largest application segment, accounting for more than half of global market demand as cities seek alternatives to road congestion.

- North America dominates the global market, driven by strong certification progress, substantial venture capital funding, and early deployment programs across major metropolitan regions.

- Asia-Pacific is the fastest-growing regional market, supported by smart city initiatives, urbanization, and government-backed advanced air mobility programs.

- Airport connectivity is emerging as a commercially attractive use case, with airlines and airport operators investing in air taxi integration to reduce travel times.

- Artificial intelligence, autonomous flight technologies, and digital air traffic management systems are transforming fleet operations and enabling future scalability of urban air mobility networks.

Air Taxi Market Trends

Commercial Deployment of eVTOL Aircraft Accelerating

The air taxi industry is transitioning from prototype testing toward commercial deployment as leading manufacturers progress through certification and production milestones. Companies are securing aircraft orders, strategic partnerships, and regulatory approvals to launch commercial services across major urban centers. Cities including Dubai, Los Angeles, Singapore, Paris, and Seoul are actively preparing vertiport infrastructure to support early operations. Fleet deployment programs are increasingly focused on short-distance urban routes where congestion costs are highest. As battery technologies improve and certification frameworks mature, commercial air taxi operations are expected to expand significantly between 2026 and 2031, establishing a new category within urban transportation systems.

Autonomous and AI-Enabled Air Mobility Ecosystems Emerging

Artificial intelligence and autonomous aviation technologies are becoming central to the long-term development of the air taxi market. Manufacturers are investing heavily in autonomous navigation, predictive maintenance, digital twin systems, and urban traffic management solutions. AI-powered route optimization and fleet management platforms are improving operational efficiency while reducing costs. Urban Traffic Management (UTM) systems are being developed to safely integrate hundreds of aircraft into metropolitan airspace. These technological advancements are expected to significantly improve aircraft utilization rates and make large-scale urban air mobility commercially viable over the next decade.

Air Taxi Market Drivers

Advancements in Electric Propulsion and Battery Technologies

Rapid improvements in battery energy density, lightweight materials, distributed electric propulsion systems, and flight control technologies are enhancing the operational performance of air taxis. Manufacturers are achieving longer flight ranges, reduced charging times, and improved payload capabilities, making eVTOL aircraft increasingly attractive for commercial applications. These advancements are lowering operating costs while improving sustainability, helping accelerate adoption among transportation operators and municipal authorities.

Growing Investments in Advanced Air Mobility Infrastructure

Governments, aerospace companies, infrastructure developers, and institutional investors are allocating significant capital toward advanced air mobility ecosystems. Investments are being directed toward aircraft manufacturing facilities, vertiports, charging infrastructure, digital air traffic systems, and certification programs. Several countries have incorporated advanced air mobility into national transportation strategies, creating favorable conditions for industry growth. The availability of substantial funding continues to accelerate commercialization timelines and support market expansion globally.

Air Taxi Market Restraints

Complex Regulatory and Certification Requirements

Air taxi operators face extensive certification requirements related to airworthiness, pilot licensing, operational safety, autonomous systems, and airspace integration. Regulatory frameworks are still evolving across many countries, creating uncertainty around deployment timelines. Certification delays can increase development costs and postpone commercial launches, making regulatory compliance one of the most significant challenges facing market participants.

Infrastructure Development Constraints

The success of commercial air taxi services depends heavily on the availability of supporting infrastructure, including vertiports, charging stations, maintenance facilities, and digital traffic management systems. Developing this infrastructure requires substantial capital investment and coordination among multiple stakeholders. Limited infrastructure availability may restrict operational scalability during the early stages of market development, particularly in emerging economies.

Air Taxi Market Opportunities

Airport Shuttle and Premium Business Mobility Services

Airport connectivity represents one of the most attractive commercial opportunities within the air taxi market. Major metropolitan airports are increasingly partnering with air taxi developers to establish dedicated shuttle routes connecting airports with city centers and business districts. These services can significantly reduce travel times for business travelers and premium passengers. As airlines seek to enhance customer experience through integrated mobility offerings, airport shuttle applications are expected to generate substantial recurring revenue opportunities for operators and infrastructure providers.

Smart City Integration and Urban Mobility Networks

The rapid expansion of smart city initiatives creates significant opportunities for air taxi operators and technology providers. Governments are increasingly incorporating advanced air mobility into long-term transportation planning to reduce congestion and improve mobility efficiency. Integrating air taxis with rail systems, metro networks, and public transportation hubs can create seamless multimodal transportation ecosystems. Companies capable of securing strategic partnerships with municipal authorities and transportation agencies will be well-positioned to benefit from the next phase of urban mobility development.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.85 Billion |

| Market Size in 2026 | USD 2.41 Billion |

| Market Size in 2031 | USD 8.97 Billion |

| CAGR | 30.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Propulsion Technology Insights

Fully electric air taxis dominate the global market, accounting for approximately 61% of total revenue in 2025. This leadership is primarily driven by strong regulatory preference for zero-emission aviation solutions, lower operating and maintenance costs compared to conventional aircraft, and rapid improvements in battery energy density and thermal efficiency. Fully electric eVTOL platforms are also the primary focus of certification programs in North America, Europe, and parts of Asia-Pacific, making them the first technology class expected to achieve large-scale commercialization. Their dominance is further reinforced by increasing urban sustainability mandates and government-backed decarbonization targets across transportation systems.

Stringent emission reduction policies in urban aviation, rapid scaling of lithium-ion and next-generation solid-state batteries, and strong investor preference for commercially viable short-haul mobility solutions. The segment benefits significantly from early mover advantage, as most leading OEMs are aligning their product pipelines around fully electric configurations for intracity travel. Hybrid-electric air taxis are gaining traction for extended range and regional mobility applications, where pure battery-electric systems face energy density limitations. Meanwhile, hydrogen fuel-cell technologies are being explored as long-term solutions to unlock longer flight ranges, faster refueling cycles, and higher payload efficiencies, although commercialization timelines remain further out due to infrastructure and storage challenges.

Aircraft Configuration Insights

Multicopter eVTOL aircraft represent the largest configuration segment, holding approximately 34% global market share in 2025. Their dominance is attributed to simplified mechanical design, higher stability in vertical take-off and landing operations, and lower certification complexity compared to more advanced configurations. These aircraft are particularly well-suited for short urban routes, making them the preferred choice for early-stage commercial deployments in dense metropolitan regions.

Faster certification timelines due to simplified flight dynamics, reduced maintenance requirements, and strong alignment with initial urban air mobility use cases such as airport transfers and intra-city commuting. Their ability to operate efficiently in constrained urban landing zones also strengthens their adoption in infrastructure-limited environments. Tiltrotor and lift-and-cruise configurations are gaining momentum due to their superior aerodynamic efficiency and extended range capabilities, making them suitable for intercity and regional routes. These configurations are expected to play a critical role in expanding air taxi networks beyond urban cores as infrastructure and battery performance continue to improve.

Application Insights

Urban passenger transportation remains the dominant application segment, contributing approximately 52% of global market revenue in 2025. This dominance is driven by severe urban traffic congestion, increasing demand for time-efficient mobility solutions, and strong government backing for sustainable urban transportation systems. Air taxis are increasingly viewed as a strategic solution for reducing pressure on road infrastructure in megacities worldwide.

Rising urban population density, expansion of smart city projects integrating multimodal transport systems, and increasing consumer willingness to pay premium pricing for time savings. Additionally, integration with ride-hailing platforms is expected to accelerate mass adoption in this segment. Airport connectivity is emerging as the fastest-growing application, supported by strong airline partnerships and airport authority investments in vertiport infrastructure. Other growing applications include emergency medical transport, high-value logistics, corporate mobility services, and tourism-based aerial experiences, all of which are expected to expand as operational ecosystems mature.

Service Model Insights

On-demand air taxi services account for the largest share of the market, representing approximately 47% of global demand in 2025. This dominance is driven by consumer preference for flexibility, convenience, and direct point-to-point travel without fixed schedules. The ride-hailing-style model closely mirrors existing urban mobility behaviors, making it the most intuitive adoption pathway for early users.

Integration with digital mobility platforms, increasing smartphone-based booking adoption, and strong parallels with established ride-sharing ecosystems. These factors significantly reduce entry barriers for consumers transitioning from ground-based mobility services. Scheduled air mobility services are expected to gain momentum as fleet sizes increase and route networks become more structured. Corporate mobility programs and tourism-focused air taxi services are also emerging as high-value revenue streams, particularly in premium urban corridors and global tourism destinations.

End User Insights

Individual consumers and corporate enterprises represent the largest end-user segments in the air taxi market. Corporate users, particularly business travelers, are driving early adoption due to strong demand for time-saving transportation between airports, business districts, and urban centers. Air taxis are increasingly being positioned as productivity-enhancing mobility solutions within enterprise travel programs.

Rising value of time-efficient mobility in high-density cities, increasing adoption of premium transport services by high-income groups, and integration of air mobility into corporate travel optimization strategies. Government agencies are also emerging as early adopters for specialized use cases such as emergency response and public service transportation. Healthcare organizations represent a rapidly expanding end-user segment, leveraging air taxis for emergency medical evacuation and organ transport applications. Logistics providers and defense agencies are also evaluating air mobility solutions for high-priority and time-sensitive operations.

Explore more data points, trends and opportunities Download Free Sample Report

Air Taxi Market Segmentations

By Propulsion Technology

- Fully Electric Air Taxis

- Hybrid-Electric Air Taxis

- Hydrogen Fuel Cell Air Taxis

- Turboelectric Air Taxis

- Turboshaft-Powered Air Taxis

By Aircraft Configuration

- Multicopter eVTOL

- Tiltrotor eVTOL

- Tiltwing eVTOL

- Lift-and-Cruise eVTOL

- Vectored-Thrust eVTOL

By Application

- Urban Passenger Transportation

- Airport Connectivity

- Corporate & Business Mobility

- Tourism & Leisure Mobility

- Emergency Medical Transport

- Logistics & Cargo Transport

- Government & Defense Services

By End User

- Individual Consumers

- Corporate Enterprises

- Healthcare Organizations

- Government & Defense Agencies

- Tourism Operators

- Logistics Providers

By Infrastructure Type

- Vertiports

- Rooftop Landing Pads

- Airport Integration Hubs

- Charging & Battery Swapping Stations

- Air Traffic Management Systems (UTM/ATM)

Regional Insights

North America

North America accounted for approximately 41% of global market revenue in 2025, making it the leading regional market. The United States is the primary growth engine due to strong venture capital funding, advanced aerospace manufacturing capabilities, and early regulatory progress supporting eVTOL certification. Cities such as Los Angeles, New York, Miami, and Dallas are among the earliest expected deployment hubs.

Strong federal and state-level investment in advanced air mobility infrastructure, presence of leading OEMs and technology developers, and increasing collaboration between aviation regulators and private companies. Additionally, high urban congestion and strong demand for premium mobility services are accelerating early adoption. Canada is also advancing regional air mobility programs focused on remote connectivity and medical transportation in underserved regions, further supporting regional expansion.

Europe

Europe represents approximately 26% of global market demand, led by Germany, France, the United Kingdom, and Italy. The region benefits from strong sustainability mandates, well-established aerospace ecosystems, and proactive regulatory frameworks supporting urban air mobility development. European cities are actively investing in vertiport planning and integrated mobility systems.

Strict environmental regulations promoting zero-emission transport, strong government-backed R&D funding for aviation innovation, and increasing public acceptance of sustainable urban mobility solutions. Additionally, collaboration between aerospace manufacturers and municipal authorities is accelerating certification readiness. Germany leads regional innovation due to its concentration of eVTOL developers and aerospace engineering expertise, while France and the UK are focusing on infrastructure integration and urban deployment pilots.

Asia-Pacific

Asia-Pacific accounted for approximately 22% of global revenue in 2025 and is projected to be the fastest-growing regional market through 2031. China dominates the region with significant investments in low-altitude economy development, urban air mobility infrastructure, and smart city integration programs. Japan, South Korea, Singapore, and India are also rapidly advancing pilot projects and regulatory frameworks.

Rapid urbanization leading to severe traffic congestion, strong government support for next-generation mobility solutions, and rising disposable incomes driving demand for premium transportation services. Expansion of smart city initiatives and integration with digital transport ecosystems further strengthens growth prospects. Asia-Pacific’s dense megacities provide strong use-case validation environments, making the region critical for large-scale commercial deployment of air taxi services.

Latin America

Latin America is an emerging market for air taxis, with Brazil leading regional demand due to its established aerospace industry and growing urban congestion challenges. Mexico is also exploring advanced air mobility solutions for major metropolitan regions.

Increasing urban traffic congestion, gradual expansion of high-income consumer segments, and government interest in aviation innovation. Additionally, Brazil’s aerospace manufacturing ecosystem supports localized development and adoption of advanced mobility platforms.

Middle East & Africa

The Middle East & Africa region is rapidly emerging as a strategic early-adoption market, led by the United Arab Emirates and Saudi Arabia. Governments in the region are heavily investing in futuristic mobility infrastructure as part of broader smart city and economic diversification strategies. Dubai is expected to be one of the first global cities to launch commercial air taxi operations.

Strong government-led infrastructure investment, high demand for luxury and premium transportation services, and strategic initiatives under national transformation programs such as Saudi Vision 2031. Additionally, favorable regulatory environments and high-income populations are accelerating pilot deployments. South Africa is also exploring air taxi applications for tourism and regional connectivity, particularly in areas with limited ground transportation infrastructure.

Key Players in the Air Taxi Market

- Joby Aviation

- Archer Aviation

- EHang Holdings

- Volocopter

- Lilium

- Vertical Aerospace

- Eve Air Mobility

- BETA Technologies

- Wisk Aero

- AutoFlight

- Overair

- Jaunt Air Mobility

- Supernal

- SkyDrive

- Ascendance Flight Technologies