Microcontroller (MCU) Market Size

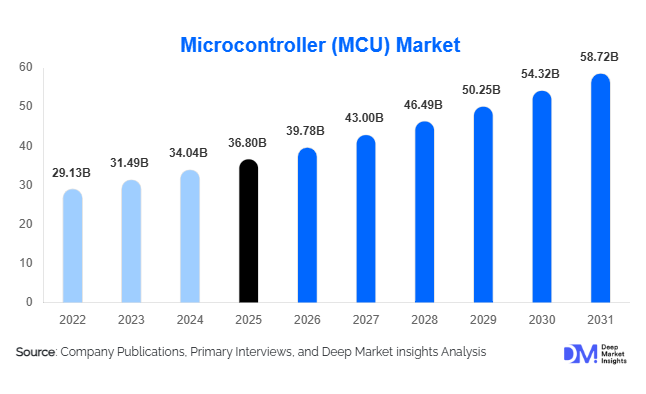

According to Deep Market Insights, the global microcontroller (MCU) market size was valued at USD 36.8 billion in 2025 and is projected to grow from USD 39.78 billion in 2026 to reach USD 58.72 billion by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The microcontroller market growth is primarily driven by the rising integration of embedded electronics across automotive systems, industrial automation, consumer electronics, healthcare devices, and IoT-enabled infrastructure. Increasing deployment of electric vehicles (EVs), Industry 4.0 technologies, smart home ecosystems, and edge AI computing is accelerating demand for advanced, low-power, and high-performance microcontrollers globally.

Key Market Insights

- 32-bit microcontrollers dominate the global MCU industry, supported by rising adoption in automotive electronics, industrial robotics, and intelligent edge computing applications.

- Automotive electronics remain the largest application segment, driven by EV production, battery management systems, ADAS deployment, and software-defined vehicle architectures.

- Asia-Pacific leads the global MCU market, accounting for the majority of electronics manufacturing, semiconductor packaging, and automotive production demand.

- Wireless-enabled and AI-integrated MCUs are the fastest-growing product categories, fueled by increasing IoT device penetration and smart consumer ecosystems.

- Industrial automation and Industry 4.0 investments are significantly increasing demand for secure, real-time, and energy-efficient microcontrollers across factories and smart infrastructure.

- Government semiconductor localization initiatives, including the U.S. CHIPS Act, “Made in China 2025,” and “Make in India,” are accelerating fab investments and strengthening domestic MCU supply chains.

Microcontroller (MCU) Market Trends

AI-Enabled Edge Microcontrollers Gaining Momentum

Manufacturers are increasingly integrating artificial intelligence and machine learning capabilities into microcontrollers to support edge computing applications. AI-enabled MCUs can process data locally without relying heavily on cloud infrastructure, enabling faster decision-making, lower latency, improved energy efficiency, and enhanced data privacy. This trend is particularly important in automotive systems, industrial robotics, smart cameras, healthcare monitoring devices, and intelligent consumer electronics. Semiconductor companies are launching MCUs with dedicated neural processing capabilities, embedded accelerators, and enhanced memory architectures to support predictive analytics and real-time processing. Edge AI adoption is expected to become one of the strongest long-term growth drivers within the global MCU ecosystem.

Rising Adoption of Ultra-Low-Power MCUs

Energy-efficient microcontrollers are witnessing significant adoption due to growing demand for battery-operated devices such as wearables, smart sensors, medical monitoring systems, and industrial IoT equipment. Ultra-low-power MCUs help extend battery life while maintaining processing performance and wireless connectivity. This trend is accelerating as sustainability regulations and energy-efficiency standards become stricter across electronics manufacturing industries. MCU suppliers are increasingly focusing on advanced sleep modes, energy harvesting support, and low-leakage semiconductor architectures. Growing smart home adoption, remote healthcare systems, and portable electronics usage are further reinforcing the market shift toward low-power embedded processing solutions.

Microcontroller (MCU) Market Drivers

Rapid Expansion of Electric Vehicles

The accelerating global transition toward electric mobility is a major driver for the MCU market. Electric vehicles contain significantly higher semiconductor content compared to conventional vehicles, requiring multiple microcontrollers for battery management, motor control, thermal regulation, infotainment, charging systems, and safety functions. Advanced driver assistance systems (ADAS), autonomous driving technologies, and connected vehicle platforms are further increasing the number of MCUs integrated into modern automobiles. Governments across Europe, China, and North America are supporting EV adoption through subsidies, emission reduction mandates, and charging infrastructure investments, creating sustained long-term demand for automotive-grade MCUs.

Industrial Automation and Industry 4.0 Growth

The increasing adoption of industrial automation technologies is significantly supporting MCU demand worldwide. Factories are integrating robotics, industrial IoT systems, programmable logic controllers, predictive maintenance platforms, and smart manufacturing infrastructure to improve operational efficiency and productivity. Microcontrollers play a central role in enabling real-time control, machine communication, and sensor data processing within industrial environments. The rise of Industry 4.0 initiatives across China, Germany, Japan, South Korea, and the United States is driving substantial investments in embedded processing technologies. Demand for reliable, secure, and low-latency MCUs is expected to remain strong across industrial sectors during the forecast period.

Microcontroller (MCU) Market Restraints

Semiconductor Supply Chain Volatility

The MCU market continues to face challenges associated with semiconductor supply chain disruptions, wafer shortages, geopolitical tensions, and fabrication capacity constraints. Automotive and industrial manufacturers remain vulnerable to prolonged lead times and procurement uncertainty due to limited mature-node semiconductor production capacity. Trade restrictions and export controls affecting semiconductor technologies are also increasing supply chain risks for global electronics manufacturers. These factors can create pricing instability and delay production schedules across end-use industries.

Pricing Pressure and Market Commoditization

The microcontroller industry is highly competitive, with intense pricing pressure among global semiconductor suppliers. Rapid commoditization of standard MCU products has reduced average selling prices, particularly within consumer electronics and low-cost IoT applications. Smaller manufacturers often face challenges maintaining profitability due to rising R&D costs, advanced packaging investments, and the need to continuously integrate new connectivity and security capabilities. This pricing environment creates barriers for emerging players attempting to compete against established semiconductor leaders with large-scale manufacturing advantages.

Microcontroller (MCU) Market Opportunities

Growth of Smart Infrastructure and IoT Ecosystems

The rapid expansion of IoT-connected infrastructure presents significant opportunities for MCU manufacturers globally. Smart cities, intelligent transportation systems, connected utilities, and smart energy management platforms increasingly depend on wireless-enabled microcontrollers capable of secure and real-time data processing. Governments and private enterprises are investing heavily in digital infrastructure modernization, creating long-term demand for low-power and connectivity-rich MCUs. Applications such as smart meters, intelligent lighting systems, surveillance equipment, and environmental monitoring platforms are expected to become major growth areas over the next decade.

Expansion of Healthcare Electronics and Remote Monitoring

The increasing adoption of connected healthcare devices and remote patient monitoring systems is creating substantial growth opportunities within the MCU market. Portable diagnostics, wearable health trackers, implantable devices, and telemedicine platforms require compact, ultra-low-power microcontrollers with secure wireless communication capabilities. Aging populations, healthcare digitization, and rising investments in preventive healthcare technologies are accelerating demand for intelligent medical electronics globally. MCU suppliers focusing on medical-grade reliability, power optimization, and embedded security are expected to benefit significantly from this expanding healthcare electronics ecosystem.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 36.8 Billion |

| Market Size in 2026 | USD 39.78 Billion |

| Market Size in 2031 | USD 58.72 Billion |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Bit Architecture Insights

32-bit microcontrollers dominate the global MCU market, accounting for approximately 48% of total revenue in 2025. These MCUs are widely adopted across automotive electronics, industrial automation, aerospace systems, and advanced IoT applications due to their superior processing power, memory handling capabilities, and support for complex software architectures. Growing deployment of edge AI, autonomous systems, and industrial robotics continues to strengthen demand for 32-bit architectures globally. Meanwhile, 8-bit and 16-bit MCUs remain important in low-cost embedded systems and consumer appliances where power efficiency and cost optimization remain critical factors.

Connectivity Type Insights

Wireless-enabled MCUs represent one of the fastest-growing product categories in the market, supported by increasing demand for smart home devices, wearable electronics, industrial IoT systems, and connected healthcare equipment. Wi-Fi, Bluetooth Low Energy (BLE), Zigbee, LoRa, and cellular IoT-enabled microcontrollers are becoming increasingly common in modern embedded systems. Wireless MCUs accounted for nearly 37% of overall market demand in 2025 and are expected to gain further share as global IoT deployment accelerates. The integration of secure connectivity protocols and low-power wireless communication capabilities remains a major focus area among semiconductor manufacturers.

Application Insights

Automotive electronics remain the leading application segment within the global MCU market, contributing nearly 29% of total market revenue in 2025. Modern vehicles require hundreds of microcontrollers for applications including ADAS, infotainment systems, battery management, powertrain control, body electronics, and advanced safety functions. Electric vehicle production growth and rising semiconductor content per vehicle continue to support strong MCU demand globally. Industrial automation applications are also witnessing rapid expansion as manufacturers invest in robotics, factory automation, predictive maintenance systems, and machine control infrastructure.

Power Consumption Insights

Ultra-low-power MCUs are experiencing strong growth due to increasing demand for battery-powered embedded devices. These MCUs are widely used in wearables, portable medical devices, environmental sensors, smart meters, and remote IoT monitoring systems where extended battery life is essential. Semiconductor manufacturers are focusing on advanced low-leakage semiconductor technologies, sleep mode optimization, and energy-efficient processing architectures to improve performance while reducing energy consumption. Rising adoption of portable electronics and wireless sensor networks continues to strengthen this segment globally.

End-Use Industry Insights

The automotive industry remains the largest end-use sector for microcontrollers globally due to rapid electrification and increasing integration of advanced electronic systems within vehicles. Industrial manufacturing represents another major growth sector as Industry 4.0 adoption expands across global factories. Consumer electronics continues to contribute substantially to MCU demand through smart appliances, gaming systems, wearables, and connected home devices. Healthcare applications are also emerging as a high-growth opportunity due to increasing deployment of connected diagnostics, patient monitoring systems, and portable medical electronics. Telecom infrastructure, energy management systems, and aerospace electronics further contribute to diversified long-term MCU demand.

Explore more data points, trends and opportunities Download Free Sample Report

Microcontroller (MCU) Market Segmentations

By Bit Architecture

- 4-bit Microcontrollers

- 8-bit Microcontrollers

- 16-bit Microcontrollers

- 32-bit Microcontrollers

- 64-bit Microcontrollers

By Connectivity Type

- Wired Connectivity MCUs

- Wireless Connectivity MCUs

- Wi-Fi MCUs

- Bluetooth/BLE MCUs

- Zigbee MCUs

- Cellular IoT MCUs

By Application

- Automotive Electronics

- Consumer Electronics

- Industrial Automation

- Healthcare & Medical Devices

- Smart Energy & Utilities

- Aerospace & Defense

- Telecommunications

By Power Consumption

- Ultra-Low Power MCUs

- Low Power MCUs

- Standard Power MCUs

- High-Performance MCUs

By End-Use Industry

- Automotive Industry

- Industrial Manufacturing

- Consumer Electronics Industry

- Healthcare Industry

- Energy & Utilities

- Aerospace & Defense

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global MCU market, accounting for nearly 52% of total revenue in 2025. China remains the largest regional market due to its leadership in electronics manufacturing, electric vehicle production, industrial automation deployment, and semiconductor consumption. Japan and South Korea continue to play critical roles in automotive electronics, industrial robotics, and advanced semiconductor manufacturing. Taiwan remains a major semiconductor fabrication and packaging hub supporting global MCU supply chains. India is emerging as one of the fastest-growing MCU markets globally, driven by electronics manufacturing expansion, automotive production growth, smart metering projects, and semiconductor localization initiatives under “Make in India.”

North America

North America accounted for approximately 21% of the global MCU market in 2025, supported primarily by strong demand from automotive, aerospace, industrial automation, and healthcare electronics industries. The United States leads regional demand due to significant investments in electric vehicles, semiconductor reshoring, AI-enabled embedded systems, and industrial digitalization. The implementation of the U.S. CHIPS Act is accelerating semiconductor fabrication investments and improving domestic supply chain resilience. Canada also contributes to regional demand through automotive manufacturing and industrial automation adoption.

Europe

Europe held nearly 18% of the global MCU market in 2025, supported by strong automotive manufacturing and industrial automation ecosystems. Germany remains the largest regional market due to its leadership in automotive engineering, industrial robotics, and factory automation technologies. France, Italy, and the United Kingdom are also witnessing rising demand for MCUs across aerospace, renewable energy, and healthcare applications. Europe’s aggressive EV adoption policies and sustainability regulations continue to accelerate demand for advanced automotive-grade microcontrollers.

Latin America

Latin America is gradually expanding within the MCU market, led primarily by Brazil and Mexico. Mexico benefits from strong automotive manufacturing integration with North American supply chains, while Brazil continues increasing investments in industrial automation and consumer electronics production. Demand for low-cost embedded electronics and connected industrial systems is supporting gradual regional growth.

Middle East & Africa

The Middle East & Africa region remains comparatively smaller but is witnessing growing demand for MCUs across smart infrastructure, industrial automation, energy management, and telecommunications applications. Countries such as the UAE and Saudi Arabia are investing heavily in smart city infrastructure and digital transformation initiatives, creating opportunities for embedded semiconductor deployment. Growing utility modernization and industrial diversification projects are expected to support long-term regional MCU demand.

Key Players in the Microcontroller (MCU) Market

- Renesas Electronics

- NXP Semiconductors

- Infineon Technologies

- STMicroelectronics

- Microchip Technology

- Texas Instruments

- Silicon Laboratories

- Analog Devices

- Qualcomm

- Espressif Systems