Pearl Jewelry Market Size

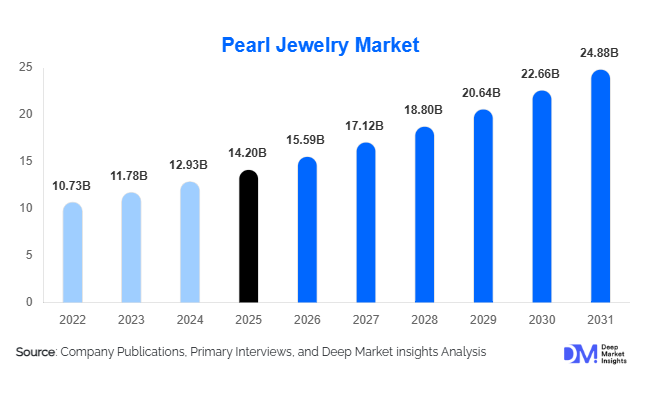

According to Deep Market Insights, the global pearl jewelry market size was valued at USD 14.2 billion in 2025 and is projected to grow from USD 15.59 billion in 2026 to reach USD 24.88 billion by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). Market growth is primarily supported by rising demand for luxury jewelry, increasing consumer preference for sustainable gemstones, growing penetration of e-commerce channels, and expanding adoption of pearl jewelry among younger demographics. Traditionally associated with formal occasions and high-end luxury consumption, pearl jewelry has undergone significant repositioning over the last decade, becoming a mainstream fashion accessory across multiple age groups and income segments.

The market is also benefiting from advances in pearl cultivation technologies, improved traceability standards, and growing demand for customized jewelry designs. Asia-Pacific continues to dominate global pearl production and consumption, while North America and Europe remain major luxury consumption centers. The emergence of direct-to-consumer jewelry brands and social media-driven fashion trends has further accelerated market expansion. Premium pearls such as South Sea, Tahitian, and Akoya pearls continue to command significant pricing premiums, while freshwater pearls account for the majority of global volume sales. The industry is increasingly characterized by sustainability initiatives, ethical sourcing programs, and investments in premium branding, positioning pearl jewelry as both a fashion statement and a long-term luxury asset.

Key Market Insights

- Freshwater pearls account for approximately 48% of global market revenue, making them the largest pearl category due to affordability and broad consumer acceptance.

- Necklaces and pearl strands remain the largest product segment, contributing nearly 34% of global market value in 2025.

- Asia-Pacific dominates the global pearl jewelry market, accounting for approximately 44% of total revenue due to strong production capabilities and consumer demand.

- India represents the fastest-growing national market, expanding at over 12% CAGR through 2031 due to increasing disposable income and wedding jewelry demand.

- Online jewelry sales continue to outperform traditional channels, with digital platforms accounting for nearly one-quarter of global pearl jewelry sales.

- Sustainability and traceability initiatives are reshaping purchasing behavior, particularly among millennial and Gen Z consumers.

Pearl Jewelry Market Trends

Everyday Luxury and Contemporary Pearl Fashion

Pearls are increasingly transitioning from traditional ceremonial jewelry toward everyday luxury fashion accessories. Global consumers, particularly millennials and Gen Z buyers, are embracing minimalist pearl earrings, pearl rings, layered necklaces, and mixed-material designs suitable for casual wear. Luxury brands and independent designers are introducing innovative collections incorporating pearls with diamonds, colored gemstones, and alternative metals. Social media platforms, celebrity endorsements, and fashion influencers have played a major role in repositioning pearls as contemporary lifestyle products rather than formal occasion accessories. This trend is significantly expanding the addressable consumer base beyond traditional luxury buyers.

Sustainable and Traceable Pearl Sourcing

Environmental sustainability has become a major differentiating factor across the pearl jewelry industry. Consumers increasingly seek transparency regarding pearl origins, farming practices, and environmental impacts. Leading pearl producers are investing in responsible aquaculture, marine ecosystem preservation, and digital traceability technologies. Blockchain-based tracking systems, certification programs, and ethical sourcing standards are becoming increasingly common across premium product categories. Sustainable pearl farming practices not only support environmental conservation but also strengthen brand value among environmentally conscious consumers. This trend is expected to influence purchasing decisions across both premium and luxury jewelry segments during the forecast period.

Pearl Jewelry Market Drivers

Growing Global Luxury Goods Consumption

Rising disposable incomes and expanding affluent populations across Asia-Pacific, North America, and the Middle East continue to support premium jewelry purchases. Pearls are increasingly viewed as timeless luxury assets with strong aesthetic appeal and relatively stable value retention. High-net-worth individuals are driving demand for premium South Sea, Tahitian, and Akoya pearls, particularly within luxury gifting and collectible jewelry categories. The expansion of luxury retail infrastructure across emerging markets further supports long-term market growth.

Expansion of E-Commerce and Direct-to-Consumer Jewelry Brands

Digital transformation has fundamentally changed jewelry purchasing behavior. Consumers now have access to wider product selections, transparent pricing, customization tools, and global brands through online channels. Direct-to-consumer pearl jewelry brands have successfully reduced distribution costs while improving customer engagement through virtual consultations, augmented reality visualization tools, and personalized shopping experiences. Online channels have significantly expanded market accessibility, particularly among younger demographics and consumers located outside major luxury retail centers.

Strong Demand from Wedding and Gifting Segments

Pearls continue to hold significant cultural and symbolic value across wedding, anniversary, and gifting occasions. Markets such as China, India, Japan, and Southeast Asia maintain strong traditions surrounding pearl jewelry ownership. The growing wedding industry, increasing premium gifting expenditures, and rising female workforce participation have collectively strengthened demand across multiple product categories. Bridal pearl jewelry sets remain among the most resilient revenue-generating segments globally.

Pearl Jewelry Market Restraints

Supply Constraints for Premium Pearl Varieties

Production of South Sea, Tahitian, and natural pearls remains limited due to biological cultivation cycles, environmental dependencies, and geographic concentration of farming operations. Supply disruptions caused by climate variability, water quality concerns, and disease outbreaks can significantly affect pearl availability and pricing. These constraints create challenges for manufacturers seeking consistent inventory levels while simultaneously supporting elevated product prices.

Competition from Alternative Luxury Jewelry Categories

The pearl jewelry market faces increasing competition from diamonds, colored gemstones, lab-grown gemstones, and alternative luxury accessories. Younger consumers often prioritize trend-driven products, creating competitive pressure for traditional pearl collections. Manufacturers must continuously innovate through modern designs, personalization features, and sustainability initiatives to maintain relevance among evolving consumer segments.

Pearl Jewelry Market Opportunities

Rapid Growth of Luxury Consumption in Emerging Markets

Emerging economies such as India, Vietnam, Indonesia, Saudi Arabia, and the UAE present significant opportunities for pearl jewelry manufacturers. Rising middle-class populations, increasing urbanization, and growing disposable incomes are driving premium jewelry purchases. Wedding traditions and luxury gifting cultures within these markets further support demand growth. Companies expanding localized retail networks and digital sales channels are expected to benefit substantially from this opportunity.

Personalized and Bespoke Jewelry Solutions

Customization has become one of the most important purchasing criteria in the luxury jewelry industry. Consumers increasingly seek unique pearl combinations, personalized engravings, customized settings, and made-to-order designs. Advances in digital design technologies and flexible manufacturing processes are enabling brands to offer tailored products while maintaining operational efficiency. Bespoke jewelry commands higher margins and strengthens long-term customer loyalty.

Technology Integration and Digital Luxury Retailing

Artificial intelligence, virtual try-on technologies, augmented reality, and blockchain-based authentication systems are creating new growth avenues for market participants. Luxury consumers increasingly expect seamless digital experiences throughout the purchasing journey. Investments in digital engagement tools improve conversion rates, reduce return rates, and enhance consumer confidence in online jewelry purchases. Companies leading technology adoption are likely to gain competitive advantages across premium market segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14.2 Billion |

| Market Size in 2026 | USD 15.59 Billion |

| Market Size in 2031 | USD 24.88 Billion |

| CAGR | 9.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Pearl Type Insights

Freshwater pearls accounted for approximately 48% of the global pearl jewelry market in 2025, making them the largest pearl type segment worldwide. The segment's leadership is primarily driven by its favorable balance between affordability, quality, and design versatility. Unlike South Sea and Tahitian pearls, freshwater pearls can be cultivated at significantly larger volumes, enabling manufacturers to offer pearl jewelry across mass-market, premium, and luxury price points. China continues to dominate global freshwater pearl production, accounting for the majority of worldwide supply, which provides manufacturers with stable raw material availability and cost efficiencies. In addition, improvements in cultivation techniques have enhanced pearl shape uniformity, luster quality, and color variety, making freshwater pearls increasingly competitive with higher-priced pearl varieties.

The growing popularity of everyday pearl fashion, particularly among younger consumers, has further strengthened demand for freshwater pearls due to their accessibility and suitability for modern jewelry designs. Meanwhile, Akoya pearls account for approximately 18% of market revenue and remain highly preferred in Japan, North America, and Europe due to their superior luster, near-perfect roundness, and strong association with luxury jewelry. South Sea pearls represent nearly 15% of global revenue, supported by exceptionally high average selling prices and strong demand from affluent consumers seeking investment-grade jewelry. Tahitian pearls contribute approximately 9% of market value and continue to benefit from increasing consumer interest in rare, naturally dark-colored pearls that differentiate luxury collections. Premiumization trends across global jewelry markets are expected to support continued growth of South Sea and Tahitian pearl categories, although freshwater pearls are expected to maintain market leadership throughout the forecast period.

Product Type Insights

Necklaces and pearl strands remain the largest product category, accounting for approximately 34% of global pearl jewelry revenue in 2025. The segment's dominance is supported by pearls' historical association with elegance, status, and ceremonial occasions. Pearl necklaces continue to be widely purchased for weddings, anniversaries, luxury gifting, and formal events, particularly across Asia-Pacific and Middle Eastern markets. The enduring appeal of classic pearl strands among both mature luxury buyers and younger consumers adopting contemporary layered jewelry styles has enabled the segment to maintain its leadership position.

Another major factor driving necklace demand is their higher average transaction value compared to earrings, rings, and bracelets, resulting in a disproportionately larger contribution to overall market revenue. Luxury brands continue to prioritize necklace collections as flagship products, incorporating premium Akoya, South Sea, and Tahitian pearls into high-value designs. Earrings account for nearly 24% of the market and represent one of the fastest-growing categories due to increasing adoption of pearl jewelry in everyday fashion. Consumers increasingly favor pearl stud earrings, minimalist drop earrings, and hybrid pearl-metal designs that can be worn in both professional and casual settings. Rings contribute approximately 15% of market revenue, supported by rising demand for personalized jewelry and contemporary stackable ring collections. Bracelets, pendants, brooches, and bespoke jewelry collectively continue to gain traction as customization trends encourage consumers to seek unique and individualized pearl jewelry pieces.

Material Setting Insights

Gold pearl jewelry dominates the global market with approximately 52% market share in 2025, driven by strong consumer perceptions of value, luxury, and long-term investment appeal. Gold settings are particularly preferred in Asia-Pacific, the Middle East, and parts of Europe, where gold jewelry carries significant cultural, ceremonial, and wealth-preservation importance. The segment benefits from strong demand across bridal jewelry, festive gifting, and premium luxury collections. The combination of pearls with yellow gold, white gold, and rose gold settings allows manufacturers to address diverse consumer preferences while maintaining premium pricing.

The segment's leadership is further supported by the increasing preference for premium and investment-oriented jewelry purchases among affluent consumers. Gold's established reputation as a store of value enhances the perceived worth of pearl jewelry, particularly during periods of economic uncertainty. Silver pearl jewelry accounts for approximately 23% of market revenue, benefiting from affordability and strong demand among younger consumers entering the jewelry market. Meanwhile, diamond-pearl combination jewelry represents one of the fastest-growing segments, supported by increasing premiumization across the luxury jewelry industry. High-net-worth consumers increasingly seek products that combine the rarity of premium pearls with the prestige of diamonds, resulting in higher average selling prices and improved profit margins for manufacturers. Platinum and alternative metal settings continue to gain popularity among luxury buyers seeking exclusivity and contemporary aesthetics.

Distribution Channel Insights

Brand-owned stores and independent jewelry retailers collectively account for approximately 61% of global pearl jewelry sales, making offline retail the leading distribution channel. The segment remains dominant because pearl jewelry is often considered a high-involvement purchase where consumers prefer physical product evaluation before making purchasing decisions. Buyers frequently assess pearl luster, size, surface quality, color consistency, and craftsmanship in person, making physical retail environments particularly important for premium and luxury purchases.

Offline channels also benefit from personalized customer service, authenticity verification, after-sales support, and custom jewelry consultation services that enhance consumer confidence. Established luxury brands continue to invest heavily in flagship stores and experiential retail formats to strengthen customer engagement and brand loyalty. However, online channels now account for approximately 24% of global market revenue and represent the fastest-growing distribution segment. Growth is being fueled by increasing consumer trust in online luxury purchases, advancements in virtual try-on technologies, AI-powered product recommendations, and transparent certification systems. Direct-to-consumer brands are successfully leveraging social media marketing, influencer partnerships, and digital customization platforms to expand their market presence while achieving higher margins by reducing intermediary costs.

End-Use Insights

Personal fashion and everyday wear represent the largest end-use category, accounting for approximately 41% of global pearl jewelry demand in 2025. The segment's leadership reflects a significant transformation in consumer perception of pearl jewelry. Once viewed primarily as formal or ceremonial accessories, pearls are increasingly incorporated into daily wardrobes through minimalist and contemporary designs that appeal to younger consumers. Social media influence, celebrity endorsements, and changing fashion trends have contributed significantly to the normalization of pearls as everyday luxury products.

The growing female workforce, rising disposable incomes, and increasing demand for versatile accessories suitable for both professional and casual environments continue to support segment expansion. Bridal and wedding applications contribute approximately 26% of market revenue and remain one of the most stable demand drivers globally. Strong wedding traditions across China, India, Japan, Southeast Asia, and the Middle East sustain consistent demand for pearl necklaces, earrings, and complete bridal jewelry sets. Luxury gifting represents another important segment, particularly in developed markets where pearls are commonly purchased for anniversaries, graduations, and milestone celebrations. Additionally, investment-grade pearl jewelry is emerging as a niche growth category as affluent consumers increasingly diversify luxury asset portfolios through rare South Sea, Tahitian, and natural pearl collections.

Explore more data points, trends and opportunities Download Free Sample Report

Pearl Jewelry Market Segmentations

By Pearl Type

- Freshwater Pearls

- Akoya Pearls

- South Sea Pearls

- Tahitian Pearls

- Natural Pearls

- Hybrid and Specialty Cultured Pearls

By Product Type

- Necklaces & Strands

- Earrings

- Rings

- Bracelets

- Pendants & Charms

- Brooches & Pins

- Bridal Pearl Jewelry Sets

- Custom/Bespoke Pearl Jewelry

By Material Setting

- Gold Pearl Jewelry

- Silver Pearl Jewelry

- Platinum Pearl Jewelry

- Diamond-Pearl Combination Jewelry

- Alternative Metal Pearl Jewelry

By Distribution Channel

- Brand-Owned Stores

- Independent Jewelry Retailers

- Department Stores

- Online/E-Commerce

- Direct-to-Consumer (D2C)

- Duty-Free & Travel Retail

By End Use

- Personal Fashion & Everyday Wear

- Bridal & Wedding Jewelry

- Luxury Gifting

- Corporate & Executive Gifting

- Cultural & Traditional Ceremonies

- Investment & Collectible Jewelry

Regional Insights

Asia-Pacific

Asia-Pacific leads the global pearl jewelry market with approximately 44% market share in 2025 and is expected to maintain its dominance throughout the forecast period. The region benefits from a unique combination of production leadership and strong consumer demand. China serves as both the world's largest freshwater pearl producer and one of the largest consumers of pearl jewelry, creating a highly integrated industry ecosystem. Strong domestic demand, extensive manufacturing infrastructure, and established export capabilities continue to support regional leadership.

Japan remains a global center for premium Akoya pearl production and luxury pearl jewelry craftsmanship, while Australia plays a critical role in South Sea pearl cultivation. India is emerging as the fastest-growing country market globally, supported by rising disposable incomes, rapid urbanization, expanding middle-class populations, and increasing expenditure on wedding jewelry. Additional growth drivers include the expansion of organized jewelry retail, increasing female workforce participation, digital jewelry sales growth, and rising luxury consumption across Southeast Asian countries including Indonesia, Thailand, Vietnam, and Singapore.

North America

North America accounts for approximately 26% of global pearl jewelry revenue, making it the second-largest regional market. The United States dominates regional demand due to strong luxury spending, high per-capita jewelry expenditure, and a well-established gifting culture. Consumers increasingly favor ethically sourced and sustainably produced pearl jewelry, encouraging brands to invest in traceability initiatives and responsible sourcing programs.

The region's growth is further supported by the rapid expansion of e-commerce, increasing adoption of customized jewelry products, and strong demand for premium fashion accessories among millennials and Gen Z consumers. Luxury jewelry brands continue to benefit from robust discretionary spending and the growing popularity of direct-to-consumer sales channels. Canada contributes stable demand through affluent urban populations and increasing consumer preference for premium jewelry products with sustainability credentials.

Europe

Europe represents approximately 21% of global pearl jewelry demand, with Germany, France, Italy, and the United Kingdom serving as the primary consuming markets. The region benefits from a strong luxury heritage, established fashion industries, and sophisticated consumer preferences. European consumers demonstrate growing demand for sustainable luxury products, making ethical sourcing and environmental certifications important purchasing criteria.

Growth across the region is supported by increasing consumer interest in premium handcrafted jewelry, expanding demand for personalized luxury products, and strong tourism-driven retail sales. France and Italy continue to benefit from their positions as global fashion capitals, while Germany's affluent consumer base supports steady premium jewelry purchases. Furthermore, increasing adoption of contemporary pearl jewelry among younger consumers is helping broaden the market beyond traditional luxury buyers.

Middle East & Africa

The Middle East and Africa account for approximately 6% of global market revenue, with the Gulf Cooperation Council countries driving the majority of regional demand. The UAE and Saudi Arabia remain the largest markets due to high disposable incomes, strong luxury consumption patterns, and deep-rooted cultural preferences for premium jewelry. Pearls maintain historical significance across Gulf markets, further supporting regional demand.

Growth is being driven by expanding luxury retail infrastructure, increasing tourism expenditure, rising numbers of high-net-worth individuals, and government initiatives aimed at diversifying economies through retail and tourism sectors. South Africa represents an emerging growth market supported by increasing luxury consumption and expanding organized jewelry retail networks. The region is also benefiting from strong demand for bespoke and high-value jewelry collections among affluent consumers.

Latin America

Latin America contributes approximately 3% of global pearl jewelry market value, with Brazil, Mexico, and Argentina accounting for the majority of regional demand. Although the market remains relatively underpenetrated compared to North America and Europe, rising household incomes and growing exposure to international luxury brands are creating favorable growth opportunities.

Regional growth is increasingly supported by expanding e-commerce adoption, improving access to premium international jewelry brands, and growing interest in luxury fashion products among younger urban consumers. Brazil remains the largest market due to its sizeable affluent population and strong luxury retail presence. Mexico is experiencing increased demand through organized retail expansion, while Argentina continues to demonstrate niche demand for premium and designer jewelry collections despite broader economic volatility.