Vibration Sensor Market Size

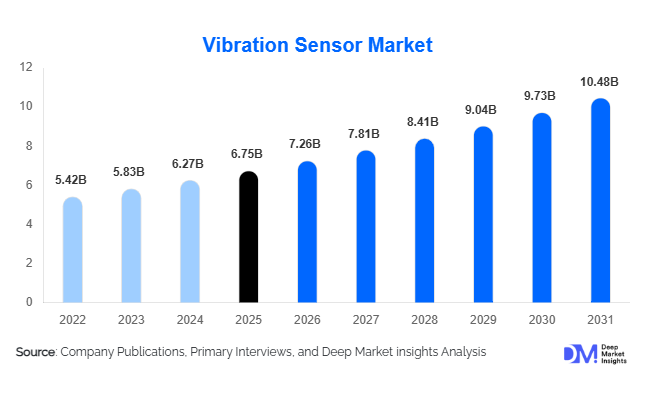

According to Deep Market Insights, the global vibration sensor market size was valued at USD 6.75 billion in 2025 and is projected to grow from USD 7.26 billion in 2026 to reach USD 10.48 billion by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The vibration sensor market growth is primarily driven by the increasing adoption of predictive maintenance technologies, rapid deployment of Industrial Internet of Things (IIoT) solutions, and rising investments in industrial automation across manufacturing, energy, transportation, and infrastructure sectors. Vibration sensors have become a critical component of condition-monitoring systems, enabling organizations to detect equipment faults before catastrophic failures occur. Growing emphasis on asset reliability, operational efficiency, and maintenance cost optimization is accelerating adoption across both developed and emerging economies.

Key Market Insights

- Predictive maintenance applications account for more than 34% of global vibration sensor demand, making them the largest application segment globally.

- Accelerometer-based vibration sensors dominate the market, representing approximately 54% of global revenue due to their versatility and accuracy.

- Asia-Pacific leads the global market with nearly 38% share, supported by industrial expansion in China, India, Japan, and South Korea.

- India is among the fastest-growing country markets, driven by manufacturing expansion, smart factory investments, and government industrial initiatives.

- Wireless vibration sensors are gaining significant traction, supported by Industry 4.0, cloud-based monitoring, and remote asset management requirements.

- Artificial intelligence, edge computing, and digital twin technologies are increasingly being integrated into vibration monitoring platforms to enhance predictive analytics capabilities.

Vibration Sensor Market Trends

Wireless Condition Monitoring Transforming Industrial Maintenance

Wireless vibration monitoring systems are becoming one of the most influential trends in the vibration sensor market. Industrial facilities are increasingly replacing traditional wired monitoring systems with wireless sensor networks to reduce installation costs and improve scalability. Technologies such as LoRaWAN, Bluetooth Low Energy, Zigbee, Wi-Fi, and private 5G networks are enabling real-time monitoring of critical assets across large manufacturing plants, refineries, power stations, and mining operations. Wireless solutions also facilitate monitoring of difficult-to-access equipment, reducing maintenance complexity while improving operational visibility. The trend is particularly strong among organizations implementing Industry 4.0 initiatives and smart factory programs.

AI-Driven Predictive Analytics Enhancing Sensor Value

Vibration sensors are increasingly being deployed alongside artificial intelligence and machine learning platforms capable of identifying subtle equipment anomalies before failures occur. Modern monitoring systems combine sensor-generated vibration data with cloud analytics, digital twins, and asset management software to provide predictive insights. Manufacturers are introducing edge-enabled sensors capable of processing data locally and reducing bandwidth requirements. This shift from reactive maintenance to predictive maintenance is creating significant value for end users by reducing unplanned downtime, extending equipment lifespan, and improving production efficiency across industrial environments.

Vibration Sensor Market Drivers

Growing Adoption of Predictive Maintenance Strategies

Predictive maintenance has emerged as the most important growth driver for the vibration sensor market. Organizations across manufacturing, oil & gas, mining, chemicals, and utilities are increasingly moving away from reactive maintenance approaches toward data-driven asset management models. Vibration sensors provide early warnings of bearing wear, shaft misalignment, imbalance, looseness, and mechanical degradation, enabling operators to schedule maintenance activities proactively. As downtime costs continue to rise, businesses are investing heavily in vibration monitoring solutions to improve equipment reliability and reduce maintenance expenditure.

Expansion of Industrial Automation and Smart Manufacturing

The rapid expansion of industrial automation is significantly increasing vibration sensor deployment across production facilities. Automated machinery, robotic systems, CNC equipment, and material handling systems require continuous condition monitoring to ensure optimal performance and uptime. Governments worldwide are promoting smart manufacturing initiatives, while manufacturers are modernizing production infrastructure to improve competitiveness. As automation levels increase, demand for vibration sensors capable of providing real-time machine health insights is expected to grow steadily throughout the forecast period.

Vibration Sensor Market Restraints

High Implementation and Integration Costs

Although vibration sensor prices have declined significantly over the past decade, complete predictive maintenance systems often require substantial investment in analytics software, networking infrastructure, cloud platforms, and skilled personnel. Small and medium-sized enterprises frequently face budget limitations that delay deployment decisions. Integration with legacy industrial systems can further increase implementation complexity and costs, particularly in older manufacturing facilities.

Data Security and Industrial Cybersecurity Concerns

The increasing use of connected vibration sensors introduces cybersecurity challenges for industrial operators. Cloud-connected monitoring systems generate large volumes of operational data, raising concerns regarding unauthorized access, data breaches, and critical infrastructure security. Industries such as defense, utilities, and oil & gas often maintain stringent cybersecurity requirements, which may slow the adoption of fully connected vibration monitoring architectures. Addressing cybersecurity risks remains essential for widespread deployment of IIoT-enabled vibration sensing solutions.

Vibration Sensor Market Opportunities

Infrastructure Monitoring and Smart Cities Development

Growing investments in transportation infrastructure, bridges, railways, airports, tunnels, and smart city projects present significant opportunities for vibration sensor manufacturers. Structural health monitoring systems increasingly rely on vibration sensors to assess asset integrity, detect deterioration, and improve public safety. Governments worldwide are investing heavily in infrastructure modernization programs, creating long-term demand for advanced vibration monitoring technologies. Sensor providers offering ruggedized and low-maintenance solutions are expected to benefit considerably from these developments.

Renewable Energy Asset Monitoring

The rapid expansion of renewable energy installations, particularly wind farms, is creating substantial opportunities for vibration sensor adoption. Wind turbines require continuous monitoring of gearboxes, bearings, shafts, and generators to ensure operational efficiency and reduce maintenance costs. Offshore wind projects, in particular, demand highly reliable monitoring solutions due to difficult maintenance access. As global renewable energy investments continue to increase, vibration sensor suppliers are expected to benefit from rising deployment across utility-scale energy infrastructure.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.75 Billion |

| Market Size in 2026 | USD 7.26 Billion |

| Market Size in 2031 | USD 10.48 Billion |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Sensor Type Insights

Accelerometers represent the largest sensor type segment, accounting for approximately 54% of global market revenue in 2025. Their dominance is attributed to superior sensitivity, broad frequency response, compact design, and compatibility with predictive maintenance systems. Piezoelectric accelerometers remain the preferred choice for industrial machinery monitoring due to their accuracy and reliability in harsh operating environments. MEMS accelerometers are experiencing rapid adoption in wireless monitoring applications because of their low power consumption and cost advantages. Velocity sensors maintain a strong presence in legacy industrial systems, while displacement sensors continue to find demand in high-precision monitoring applications where shaft movement and alignment measurements are critical.

Technology Insights

MEMS-based vibration sensors account for approximately 37% of the market and represent the fastest-growing technology segment. Their compact size, low manufacturing cost, and compatibility with wireless monitoring systems make them highly attractive for industrial IoT deployments. Piezoelectric technology continues to dominate mission-critical industrial applications where high sensitivity and long-term reliability are required. Optical and fiber-optic vibration sensors are gaining attention in aerospace, defense, and infrastructure monitoring due to their immunity to electromagnetic interference. Capacitive and piezoresistive technologies are increasingly utilized in automotive and electronics applications, supporting broader market diversification.

Application Insights

Predictive maintenance remains the leading application segment, accounting for approximately 34% of global vibration sensor demand. Manufacturers are deploying sensors extensively to monitor motors, pumps, compressors, turbines, and rotating machinery. Condition monitoring represents another major application area, particularly in energy generation, mining, and oil & gas operations. Structural health monitoring is experiencing strong growth as governments and infrastructure operators adopt sensor-based solutions for bridges, rail systems, and public infrastructure assets. Research and development testing applications continue to support demand in aerospace, automotive, and electronics industries where vibration analysis is essential for product validation and performance optimization.

End-Use Industry Insights

Manufacturing remains the largest end-use industry, accounting for approximately 26% of total market demand. The sector's adoption is driven by increasing automation, predictive maintenance programs, and smart factory initiatives. Oil & gas operators continue to invest in vibration monitoring systems to improve reliability of compressors, pumps, and drilling equipment operating in harsh environments. The power generation sector is another major consumer, utilizing vibration sensors for turbine and generator monitoring. Aerospace and defense applications are expanding steadily as aircraft manufacturers and operators emphasize safety, reliability, and maintenance optimization. Renewable energy, particularly wind power, represents one of the fastest-growing end-use sectors globally.

Connectivity Insights

Wired vibration sensors continue to dominate the market, accounting for nearly 65% of global revenue in 2025 due to their established presence in industrial environments and superior reliability in mission-critical applications. However, wireless vibration sensors are growing significantly faster than the overall market. Organizations are increasingly deploying wireless solutions to monitor remote assets, reduce installation costs, and improve maintenance flexibility. Wireless technologies including LoRaWAN, Bluetooth, Zigbee, and 5G connectivity are enabling large-scale condition monitoring deployments across industrial facilities and infrastructure networks.

Explore more data points, trends and opportunities Download Free Sample Report

Vibration Sensor Market Segmentations

By Sensor Type

- Accelerometers

- Velocity Sensors

- Displacement/Proximity Sensors

By Technology

- MEMS-Based Sensors

- Piezoelectric Sensors

- Piezoresistive Sensors

- Optical/Fiber Optic Sensors

- Capacitive Sensors

- Electromagnetic Sensors

By Connectivity

- Wired Sensors

- Wireless Sensors

By Application

- Predictive Maintenance

- Condition Monitoring

- Machine Health Diagnostics

- Equipment Protection Systems

- Structural Health Monitoring

- Process Monitoring

- Research & Development Testing

By End-Use Industry

- Manufacturing

- Automotive & Transportation

- Aerospace & Defense

- Oil & Gas

- Power Generation

- Mining & Metals

- Chemicals & Petrochemicals

- Construction & Infrastructure

- Electronics & Semiconductor Manufacturing

- Healthcare Equipment

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global vibration sensor market, accounting for approximately 38% of total market revenue in 2025, making it the largest regional market worldwide. The region's leadership is primarily driven by rapid industrialization, large-scale manufacturing activity, expanding automation investments, and government-led smart manufacturing initiatives. China represents the largest country-level market within the region, supported by its position as the world's largest manufacturing hub and continued implementation of industrial modernization programs under initiatives such as Made in China 2025. The country's growing adoption of predictive maintenance technologies across automotive, electronics, heavy machinery, steel, and energy sectors continues to generate substantial demand for vibration monitoring solutions.

Japan and South Korea remain major contributors owing to their highly automated industrial ecosystems, advanced robotics manufacturing, semiconductor production facilities, and precision engineering industries. The increasing deployment of vibration sensors in industrial robots, semiconductor fabrication equipment, and high-precision manufacturing systems is supporting sustained market growth. India is emerging as the fastest-growing country market in the region, driven by expanding manufacturing investments, industrial corridor development projects, railway modernization programs, and government initiatives such as Make in India and Production Linked Incentive (PLI) schemes. Additionally, Southeast Asian economies including Vietnam, Thailand, Indonesia, and Malaysia are witnessing accelerated adoption of vibration monitoring technologies as multinational manufacturers diversify production bases beyond China. Rising investments in renewable energy, infrastructure development, and factory automation are expected to further strengthen regional demand throughout the forecast period.

North America

North America accounts for nearly 30% of global vibration sensor market revenue, with the United States representing the dominant share of regional demand. The region benefits from a highly mature industrial base, widespread adoption of predictive maintenance strategies, and extensive deployment of Industrial Internet of Things (IIoT) technologies. U.S. manufacturers continue to invest heavily in digital transformation initiatives aimed at improving operational efficiency, reducing downtime, and extending asset life. Industries including aerospace, defense, oil & gas, power generation, automotive manufacturing, and chemicals remain among the largest consumers of vibration monitoring solutions.

The region's strong emphasis on asset reliability and workforce productivity is accelerating the deployment of advanced condition-monitoring systems integrated with artificial intelligence and cloud analytics platforms. Growth is further supported by rising investments in energy infrastructure, semiconductor manufacturing facilities, and advanced manufacturing reshoring initiatives. Canada contributes significantly through demand from mining operations, utilities, energy infrastructure, and transportation sectors. Meanwhile, increasing adoption of vibration monitoring in renewable energy installations, particularly wind power projects across the United States and Canada, is creating new avenues for market expansion. The growing focus on industrial cybersecurity, smart factories, and digital twin technologies is expected to sustain long-term demand for advanced vibration sensing solutions across North America.

Europe

Europe remains a key market for vibration sensors, accounting for approximately 24% of global market revenue. The region's growth is strongly supported by its advanced manufacturing sector, strict equipment reliability standards, and widespread adoption of Industry 4.0 technologies. Germany serves as the largest market within Europe due to its leadership in industrial automation, automotive manufacturing, machine tools, and industrial machinery production. German manufacturers are among the earliest adopters of predictive maintenance systems, creating consistent demand for high-performance vibration monitoring technologies.

The United Kingdom, France, and Italy also contribute significantly to regional demand through aerospace, defense, automotive, railway, and energy industries. The region's transition toward renewable energy and carbon-neutral industrial operations is further supporting vibration sensor adoption, particularly across wind farms, power generation assets, and energy storage infrastructure. European regulations emphasizing workplace safety, equipment efficiency, and operational sustainability are encouraging industrial operators to invest in advanced monitoring systems. Additionally, increasing investments in smart factories, digital manufacturing platforms, and industrial automation upgrades across Eastern Europe are creating new growth opportunities. The growing use of vibration sensors in rail infrastructure monitoring, aerospace maintenance, and industrial robotics is expected to strengthen Europe's market position throughout the forecast period.

Latin America

Latin America represents approximately 3% of global vibration sensor demand, with Brazil emerging as the largest market in the region. Demand is primarily driven by mining, oil & gas, power generation, metals processing, and manufacturing industries that require continuous equipment monitoring to maintain operational efficiency. Brazil's large mining sector and expanding industrial base continue to generate demand for vibration sensors used in pumps, conveyors, crushers, turbines, and rotating equipment. Growing investments in industrial modernization and predictive maintenance initiatives are gradually increasing market penetration across the country.

Mexico is witnessing accelerated adoption due to expanding automotive production, foreign direct investment inflows, and nearshoring activities that are attracting global manufacturers to establish new production facilities. As industrial automation levels increase, demand for machine health monitoring systems is expected to rise accordingly. Chile and Peru are also important contributors due to their extensive mining operations, where vibration monitoring plays a critical role in reducing equipment failures and maximizing asset utilization. Although overall adoption remains lower than in North America and Europe, increasing awareness of predictive maintenance benefits and continued industrial development are expected to support steady market growth across the region.

Middle East & Africa

The Middle East & Africa accounts for approximately 5% of global vibration sensor market revenue and is expected to witness steady growth during the forecast period. The region's demand is primarily driven by oil & gas infrastructure, petrochemical facilities, mining operations, utilities, and large-scale infrastructure development projects. Saudi Arabia and the United Arab Emirates represent the largest markets, supported by ongoing industrial diversification programs, smart manufacturing investments, and economic transformation initiatives such as Saudi Vision 2031. These programs are accelerating adoption of advanced asset monitoring and predictive maintenance technologies across industrial facilities.

The region's extensive oil & gas operations create significant demand for vibration sensors used in compressors, pumps, turbines, drilling equipment, and pipeline infrastructure. South Africa contributes substantially through mining, metals processing, and industrial manufacturing sectors where equipment reliability remains a critical operational priority. Additionally, rising investments in transportation infrastructure, renewable energy projects, desalination facilities, and smart city developments across the Gulf Cooperation Council (GCC) countries are generating new opportunities for vibration monitoring solutions. The increasing focus on reducing unplanned downtime, improving operational efficiency, and extending asset lifespan is expected to drive continued adoption of vibration sensors throughout the Middle East & Africa over the coming years.

Key Players in the Vibration Sensor Market

- Honeywell International

- Emerson Electric

- Analog Devices

- TE Connectivity

- Bosch Sensortec

- SKF

- Schaeffler

- Spectris

- Safran

- STMicroelectronics

- Parker Hannifin

- Rockwell Automation

- National Instruments

- Baker Hughes

- Baumer