Women’s Sportswear Market Size

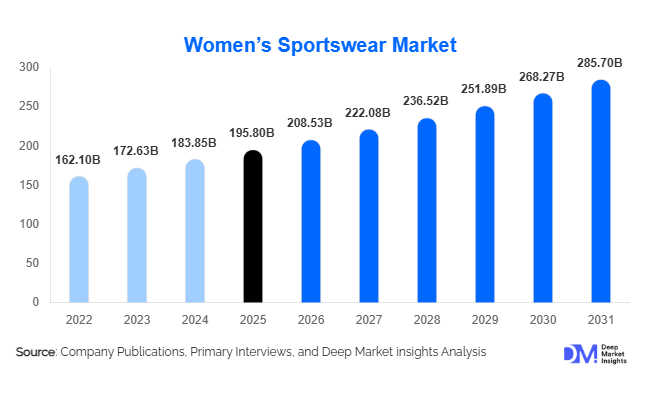

According to Deep Market Insights, the global women’s sportswear market size was valued at USD 195.8 billion in 2025 and is projected to grow from USD 208.53 billion in 2026 to reach USD 285.70 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The women’s sportswear market growth is being driven by increasing female participation in fitness and sports activities, the continued expansion of athleisure fashion, rising health and wellness awareness, and growing demand for multifunctional apparel that combines performance, comfort, and style. Technological advancements in moisture-wicking fabrics, compression technology, sustainable materials, and smart textiles are further enhancing product adoption across both developed and emerging markets.

Key Market Insights

- Athleisure continues to transform women’s sportswear into an everyday lifestyle category, driving demand beyond traditional athletic applications.

- Sustainable and recycled fabric adoption is accelerating globally, supported by consumer demand and stricter environmental regulations across North America and Europe.

- North America dominates the global market, accounting for approximately 34% of global revenue in 2025, supported by high sports participation and premium brand penetration.

- Asia-Pacific is the fastest-growing regional market, driven by rising disposable incomes, increasing female workforce participation, and expanding fitness culture across China, India, and Southeast Asia.

- E-commerce and direct-to-consumer channels are reshaping purchasing behavior, enabling brands to improve customer engagement and profitability.

- Performance innovation remains a key competitive differentiator, with manufacturers investing in smart fabrics, temperature-regulating materials, and compression-enhancing technologies.

What are the latest trends in the women’s sportswear market?

Athleisure Continues to Blur the Line Between Fashion and Sportswear

Athleisure remains one of the most influential trends shaping the women’s sportswear market. Consumers increasingly seek versatile apparel that can seamlessly transition from workouts to work environments, travel, and social activities. Leggings, performance tops, sports bras, and premium joggers are becoming wardrobe staples rather than products reserved solely for athletic activities. Major brands are responding by introducing fashion-forward collections featuring premium fabrics, innovative cuts, and lifestyle-focused designs. This trend has significantly expanded the addressable market by attracting consumers who may not actively participate in sports but value comfort, functionality, and contemporary styling.

Sustainable Sportswear and Circular Manufacturing Models

Sustainability is becoming a central purchasing criterion for sportswear consumers. Manufacturers are increasingly incorporating recycled polyester, organic cotton, bio-based fibers, and low-impact production processes into their product portfolios. Brands are also introducing garment recycling programs, circular product initiatives, and supply-chain transparency measures to meet growing environmental expectations. Consumers are showing willingness to pay premium prices for products that demonstrate measurable sustainability credentials. The trend is particularly strong in Europe and North America, where environmental regulations and consumer awareness continue to influence purchasing decisions.

What are the key drivers in the women’s sportswear market?

Growing Female Participation in Sports and Fitness Activities

The increasing participation of women in organized sports, gym memberships, running events, yoga programs, cycling, and outdoor recreational activities remains one of the strongest drivers of market growth. Government-supported sports initiatives, greater social acceptance of female sports participation, and rising awareness regarding health and wellness are expanding the global consumer base. Professional women’s sports leagues and international sporting events are also increasing visibility and inspiring greater participation among younger demographics. This trend is creating sustained demand across nearly every sportswear product category.

Expansion of Digital Commerce and Direct-to-Consumer Models

The rapid growth of online retail channels is transforming the women’s sportswear market. Direct-to-consumer business models allow brands to build stronger customer relationships, improve margins, and respond more quickly to changing consumer preferences. Online platforms offer greater product variety, enhanced personalization, convenient shopping experiences, and competitive pricing. Social media marketing, influencer partnerships, and mobile commerce are further supporting digital sales growth. As a result, online channels accounted for approximately 34% of total women’s sportswear sales in 2025 and continue to gain market share globally.

Rising Health and Wellness Awareness

Consumers increasingly prioritize active lifestyles, preventive healthcare, and personal wellness. The growing popularity of fitness apps, wellness communities, home workouts, and gym memberships has created sustained demand for high-performance sportswear products. Women are investing in apparel that offers comfort, flexibility, breathability, and performance enhancement, supporting long-term market expansion.

What are the restraints for the global market?

Volatility in Raw Material Costs

The women’s sportswear industry remains highly dependent on petroleum-based materials such as polyester, nylon, and elastane. Fluctuations in raw material prices can significantly impact manufacturing costs, supply chain stability, and profit margins. Price volatility often forces brands to absorb higher costs or pass increases on to consumers, creating challenges in maintaining competitiveness across different pricing segments.

Intense Competitive Environment

The market is characterized by strong competition among global athletic apparel leaders, regional manufacturers, direct-to-consumer brands, and private-label retailers. Continuous product innovation, marketing investments, celebrity endorsements, and pricing pressures create barriers for new entrants and compress profit margins for established participants. Maintaining brand differentiation and consumer loyalty remains a significant challenge across most regional markets.

What are the key opportunities in the women’s sportswear industry?

Expansion of Sustainable Performance Apparel

The growing consumer preference for environmentally responsible products presents a significant opportunity for manufacturers. Companies investing in recycled fabrics, biodegradable materials, water-efficient production technologies, and transparent supply chains can capture premium market segments while strengthening long-term brand equity. Sustainability certifications and circular economy initiatives are expected to become increasingly important competitive differentiators over the forecast period.

Growth in Emerging Market Demand

Emerging economies, including India, China, Indonesia, Vietnam, Brazil, Saudi Arabia, and the UAE are witnessing rising female workforce participation, growing disposable incomes, and increasing health awareness. These factors are creating substantial demand for sportswear products across multiple price categories. Manufacturers that establish localized product portfolios and regional distribution networks can benefit from significant long-term growth opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 195.8 Billion |

| Market Size in 2026 | USD 208.53 Billion |

| Market Size in 2031 | USD 285.70 Billion |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Bottom wear, particularly leggings and tights, represents the largest product segment within the women’s sportswear market, accounting for approximately 24% of global revenue in 2025. The segment benefits from broad applicability across fitness, yoga, running, athleisure, and casual wear applications. Sports bras continue to experience strong growth as consumers increasingly prioritize comfort, support, and performance during physical activities. Performance tops and outerwear remain important categories driven by innovations in moisture management, temperature regulation, and lightweight construction. Sports footwear also represents a substantial revenue contributor, supported by ongoing product innovation and growing participation in fitness activities worldwide.

Activity Category Insights

Athleisure remains the largest activity category, accounting for approximately 31% of global market demand. Consumers increasingly wear sportswear for everyday activities rather than exclusively for exercise, significantly expanding product usage occasions. Fitness and gym training applications remain major contributors, supported by increasing gym memberships and home fitness participation. Running and jogging continue generating substantial demand for specialized footwear, sports bras, and performance apparel. Yoga and Pilates segments are also expanding rapidly due to growing wellness trends and increasing adoption among younger female consumers.

Fabric Type Insights

Polyester-based sportswear dominates the market, representing approximately 42% of global demand in 2025. Polyester remains the preferred material due to its durability, moisture-wicking properties, affordability, and performance characteristics. Nylon-based products maintain strong demand in premium applications requiring enhanced comfort and stretch. Sustainable fabrics, including recycled polyester and bio-based materials, represent the fastest-growing fabric segment as brands prioritize environmental responsibility and consumers increasingly seek sustainable alternatives. Smart textiles incorporating advanced functionality and biometric capabilities are also emerging as a high-growth niche category.

Distribution Channel Insights

Online retail channels lead global distribution, accounting for approximately 34% of market revenue in 2025. E-commerce platforms offer consumers greater convenience, wider product selection, and competitive pricing. Brand-owned digital platforms continue gaining importance as manufacturers seek to strengthen direct consumer relationships and improve profitability. Specialty sporting goods retailers remain important distribution channels due to their product expertise and personalized customer experiences. Department stores and hypermarkets continue serving value-oriented consumer segments, particularly in emerging markets.

Consumer Age Group Insights

Women aged 20–34 years account for the largest share of global demand, representing approximately 41% of total market revenue. This demographic demonstrates high engagement in fitness activities, strong athleisure adoption, and frequent sportswear purchases. Consumers aged 35–49 years remain significant contributors due to growing health awareness and increasing purchasing power. Teenagers represent an important growth segment driven by social media influence, while consumers aged 50 years and above are increasingly adopting active lifestyles, supporting demand for comfort-focused performance apparel.

Explore more data points, trends and opportunities Download Free Sample Report

Women’s Sportswear Market Segmentations

By Product Type

- Sports Bras

- Tops

- Bottom Wear

- Outerwear

- Swim & Water Sportswear

- Sports Footwear

- Accessories

By Activity Category

- Running & Jogging

- Fitness & Gym Training

- Yoga & Pilates

- Outdoor Recreation

- Team Sports

- Racquet Sports

- Swimming & Water Sports

- Cycling

- Athleisure/Casual Sportswear

- Others

By Fabric Type

- Polyester-Based Sportswear

- Nylon-Based Sportswear

- Cotton-Based Sportswear

- Spandex/Elastane-Based Sportswear

- Recycled & Sustainable Fabrics

- Smart & Functional Textiles

By Distribution Channel

- Brand-Owned Stores

- Sporting Goods Retailers

- Department Stores

- Hypermarkets & Supermarkets

- Online Marketplaces

- Brand-Owned E-Commerce

- Specialty Fitness Stores

By End Use

- Fitness & Wellness

- Professional Sports

- Recreational Sports

- Athleisure & Everyday Wear

- Outdoor Activities

Regional Insights

North America

North America accounted for approximately 34% of global women’s sportswear revenue in 2025, making it the largest regional market. The United States dominates regional demand, supported by high sports participation rates, established fitness culture, strong athleisure adoption, and significant spending on premium apparel. Canada also contributes substantially through growing outdoor recreation participation and increasing consumer interest in wellness-oriented lifestyles. The region remains a global leader in innovation, brand development, and digital commerce adoption.

Europe

Europe represented approximately 28% of global market revenue in 2025. Germany, the United Kingdom, France, Italy, and Spain are the region’s largest markets. Sustainability remains a defining characteristic of European consumer preferences, encouraging demand for recycled fabrics and environmentally responsible production methods. Premium sportswear and performance apparel continue experiencing strong growth, particularly among urban consumers focused on health, fitness, and active lifestyles.

Asia-Pacific

Asia-Pacific accounted for approximately 30% of global revenue and represents the fastest-growing regional market, with an expected CAGR exceeding 8% through 2031. China remains the largest regional market, accounting for nearly 40% of Asia-Pacific demand, supported by urbanization, increasing disposable incomes, and growing participation in fitness activities. India is among the fastest-growing national markets globally due to expanding middle-class populations, increasing female workforce participation, and government-supported fitness initiatives. Japan, South Korea, and Australia continue contributing significant premium demand.

Latin America

Latin America accounted for approximately 5% of global market revenue in 2025. Brazil remains the largest market within the region, supported by a strong fitness culture and growing sports participation among women. Mexico and Argentina are also experiencing increasing demand, particularly in urban centers where health and wellness trends continue gaining popularity. International brands are expanding regional presence through localized product offerings and digital retail channels.

Middle East & Africa

The Middle East and Africa represented approximately 3% of global market revenue in 2025. Saudi Arabia and the United Arab Emirates are emerging as important growth markets due to government initiatives encouraging female participation in sports and fitness activities. South Africa remains the region’s largest established market, supported by growing demand for performance apparel, outdoor recreation products, and athleisure fashion. Continued investments in sports infrastructure and wellness programs are expected to support long-term regional growth.