Personalized Jewelry Market Size

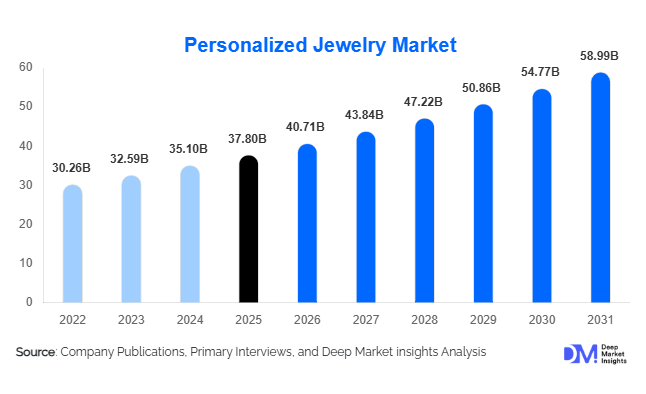

According to Deep Market Insights, the global personalized jewelry market size was valued at USD 37.8 billion in 2025 and is projected to grow from USD 40.71 billion in 2026 to reach USD 58.99 billion by 2031, expanding at a CAGR of 7.7% during the forecast period (2026–2031). The personalized jewelry market growth is primarily driven by rising consumer preference for individualized luxury products, increasing demand for emotionally meaningful gifting, and the rapid adoption of digital customization technologies. Personalized jewelry has evolved beyond traditional engraving to include birthstones, fingerprints, handwritten messages, coordinates, photo jewelry, and fully bespoke designs. Growing disposable incomes, strong e-commerce penetration, and advancements in computer-aided design (CAD), 3D printing, and laser engraving are enabling manufacturers to deliver highly customized products at scale while reducing production lead times.

Key Market Insights

- Personalized gifting continues to drive market growth, with birthdays, anniversaries, weddings, and milestone celebrations accounting for a significant share of global demand.

- Online sales channels represent the fastest-growing distribution segment, supported by virtual try-on tools, AI-powered customization platforms, and direct-to-consumer business models.

- Asia-Pacific dominates the global market, led by China and India, where cultural affinity for jewelry and rising disposable incomes support strong demand.

- North America remains a major premium market, benefiting from high consumer spending, digital retail maturity, and strong adoption of personalized luxury products.

- Sustainable and ethically sourced jewelry is gaining importance, particularly among Millennials and Generation Z consumers seeking environmentally responsible purchases.

- Technology integration is reshaping customization capabilities, including AI-assisted design recommendations, 3D modeling, rapid prototyping, and personalized shopping experiences.

Personalized Jewelry Market Trends

Rise of Emotional and Meaning-Based Purchasing

Consumers increasingly view jewelry as a medium for storytelling, emotional expression, and personal identity. Rather than purchasing generic accessories, buyers are seeking products that commemorate important life events, relationships, and achievements. Name necklaces, birthstone jewelry, fingerprint engravings, and custom family designs have become highly popular among younger consumers. Social media platforms have amplified this trend by showcasing personalized pieces as symbols of individuality and self-expression. Brands are increasingly offering extensive customization options that allow consumers to participate in the design process, creating stronger emotional attachment and higher willingness to pay premium prices.

Digital Manufacturing and Mass Customization Expansion

Advancements in digital manufacturing technologies are transforming the personalized jewelry industry. CAD software, 3D printing, laser engraving systems, and AI-driven design tools enable manufacturers to produce customized pieces with greater precision and shorter lead times. These technologies reduce inventory requirements while improving scalability and operational efficiency. E-commerce platforms are integrating visualization tools, augmented reality try-on features, and real-time customization interfaces that allow consumers to design products before purchase. The convergence of technology and craftsmanship is expanding accessibility to personalized jewelry across both premium and mass-market price segments.

Personalized Jewelry Market Drivers

Growing Demand for Personalized Gifting

Gift-giving remains one of the strongest drivers of personalized jewelry demand globally. Consumers increasingly prefer customized products that carry emotional significance compared to traditional gifts. Weddings, anniversaries, birthdays, graduations, Mother’s Day, Valentine’s Day, and other celebrations continue to generate substantial demand for engraved and customized jewelry products. Personalized gifts often command higher perceived value and create stronger emotional connections, encouraging repeat purchases and premium pricing opportunities for manufacturers.

Expansion of E-Commerce and Direct-to-Consumer Sales

The rapid growth of online retail has significantly expanded market accessibility. Consumers can now customize products through interactive websites, mobile applications, and social commerce platforms. Direct-to-consumer brands have leveraged digital marketing, influencer partnerships, and online customization tools to reach broader audiences while reducing dependence on traditional retail channels. Improved logistics and fulfillment capabilities have further enhanced customer convenience, supporting sustained market expansion.

Personalized Jewelry Market Restraints

Volatility in Precious Metal and Gemstone Prices

Fluctuations in gold, silver, platinum, and gemstone prices remain a major challenge for manufacturers and retailers. Rising raw material costs can reduce profit margins and increase retail pricing, potentially impacting consumer demand. Smaller manufacturers are particularly vulnerable to commodity price volatility due to limited purchasing power and hedging capabilities.

Counterfeit Products and Market Fragmentation

The personalized jewelry industry remains highly fragmented, with numerous online sellers competing on price rather than quality. Counterfeit products, imitation precious metals, and inconsistent product quality can undermine consumer trust and negatively impact established brands. Maintaining authenticity, craftsmanship standards, and brand reputation remains critical for long-term success.

Personalized Jewelry Market Opportunities

AI-Powered Design and Customization Platforms

Artificial intelligence is creating significant opportunities for personalized jewelry brands. AI-powered recommendation engines, generative design platforms, and virtual design assistants enable customers to create unique jewelry pieces with minimal design expertise. These technologies improve conversion rates, enhance customer engagement, and reduce design costs. New entrants can leverage AI-native business models to compete effectively with established players while offering highly personalized shopping experiences.

Sustainable and Ethical Personalized Jewelry

Growing consumer awareness of environmental and social responsibility is creating opportunities for sustainable personalized jewelry. Brands utilizing recycled precious metals, ethically sourced gemstones, lab-grown diamonds, and transparent supply chains are gaining competitive advantages. Sustainability-focused collections resonate particularly well with younger consumers who increasingly align purchasing decisions with environmental values. This trend supports premium pricing and strengthens long-term customer loyalty.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 37.8 Billion |

| Market Size in 2026 | USD 40.71 Billion |

| Market Size in 2031 | USD 58.99 Billion |

| CAGR | 7.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Necklaces and pendants account for the largest share of the personalized jewelry market, representing approximately 34% of global revenue in 2025. Their popularity stems from versatility, gifting appeal, and broad customization options including names, initials, birthstones, coordinates, and photo lockets. Rings represent another significant category driven by wedding, engagement, and relationship-oriented purchases. Personalized bracelets continue to gain popularity among younger consumers seeking affordable yet meaningful accessories. Earrings and specialty products such as customized cufflinks, anklets, and commemorative jewelry contribute to market diversification. The increasing preference for unique self-expression is encouraging consumers to invest in multiple personalized jewelry categories rather than single-product purchases.

Material Insights

Gold remains the dominant material segment, accounting for approximately 41% of global personalized jewelry revenue. Strong cultural significance, investment value, and premium positioning continue to support gold jewelry demand across Asia-Pacific, the Middle East, and North America. Sterling silver remains highly popular in mid-priced and fashion-oriented segments due to affordability and versatility. Diamond and gemstone-based personalized jewelry continue gaining traction in premium and luxury categories, while alternative materials such as titanium, stainless steel, resin, and recycled materials are increasingly being adopted by sustainability-focused brands. The growing popularity of lab-grown diamonds is further reshaping material preferences across multiple consumer demographics.

Customization Type Insights

Engraving-based customization represents the largest personalization category, accounting for nearly 29% of market revenue. Consumers continue to favor engraved names, dates, messages, and symbols due to their affordability and emotional significance. Birthstone customization remains highly popular for family-themed and commemorative jewelry. Fingerprint, handwriting, and signature jewelry are emerging as premium personalization categories, particularly within luxury gifting segments. Fully bespoke jewelry design services are gaining traction among affluent consumers seeking exclusive and one-of-a-kind pieces that reflect personal stories and heritage.

Distribution Channel Insights

Online channels account for approximately 44% of global personalized jewelry sales and represent the fastest-growing distribution segment. Brand websites, e-commerce marketplaces, and social commerce platforms enable consumers to customize products directly while benefiting from extensive product visualization tools. Traditional jewelry stores remain important, particularly for premium and luxury purchases where consumers value in-person consultation and product evaluation. Independent jewelers and specialty boutiques continue to play a significant role in high-end customization and bespoke design services. Omnichannel strategies are becoming increasingly important as consumers blend online research with offline purchasing experiences.

End User Insights

Women represent the largest end-user segment, accounting for approximately 63% of global market demand. Female consumers exhibit higher purchasing frequency and stronger engagement with personalized fashion accessories. Men's personalized jewelry is among the fastest-growing segments, driven by increasing acceptance of customized bracelets, rings, necklaces, and luxury accessories. Children and teen-focused personalized jewelry categories continue expanding through family gifting trends. Corporate buyers are emerging as a niche but growing segment, utilizing customized jewelry products and commemorative accessories for employee recognition and executive gifting programs.

Explore more data points, trends and opportunities Download Free Sample Report

Personalized Jewelry Market Segmentations

By Product Type

- Necklaces & Pendants

- Rings

- Bracelets

- Earrings

- Other Personalized Jewelry

By Material

- Gold

- Silver

- Platinum

- Diamond-Based Jewelry

- Gemstone-Based Jewelry

- Stainless Steel & Titanium

- Alternative Materials

By Customization Type

- Engraving-Based Customization

- Name & Initial Customization

- Birthstone Customization

- Photo/Image Customization

- Fingerprint Customization

- Handwriting & Signature Jewelry

- Fully Bespoke Jewelry Design

By Distribution Channel

- Online Retail

- Jewelry Chains

- Independent Jewelers

- Luxury Boutiques

- Department Stores

By End User

- Women

- Men

- Children & Teens

- Corporate & Institutional Buyers

Regional Insights

Asia-Pacific

Asia-Pacific accounted for approximately 37% of the global personalized jewelry market revenue in 2025, making it the largest regional market worldwide. The region's leadership is primarily driven by a combination of strong cultural affinity toward jewelry ownership, rapidly growing middle-class populations, increasing disposable incomes, and accelerating e-commerce penetration. Personalized jewelry has gained substantial popularity across Asia-Pacific as consumers increasingly seek products that combine emotional value with fashion appeal. China represents the largest country-level market within the region, supported by strong luxury consumption, widespread adoption of online retail platforms, and increasing consumer spending on customized gifting products. The popularity of self-expression among younger consumers and the growing influence of social media platforms continue to stimulate demand for name necklaces, customized rings, and birthstone jewelry. In India, deep-rooted traditions surrounding gold jewelry, weddings, family gifting, and religious celebrations provide a strong foundation for personalized jewelry adoption. Rising urbanization and the expansion of premium jewelry retail chains are further driving market growth.

Japan and South Korea contribute significantly through demand for fashion-forward and minimalist personalized jewelry designs. Consumers in these markets place high value on craftsmanship, exclusivity, and premium materials. Meanwhile, Southeast Asian countries such as Indonesia, Thailand, Vietnam, Malaysia, and the Philippines are emerging as high-growth markets due to increasing disposable incomes, expanding digital commerce ecosystems, and growing participation of younger consumers in fashion and luxury categories. The primary growth drivers across Asia-Pacific include increasing wedding expenditures, rising gifting culture, growing demand for premium lifestyle products, expansion of direct-to-consumer jewelry brands, and continued investment in digital customization technologies. The region is expected to remain the fastest-growing market globally throughout the forecast period.

North America

North America accounted for nearly 29% of global personalized jewelry market revenue in 2025, with the United States representing the dominant share of regional demand. The region benefits from high consumer purchasing power, advanced digital retail infrastructure, and strong consumer acceptance of customized luxury products. Personalized jewelry has become an increasingly important segment within the broader fashion accessories and luxury goods markets as consumers prioritize products that reflect individuality and emotional significance. The United States remains the largest market due to strong demand for personalized gifts associated with birthdays, anniversaries, engagements, weddings, and family celebrations. The growing popularity of self-purchasing among Millennials and Generation Z consumers has further accelerated market expansion. Consumers increasingly seek customized products featuring names, initials, birthstones, handwritten messages, and family-oriented designs.

Canada contributes stable demand through premium jewelry purchases and growing adoption of sustainable and ethically sourced products. Mexico continues to emerge as a growth market due to increasing middle-income consumer spending, rising urbanization, and expanding online jewelry retail channels. Key regional growth drivers include strong penetration of direct-to-consumer jewelry brands, widespread adoption of AI-powered customization tools, high social media influence on purchasing decisions, and growing demand for sustainable and lab-grown diamond jewelry. The increasing prevalence of omnichannel retail strategies and virtual try-on technologies is also enhancing customer engagement across the region.

Europe

Europe accounted for approximately 24% of global personalized jewelry market revenue in 2025. The region benefits from a long-standing heritage of jewelry craftsmanship, luxury manufacturing expertise, and strong consumer preference for premium-quality products. Personalized jewelry is increasingly positioned as both a fashion accessory and a sentimental keepsake, supporting demand across multiple consumer segments. The United Kingdom represents one of the largest personalized jewelry markets in Europe, driven by strong online retail penetration and widespread gifting culture. Germany contributes significant demand through its affluent consumer base and growing preference for high-quality customized jewelry. France and Italy remain important luxury jewelry markets where consumers increasingly seek bespoke products that combine personalization with premium craftsmanship. Spain continues to experience rising demand driven by fashion-conscious younger consumers and expanding digital commerce adoption.

One of the most important growth drivers in Europe is the increasing consumer focus on sustainability and ethical sourcing. European buyers demonstrate strong preference for recycled precious metals, conflict-free gemstones, and environmentally responsible production practices. Regulatory emphasis on supply chain transparency is encouraging manufacturers to invest in sustainable sourcing strategies and traceability technologies. Additional regional growth drivers include premiumization trends, increasing demand for handcrafted products, growing popularity of customized engagement and wedding jewelry, and continued expansion of luxury e-commerce platforms.

Latin America

Latin America accounted for approximately 4% of global personalized jewelry market revenue in 2025. Although relatively smaller compared to other regions, the market is demonstrating steady growth supported by improving economic conditions, increasing urbanization, and growing consumer awareness of personalized luxury products. Brazil represents the largest market within the region due to its sizeable population, expanding middle class, and strong cultural preference for jewelry ownership. Consumers increasingly seek customized jewelry products for gifting occasions, family celebrations, and personal expression. Mexico also contributes significantly through growing disposable incomes and rising adoption of online jewelry retail platforms.

Demand throughout the region is particularly strong within the mid-premium segment, where consumers seek affordable customization options without entering luxury price ranges. Social media platforms are playing a crucial role in driving product awareness and influencing purchasing decisions among younger demographics. Key growth drivers include increasing e-commerce penetration, expanding access to customized jewelry through digital platforms, rising consumer spending on fashion accessories, and the growing influence of global jewelry trends. Improvements in logistics infrastructure and cross-border e-commerce are also enhancing market accessibility.

Middle East & Africa

The Middle East and Africa accounted for approximately 6% of global personalized jewelry market revenue in 2025. Demand within the region is heavily influenced by strong cultural affinity for precious metal jewelry, luxury consumption patterns, and the importance of jewelry in weddings, religious celebrations, and family gifting traditions. The United Arab Emirates remains the largest personalized jewelry market in the region due to its status as a global luxury retail hub. High-income consumers, strong tourism inflows, and extensive presence of international luxury jewelry brands continue to support demand. Saudi Arabia is emerging as a major growth market as increasing female workforce participation, rising disposable incomes, and luxury retail expansion stimulate jewelry purchases.

South Africa contributes through both domestic consumption and its strategic role in the global jewelry supply chain. Growing urbanization and premium consumer spending across countries such as Qatar, Kuwait, and Bahrain are further supporting regional demand. The primary growth drivers include rising luxury retail investments, increasing tourism-related jewelry purchases, strong demand for customized wedding and bridal jewelry, and expanding availability of premium jewelry through both online and offline channels. The region is also witnessing growing adoption of bespoke luxury products among high-net-worth consumers seeking exclusivity and personalized designs.

Key Players in the Personalized Jewelry Market

- Pandora

- Signet Jewelers

- Tiffany & Co.

- Cartier

- Swarovski

- Chow Tai Fook

- Bulgari

- David Yurman

- Blue Nile

- James Allen

- Harry Winston

- Graff

- Monica Vinader

- Kendra Scott

- Tanishq