Smart Watch Market Size

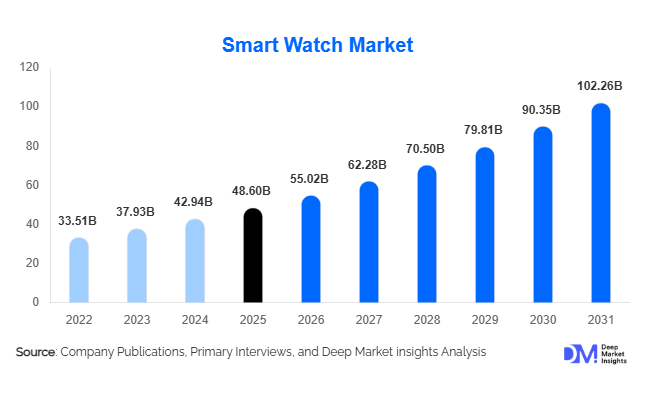

According to Deep Market Insights, the global smart watch market size was valued at USD 48.6 billion in 2025 and is projected to grow from USD 55.02 billion in 2026 to reach USD 102.26 billion by 2031, expanding at a CAGR of 13.2% during the forecast period (2026–2031). The smart watch market growth is primarily driven by rising consumer awareness regarding digital health monitoring, increasing smartphone connectivity, rapid adoption of wearable technologies, and the expansion of AI-enabled fitness and wellness ecosystems. Smart watches are increasingly evolving into multifunctional wearable platforms capable of biometric monitoring, communication, contactless payments, productivity management, and remote healthcare integration.

The market is witnessing strong momentum due to growing demand for preventive healthcare solutions and lifestyle management technologies. Features such as ECG monitoring, blood oxygen tracking, sleep analytics, GPS navigation, and stress monitoring are significantly increasing adoption among health-conscious consumers. Technological advancements in AMOLED displays, low-power processors, and miniaturized sensors are also improving functionality and battery performance. In addition, ecosystem integration with smartphones, cloud services, digital assistants, and IoT devices is enhancing customer engagement and long-term retention.

North America continues to dominate the premium smart watch market due to strong consumer purchasing power and high digital health adoption, while Asia-Pacific is emerging as the fastest-growing regional market supported by manufacturing expansion, affordable pricing strategies, and rising middle-class demand in China and India. Enterprise adoption across logistics, manufacturing, healthcare, and workforce safety management is also expanding the addressable market beyond traditional consumer electronics applications.

Key Market Insights

- Health and wellness monitoring remains the largest application segment, driven by increasing demand for preventive healthcare and real-time biometric tracking.

- AMOLED display smart watches dominate premium wearable demand due to superior display quality, power efficiency, and enhanced user experience.

- North America leads the global market, supported by high adoption of premium wearable ecosystems and digital health technologies.

- Asia-Pacific is the fastest-growing regional market, driven by rapid wearable penetration across China, India, and Southeast Asia.

- Mid-range smart watches priced between USD 100–300 account for the largest market share, balancing affordability with advanced functionality.

- AI-powered health analytics and remote healthcare integration are reshaping the wearable ecosystem globally.

Smart Watch Market Trends

AI-Driven Health Monitoring and Personalized Analytics

Artificial intelligence integration is becoming a defining trend in the smart watch industry. Manufacturers are increasingly deploying AI-enabled algorithms capable of analyzing continuous biometric data such as heart rate variability, sleep patterns, blood oxygen levels, stress indicators, and physical activity. These systems generate personalized health recommendations, fitness coaching, and predictive wellness insights. Smart watches are gradually transitioning from passive monitoring devices into active health management platforms capable of identifying irregularities and providing preventive alerts. AI integration is also strengthening recurring revenue opportunities through subscription-based wellness services, cloud analytics, and connected healthcare ecosystems.

Standalone LTE and eSIM-Enabled Smart Watches Expanding

Demand for standalone smart watches with LTE and eSIM connectivity is rising globally as consumers seek wearable devices capable of independent communication without smartphone dependency. Standalone devices enable voice calls, messaging, GPS navigation, emergency communication, music streaming, and digital payments directly from the watch. Telecom operators are increasingly partnering with wearable manufacturers to expand connected wearable ecosystems and bundled data plans. This trend is particularly strong among fitness users, enterprise workers, and consumers seeking convenience during outdoor activities and travel.

Smart Watch Market Drivers

Growing Consumer Focus on Preventive Healthcare

The increasing prevalence of lifestyle-related diseases such as obesity, diabetes, hypertension, and cardiovascular disorders is driving global demand for wearable health-monitoring technologies. Consumers are increasingly prioritizing preventive healthcare and wellness management, resulting in strong adoption of smart watches equipped with ECG monitoring, sleep tracking, calorie monitoring, blood oxygen sensing, and stress analytics. Governments, healthcare providers, and insurers are also promoting digital health ecosystems and remote patient monitoring, further accelerating wearable device adoption.

Rapid Advancements in Wearable Technology

Technological innovation in sensors, displays, processors, and battery systems continues to improve smart watch functionality and user experience. Manufacturers are introducing advanced AMOLED displays, miniaturized health sensors, energy-efficient chipsets, and AI-powered software capabilities. Improved integration with smartphones, cloud platforms, IoT ecosystems, and digital assistants is strengthening consumer dependence on wearable technologies. Enhanced battery efficiency and waterproofing technologies are also improving device usability across fitness, sports, and industrial applications.

Smart Watch Market Restraints

Battery Life Limitations and Frequent Charging Requirements

Despite improvements in power efficiency, battery limitations remain a major challenge for the smart watch industry. Advanced functionalities such as continuous health monitoring, GPS tracking, LTE connectivity, and AMOLED displays consume substantial power, requiring frequent charging cycles. Consumers increasingly expect multi-day battery performance without compromising device functionality, creating engineering and design challenges for manufacturers.

Data Privacy and Cybersecurity Concerns

Smart watches continuously collect sensitive biometric and behavioral data, raising concerns related to cybersecurity, unauthorized access, and misuse of personal information. Regulatory requirements surrounding data protection and digital health compliance are becoming increasingly stringent across North America and Europe. Manufacturers must invest heavily in encryption technologies, cloud security infrastructure, and compliance systems to maintain consumer trust and regulatory approval.

Smart Watch Market Opportunities

Expansion of Remote Patient Monitoring Ecosystems

The rapid expansion of digital healthcare and telemedicine platforms presents significant opportunities for smart watch manufacturers. Hospitals, healthcare providers, insurers, and digital health startups are increasingly integrating wearable-generated biometric data into remote patient monitoring systems. Medical-grade smart watches capable of ECG tracking, arrhythmia detection, and chronic disease monitoring are expected to witness strong adoption, particularly among aging populations in North America, Europe, Japan, and China. Regulatory approvals for clinical-grade wearable technologies are likely to create new high-value revenue streams within healthcare ecosystems.

Affordable Smart Watch Penetration in Emerging Economies

Emerging economies such as India, Indonesia, Brazil, Vietnam, and parts of Africa present major growth opportunities due to rising smartphone penetration, improving internet infrastructure, and growing middle-class populations. Regional manufacturers are introducing competitively priced smart watches with fitness tracking, communication, and payment functionalities tailored for price-sensitive consumers. Aggressive online retail expansion and localized manufacturing initiatives are improving accessibility and supporting mass-market wearable adoption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 48.6 Billion |

| Market Size in 2026 | USD 55.02 Billion |

| Market Size in 2031 | USD 102.26 Billion |

| CAGR | 13.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Operating System Insights

WatchOS-based smart watches dominate the global market with approximately 32% revenue share in 2025 due to strong ecosystem integration, premium user experience, and high customer loyalty within the Apple ecosystem. Android Wear / Wear OS smart watches continue to maintain strong market presence through broad smartphone compatibility and increasing support from Samsung and Google ecosystems. Proprietary operating systems developed by Chinese manufacturers are gaining traction in emerging markets due to lower hardware requirements, extended battery life, and competitive pricing strategies. Hybrid operating systems are also emerging in niche categories where battery efficiency and limited smart functionality are prioritized over advanced app ecosystems.

Product Type Insights

Extension smart watches account for nearly 39% of the global market due to their ability to complement smartphone functionality through notifications, communication, and fitness tracking. Standalone smart watches are among the fastest-growing segments as LTE connectivity enables independent calling, GPS tracking, and mobile payments without requiring smartphone pairing. Fitness-focused smart watches remain highly popular among health-conscious consumers and athletes due to advanced activity tracking and sports analytics. Luxury smart watches are expanding in North America and Europe as consumers increasingly demand premium aesthetics combined with digital functionality. Rugged and outdoor smart watches are witnessing growing demand across military, industrial, and adventure sports applications due to enhanced durability and GPS capabilities.

Application Insights

Health and wellness monitoring remains the leading application segment, accounting for approximately 34% of the global smart watch market in 2025. Consumers increasingly rely on wearable devices for continuous heart rate monitoring, sleep analysis, stress tracking, and physical activity management. Fitness and sports tracking applications continue to experience strong adoption among athletes, gym users, and recreational fitness consumers. Mobile payments and contactless transaction capabilities are becoming increasingly important in urban digital ecosystems. Enterprise and workforce management applications are emerging rapidly in industries such as logistics, manufacturing, construction, and mining, where smart watches are being used for employee safety monitoring, communication, and productivity management.

Distribution Channel Insights

Online retail channels dominate the smart watch market, accounting for nearly 58% of global sales in 2025. E-commerce platforms provide consumers with access to broad product portfolios, competitive pricing, customer reviews, and convenient purchasing experiences. Brand-owned online stores are increasingly strengthening direct-to-consumer engagement strategies through product customization, subscription services, and ecosystem bundling. Multi-brand electronics retailers continue to play an important role in premium smart watch sales by offering in-store product demonstrations and customer support. Telecom operator stores are also emerging as important distribution channels for LTE-enabled wearable devices bundled with connectivity plans.

End User Insights

Consumer and individual users represent approximately 76% of total smartwatch market revenue globally, driven by rising fitness awareness, digital lifestyle adoption, and increasing health consciousness. Healthcare institutions are among the fastest-growing end-use segments as wearable technologies become integrated into remote patient monitoring systems and telemedicine platforms. Corporate and enterprise users are increasingly deploying smart watches for workforce productivity management, employee safety monitoring, and logistics coordination. Sports organizations and fitness institutions are also adopting advanced wearable analytics for athlete performance tracking and injury prevention.

Explore more data points, trends and opportunities Download Free Sample Report

Smart Watch Market Segmentations

By Product Type

- Extension Smart Watches

- Standalone Smart Watches

- Hybrid Smart Watches

- Fitness-focused Smart Watches

- Luxury Smart Watches

- Kids Smart Watches

- Rugged / Outdoor Smart Watches

- Medical-grade Smart Watches

By Application

- Health & Wellness Monitoring

- Fitness & Sports Tracking

- Communication & Notifications

- Navigation & Location Tracking

- Mobile Payments & Digital Wallets

- Enterprise & Workforce Management

- Remote Patient Monitoring

- Lifestyle & Entertainment

By Distribution Channel

- Online Retail

- Brand-owned Stores

- Multi-brand Electronics Retailers

- Telecom Operator Stores

- Specialty Sports & Fitness Stores

- Healthcare Device Retailers

Regional Insights

North America

North America accounted for approximately 36% of the global smart watch market in 2025, led primarily by the United States. High disposable income, strong digital healthcare adoption, widespread smartphone penetration, and consumer preference for premium wearable ecosystems continue to support market leadership. The United States dominates regional demand due to extensive adoption of Apple Watch and Samsung Galaxy Watch ecosystems. Canada is also witnessing stable growth supported by increasing fitness awareness and healthcare digitization initiatives.

Europe

Europe represented nearly 24% of global smart watch revenue in 2025. Germany, the United Kingdom, France, Italy, and Nordic countries are major contributors to regional demand. European consumers increasingly prefer premium wearable devices with advanced health-monitoring capabilities and sustainability-focused product designs. Regulatory support for digital healthcare integration and aging populations are accelerating wearable adoption across the region.

Asia-Pacific

Asia-Pacific accounted for approximately 30% of global smart watch market revenue in 2025 and remains the fastest-growing regional market. China dominates both manufacturing and consumption due to strong domestic production ecosystems and affordable product availability. India is emerging as one of the fastest-growing national markets globally, driven by rising smartphone penetration, growing middle-class income, and aggressive pricing by domestic and Chinese wearable brands. Japan and South Korea continue to demonstrate strong demand for technologically advanced and premium wearable devices.

Latin America

Latin America accounted for nearly 6% of global demand in 2025, with Brazil and Mexico representing the largest regional markets. Improving digital infrastructure, expanding e-commerce channels, and rising awareness regarding fitness tracking technologies are supporting market growth. Affordable smart watch models are particularly gaining traction among younger urban consumers.

Middle East & Africa

The Middle East & Africa region represented approximately 4% of the global smart watch market in 2025. The UAE and Saudi Arabia are leading regional markets due to strong consumer spending power and digital transformation initiatives. Governments across the Gulf region are promoting connected healthcare infrastructure and smart city initiatives, supporting wearable technology adoption. South Africa also remains an important regional market due to growing consumer electronics demand and expanding mobile connectivity.

Key Players in the Smart Watch Market

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- Garmin Ltd.

- Google LLC

- Fitbit (Google)

- Amazfit / Zepp Health Corporation

- Fossil Group Inc.

- Polar Electro Oy

- Suunto Oy

- Mobvoi Information Technology Company Limited

- Noise

- boAt Lifestyle

- Casio Computer Co., Ltd.