Sustainable Footwear Market Size

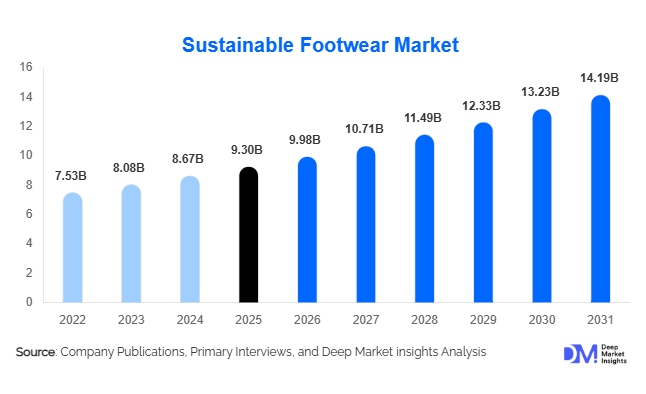

According to Deep Market Insights, the global sustainable footwear market size was valued at USD 9.3 billion in 2025 and is projected to grow from USD 9.98 billion in 2026 to reach USD 14.19 billion by 2031, expanding at a CAGR of 7.3% during the forecast period (2026–2031). The sustainable footwear market growth is being driven by increasing consumer preference for environmentally responsible products, growing adoption of recycled and bio-based materials, expansion of circular economy initiatives, and rising regulatory pressure on brands to reduce carbon emissions and supply chain waste. Sustainability has evolved from a niche purchasing criterion into a mainstream consumer expectation, particularly among Millennials and Generation Z demographics. Major global footwear brands are incorporating recycled plastics, organic textiles, natural rubber, and plant-based leather alternatives into their product portfolios, while emerging sustainable footwear specialists continue to drive innovation in material science and circular business models.

Key Market Insights

- Recycled and bio-based materials are becoming mainstream in footwear manufacturing, enabling brands to reduce dependence on petroleum-based synthetic materials.

- Circular economy models including footwear take-back, resale, repair, and recycling programs are gaining traction, particularly across Europe and North America.

- Asia-Pacific dominates the global sustainable footwear market, supported by extensive footwear manufacturing capacity and rapidly growing consumer demand.

- India represents one of the fastest-growing country markets, driven by rising environmental awareness, increasing disposable income, and expanding e-commerce penetration.

- Online retail channels continue to gain market share, supported by direct-to-consumer business models and sustainability-focused brand positioning.

- Technological innovation in plant-based leather, carbon-negative materials, and advanced recycling technologies is reshaping product development and competitive dynamics.

What are the latest trends in the sustainable footwear market?

Circular Footwear Programs Expanding Globally

Footwear manufacturers are increasingly investing in circular economy initiatives designed to reduce waste and improve material recovery rates. Take-back programs, refurbishment services, footwear rental concepts, and recycling partnerships are becoming important components of sustainability strategies. Brands are designing products with easier disassembly and recyclability in mind, enabling greater recovery of valuable materials such as rubber, textiles, and plastics. Circular footwear programs not only support environmental objectives but also create additional revenue streams through resale and remanufacturing activities. The trend is particularly strong in Europe where regulatory support for Extended Producer Responsibility (EPR) programs is encouraging manufacturers to develop closed-loop systems.

Rise of Bio-Based and Alternative Leather Materials

Plant-derived leather alternatives are transforming the sustainable footwear industry. Materials derived from pineapple fibers, mushrooms, apples, cactus, cork, algae, and sugarcane are increasingly being commercialized across footwear categories. These materials provide significantly lower environmental impact compared with conventional animal leather and synthetic alternatives while appealing to environmentally conscious consumers. Manufacturers are investing heavily in proprietary material innovations that offer durability, comfort, and scalability while reducing lifecycle emissions. As production technologies mature, alternative leather materials are expected to become increasingly cost-competitive with traditional options.

What are the key drivers in the sustainable footwear market?

Growing Consumer Preference for Sustainable Products

Consumer purchasing behavior is increasingly influenced by environmental considerations. Buyers are evaluating footwear products based on sustainability credentials, material sourcing transparency, carbon footprint, and ethical manufacturing practices. Younger consumer groups are particularly willing to support brands that demonstrate measurable environmental commitments. This shift in purchasing priorities is encouraging both established footwear companies and emerging brands to accelerate sustainability initiatives across product development and supply chains.

Regulatory Support and ESG Compliance Requirements

Governments and regulatory bodies worldwide are introducing stricter sustainability standards related to emissions reduction, waste management, material traceability, and environmental disclosures. These regulations are encouraging footwear manufacturers to adopt sustainable materials and improve manufacturing processes. In parallel, investors are placing increasing emphasis on Environmental, Social, and Governance (ESG) performance, creating additional incentives for sustainable product development and responsible sourcing initiatives.

Advancements in Sustainable Material Technologies

Rapid innovation in recycled polymers, bio-based foams, regenerative fibers, and carbon-negative materials is enabling manufacturers to improve product performance while reducing environmental impact. These technological advancements are helping sustainable footwear achieve comparable durability, comfort, and aesthetics to conventional footwear products, thereby supporting broader market adoption.

What are the restraints for the global market?

Higher Manufacturing Costs Compared to Conventional Footwear

Sustainable materials and certified manufacturing processes often involve higher procurement, certification, and processing costs than traditional alternatives. While consumers increasingly value sustainability, price sensitivity remains a barrier in several emerging markets. Manufacturers must balance sustainability goals with affordability to achieve large-scale adoption.

Complexity of Sustainable Supply Chains

Securing consistent supplies of certified recycled and bio-based materials remains challenging. Fragmented supplier ecosystems, certification requirements, and limited production scalability for some alternative materials can create supply constraints and increase operational complexity. Maintaining full traceability across global supply chains also requires substantial investment in digital monitoring and reporting systems.

What are the key opportunities in the sustainable footwear industry?

Expansion into Emerging Consumer Markets

Countries such as India, Indonesia, Vietnam, Brazil, Mexico, and the United Arab Emirates represent significant growth opportunities for sustainable footwear manufacturers. Rising urbanization, growing middle-class populations, and increasing awareness of environmental issues are creating favorable demand conditions. Companies that localize product offerings and establish regional manufacturing partnerships can capture substantial market share in these high-growth markets.

Footwear Recycling and Circular Economy Infrastructure

The development of large-scale footwear collection, sorting, refurbishment, and recycling systems represents a major growth opportunity. As regulatory frameworks increasingly support circular economy models, companies capable of establishing efficient recycling ecosystems can reduce material costs, strengthen sustainability credentials, and generate recurring revenue streams from recovered materials and resale programs.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.3 Billion |

| Market Size in 2026 | USD 9.98 Billion |

| Market Size in 2031 | USD 14.19 Billion |

| CAGR | 7.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Non-athletic sustainable footwear accounts for approximately 61% of the global market revenue, making it the largest product category. Casual shoes, sneakers, loafers, and sustainable fashion footwear continue to benefit from widespread consumer adoption across everyday wear applications. Sustainable sneakers have become particularly popular among younger consumers seeking environmentally responsible lifestyle products. Athletic sustainable footwear is also experiencing strong growth, supported by increasing participation in sports, fitness, and outdoor recreational activities. Performance-focused products incorporating recycled materials and bio-based cushioning technologies are becoming increasingly prevalent across running, training, and outdoor footwear segments.

Material Type Insights

Recycled material footwear represents the largest material category, accounting for approximately 38% of global market revenue in 2025. Recycled PET, recycled rubber, and reclaimed textile fibers are widely used due to their scalability and cost-effectiveness. Plant-based leather alternatives represent one of the fastest-growing material segments, driven by advancements in mushroom leather, pineapple leather, cactus leather, and apple leather technologies. Bio-based materials such as sugarcane EVA and natural rubber are also gaining traction as brands seek lower-carbon alternatives to petroleum-derived components.

Distribution Channel Insights

Online retail channels account for approximately 42% of global sustainable footwear sales. Direct-to-consumer websites, digital marketplaces, and sustainability-focused e-commerce platforms continue to gain importance as consumers increasingly research product sustainability credentials online before purchasing. Brand-owned e-commerce channels are particularly effective for communicating environmental initiatives, traceability information, and sustainability certifications. Offline retail remains important for product trial and premium customer experiences, especially within specialty footwear stores and branded retail outlets.

Consumer Group Insights

Men's sustainable footwear accounts for approximately 54% of total market demand, supported by broader product availability and higher average spending per purchase. Women's footwear represents a rapidly expanding segment as sustainable fashion trends gain momentum globally. Children's sustainable footwear remains a smaller but growing category, benefiting from increasing parental awareness regarding environmental responsibility and product safety. Demand for durable, non-toxic, and responsibly sourced footwear is supporting growth within this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Sustainable Footwear Market Segmentations

By Product Type

- Athletic Sustainable Footwear

- Non-Athletic Sustainable Footwear

By Material Type

- Recycled Materials

- Bio-Based Materials

- Plant-Based Leather

- Organic Textile Materials

- Regenerative & Carbon-Negative Materials

By Consumer Group

- Men

- Women

- Children

By Distribution Channel

- Online Retail

- Brand-Owned E-Commerce

- Third-Party Marketplaces

- Specialty Footwear Stores

- Brand Stores

- Department Stores

- Hypermarkets & Supermarkets

By Price Category

- Economy

- Mid-Range

- Premium

- Luxury

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 37% of the global sustainable footwear market, making it the largest regional market. China remains the dominant country due to its manufacturing leadership and rapidly growing, environmentally conscious consumer base. India is among the fastest-growing markets globally, supported by rising disposable incomes, expanding digital commerce, and increasing sustainability awareness. Japan, South Korea, and Australia also contribute significantly through strong demand for premium and innovative sustainable footwear products.

Europe

Europe represents approximately 31% of global market revenue. Germany, France, the United Kingdom, Italy, Spain, and the Nordic countries lead regional demand. Strict environmental regulations, strong consumer awareness, and widespread adoption of sustainable fashion products continue to support market growth. Germany alone accounts for approximately 7% of global demand, making it one of the most important country markets worldwide.

North America

North America accounts for approximately 24% of global market demand, led by the United States and Canada. Strong consumer purchasing power, growing ESG awareness, and established sustainable brands support regional growth. Demand is particularly strong within premium and athletic sustainable footwear categories, with consumers increasingly seeking transparent supply chains and certified sustainable products.

Latin America

Brazil represents the largest sustainable footwear market in Latin America. Rising environmental awareness, growth in e-commerce, and expanding middle-class purchasing power are supporting regional demand. Mexico and Argentina are also emerging as important markets for sustainable consumer goods, including footwear.

Middle East & Africa

The Middle East and Africa region accounts for approximately 3% of global market revenue. The UAE, Saudi Arabia, and South Africa represent the most significant markets due to rising sustainability initiatives, increasing premium consumer spending, and expanding retail infrastructure. Growing awareness of environmental issues is expected to support future market expansion across the region.

Key Players in the Sustainable Footwear Market

- Nike Inc.

- Adidas AG

- PUMA SE

- VEJA

- Rothy's Inc.

- Allbirds Inc.

- Timberland

- Native Shoes

- Cariuma

- Tropicfeel

- Nisolo

- Ecoalf

- Vivobarefoot

- Thousand Fell

- Po-Zu