PET Composite Copper Foil Market Size

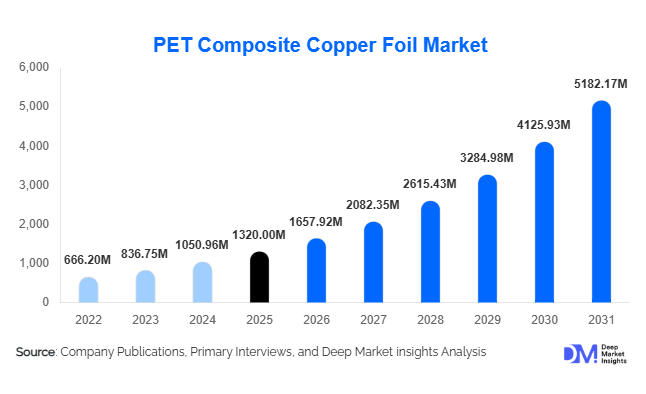

According to Deep Market Insights, the global PET Composite Copper Foil market size was valued at USD 1,320 million in 2025 and is projected to grow from USD 1,657.92 million in 2026 to reach USD 5,182.17 million by 2031, expanding at a CAGR of 25.6% during the forecast period (2026–2031). The market growth is primarily driven by the rapid expansion of electric vehicle (EV) production, increasing investments in lithium-ion battery manufacturing, and growing adoption of lightweight current collector materials that improve battery energy density and safety. PET composite copper foil combines ultra-thin copper layers with PET substrates, enabling substantial reductions in copper consumption while maintaining conductivity and structural performance. As battery manufacturers seek to reduce battery weight and improve charging efficiency, PET composite copper foil is emerging as a key material for next-generation lithium-ion, sodium-ion, and solid-state battery architectures.

Key Market Insights

- PET composite copper foil is increasingly replacing conventional electrolytic copper foil due to its ability to reduce copper usage by up to 50% while improving battery safety.

- Electric vehicle batteries account for more than 58% of total market demand, making automotive electrification the primary growth engine.

- Asia-Pacific dominates the global market with approximately 76% share, supported by China's extensive battery manufacturing ecosystem.

- India is emerging as the fastest-growing country market, driven by battery localization initiatives, EV manufacturing investments, and government incentive programs.

- Energy storage systems (ESS) represent the fastest-growing application segment, benefiting from renewable energy integration and grid modernization projects worldwide.

- Technological advancements in sputtering and roll-to-roll manufacturing are improving production yields and accelerating commercialization across global battery supply chains.

PET Composite Copper Foil Market Trends

Shift Toward Ultra-Thin Composite Current Collectors

Battery manufacturers are increasingly adopting ultra-thin PET composite copper foil structures to maximize energy density while minimizing battery weight. The transition toward thinner current collectors is particularly evident in electric vehicle and premium consumer electronics applications where energy efficiency and compact battery design are critical. Manufacturers are investing heavily in advanced sputtering and electroplating technologies capable of producing highly uniform copper layers below 6 μm thickness. These innovations not only reduce copper consumption but also improve thermal management and battery cycle life. As battery cell manufacturers pursue higher-performance architectures, ultra-thin composite copper foil is expected to become a standard component in next-generation battery designs.

Growing Adoption in Energy Storage Systems

Grid-scale energy storage projects are emerging as a major demand driver for PET composite copper foil. Utility operators are increasingly deploying large-scale battery systems to support renewable energy integration, peak-load balancing, and grid stabilization. Composite current collectors offer improved safety characteristics and lower raw material requirements compared to conventional copper foil, making them attractive for stationary energy storage applications. As governments expand renewable energy capacity and strengthen grid resilience initiatives, ESS installations are expected to create a significant secondary growth avenue beyond electric vehicles. Manufacturers are actively developing specialized composite copper foil solutions optimized for long-duration energy storage and high-cycle applications.

PET Composite Copper Foil Market Drivers

Rapid Expansion of Electric Vehicle Production

The accelerating adoption of electric vehicles globally is creating substantial demand for advanced battery materials. Automakers are increasingly prioritizing lightweight battery components that enhance driving range and improve overall vehicle efficiency. PET composite copper foil contributes directly to these objectives by reducing battery weight while maintaining high electrical conductivity. Growing EV production across China, Europe, North America, and emerging Asian markets continues to stimulate demand for battery-grade composite current collectors. Government incentives, stricter emission regulations, and rising consumer acceptance of EVs further reinforce this growth trajectory.

Need for Copper Consumption Optimization

Copper remains one of the most significant cost contributors in battery manufacturing. Volatility in copper prices has encouraged battery producers to seek alternatives that reduce raw material dependence without compromising performance. PET composite copper foil can lower copper usage by approximately 40–60%, offering substantial material savings at scale. This cost advantage is becoming increasingly important as battery manufacturers strive to improve profitability while maintaining competitive pricing in rapidly expanding EV and energy storage markets.

Growing Emphasis on Battery Safety

Battery safety has become a critical priority across automotive, consumer electronics, and energy storage industries. PET composite copper foil improves safety performance by reducing metal mass and enhancing structural stability within battery cells. Regulatory authorities and OEMs are increasingly focusing on thermal management and thermal runaway prevention, encouraging the adoption of advanced current collector materials. As safety standards become more stringent globally, PET composite copper foil is expected to gain wider acceptance among battery manufacturers.

PET Composite Copper Foil Market Restraints

High Manufacturing Complexity and Capital Requirements

The production of PET composite copper foil requires sophisticated vacuum sputtering, electroplating, and roll-to-roll processing technologies. These manufacturing processes involve substantial capital expenditure and require highly specialized technical expertise. Production yield optimization remains a challenge for new entrants, limiting rapid capacity expansion outside established manufacturing hubs. High equipment costs and lengthy qualification procedures continue to act as barriers for companies seeking to enter the market.

Lengthy OEM Qualification Cycles

Battery manufacturers typically conduct extensive testing and validation before approving new materials for commercial use. PET composite copper foil suppliers must undergo rigorous qualification processes related to conductivity, durability, adhesion strength, and safety performance. These qualification cycles can extend for several years, delaying commercialization and limiting the speed at which innovative products can penetrate the market. The dependence on long-term supply agreements also creates challenges for emerging suppliers seeking to establish market presence.

PET Composite Copper Foil Market Opportunities

Battery Manufacturing Localization Initiatives

Governments worldwide are actively supporting domestic battery production through incentives, subsidies, and localization mandates. New battery gigafactories being developed across North America, Europe, India, and Southeast Asia require reliable access to advanced battery materials. PET composite copper foil manufacturers that establish local production facilities near battery manufacturing clusters can secure long-term supply contracts while reducing logistics costs. This trend is expected to create significant opportunities for both established players and new entrants.

Commercialization of Sodium-Ion and Solid-State Batteries

Emerging battery technologies are creating new demand opportunities for advanced current collectors. Sodium-ion and solid-state batteries require lightweight, high-performance materials capable of supporting improved energy density and enhanced safety characteristics. PET composite copper foil is well positioned to benefit from the commercialization of these next-generation battery chemistries. Companies that develop specialized products tailored to emerging battery platforms are expected to gain early-mover advantages and command premium pricing.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1320 Million |

| Market Size in 2026 | USD 1657.92 Million |

| Market Size in 2031 | USD 5182.17 Million |

| CAGR | 25.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

PET composite copper foil for lithium-ion batteries dominates the market, accounting for approximately 67% of total revenue in 2025. The segment benefits from strong demand across electric vehicles, energy storage systems, and consumer electronics. Lithium-ion battery manufacturers continue to prioritize lightweight current collectors that improve battery efficiency and reduce material consumption. Sodium-ion battery applications are emerging as a promising growth segment, supported by increasing investments in alternative battery chemistries for stationary storage and cost-sensitive transportation applications. Solid-state battery applications are expected to witness significant growth during the forecast period as commercialization efforts accelerate globally.

Manufacturing Technology Insights

Hybrid sputtering-electroplating technology represents the leading manufacturing segment, accounting for approximately 42% of the global market. The technology offers an optimal balance between production efficiency, copper adhesion strength, and cost competitiveness. Roll-to-roll continuous deposition systems are gaining adoption as manufacturers scale commercial production capacities. Vacuum magnetron sputtering remains critical for achieving ultra-thin copper layers and high-performance battery applications, while advancements in electroplating technologies continue to improve manufacturing yields and reduce production costs.

Thickness Insights

The 4–6 μm thickness segment holds the largest market share at nearly 39% of global demand. This thickness range provides an ideal balance between conductivity, mechanical strength, and weight reduction. Battery manufacturers increasingly favor this category because it enables higher energy density while maintaining production reliability. Ultra-thin foil segments below 4 μm are experiencing rapid growth as EV and premium electronics manufacturers pursue next-generation battery designs with enhanced performance characteristics.

End-Use Industry Insights

Electric vehicles represent the largest end-use industry, accounting for approximately 54% of global PET composite copper foil consumption in 2025. The segment continues to benefit from rising EV adoption and growing battery production capacities worldwide. Battery manufacturing companies constitute the second-largest consumer group, supplying materials to automotive, consumer electronics, and energy storage sectors. Energy storage systems are emerging as the fastest-growing end-use segment, driven by renewable energy deployment, grid modernization initiatives, and increasing investments in utility-scale battery projects. Aerospace, defense electronics, and industrial automation applications are also creating niche demand opportunities for high-performance composite current collectors.

Explore more data points, trends and opportunities Download Free Sample Report

PET Composite Copper Foil Market Segmentations

By Product Type

- PET Composite Copper Foil for Lithium-Ion Batteries

- PET Composite Copper Foil for Sodium-Ion Batteries

- PET Composite Copper Foil for Solid-State Batteries

- PET Composite Copper Foil for Printed Circuit Applications

- PET Composite Copper Foil for Electromagnetic Shielding Applications

By Manufacturing Technology

- Vacuum Magnetron Sputtering

- Water Plating / Electroplating

- Hybrid Sputtering-Electroplating

- Roll-to-Roll Continuous Deposition

By Copper Layer Structure

- Single-Sided PET Composite Copper Foil

- Double-Sided PET Composite Copper Foil

By Thickness

- Below 4 μm

- 4–6 μm

- 6–8 μm

- Above 8 μm

By Battery Application

- EV Power Batteries

- Plug-in Hybrid Batteries

- Energy Storage System (ESS) Batteries

- Consumer Electronics Batteries

- Power Tool Batteries

Regional Insights

Asia-Pacific

Asia-Pacific dominates the PET composite copper foil market with approximately 76% share of global revenue. China alone accounts for nearly 58% of worldwide demand, supported by its leadership in battery manufacturing, electric vehicle production, and advanced materials processing. South Korea and Japan remain important markets due to their strong presence in battery technology development and consumer electronics manufacturing. India is emerging as the fastest-growing market within the region, supported by government-backed battery manufacturing programs and expanding EV production capacity. Taiwan and Southeast Asia are also witnessing increasing investments in battery supply chain infrastructure.

North America

North America accounts for roughly 10% of global market demand, led by the United States. Significant investments in battery gigafactories, EV manufacturing facilities, and domestic battery supply chains are driving market expansion. Federal incentives supporting clean energy technologies and battery localization are creating favorable conditions for PET composite copper foil adoption. Canada is also strengthening its position through critical mineral development and battery manufacturing investments.

Europe

Europe represents approximately 9% of global market revenue. Germany remains the largest regional market due to its strong automotive industry and substantial investments in battery manufacturing. France, Sweden, Hungary, and Poland are becoming important battery production hubs as European governments accelerate energy transition initiatives. Increasing focus on battery sustainability and supply chain security is supporting demand for advanced current collector materials across the region.

Latin America

Latin America accounts for nearly 3% of global demand, with Brazil and Mexico serving as the primary markets. Growing automotive manufacturing activities and increasing interest in battery assembly operations are supporting regional market development. Although adoption remains at an early stage, expanding electrification efforts are expected to stimulate future demand for PET composite copper foil.

Middle East & Africa

The Middle East & Africa region contributes approximately 2% of global market revenue. Saudi Arabia and the United Arab Emirates are investing heavily in battery manufacturing, renewable energy projects, and industrial diversification initiatives. South Africa remains a key participant due to its established industrial base and growing involvement in battery value chains. Increasing deployment of energy storage systems is expected to support future regional growth.

Key Players in the PET Composite Copper Foil Market

- Jiangsu Double Star New Material

- Baoming Technology

- SK Nexilis

- ILJIN Materials

- Solus Advanced Materials

- Furukawa Electric

- Mitsui Mining & Smelting

- Nan Ya Plastics

- JX Advanced Metals

- Doosan Corporation

- Kingboard Holdings

- Chang Chun Group

- Toyo Ink SC Holdings

- LCY Technology

- Nordson Electronic Materials