Stainless Steel Jewelry Market Size

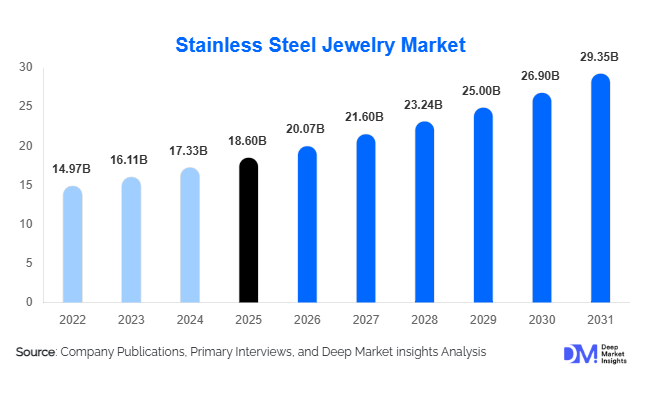

According to Deep Market Insights, the global stainless steel jewelry market size was valued at USD 18.6 billion in 2025 and is projected to grow from USD 20.07 billion in 2026 to reach USD 29.35 billion by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The stainless steel jewelry market growth is primarily driven by increasing consumer preference for affordable luxury accessories, rising demand for hypoallergenic and durable jewelry, and the rapid expansion of digital jewelry retail platforms globally.

Key Market Insights

- Stainless steel jewelry is increasingly positioned as an affordable luxury category, attracting younger consumers seeking fashionable yet durable accessories.

- Online retail channels dominate market expansion, supported by influencer marketing, direct-to-consumer jewelry brands, and rapid social commerce growth.

- Asia-Pacific dominates the global market, led by China’s manufacturing leadership and rising fashion jewelry demand across India and Southeast Asia.

- Men’s stainless steel jewelry is among the fastest-growing categories, driven by streetwear trends, celebrity influence, and rising adoption of fashion accessories among male consumers.

- 316L surgical-grade stainless steel is witnessing strong adoption due to its hypoallergenic properties, corrosion resistance, and suitability for everyday wear.

- Sustainable and recycled stainless steel jewelry is gaining traction among environmentally conscious consumers, especially in Europe and North America.

Stainless Steel Jewelry Market Trends

Personalized and Minimalist Jewelry Trends Accelerating Demand

Minimalist aesthetics and personalized jewelry designs are becoming dominant trends within the stainless steel jewelry market. Consumers increasingly prefer lightweight, versatile, and everyday wearable accessories that complement modern fashion styles. Layered chains, engraved bracelets, zodiac pendants, and custom name necklaces are witnessing rising popularity across younger demographics, particularly millennials and Generation Z consumers. Personalized jewelry products provide emotional value and gifting appeal, enabling brands to command premium pricing and improve customer retention. Social media platforms such as Instagram, TikTok, and Pinterest are significantly influencing jewelry design trends, accelerating product launch cycles and driving demand for fashion-responsive collections. Jewelry brands are increasingly integrating laser engraving technologies and AI-assisted customization tools to support scalable personalization services.

Sustainable and Hypoallergenic Jewelry Gaining Popularity

Sustainability and skin-friendly product preferences are reshaping the competitive landscape of the stainless steel jewelry industry. Consumers are increasingly prioritizing hypoallergenic materials such as 316L surgical stainless steel due to rising awareness regarding skin sensitivity associated with low-quality alloys. In parallel, recycled stainless steel jewelry and eco-friendly production methods are gaining traction, especially among environmentally conscious consumers in Western markets. Jewelry companies are investing in sustainable packaging, low-emission coating technologies, and cleaner manufacturing processes such as physical vapor deposition (PVD) coatings to reduce environmental impact. Brands that communicate ethical sourcing practices and sustainable manufacturing narratives are strengthening their premium positioning in global fashion jewelry markets.

Stainless Steel Jewelry Market Drivers

Rising Demand for Affordable Luxury Accessories

Consumers globally are increasingly shifting toward affordable luxury products that deliver premium aesthetics without the high price associated with precious metals such as gold and platinum. Stainless steel jewelry offers durability, corrosion resistance, and visual similarity to premium jewelry materials at significantly lower costs, making it highly attractive across middle-income and younger consumer groups. The ability to frequently purchase multiple fashion-oriented accessories is encouraging repeat buying behavior and accelerating market growth. Rising urbanization, increasing fashion consciousness, and higher discretionary spending are also supporting global adoption of stainless steel jewelry products.

Rapid Expansion of E-Commerce and Social Commerce Platforms

The rapid growth of digital retail infrastructure has significantly expanded the accessibility of stainless steel jewelry products globally. E-commerce marketplaces, direct-to-consumer platforms, and social commerce channels enable consumers to compare pricing, designs, and customer reviews instantly. Jewelry brands are leveraging influencer partnerships, live commerce, AI-driven recommendations, and virtual try-on technologies to improve online conversion rates and customer engagement. Digital-first jewelry brands are increasingly bypassing traditional retail channels, enabling faster international expansion and higher operating margins. Social media-driven fashion purchasing behavior is particularly influential among younger consumers, accelerating online jewelry sales growth worldwide.

Stainless Steel Jewelry Market Restraints

Intense Pricing Competition and Product Commoditization

The stainless steel jewelry market remains highly competitive due to relatively low entry barriers in online retail and manufacturing. Numerous small-scale sellers and unorganized manufacturers compete aggressively on pricing, particularly across e-commerce marketplaces. This intense competition creates pricing pressure and margin compression for both emerging brands and established players. Product commoditization also increases customer switching behavior, making brand differentiation increasingly important for long-term profitability.

Volatility in Raw Material and Manufacturing Costs

Fluctuations in nickel, chromium, and stainless steel raw material prices continue to impact production costs globally. Rising logistics expenses, energy price inflation, and geopolitical trade disruptions have further increased operational challenges for manufacturers. Smaller jewelry producers with limited procurement scale are especially vulnerable to supply chain disruptions and margin volatility. Environmental regulations related to electroplating chemicals and wastewater management are also increasing compliance costs across manufacturing hubs.

Stainless Steel Jewelry Market Opportunities

Expansion of Men’s Jewelry and Gender-Neutral Fashion

The global rise of gender-neutral fashion and men’s accessories presents substantial growth opportunities for stainless steel jewelry manufacturers. Male consumers are increasingly adopting rings, bracelets, chains, and pendants as part of everyday fashion styling, supported by celebrity influence, luxury streetwear trends, and social media exposure. Jewelry brands are expanding male-focused product portfolios featuring industrial, minimalist, and urban-inspired designs. This trend is particularly strong across North America, Europe, South Korea, and urban Asia-Pacific markets, where men’s fashion spending continues to rise.

Growth of Sustainable and Recycled Jewelry Collections

Sustainability-focused product innovation is creating new premiumization opportunities within the stainless steel jewelry market. Consumers increasingly prefer recycled stainless steel jewelry and eco-conscious manufacturing practices that reduce environmental impact. Jewelry companies integrating sustainable sourcing, ethical manufacturing, and low-emission coating technologies are strengthening their competitive positioning, particularly among environmentally conscious consumers in Europe and North America. Recycled steel collections, biodegradable packaging, and carbon-conscious branding strategies are expected to become increasingly important market differentiators over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.6 Billion |

| Market Size in 2026 | USD 20.07 Billion |

| Market Size in 2031 | USD 29.35 Billion |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Necklaces and chains dominate the stainless steel jewelry market, accounting for the largest share of global demand due to their broad fashion compatibility, unisex appeal, and strong alignment with layered styling trends. Minimalist chains, pendants, and personalized necklaces continue to witness high consumer adoption across younger demographics. Rings represent another significant segment, particularly within men’s jewelry and affordable wedding band categories. Earrings and bracelets are also witnessing strong demand growth, supported by increasing preference for hypoallergenic and daily-wear jewelry products. Body jewelry, including nose rings and industrial bars made from surgical-grade stainless steel, is expanding steadily among younger urban consumers seeking durable and skin-friendly accessories.

Material Type Insights

316L surgical stainless steel remains the leading material segment globally due to its superior corrosion resistance, durability, and hypoallergenic properties. Consumers increasingly prefer 316L-grade jewelry for long-duration wear and sensitive skin applications, particularly in earrings and body jewelry categories. Gold-plated stainless steel jewelry is rapidly gaining popularity within premium fashion segments, offering luxury-inspired aesthetics at affordable price points. Rose gold and black oxidized finishes are also emerging as high-growth categories due to rising demand for fashion-forward and gender-neutral accessories. PVD-coated jewelry is gaining traction as brands prioritize anti-tarnish durability and environmentally safer finishing technologies.

Distribution Channel Insights

Online retail platforms dominate the stainless steel jewelry market, supported by growing consumer trust in digital jewelry purchases, social media marketing, and global accessibility of e-commerce channels. Brand-owned websites and direct-to-consumer business models are increasingly preferred because they improve margins, enable personalized customer engagement, and support rapid product launches. Third-party marketplaces continue to play a major role in expanding product visibility and price competitiveness. Offline retail channels, including jewelry specialty stores and department stores, remain important for premium and luxury-oriented collections where customers value physical product evaluation before purchase. Boutique stores and independent designer channels are also gaining traction among consumers seeking customized and limited-edition jewelry designs.

Gender Insights

Women account for the largest share of the global stainless steel jewelry market, supported by higher spending on fashion accessories, everyday jewelry styling, and personalized products. Female consumers increasingly prefer durable, affordable, and low-maintenance jewelry suitable for both casual and professional wear. However, men’s stainless steel jewelry is emerging as the fastest-growing segment globally, driven by rising acceptance of fashion accessories among male consumers and the growing influence of luxury streetwear culture. Unisex jewelry collections are also gaining momentum as gender-neutral fashion trends continue to influence global consumer preferences.

Age Group Insights

Millennials represent the largest consumer segment in the stainless steel jewelry market due to their strong engagement with digital retail platforms, fashion-conscious purchasing behavior, and preference for affordable luxury products. Consumers aged 25–40 years prioritize trendy yet durable accessories that align with fast-changing fashion cycles. Generation Z consumers are driving rapid growth in personalized jewelry, streetwear-inspired accessories, and social media-influenced purchasing trends. Older demographics, particularly consumers above 45 years, continue to contribute to demand for minimalist, premium-finish, and hypoallergenic jewelry collections designed for long-term everyday use.

Explore more data points, trends and opportunities Download Free Sample Report

Stainless Steel Jewelry Market Segmentations

By Product Type

- Rings

- Necklaces & Chains

- Earrings

- Bracelets

- Body Jewelry

- Watches & Jewelry Watches

- Customized & Engraved Jewelry

By Material Type

- 304 Stainless Steel Jewelry

- 316 Stainless Steel Jewelry

- 316L Surgical Stainless Steel Jewelry

- Gold-Plated Stainless Steel Jewelry

- Rose Gold Stainless Steel Jewelry

- Black Oxidized Stainless Steel Jewelry

- Hypoallergenic Stainless Steel Jewelry

By Distribution Channel

- Online Retail

- Brand-Owned E-Commerce Platforms

- Jewelry Specialty Stores

- Department Stores

- Fashion Accessory Retail Chains

- Independent Designers & Boutique Stores

By Gender

- Men

- Women

- Unisex

- Kids & Teen Jewelry

By End Use

- Fashion & Lifestyle

- Wedding & Occasion Wear

- Corporate & Professional Accessories

- Religious & Cultural Usage

- Gift & Personalization Industry

- Medical & Hypoallergenic Wear

Regional Insights

North America

North America accounts for a significant share of the global stainless steel jewelry market, led primarily by the United States. Strong consumer spending on fashion accessories, rising adoption of men’s jewelry, and increasing demand for sustainable products continue to support regional growth. Online jewelry retail penetration remains exceptionally high in the region, enabling digital-first brands to expand rapidly. Consumers increasingly prioritize personalized and hypoallergenic jewelry collections, while luxury-inspired stainless steel accessories continue gaining popularity among younger demographics. Canada also demonstrates stable growth supported by premium retail expansion and rising fashion-conscious consumer behavior.

Europe

Europe remains one of the most mature markets for stainless steel jewelry, supported by strong fashion culture, sustainability awareness, and premium jewelry design capabilities. Countries such as Germany, the United Kingdom, France, and Italy represent major consumption hubs. European consumers increasingly prioritize ethical sourcing, recycled stainless steel, and environmentally friendly coating technologies, encouraging brands to invest in sustainable manufacturing practices. Italy continues to play an important role in jewelry craftsmanship and luxury-inspired design innovation, while the United Kingdom exhibits particularly strong demand for minimalist and personalized fashion jewelry products.

Asia-Pacific

Asia-Pacific dominates the global stainless steel jewelry market, accounting for the largest share of global revenue. China remains the world’s leading manufacturing and export hub due to its large-scale production infrastructure, integrated stainless steel supply chain, and competitive labor ecosystem. India is emerging as one of the fastest-growing markets globally, supported by rising disposable incomes, urbanization, and increasing adoption of fashion jewelry among younger consumers. South Korea and Japan continue influencing premium fashion trends, particularly within minimalist and streetwear-inspired jewelry categories. Expanding e-commerce penetration and social commerce adoption across Southeast Asia are further accelerating regional market growth.

Latin America

Latin America is witnessing steady growth in stainless steel jewelry demand, particularly across Brazil and Mexico. Rising urbanization, increasing fashion awareness, and affordability advantages compared to precious metal jewelry are supporting regional adoption. Younger consumers are increasingly influenced by social media-driven fashion trends, encouraging demand for layered chains, bracelets, and personalized accessories. The expansion of digital retail infrastructure and cross-border e-commerce platforms is also improving market accessibility across the region.

Middle East & Africa

The Middle East and Africa region is experiencing growing demand for premium stainless steel jewelry collections, supported by luxury retail expansion and rising youth populations. The UAE remains a major regional fashion and jewelry retail hub due to strong tourism infrastructure and high luxury consumption. Saudi Arabia is witnessing increasing adoption of contemporary fashion accessories among younger consumers. South Africa continues to represent an important regional retail market supported by expanding urban middle-class populations and rising exposure to international fashion trends.

Key Players in the Stainless Steel Jewelry Market

- Pandora

- Fossil Group

- Swarovski

- Tiffany & Co.

- Thomas Sabo

- David Yurman

- Police Jewelry

- Morellato Group

- Nomination Italy

- Mejuri

- Missoma

- Alex and Ani

- Skagen

- Brosway

- Cartier