Raw Dog Food Market Size

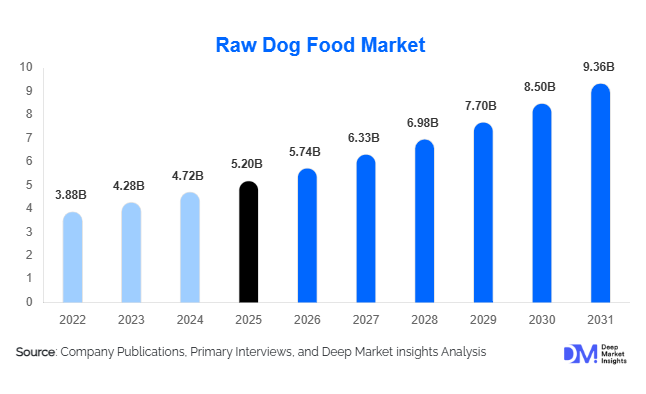

According to Deep Market Insights, the global raw dog food market size was valued at USD 5.2 billion in 2025 and is projected to grow from USD 5.74 billion in 2026 to reach USD 9.36 billion by 2031, expanding at a CAGR of 10.3% during the forecast period (2026–2031). The raw dog food market growth is primarily driven by increasing pet humanization, rising consumer preference for minimally processed pet nutrition, growing awareness regarding canine digestive health, and expanding demand for biologically appropriate raw food (BARF) diets. Consumers are increasingly seeking premium pet nutrition solutions containing natural ingredients, high-quality animal proteins, and limited processing, positioning raw dog food as one of the fastest-growing segments within the broader premium pet food industry.

Key Market Insights

- Frozen raw dog food remains the largest product category, accounting for nearly 38% of global market revenue due to superior nutrient retention and consumer perception of freshness.

- Chicken-based formulations dominate protein demand, representing approximately 29% of total market sales because of affordability, digestibility, and widespread availability.

- North America dominates the global market, supported by high pet ownership rates, premiumization trends, and strong direct-to-consumer distribution networks.

- Asia-Pacific is the fastest-growing region, led by increasing pet adoption rates and rising disposable incomes across China, India, South Korea, and Southeast Asia.

- Online retail and subscription-based sales channels are expanding rapidly, allowing manufacturers to strengthen customer retention and improve profitability.

- Functional raw nutrition products, including formulations targeting digestive health, immunity, allergies, and joint care, are becoming major growth drivers across premium consumer segments.

Raw Dog Food Market Trends

Premium Human-Grade Nutrition Driving Product Innovation

Pet owners increasingly view dogs as family members, creating strong demand for premium nutrition products that mirror human dietary preferences. Raw dog food manufacturers are responding through human-grade ingredients, ethically sourced proteins, organic vegetables, and transparent supply chains. Consumers are actively seeking clean-label formulations free from artificial preservatives, fillers, grains, and synthetic additives. Premiumization is also driving demand for single-protein diets, limited-ingredient recipes, and customized meal plans. Companies are increasingly investing in nutritional research, ingredient traceability systems, and enhanced quality control measures to differentiate products within an increasingly competitive market. This trend is expected to continue driving average selling prices upward while supporting long-term market value growth.

Rapid Expansion of Freeze-Dried and Functional Raw Diets

Freeze-dried raw dog food is emerging as one of the fastest-growing product categories due to its convenience, extended shelf life, and preservation of nutritional integrity. Consumers appreciate the ability to store and transport freeze-dried products without refrigeration while maintaining many benefits associated with frozen raw diets. Simultaneously, functional nutrition is becoming a major purchasing criterion. Manufacturers are incorporating probiotics, omega fatty acids, joint-support ingredients, immune-enhancing nutrients, and digestive health supplements into raw formulations. These products appeal to owners seeking preventive health solutions and veterinary-supported nutritional approaches. The combination of convenience and functionality is creating a significant premium segment within the global raw dog food market.

Raw Dog Food Market Drivers

Growing Pet Humanization and Premium Spending

Pet humanization continues to be the most significant growth driver for the raw dog food market. Across developed and emerging economies, dog owners are increasingly willing to spend on premium products that improve pet health and longevity. Consumers are shifting away from conventional kibble toward minimally processed alternatives that more closely resemble natural canine diets. This trend has substantially increased spending on premium pet nutrition, with raw food products often commanding significantly higher prices than traditional pet foods. The willingness of consumers to invest in health-focused nutrition remains a fundamental factor supporting market expansion.

Increasing Awareness of Canine Health and Wellness

Rising awareness regarding obesity, digestive disorders, food sensitivities, allergies, and skin conditions in dogs is encouraging pet owners to adopt specialized nutritional solutions. Raw diets are increasingly perceived as supporting improved digestion, enhanced coat quality, stronger immunity, and better energy levels. Veterinary nutrition education, social media influence, and growing access to pet health information are accelerating consumer adoption of raw feeding practices. The growing emphasis on preventive healthcare for pets is expected to sustain demand throughout the forecast period.

Raw Dog Food Market Restraints

Food Safety and Regulatory Compliance Challenges

Food safety concerns remain a major challenge for market participants. Regulatory authorities in several countries continue to monitor risks associated with bacterial contamination, including Salmonella, E. coli, and Listeria. Manufacturers must invest heavily in pathogen testing, high-pressure processing technologies, traceability systems, and quality assurance programs to comply with evolving regulatory standards. These requirements increase production costs and create barriers for smaller manufacturers seeking market entry.

Higher Product Costs Compared to Conventional Pet Food

Raw dog food products remain significantly more expensive than traditional kibble due to premium ingredient sourcing, cold-chain logistics requirements, specialized manufacturing processes, and rigorous safety testing. Although premium consumers are willing to pay higher prices, cost remains a limiting factor for mainstream adoption. Economic uncertainty and inflationary pressures can further affect consumer purchasing behavior, particularly within price-sensitive market segments.

Raw Dog Food Market Opportunities

Expansion Across Emerging Asia-Pacific Pet Care Markets

Asia-Pacific presents one of the most attractive growth opportunities for raw dog food manufacturers. Rapid urbanization, increasing pet ownership, and rising disposable incomes are creating substantial demand for premium pet nutrition across China, India, Indonesia, Thailand, Vietnam, and South Korea. As awareness regarding pet health continues to improve, consumers are increasingly adopting premium and specialized feeding solutions. Companies establishing local production facilities, regional partnerships, and localized product offerings are expected to gain significant competitive advantages within these high-growth markets.

Direct-to-Consumer and Subscription-Based Business Models

The continued expansion of direct-to-consumer (DTC) sales channels provides significant opportunities for both established companies and new entrants. Subscription-based delivery models enable predictable recurring revenues, improved customer retention, and enhanced consumer convenience. Personalized feeding plans supported by digital platforms and data analytics are creating additional value propositions. Manufacturers can also achieve higher profit margins through DTC channels by reducing dependence on traditional retail intermediaries. As online pet food purchasing continues to expand globally, subscription-based raw dog food services are expected to become an increasingly important growth engine.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.2 Billion |

| Market Size in 2026 | USD 5.74 Billion |

| Market Size in 2031 | USD 9.36 Billion |

| CAGR | 10.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Format Insights

Frozen raw dog food dominates the market, accounting for approximately 38% of global revenue in 2025. Consumers perceive frozen products as offering the highest nutritional integrity and freshness while preserving natural proteins, vitamins, and enzymes. Freeze-dried raw dog food is emerging as the fastest-growing segment due to convenience, portability, and longer shelf life. Air-dried and dehydrated products continue gaining popularity among consumers seeking alternatives that combine nutritional benefits with easier storage requirements. Raw treats, toppers, and mixers are also experiencing increased demand as pet owners gradually incorporate raw nutrition into traditional feeding routines without fully transitioning to complete raw diets.

Protein Source Insights

Chicken-based raw dog food remains the largest protein segment, representing nearly 29% of global market demand due to affordability, broad availability, and strong acceptance among dogs. Beef-based products constitute the second-largest category, benefiting from premium positioning and high protein content. Turkey and lamb formulations are increasingly utilized in allergy-sensitive and limited-ingredient diets. Fish-based products are gaining traction due to growing consumer awareness of omega-3 fatty acids and their benefits for skin, coat, and cognitive health. Exotic proteins such as venison, rabbit, duck, and bison continue to attract premium consumers seeking novel protein alternatives for dogs with food sensitivities.

Distribution Channel Insights

Online retail channels account for approximately 31% of global raw dog food sales and represent the fastest-growing distribution segment. E-commerce platforms, manufacturer websites, and subscription-based delivery services are transforming purchasing behavior through convenience and recurring delivery models. Pet specialty stores continue to maintain a strong presence due to personalized recommendations and premium product assortments. Veterinary clinics are becoming increasingly important sales channels for therapeutic and functional raw nutrition products. Independent pet retailers and premium supermarkets also contribute significantly to market penetration across developed regions.

End-User Insights

Household pet owners represent the dominant end-user segment, accounting for approximately 74% of total market demand. Increasing awareness regarding canine health and wellness continues to drive adoption among individual consumers. Professional breeders are expanding their use of raw diets to improve breeding outcomes and puppy development. Kennels, boarding facilities, and working dog organizations are increasingly incorporating premium nutrition programs to enhance canine performance and overall health. Veterinary nutrition programs represent one of the fastest-growing end-user categories as specialized raw diets gain acceptance for digestive health, allergy management, and weight control applications.

Explore more data points, trends and opportunities Download Free Sample Report

Raw Dog Food Market Segmentations

By Product Format

- Frozen Raw Dog Food

- Freeze-Dried Raw Dog Food

- Air-Dried Raw Dog Food

- Dehydrated Raw Dog Food

- Raw Frozen Nuggets/Patties

- Raw Complete Meal Formulations

- Raw Treats & Snacks

- Raw Mixers & Toppers

By Protein Source

- Chicken-Based

- Beef-Based

- Turkey-Based

- Lamb-Based

- Fish & Seafood-Based

- Duck-Based

- Venison-Based

- Rabbit-Based

- Exotic Proteins (Bison, Kangaroo, Quail, etc.)

By Nutritional Formulation

- Complete & Balanced Diets

- Limited Ingredient Diets

- Grain-Free Raw Diets

- Organic Raw Diets

- Functional Raw Diets

- Veterinary-Specific Raw Diets

By Distribution Channel

- Pet Specialty Stores

- Veterinary Clinics

- Independent Pet Retailers

- Supermarkets & Hypermarkets

- Online Retail/E-commerce

- Direct-to-Consumer Subscription Platforms

By End User

- Household Pet Owners

- Professional Breeders

- Kennels & Boarding Facilities

- Working Dog Organizations

- Animal Shelters & Rescue Centers

- Veterinary Nutrition Programs

Regional Insights

North America

North America accounts for approximately 38% of the global raw dog food market and remains the largest regional market. The United States alone contributes nearly 32% of global demand, supported by high pet ownership rates, advanced cold-chain infrastructure, strong premiumization trends, and widespread consumer acceptance of alternative pet nutrition. Canada continues to experience robust growth due to increasing demand for premium pet food and expanding online distribution channels. The region benefits from strong consumer purchasing power and a highly developed pet care ecosystem.

Europe

Europe represents approximately 31% of global market revenue and remains one of the most mature raw feeding markets worldwide. The United Kingdom, Germany, France, and the Netherlands are major contributors to regional demand. Consumers across Europe demonstrate strong interest in natural feeding approaches, sustainability, animal welfare, and ingredient transparency. Established raw feeding communities and stringent product quality standards continue to support long-term market growth throughout the region.

Asia-Pacific

Asia-Pacific accounts for approximately 22% of global demand and is projected to register the fastest growth through 2031. China represents the largest market within the region and is expected to achieve annual growth exceeding 15% during the forecast period. Rising urbanization, increasing pet ownership, and growing disposable incomes are driving demand for premium pet nutrition products. India, South Korea, Japan, and Australia are also emerging as important growth markets as consumer awareness regarding pet health continues to expand.

Latin America

Latin America accounts for approximately 5% of the global market, with Brazil representing the dominant regional market. Increasing pet ownership, improving economic conditions, and growing awareness regarding premium pet nutrition are supporting demand growth. Mexico and Argentina are also witnessing rising adoption of premium and specialty pet food products. Although market penetration remains relatively low compared to developed regions, long-term growth prospects remain favorable.

Middle East & Africa

The Middle East & Africa region contributes approximately 4% of global market revenue. The United Arab Emirates and Saudi Arabia are emerging as premium pet food markets due to rising disposable incomes and increasing pet ownership among urban consumers. South Africa remains the largest market within Africa, supported by a developed pet care industry and growing consumer awareness regarding premium nutrition. Expanding retail infrastructure and e-commerce penetration are expected to support future market development across the region.

Key Players in the Raw Dog Food Market

- Stella & Chewy's

- Primal Pet Foods

- Instinct Pet Food

- We Feed Raw

- Bravo Pet Foods

- Vital Essentials

- Steve's Real Food

- Northwest Naturals

- Raw Bistro

- K9 Natural

- Ziwi Peak

- Natural Instinct

- Natures Menu

- Carnivora

- Nature's Diet