Orthopedic Shoes Market Size

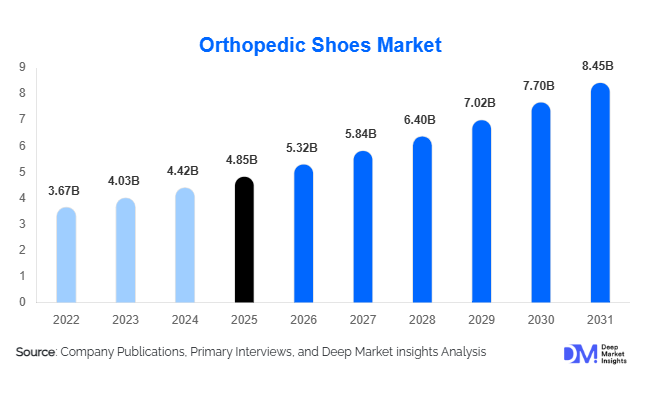

According to Deep Market Insights, the global orthopedic shoes market size was valued at USD 4.85 billion in 2025 and is projected to grow from USD 5.32 billion in 2026 to reach USD 8.45 billion by 2031, expanding at a CAGR of 9.7% during the forecast period (2026–2031). The orthopedic shoes market growth is primarily driven by the rising prevalence of diabetes, musculoskeletal disorders, arthritis, and foot deformities, coupled with increasing awareness regarding preventive foot care and mobility enhancement. Growing adoption of customized orthopedic footwear, expanding geriatric populations, and advancements in footwear technologies are further supporting market expansion globally.

Key Market Insights

- Therapeutic orthopedic shoes remain the largest product category, accounting for nearly 38% of global revenue due to strong demand among diabetic and arthritis patients.

- North America dominates the orthopedic shoes market, representing approximately 38% of global demand, supported by advanced healthcare infrastructure and favorable reimbursement policies.

- Asia-Pacific is the fastest-growing regional market, driven by increasing diabetes prevalence, aging populations, and rising healthcare awareness across China, India, and Southeast Asia.

- Non-prescription orthopedic footwear is gaining traction, accounting for nearly 57% of market demand as consumers increasingly prioritize comfort, posture support, and preventive healthcare.

- Digital customization technologies, including 3D foot scanning and AI-based gait analysis, are transforming product development and customer experience.

- E-commerce and direct-to-consumer sales channels are accelerating market penetration by improving accessibility to specialized footwear products.

rthopedic Shoes Market Trends

Growing Adoption of Customized Orthopedic Footwear

The orthopedic footwear industry is increasingly shifting toward personalized solutions that address individual foot anatomy and medical conditions. Advances in 3D scanning, pressure-mapping systems, and digital fitting technologies are enabling manufacturers to offer highly customized footwear with improved comfort and therapeutic effectiveness. Consumers are increasingly seeking footwear tailored to specific conditions such as plantar fasciitis, diabetic neuropathy, bunions, and flat feet. The integration of digital assessment tools has significantly reduced production lead times while improving fit accuracy. As customization becomes more affordable, both established brands and emerging companies are investing heavily in mass-customization platforms that combine medical functionality with modern aesthetics.

Integration of Comfort, Wellness, and Lifestyle Footwear

Orthopedic footwear is increasingly moving beyond its traditional medical positioning and entering the broader comfort and wellness footwear segment. Consumers are purchasing orthopedic shoes not only for corrective purposes but also for everyday comfort, posture improvement, and injury prevention. Manufacturers are incorporating memory foam cushioning, shock-absorption technologies, lightweight materials, and ergonomic designs that appeal to younger demographics. Fashion-forward orthopedic shoes are reducing the stigma traditionally associated with medical footwear, enabling brands to attract a wider customer base. This trend is particularly evident in North America and Europe, where wellness-focused consumers are driving demand for preventive orthopedic products.

Orthopedic Shoes Market Drivers

Rising Prevalence of Diabetes and Foot Disorders

The increasing global incidence of diabetes is one of the strongest growth drivers for the orthopedic shoes market. Diabetic patients face a heightened risk of neuropathy, ulcers, and foot deformities, making specialized footwear essential for preventive care. Healthcare providers increasingly recommend orthopedic shoes as part of comprehensive diabetes management programs. Rising obesity rates and sedentary lifestyles are further contributing to foot-related complications, creating sustained demand for therapeutic footwear solutions. Growing awareness regarding diabetic foot care is supporting market expansion across both developed and emerging economies.

Expansion of the Global Elderly Population

Aging populations worldwide continue to create substantial demand for orthopedic footwear. Elderly individuals frequently experience conditions such as arthritis, osteoarthritis, reduced mobility, and foot pain that require supportive and corrective footwear. Countries including Japan, Germany, Italy, China, and South Korea are witnessing significant demographic shifts that are strengthening demand. Orthopedic shoes help improve balance, reduce fall risks, and enhance mobility, making them increasingly important in elderly healthcare and homecare settings.

Orthopedic Shoes Market Restraints

High Product Costs and Limited Affordability

Orthopedic footwear typically commands premium pricing due to specialized materials, medical certifications, customized manufacturing processes, and advanced comfort technologies. Customized products can cost several times more than conventional footwear, limiting adoption among cost-sensitive consumers. In many developing economies, limited insurance coverage and out-of-pocket healthcare spending create affordability challenges that restrict market penetration.

Consumer Perception and Fashion Constraints

Although product aesthetics have improved significantly, orthopedic shoes continue to face perception challenges among younger consumers who prioritize fashion and style. Many customers still associate orthopedic footwear with bulky designs and medical necessity rather than lifestyle benefits. This perception gap can delay adoption among consumers who may benefit from orthopedic products but remain reluctant to purchase them due to appearance-related concerns.

Orthopedic Shoes Market Opportunities

Expansion of Diabetic Footwear Programs

The rapidly increasing global diabetic population presents a major opportunity for orthopedic footwear manufacturers. Governments, healthcare providers, and insurance companies are increasingly supporting preventive diabetic foot care initiatives that encourage the adoption of specialized footwear. Manufacturers that develop certified diabetic footwear solutions with advanced pressure-relief technologies are positioned to benefit from expanding reimbursement programs and hospital partnerships. The growing focus on reducing diabetic complications and lower-limb amputations is expected to create long-term demand for therapeutic footwear products.

Digital Foot Scanning and AI-Driven Customization

Emerging digital technologies are transforming the orthopedic footwear industry by enabling scalable customization. AI-powered gait analysis, smartphone-based foot measurement applications, and 3D foot scanning systems allow manufacturers to provide individualized footwear solutions with greater efficiency and accuracy. These technologies reduce fitting errors, improve patient outcomes, and create premium product offerings with higher margins. As digital healthcare adoption expands globally, orthopedic footwear companies have significant opportunities to differentiate themselves through technology-enabled customer experiences.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.85 Billion |

| Market Size in 2026 | USD 5.32 Billion |

| Market Size in 2031 | USD 8.45 Billion |

| CAGR | 9.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Therapeutic orthopedic shoes represent the largest product category, accounting for approximately 38% of global market revenue in 2025. Demand is driven primarily by diabetic patients, arthritis sufferers, and individuals requiring medical-grade footwear to manage chronic foot conditions. Corrective orthopedic shoes also maintain a significant share due to increasing diagnosis of structural foot abnormalities such as flat feet, heel spurs, and bunions. Customized orthopedic footwear is emerging as one of the fastest-growing segments as consumers increasingly seek personalized solutions tailored to their specific biomechanical requirements. Sports orthopedic footwear is also gaining popularity among athletes and fitness-conscious consumers seeking injury prevention and recovery support.

Material Insights

Leather remains the dominant material segment, accounting for approximately 42% of global market revenue due to its durability, breathability, flexibility, and premium appeal. Leather orthopedic shoes are widely preferred among elderly consumers and patients requiring long-term therapeutic footwear. Synthetic materials are gaining market share owing to lower production costs, lightweight properties, and increasing sustainability initiatives. Mesh and textile materials are witnessing strong adoption in sports orthopedic footwear due to enhanced breathability and comfort. Hybrid composite materials are also emerging as manufacturers seek to balance performance, durability, and environmental sustainability.

Distribution Channel Insights

Specialty orthopedic footwear stores account for the largest share of global sales, representing nearly 29% of the market. These stores provide professional fitting services, personalized consultations, and access to a broad range of therapeutic products. Hospital and orthopedic clinic channels remain critical for medically prescribed footwear, particularly among diabetic and post-surgical patients. E-commerce is the fastest-growing distribution channel as consumers increasingly prefer online purchasing supported by digital fitting tools and flexible return policies. Direct-to-consumer sales models are also expanding rapidly as manufacturers strengthen their digital presence and improve customer engagement through personalized online experiences.

End-User Insights

Homecare users represent the largest end-user segment, accounting for approximately 35% of global demand. Increasing self-management of chronic conditions, rising elderly populations, and growing awareness of preventive healthcare are supporting segment growth. Hospitals and orthopedic clinics remain major consumers of orthopedic footwear due to physician recommendations and post-operative rehabilitation programs. Rehabilitation centers are experiencing increasing demand as sports injuries and orthopedic surgeries become more prevalent. Elderly care facilities are also emerging as an important growth segment due to the increasing need for mobility-enhancing footwear among aging populations.

Explore more data points, trends and opportunities Download Free Sample Report

Orthopedic Shoes Market Segmentations

By Product Type

- Therapeutic Orthopedic Shoes

- Corrective Orthopedic Shoes

- Preventive Orthopedic Shoes

- Customized Orthopedic Shoes

- Sports Orthopedic Footwear

By Material

- Leather

- Synthetic Materials

- Mesh/Textile Materials

- EVA-Based Materials

- Polyurethane-Based Materials

- Hybrid Composite Materials

By Consumer Group

- Men

- Women

- Children

By Distribution Channel

- Hospital-Based Sales

- Orthopedic Clinics

- Specialty Footwear Stores

- Pharmacies & Medical Retail

- E-commerce Platforms

- Direct-to-Consumer (DTC)

By Prescription Type

- Prescription Orthopedic Shoes

- Non-Prescription Orthopedic Shoes

Regional Insights

North America

North America accounted for approximately 38% of the global orthopedic shoes market in 2025, making it the largest regional market. The United States dominates regional demand due to high diabetes prevalence, favorable reimbursement structures, advanced healthcare infrastructure, and strong consumer awareness regarding preventive foot care. Canada also contributes significantly through increasing healthcare spending and growing elderly populations. The region continues to lead innovation in customized orthopedic footwear and digital fitting technologies.

Europe

Europe represents nearly 29% of global market demand, supported by well-established healthcare systems and strong adoption of orthopedic products. Germany leads regional consumption owing to its advanced orthopedic care infrastructure and reimbursement programs. France, the United Kingdom, Italy, and Spain also contribute significantly to market growth. Rising elderly populations and growing awareness regarding mobility improvement continue to support orthopedic footwear demand across the region.

Asia-Pacific

Asia-Pacific accounts for approximately 24% of global demand and is projected to be the fastest-growing region during the forecast period. China and India are emerging as key growth engines due to rapidly expanding diabetic populations, increasing healthcare expenditure, and rising awareness of preventive foot care. Japan remains a mature market characterized by strong demand from elderly consumers. Improving healthcare infrastructure and expanding e-commerce penetration are further supporting regional growth.

Latin America

Latin America accounts for roughly 5% of global market revenue, with Brazil serving as the largest regional market. Increasing healthcare access, rising obesity rates, and growing awareness regarding orthopedic conditions are supporting demand growth. Mexico and Argentina are also emerging as important markets due to expanding healthcare investments and increasing prevalence of chronic diseases.

Middle East & Africa

The Middle East & Africa region contributes approximately 4% of global demand. Saudi Arabia and the United Arab Emirates lead regional consumption due to high diabetes prevalence and increasing healthcare spending. South Africa remains the largest African market, supported by growing awareness of orthopedic health and improving healthcare accessibility. The region offers long-term growth opportunities as healthcare infrastructure continues to develop.

Key Players in the Orthopedic Shoes Market

- Orthofeet

- Dr. Comfort

- Aetrex Worldwide

- Drew Shoe

- Propet

- Mephisto

- New Balance

- Skechers

- Finn Comfort

- Bauerfeind

- Podartis

- DARCO International

- Apex Foot Health Industries

- Vionic Group

- ComfortFit Orthotic Labs