AdTech Market Size

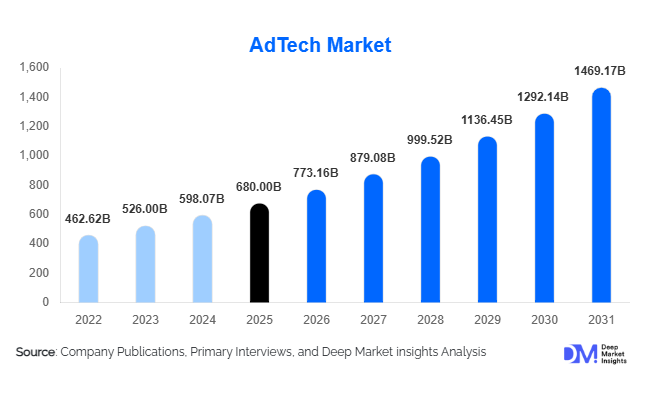

According to Deep Market Insights, the global AdTech market size was valued at USD 680.0 billion in 2025 and is projected to grow from USD 773.16 billion in 2026 to reach USD 1,469.17 billion by 2031, expanding at a CAGR of 13.7% during the forecast period (2026–2031). The AdTech market growth is primarily driven by the increasing adoption of programmatic advertising, rapid expansion of retail media networks, growing digital media consumption across mobile and connected devices, and the integration of artificial intelligence into campaign optimization and audience targeting. Rising investments in privacy-compliant advertising technologies, identity resolution platforms, and omnichannel advertising solutions are further strengthening market expansion across developed and emerging economies.

Key Market Insights

- Programmatic advertising continues to dominate digital advertising transactions, accounting for the majority of display, video, mobile, and connected TV advertising expenditures globally.

- Retail media networks are emerging as one of the fastest-growing advertising channels, supported by retailers monetizing first-party consumer data and expanding commerce media ecosystems.

- North America dominates the global AdTech market, driven by the presence of major technology companies, mature digital advertising infrastructure, and high enterprise advertising spending.

- Asia-Pacific is the fastest-growing regional market, supported by rapid digitalization, expanding e-commerce activity, and increasing internet penetration across India, China, and Southeast Asia.

- Artificial intelligence and machine learning technologies are transforming advertising operations, enabling advanced targeting, automated campaign management, and real-time bidding optimization.

- Privacy-focused advertising solutions are gaining importance, as advertisers transition away from third-party cookies and invest in first-party data, clean rooms, and identity resolution technologies.

AdTech Market Trends

Retail Media Networks Becoming a Core Advertising Channel

Retail media has emerged as one of the most significant developments within the AdTech industry. Large retailers are increasingly leveraging their first-party consumer data to create advertising ecosystems that allow brands to target consumers at the point of purchase. This trend is accelerating as advertisers seek alternatives to third-party cookie-based targeting. Retail media platforms provide closed-loop attribution, enabling marketers to directly measure advertising impact on sales. Major retailers continue investing heavily in advertising technology infrastructure, audience segmentation tools, and commerce media platforms to compete for digital advertising budgets. The expansion of retail media is expected to create substantial revenue opportunities for technology providers specializing in campaign management, audience monetization, and measurement solutions.

Artificial Intelligence Reshaping Advertising Operations

Artificial intelligence is transforming nearly every aspect of digital advertising. AI-powered technologies are improving audience targeting, bid optimization, campaign automation, creative development, and performance measurement. Generative AI solutions are reducing content production timelines while enabling large-scale personalization of advertising creatives. Machine learning algorithms are improving conversion rates and return on advertising spend by dynamically adjusting campaign parameters in real time. As advertisers increasingly prioritize efficiency and measurable outcomes, AI adoption is becoming a competitive necessity across the AdTech ecosystem. Investments in predictive analytics, autonomous media buying platforms, and AI-driven creative optimization solutions are expected to accelerate significantly throughout the forecast period.

AdTech Market Drivers

Growth of Programmatic Advertising Ecosystems

The rapid adoption of programmatic advertising remains one of the primary drivers of AdTech market growth. Automated media buying platforms enable advertisers to purchase inventory across multiple channels efficiently while improving targeting accuracy and campaign performance. Programmatic advertising reduces manual intervention, enhances scalability, and provides real-time optimization capabilities. As organizations seek greater transparency and efficiency in advertising operations, demand for demand-side platforms (DSPs), supply-side platforms (SSPs), and advertising exchanges continues to expand globally.

Expansion of Digital Media Consumption

Growing digital media consumption across mobile devices, connected television, gaming platforms, streaming services, and social media channels is generating substantial demand for advertising technologies. Consumers are spending increasing amounts of time across digital ecosystems, encouraging brands to allocate larger portions of marketing budgets toward digital channels. Emerging markets are experiencing particularly strong growth due to rising internet penetration, smartphone adoption, and digital commerce activity. This shift is creating significant opportunities for AdTech providers to deliver advanced audience targeting and omnichannel advertising solutions.

AdTech Market Restraints

Increasing Data Privacy Regulations

The implementation of stringent privacy regulations such as GDPR, CCPA, CPRA, and similar frameworks across global markets is creating challenges for AdTech participants. Compliance requirements are increasing operational complexity and limiting access to consumer data. Organizations must invest heavily in consent management, data governance, and privacy-preserving advertising technologies to maintain regulatory compliance. These requirements can particularly impact smaller providers with limited resources, potentially slowing innovation and market expansion.

Identity Resolution and Attribution Challenges

The ongoing phaseout of third-party cookies and platform-level tracking restrictions has created significant challenges for audience targeting and campaign measurement. Advertisers face difficulties maintaining user identification across fragmented digital environments, reducing targeting precision and attribution accuracy. While identity graphs, clean rooms, and first-party data strategies are emerging as alternatives, implementation remains complex and costly. These challenges continue to influence technology investment priorities across the AdTech ecosystem.

AdTech Market Opportunities

Connected TV Advertising Expansion

The rapid adoption of streaming platforms and ad-supported video services presents a significant growth opportunity for AdTech providers. Connected TV advertising combines the reach of traditional television with the targeting and measurement capabilities of digital advertising. As consumers increasingly migrate from linear television to streaming environments, advertisers are allocating larger budgets toward CTV campaigns. This trend is creating demand for specialized DSPs, SSPs, audience measurement tools, and identity solutions designed specifically for connected television ecosystems.

Privacy-First Advertising Technologies

The transition toward privacy-centric advertising models is creating substantial opportunities for companies developing alternative targeting and measurement technologies. Solutions such as customer data platforms, clean rooms, contextual advertising platforms, and consent management systems are experiencing strong demand. Organizations capable of enabling effective advertising while maintaining compliance with evolving privacy regulations are expected to benefit from long-term market growth. As advertisers seek sustainable alternatives to traditional tracking methods, privacy-focused innovation is becoming a major area of investment across the industry.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 680 Billion |

| Market Size in 2026 | USD 773.16 Billion |

| Market Size in 2031 | USD 1469.17 Billion |

| CAGR | 13.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Solution Type Insights

Demand-side platforms (DSPs) dominate the global AdTech market, accounting for approximately 33% of total market revenue in 2025. DSPs have emerged as the leading solution category due to the widespread adoption of programmatic advertising, which now represents the majority of digital advertising transactions globally. The ability of DSPs to automate media buying, optimize bids in real time, and provide centralized campaign management across search, display, video, mobile, connected TV (CTV), and retail media channels has significantly increased their adoption among advertisers. The growing demand for audience-level targeting, AI-powered campaign optimization, and measurable return on advertising spend (ROAS) continues to strengthen DSP market leadership.

Supply-side platforms (SSPs) remain a critical component of the AdTech ecosystem, enabling publishers to maximize advertising inventory utilization, improve yield management, and facilitate real-time auction-based selling. Audience and data technologies, including customer data platforms (CDPs), data management platforms (DMPs), identity resolution platforms, and data clean rooms, are among the fastest-growing segments as advertisers transition from third-party cookie dependency toward first-party data strategies. In parallel, measurement, attribution, verification, and fraud detection solutions are witnessing strong demand as brands increasingly prioritize transparency, viewability, brand safety, and campaign performance accountability. The growing complexity of omnichannel advertising environments is expected to drive continued investment across all AdTech solution categories throughout the forecast period.

Advertising Format Insights

Search advertising remains the largest advertising format segment, accounting for approximately 26% of the global AdTech market in 2025. Its leadership position is driven by high purchase intent, superior conversion rates, and measurable performance metrics compared to most other digital advertising formats. Advertisers continue to allocate significant budgets toward search campaigns because they directly engage consumers actively seeking products or services, resulting in higher customer acquisition efficiency and stronger return on investment.

Video advertising represents one of the fastest-growing segments within the market, supported by rising consumption of streaming content, short-form video platforms, and social media video engagement. Connected TV advertising is experiencing particularly strong momentum as audiences increasingly shift away from traditional linear television toward ad-supported streaming platforms. This transition allows advertisers to combine television-scale reach with digital targeting precision and campaign measurement capabilities. Retail media advertising is another rapidly expanding category, benefiting from retailers' ability to leverage first-party shopper data and provide advertisers with closed-loop attribution. Native advertising, digital audio advertising, and digital out-of-home (DOOH) advertising are also gaining traction as brands seek diversified omnichannel consumer engagement strategies.

Deployment Model Insights

Cloud-based deployment dominates the AdTech market, accounting for approximately 82% of total market revenue in 2025. The segment's leadership is primarily driven by the need for real-time data processing, scalable infrastructure, and cost-efficient deployment models capable of handling billions of advertising transactions daily. Cloud-native AdTech platforms enable advertisers, agencies, publishers, and media owners to manage campaigns across multiple geographies and channels while supporting advanced analytics, machine learning algorithms, and audience segmentation capabilities.

The increasing adoption of artificial intelligence, programmatic advertising, and omnichannel marketing strategies has further accelerated migration toward cloud environments. Cloud platforms provide enhanced flexibility, faster software updates, reduced infrastructure costs, and seamless integration with external data sources. Hybrid deployment models continue to attract organizations operating in highly regulated sectors such as healthcare, government, and financial services, where specific data governance requirements necessitate partial on-premise control. While on-premise deployments maintain relevance in certain regulatory environments, their market share continues to decline as organizations prioritize scalability, agility, and digital transformation initiatives.

Enterprise Size Insights

Large enterprises account for approximately 71% of global AdTech spending in 2025, making them the largest customer segment in the market. Their dominance stems from substantial advertising budgets, multinational operations, extensive customer databases, and the need to manage highly complex omnichannel marketing campaigns. Large organizations increasingly deploy integrated advertising technology stacks that combine campaign management, audience targeting, customer data platforms, attribution solutions, and AI-driven analytics to improve marketing effectiveness and optimize advertising investments.

The growing importance of customer personalization, cross-channel engagement, and performance measurement has encouraged enterprises to invest heavily in advanced AdTech infrastructure. Meanwhile, small and medium-sized enterprises (SMEs) are emerging as an important growth segment due to the increasing availability of self-service advertising platforms, automated campaign management tools, and AI-powered optimization solutions. Lower implementation costs and subscription-based pricing models are enabling SMEs to access sophisticated advertising capabilities that were previously limited to large corporations. This democratization of AdTech is expanding market penetration and supporting long-term industry growth.

Platform Insights

Mobile platforms represent the largest platform segment, accounting for approximately 48% of total AdTech market revenue in 2025. The segment's leadership is driven by the continued growth of smartphone adoption, mobile internet usage, app-based commerce, and social media engagement worldwide. Consumers increasingly spend the majority of their digital time on mobile devices, making mobile advertising the primary channel for audience acquisition, engagement, and conversion activities across industries.

The rapid growth of mobile commerce, digital payments, location-based marketing, and in-app advertising continues to strengthen advertiser investment in mobile-focused AdTech solutions. While desktop and web-based advertising remain important for enterprise software, financial services, and information-driven campaigns, connected TV is emerging as the fastest-growing platform category due to increasing streaming consumption. Gaming platforms, digital audio services, and digital out-of-home advertising networks are also generating new growth opportunities as advertisers seek access to highly engaged and contextually relevant audiences. The convergence of mobile, video, commerce, and AI-powered advertising capabilities is expected to further reinforce mobile platform dominance over the forecast period.

End-Use Industry Insights

Retail and consumer goods represent the largest end-use industry within the AdTech market, contributing approximately 24% of total global demand in 2025. The segment's leadership is supported by the rapid expansion of e-commerce, omnichannel retail strategies, retail media networks, and direct-to-consumer business models. Retailers increasingly rely on advertising technologies to improve customer acquisition, personalize shopping experiences, optimize conversion rates, and monetize first-party customer data through commerce media initiatives.

Media and entertainment companies remain another major source of demand, utilizing advertising technologies to monetize digital content, streaming services, gaming platforms, and online media properties. The BFSI sector continues to increase investments in digital advertising for customer acquisition and product cross-selling initiatives. Automotive manufacturers are leveraging AdTech platforms to engage consumers throughout increasingly digital vehicle purchasing journeys, while healthcare organizations are adopting privacy-compliant advertising technologies to improve patient outreach and engagement. Among emerging opportunities, the healthcare and automotive sectors are projected to record some of the highest growth rates due to digital transformation initiatives, increasing consumer engagement across online channels, and growing adoption of data-driven marketing strategies.

Explore more data points, trends and opportunities Download Free Sample Report

AdTech Market Segmentations

By Solution Type

- Demand-Side Platforms (DSPs)

- Supply-Side Platforms (SSPs)

- Audience & Data Platforms (DMPs, CDPs, Identity Resolution Platforms)

- Ad Servers & Campaign Management Platforms

- Measurement, Attribution & Verification Solutions

- Ad Exchanges & Ad Networks

- Retail Media Platforms

By Advertising Format

- Search Advertising

- Display Advertising

- Video Advertising

- Native Advertising

- Social Media Advertising

- Connected TV (CTV) Advertising

- Audio Advertising

- Digital Out-of-Home (DOOH) Advertising

- Retail Media Advertising

By Deployment Model

- Cloud-Based

- On-Premise

- Hybrid

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Platform

- Mobile

- Desktop/Web

- Connected TV (CTV)

- Gaming Platforms

- Digital Audio Platforms

- Digital Out-of-Home Platforms

Regional Insights

North America

North America remains the largest regional AdTech market, accounting for approximately 35% of global market revenue in 2025. The United States contributes the overwhelming majority of regional demand, supported by the presence of leading advertising technology companies including Google, Meta, Amazon, Microsoft, and The Trade Desk. The region benefits from highly developed digital advertising infrastructure, strong enterprise technology adoption, sophisticated programmatic advertising ecosystems, and some of the world's highest digital advertising expenditures.

Key growth drivers include increasing investments in artificial intelligence-powered advertising platforms, rapid expansion of connected TV advertising, strong adoption of retail media networks, and continued migration of advertising budgets from traditional media toward digital channels. Canada is also experiencing steady growth, driven by rising programmatic advertising adoption, e-commerce expansion, and increased investment in first-party data solutions. The region's mature digital economy and continuous innovation in advertising technologies are expected to sustain its leadership position throughout the forecast period.

Europe

Europe accounts for approximately 24% of the global AdTech market, with the United Kingdom, Germany, and France representing the largest contributors to regional demand. The region has established itself as a leader in privacy-focused advertising technologies due to stringent regulatory frameworks such as GDPR and increasing emphasis on consumer data protection.

Growth in Europe is being driven by rising digital advertising expenditures, expanding e-commerce penetration, increasing adoption of contextual advertising solutions, and growing investments in first-party data infrastructure. The United Kingdom remains the region's largest market due to its mature digital advertising ecosystem and high concentration of global advertisers. Germany benefits from strong industrial digitization and enterprise marketing investments, while France is witnessing growing demand for AI-enabled advertising solutions. Increasing connected TV adoption, retail media network expansion, and digital transformation initiatives across major industries continue to support regional market growth.

Asia-Pacific

Asia-Pacific accounts for approximately 29% of global AdTech market revenue in 2025 and is projected to be the fastest-growing regional market throughout the forecast period. China remains the largest regional contributor, benefiting from a highly developed digital commerce ecosystem, strong mobile advertising penetration, and large-scale digital consumer engagement. India is emerging as the fastest-growing national market globally, supported by expanding internet access, rapid smartphone adoption, growing digital payments infrastructure, and increasing digital advertising investments.

Major growth drivers include rising e-commerce activity, expanding social commerce ecosystems, increasing mobile-first consumer behavior, and accelerating adoption of digital media platforms. Japan and South Korea continue to benefit from advanced digital infrastructure and high advertising technology sophistication, while Southeast Asian markets including Indonesia, Vietnam, Thailand, and the Philippines are witnessing substantial growth due to expanding internet populations and rapidly developing digital economies. The region's combination of population scale, digital transformation, and economic growth makes it the most attractive market for future AdTech investments.

Latin America

Latin America is experiencing steady expansion in AdTech adoption, led primarily by Brazil and Mexico. The region is benefiting from increasing internet penetration, rising smartphone usage, expanding social media engagement, and strong growth in e-commerce activity. Brands across the region are increasingly embracing performance marketing and programmatic advertising solutions to improve campaign efficiency and customer acquisition outcomes.

Key growth drivers include rapid digitalization of retail, growing adoption of mobile commerce, increasing use of digital payment platforms, and rising investments by multinational brands targeting Latin American consumers. Brazil remains the dominant market due to its large digital population and mature advertising ecosystem, while Mexico is witnessing strong growth supported by cross-border commerce activity and increasing digital media consumption. As businesses continue shifting advertising budgets toward measurable digital channels, demand for advanced AdTech solutions is expected to accelerate across the region.

Middle East & Africa

The Middle East and Africa region is emerging as a promising growth market for AdTech solutions, supported by increasing digital transformation initiatives, improving internet connectivity, and growing mobile-first consumer engagement. The United Arab Emirates and Saudi Arabia represent the largest markets within the Middle East due to significant investments in digital infrastructure, smart city initiatives, and digital economy development programs.

Key regional growth drivers include government-led digital transformation programs, rising social media usage, expanding e-commerce activity, and increasing adoption of mobile advertising solutions. Saudi Arabia's Vision 2031 initiative and the UAE's digital economy strategies are encouraging greater investment in digital marketing technologies. In Africa, South Africa remains the most mature advertising market, while Nigeria, Kenya, and Egypt are witnessing rapid growth due to expanding internet penetration and increasing smartphone adoption. The region's relatively low digital advertising penetration compared to developed markets presents substantial long-term growth opportunities for AdTech providers.

Key Players in the AdTech Market

- Alphabet (Google)

- Meta Platforms

- Amazon Advertising

- Microsoft Advertising

- The Trade Desk

- Adobe

- Criteo

- PubMatic

- Magnite

- Yahoo Advertising

- Xandr

- MediaMath

- Index Exchange

- OpenX

- Taboola