Microwave Ovens Market Size

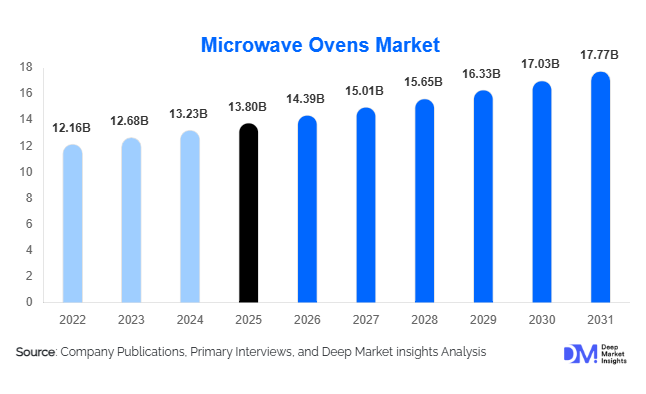

According to Deep Market Insights, the global microwave ovens market size was valued at USD 13.8 billion in 2025 and is projected to grow from USD 14.39 billion in 2026 to reach USD 17.77 billion by 2031, expanding at a CAGR of 4.3% during the forecast period (2026–2031). The microwave ovens market growth is primarily driven by increasing urbanization, rising demand for convenience-oriented cooking appliances, growing adoption of smart kitchen technologies, and expanding penetration of household appliances across emerging economies. The market continues to benefit from changing consumer lifestyles, higher disposable incomes, and the increasing popularity of multifunctional cooking equipment capable of reheating, grilling, baking, steaming, and air-frying. Furthermore, commercial foodservice establishments, quick-service restaurants, convenience stores, and institutional kitchens are increasingly deploying high-performance microwave ovens to improve operational efficiency and reduce food preparation times.

Key Market Insights

- Convection microwave ovens account for the largest revenue share globally, supported by growing consumer preference for multifunctional cooking appliances.

- Smart microwave ovens featuring Wi-Fi connectivity and AI-powered cooking assistance are witnessing rapid adoption, particularly in developed markets.

- Asia-Pacific dominates the global microwave ovens market, accounting for approximately 41% of total revenue in 2025, led by China, Japan, South Korea, and India.

- India represents one of the fastest-growing national markets, driven by increasing appliance penetration and rising middle-class consumption.

- Commercial foodservice applications are expanding rapidly, fueled by growth in quick-service restaurants, cloud kitchens, and convenience food consumption.

- Inverter technology is becoming a major differentiator, offering improved energy efficiency, precise cooking control, and enhanced food quality.

Microwave Ovens Market Trends

Smart and Connected Kitchen Appliances Gaining Momentum

The integration of microwave ovens into connected home ecosystems is emerging as one of the most influential market trends. Consumers increasingly prefer appliances that can be remotely controlled through smartphones, voice assistants, and smart-home platforms. Manufacturers are introducing microwave ovens equipped with Wi-Fi connectivity, AI-assisted cooking algorithms, recipe synchronization, and predictive maintenance capabilities. These innovations enhance convenience while allowing manufacturers to differentiate their offerings within a highly competitive market. Smart microwaves are particularly popular among younger consumers and technology-savvy households that seek seamless integration between kitchen appliances and digital lifestyles. As smart-home adoption expands globally, connected microwave ovens are expected to capture a growing share of premium appliance sales.

Multifunctional Cooking Systems Reshaping Product Demand

Consumer demand is increasingly shifting from basic reheating appliances toward multifunctional cooking systems capable of performing several cooking tasks within a single unit. Manufacturers are introducing products that combine microwave heating, convection cooking, grilling, steaming, and air-frying capabilities. These multifunctional models appeal particularly to urban consumers living in compact residential spaces who seek appliance consolidation without sacrificing cooking flexibility. The trend is also supported by rising energy-efficiency awareness, as consumers prefer versatile appliances that reduce overall kitchen equipment requirements. Premium multifunctional microwave ovens are generating higher average selling prices and stronger margins for manufacturers, making this segment a major focus for product development investments.

Microwave Ovens Market Drivers

Growing Preference for Convenience Cooking

Busy lifestyles, increasing workforce participation, and the growth of dual-income households continue to drive demand for convenient cooking solutions. Microwave ovens significantly reduce meal preparation times and support the growing consumption of ready-to-eat and frozen foods. Urban consumers increasingly prioritize appliances that save time while maintaining food quality, making microwave ovens an essential component of modern kitchens. This trend is particularly evident among younger demographics and single-person households, where demand for compact and easy-to-use cooking appliances remains strong.

Expansion of Commercial Foodservice Infrastructure

The rapid growth of quick-service restaurants, cloud kitchens, institutional foodservice facilities, hospitals, convenience stores, and corporate cafeterias is creating sustained demand for commercial microwave ovens. Foodservice operators increasingly require equipment capable of delivering speed, consistency, and operational efficiency. Commercial microwave ovens help reduce labor requirements, improve throughput, and support standardized food preparation. The continued expansion of food delivery platforms and convenience meal offerings is expected to further strengthen commercial demand throughout the forecast period.

Microwave Ovens Market Restraints

High Market Saturation in Developed Economies

Microwave oven ownership rates exceed 90% in several developed countries, particularly across North America, Japan, and Western Europe. As a result, demand in these markets is largely replacement-driven rather than supported by new household penetration. This limits overall volume growth and increases competitive pressure among manufacturers seeking to differentiate through product innovation and premiumization strategies.

Pricing Pressure and Intense Market Competition

The global microwave ovens market remains highly competitive, with numerous multinational and regional manufacturers competing across multiple price segments. Intense pricing pressure, particularly within entry-level categories, can negatively affect profit margins. Additionally, fluctuations in raw material costs, electronic component prices, logistics expenses, and semiconductor availability create challenges for manufacturers attempting to maintain profitability while remaining price competitive.

Microwave Ovens Market Opportunities

Expansion Across Emerging Household Markets

Significant opportunities exist in emerging economies where microwave oven penetration remains substantially lower than in developed regions. Countries such as India, Indonesia, Vietnam, the Philippines, Egypt, and Nigeria are witnessing rapid urbanization, increasing disposable incomes, and growing demand for modern household appliances. Manufacturers can capitalize on these trends through localized product offerings, affordable pricing strategies, and expanded distribution networks. Rising middle-class populations are expected to generate strong first-time purchase demand over the coming decade.

Commercial Kitchen Modernization and Cloud Kitchen Growth

The global expansion of cloud kitchens, food delivery services, convenience retail chains, and institutional foodservice operations presents a significant growth opportunity for commercial microwave oven manufacturers. Operators increasingly seek programmable, energy-efficient, and high-capacity microwave systems that improve operational efficiency and reduce labor costs. The continued evolution of digital food delivery ecosystems is expected to support long-term demand for advanced commercial cooking equipment worldwide.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13.8 Billion |

| Market Size in 2026 | USD 14.39 Billion |

| Market Size in 2031 | USD 17.77 Billion |

| CAGR | 4.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Convection microwave ovens dominate the global market, accounting for approximately 39% of total revenue in 2025. Their ability to combine conventional microwave functionality with baking, roasting, and grilling capabilities makes them highly attractive to consumers seeking multifunctional appliances. Grill microwave ovens continue to maintain strong demand among mid-range consumers due to their affordability and versatility. Solo microwave ovens remain popular in price-sensitive markets and among first-time buyers, particularly in emerging economies. Meanwhile, combination steam and air-fryer-integrated microwave ovens are gaining momentum within premium segments, driven by growing consumer interest in healthy cooking solutions and appliance consolidation.

Installation Type Insights

Countertop microwave ovens account for the largest share of the global market, representing approximately 62% of total revenue. Their popularity stems from affordability, easy installation, portability, and broad availability across retail channels. Built-in microwave ovens are experiencing strong growth, particularly in developed regions where consumers increasingly prefer integrated kitchen designs. Over-the-range microwave ovens maintain stable demand in North America, where they provide both cooking and ventilation functionality. Drawer microwave ovens represent a niche but rapidly growing premium segment driven by luxury residential construction and smart-home integration trends.

Technology Insights

Conventional magnetron technology continues to account for the majority of global microwave oven sales, representing approximately 70% of market revenue. However, inverter technology is emerging as the fastest-growing segment due to its ability to deliver consistent heating, improved energy efficiency, and enhanced cooking precision. Smart microwave ovens equipped with Wi-Fi connectivity, voice assistant compatibility, and AI-powered cooking programs are increasingly gaining market share among premium consumers. Manufacturers are investing heavily in intelligent cooking technologies to strengthen product differentiation and capture higher-margin market segments.

End-Use Insights

Residential applications account for approximately 63% of global microwave oven demand, supported by widespread household adoption and replacement purchases. Family households represent the largest consumer category, while premium smart-home users are increasingly driving demand for connected appliances. Commercial applications continue to exhibit faster growth, supported by expansion within quick-service restaurants, cloud kitchens, hospitals, hotels, and institutional foodservice facilities. The growing popularity of food delivery services and ready-to-eat meal consumption is expected to accelerate commercial microwave oven adoption globally. Healthcare facilities and corporate cafeterias are also emerging as important end-use segments due to increasing demand for efficient food preparation solutions.

Distribution Channel Insights

Offline retail channels continue to dominate microwave oven sales, accounting for approximately 68% of global revenue. Consumers frequently prefer physical inspection of appliances before making purchase decisions, particularly for larger and premium models. Electronics retailers, appliance specialty stores, and hypermarkets remain key distribution channels. However, online retail continues to gain momentum due to increasing internet penetration, improved logistics infrastructure, and growing consumer confidence in e-commerce platforms. Direct-to-consumer sales through manufacturer websites are also increasing as brands seek stronger customer engagement and higher profit margins.

Explore more data points, trends and opportunities Download Free Sample Report

Microwave Ovens Market Segmentations

By Product Type

- Solo Microwave Ovens

- Grill Microwave Ovens

- Convection Microwave Ovens

- Combination Steam-Microwave Ovens

- Air Fryer Integrated Microwave Ovens

By Installation Type

- Countertop Microwave Ovens

- Built-in Microwave Ovens

- Over-the-Range Microwave Ovens

- Drawer Microwave Ovens

By Capacity

- Below 20 Liters

- 20–25 Liters

- 25–30 Liters

- Above 30 Liters

By Technology

- Conventional Magnetron Technology

- Inverter Technology

- Smart Connected Microwave Ovens

- AI-Enabled Microwave Ovens

By End User

- Residential

- Restaurants & Quick Service Restaurants

- Hotels & Hospitality

- Healthcare Facilities

- Corporate & Institutional Foodservice

- Convenience Stores

Regional Insights

Asia-Pacific

Asia-Pacific represents the largest regional market, accounting for approximately 41% of global microwave oven revenue in 2025, driven by a powerful combination of manufacturing dominance and rapidly expanding consumer demand. China remains the global production and consumption hub, supported by large-scale appliance manufacturing clusters, strong domestic supply chains, and continuous product innovation from leading brands. Japan and South Korea maintain mature markets with exceptionally high penetration rates and strong demand for premium, technologically advanced microwave ovens featuring inverter technology and smart connectivity. India is emerging as one of the fastest-growing markets globally, fueled by rapid urbanization, rising disposable incomes, expansion of nuclear families, and increasing adoption of compact kitchen appliances in urban housing developments. Southeast Asian economies, including Indonesia, Vietnam, Thailand, and the Philippines, are also witnessing strong growth due to rising middle-class populations and expanding retail distribution networks.

North America

North America accounts for approximately 28% of global market revenue, with the United States contributing nearly 24% of global demand. The region is characterized by high household penetration rates, strong replacement cycles, and a mature consumer base that increasingly favors premium and feature-rich microwave ovens. Consumers are shifting toward smart kitchen ecosystems, integrating microwave ovens with voice assistants, IoT platforms, and energy-efficient inverter technologies. Canada continues to show stable growth driven by residential remodeling and kitchen modernization trends, while Mexico benefits from rising domestic consumption and its growing role as a manufacturing base supporting exports to the U.S. market.

Europe

Europe accounts for approximately 22% of global microwave oven revenue, with Germany, the United Kingdom, France, Italy, and Spain representing the leading markets. The region is highly influenced by architectural trends favoring modular and built-in kitchen designs, which is significantly boosting demand for integrated microwave ovens. Strict energy-efficiency regulations and sustainability mandates across the European Union are encouraging consumers to replace older appliances with advanced, low-energy models. Premiumization is a key trend, with strong demand for smart and multifunctional microwave ovens across urban households.

Latin America

Latin America represents approximately 4% of global microwave oven demand, with Brazil, Mexico, Argentina, Chile, and Colombia leading regional consumption. Growth in the region is supported by rapid urbanization, expanding middle-class populations, and improving access to modern retail and e-commerce channels. Mexico plays a dual role as both a major consumer market and a strategic manufacturing hub supplying appliances to North America. Brazil remains the largest domestic market, driven by increasing urban household formation and rising demand for affordable kitchen appliances.

Middle East & Africa

The Middle East and Africa account for approximately 5% of global microwave oven demand, with key markets including Saudi Arabia, the United Arab Emirates, South Africa, Egypt, and Nigeria. The region is experiencing steady growth driven by urbanization, infrastructure development, and rising adoption of modern kitchen appliances. Gulf countries, in particular, are witnessing strong demand for premium and smart-home-enabled microwave ovens due to high disposable incomes and rapid expansion of luxury residential developments. In Africa, increasing retail modernization and improving electricity access are gradually supporting appliance penetration.

Key Players in the Microwave Ovens Market

- Panasonic Holdings Corporation

- Midea Group

- LG Electronics

- Samsung Electronics

- Whirlpool Corporation

- Sharp Corporation

- Haier Group

- Toshiba Corporation

- Electrolux AB

- BSH Home Appliances

- GE Appliances

- Breville Group

- Miele

- Smeg

- Alto-Shaam