Laptop Market Size

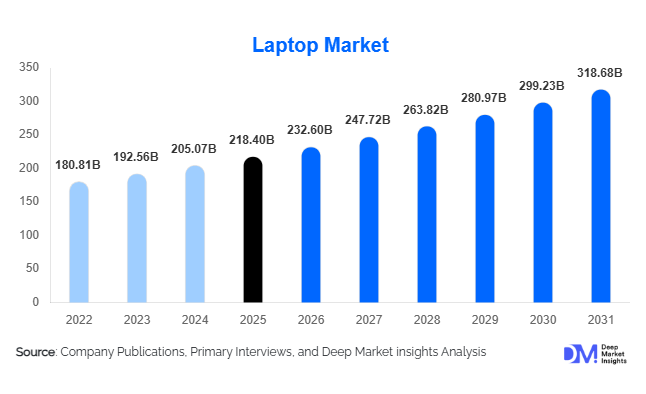

According to Deep Market Insights, the global laptop market size was valued at USD 218.4 billion in 2025 and is projected to grow from USD 232.60 billion in 2026 to reach USD 318.68 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The laptop market growth is primarily driven by accelerating enterprise digitalization, increasing adoption of hybrid work models, rising demand for AI-enabled personal computing devices, and continued investments in digital education infrastructure. Growing consumer preference for portable computing solutions, combined with advancements in processor technology, battery performance, and cloud-based productivity applications, continues to support market expansion across both developed and emerging economies.

Key Market Insights

- AI-enabled PCs are emerging as the next major upgrade cycle, driving replacement demand across enterprise and premium consumer segments.

- Hybrid work and remote collaboration models continue to fuel laptop adoption, particularly among corporate users requiring mobile productivity solutions.

- Asia-Pacific dominates the global laptop market, accounting for more than 40% of global revenues, supported by strong manufacturing capabilities and rising domestic demand.

- India is among the fastest-growing laptop markets globally, benefiting from digital education initiatives, expanding internet penetration, and government-led manufacturing programs.

- Gaming and creator-focused laptops are outperforming traditional consumer categories, supported by growing esports participation and content creation activities.

- ARM-based computing platforms and AI processors are reshaping product innovation, improving power efficiency, battery life, and local AI processing capabilities.

Laptop Market Trends

AI-Powered Computing Becoming Mainstream

The laptop industry is undergoing a significant transformation as manufacturers increasingly integrate dedicated AI processing capabilities into devices. New generations of processors from Intel, AMD, Qualcomm, and Apple incorporate neural processing units capable of handling AI workloads locally without relying entirely on cloud infrastructure. AI-powered features such as real-time translation, intelligent video conferencing, content generation, cybersecurity monitoring, and predictive system optimization are becoming standard offerings. Enterprise customers are actively evaluating AI-capable laptops as part of broader workplace productivity strategies, while consumers increasingly expect AI-enhanced user experiences. This transition is expected to drive a major replacement cycle over the coming years and contribute to higher average selling prices across premium laptop categories.

Premiumization and High-Performance Mobility

Consumer preferences are shifting toward premium devices that offer superior portability, longer battery life, enhanced displays, and higher performance. Ultrabooks, gaming laptops, creator-focused notebooks, and mobile workstations are experiencing strong growth as users increasingly demand desktop-level performance in portable form factors. OLED displays, advanced cooling systems, high-refresh-rate screens, and lightweight chassis designs are becoming key differentiators. Manufacturers are also focusing on sustainable materials, modular designs, and extended device lifecycles to align with evolving customer expectations. The growing popularity of hybrid work, remote learning, and digital content creation continues to reinforce demand for premium mobile computing solutions.

Laptop Market Drivers

Expansion of Hybrid Work Environments

Hybrid work has fundamentally reshaped enterprise IT procurement strategies worldwide. Organizations increasingly require secure, portable, and high-performance computing devices that enable employees to work seamlessly across office, home, and remote locations. Laptops have become the primary productivity platform for knowledge workers, driving continuous replacement demand across large enterprises, government agencies, and small businesses. Investments in cloud collaboration platforms, virtual desktop infrastructure, and cybersecurity solutions further support laptop adoption. As organizations continue optimizing workforce flexibility, demand for business-class notebooks is expected to remain robust throughout the forecast period.

Growth of Digital Education and Online Learning

Governments and educational institutions worldwide continue investing heavily in digital learning infrastructure. One-device-per-student initiatives, online learning programs, and digital classrooms have significantly increased laptop penetration among students and educators. Emerging economies are particularly active in expanding educational technology access, creating substantial demand for entry-level and mid-range notebooks. In addition, universities increasingly require students to own personal computing devices capable of supporting specialized software applications, further strengthening long-term market demand.

Laptop Market Restraints

Component Cost Volatility and Supply Chain Risks

The laptop market remains vulnerable to fluctuations in semiconductor, memory, storage, and display component pricing. Increases in DRAM and NAND flash memory prices directly affect manufacturing costs and reduce pricing flexibility for original equipment manufacturers. Geopolitical tensions, trade restrictions, and supply chain disruptions can further impact component availability and production schedules. These factors may create temporary shortages and increase average device prices, potentially slowing adoption among price-sensitive customer segments.

Market Saturation in Mature Economies

Many developed markets, including North America, Western Europe, Japan, and South Korea, have already achieved high levels of laptop penetration. As a result, growth in these regions is increasingly dependent on replacement purchases rather than first-time adoption. Longer product lifecycles, improved hardware durability, and economic uncertainty can delay replacement decisions among both consumers and enterprises. Manufacturers must therefore rely on technological innovation and premium product differentiation to stimulate demand within mature markets.

Laptop Market Opportunities

Enterprise AI-PC Upgrade Cycle

The emergence of AI-enabled personal computers represents one of the largest growth opportunities in the laptop market. Enterprises are increasingly exploring AI-driven productivity applications that require advanced processing capabilities and local AI inference. As organizations modernize workplace technology infrastructure, demand for AI-capable laptops is expected to accelerate significantly. Vendors offering integrated AI software ecosystems, enterprise security solutions, and device management capabilities will be well-positioned to capture future growth opportunities.

Expansion Across Emerging Economies

Rapid digitalization across emerging markets presents substantial opportunities for laptop manufacturers. Countries such as India, Indonesia, Vietnam, Brazil, Nigeria, and Mexico continue experiencing growth in internet access, digital services adoption, and middle-class purchasing power. Government initiatives supporting digital literacy, online education, and domestic electronics manufacturing further contribute to market expansion. Affordable notebook offerings tailored to local requirements can help manufacturers capture significant untapped demand in these high-growth regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 218.4 Billion |

| Market Size in 2026 | USD 232.60 Billion |

| Market Size in 2031 | USD 318.68 Billion |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Traditional clamshell laptops remain the dominant product category, accounting for approximately 57% of global laptop revenues in 2025. Their leadership is supported by broad applicability across consumer, educational, and enterprise environments. Ultrabooks continue gaining popularity among professionals seeking lightweight and highly portable devices, while gaming laptops represent one of the fastest-growing categories due to increasing participation in esports and digital entertainment. Mobile workstations are experiencing strong adoption among engineering, design, and content creation professionals who require high-performance computing capabilities. Convertible and detachable 2-in-1 laptops are also gaining traction as organizations seek greater flexibility between tablet and notebook functionality.

Application Insights

Business productivity applications remain the largest contributor to laptop demand globally, supported by enterprise digital transformation initiatives and growing reliance on cloud-based software solutions. Personal computing continues to represent a substantial portion of demand, particularly for entertainment, education, and communication purposes. Gaming applications are experiencing above-average growth due to expanding esports ecosystems and increasing consumer spending on premium hardware. Content creation, software development, engineering design, and AI model development are emerging as high-value application segments requiring advanced computing performance. The rise of edge AI computing is further creating new opportunities for laptops capable of handling local AI workloads efficiently.

Distribution Channel Insights

Online sales channels account for a growing share of global laptop purchases, representing approximately 36% of market revenues. Consumers increasingly prefer e-commerce platforms due to wider product selection, competitive pricing, and convenient purchasing experiences. Direct-to-consumer sales through manufacturer websites are also expanding as brands strengthen digital engagement strategies. Traditional electronics retailers remain important for product demonstrations and customer support, particularly in emerging markets. Enterprise procurement channels continue to dominate commercial sales, with system integrators and managed service providers playing an increasingly important role in large-scale deployment projects.

End-User Insights

The consumer segment accounts for approximately 45% of global laptop revenues, supported by demand for personal computing, entertainment, education, and remote work applications. Enterprise customers represent the largest commercial segment and continue investing in workforce mobility solutions, cybersecurity infrastructure, and AI-enabled computing devices. Educational institutions remain a major source of demand, particularly in emerging economies implementing digital learning initiatives. Government agencies increasingly deploy laptops to support e-governance, public administration, and digital service delivery. Industrial, defense, and field operations applications continue generating demand for ruggedized and specialized computing systems designed for harsh operating environments.

Price Band Insights

The mid-range laptop segment, priced between USD 500 and USD 1,000, dominates the global market with approximately 38% revenue share. This category balances affordability and performance, making it attractive to consumers, students, and small businesses. Premium laptops priced between USD 1,000 and USD 2,000 continue gaining share due to increasing demand for high-performance devices and AI-enabled computing capabilities. Entry-level notebooks remain important in emerging markets, while ultra-premium devices above USD 2,000 are benefiting from strong demand among gamers, creators, and professional users requiring advanced performance features.

Explore more data points, trends and opportunities Download Free Sample Report

Laptop Market Segmentations

By Product Type

- Traditional Clamshell Laptops

- Ultrabooks

- 2-in-1 Convertible Laptops

- Detachable 2-in-1 Laptops

- Gaming Laptops

- Mobile Workstations

- Rugged Laptops

- Chromebooks

By Application

- Personal Computing

- Business Productivity

- Content Creation & Design

- Software Development

- Gaming & Esports

- Scientific Computing

- AI Development & Edge AI Applications

By End User

- Consumer

- Enterprise/Commercial

- Education

- Government & Public Sector

- Industrial & Field Operations

- Defense & Aerospace

By Distribution Channel

- Online Direct-to-Consumer

- Brand-Owned Stores

- Multi-Brand Electronics Retail

- Enterprise/System Integrator Sales

- Institutional Procurement

By Operating System

- Windows

- macOS

- ChromeOS

- Linux

- Other Operating Systems

Regional Insights

North America

North America accounted for approximately 28% of global laptop market revenues in 2025, led primarily by the United States. Enterprise refresh cycles, AI-PC adoption, and strong consumer spending continue driving regional demand. The United States represents nearly 24% of global laptop revenues, supported by high average selling prices and strong penetration across both enterprise and consumer segments. Canada contributes steadily through educational and government procurement programs, while increasing adoption of AI-enabled devices is expected to sustain long-term market growth.

Europe

Europe represents approximately 22% of global laptop revenues, with Germany, the United Kingdom, France, Italy, and Spain serving as major demand centers. Enterprise modernization initiatives, sustainability regulations, and growing digital transformation investments continue driving notebook adoption. Demand for energy-efficient devices and premium business-class laptops remains particularly strong among European enterprises. The region also benefits from well-established educational technology programs and increasing investments in hybrid workplace infrastructure.

Asia-Pacific

Asia-Pacific dominates the global laptop market with approximately 41% market share. China remains both the largest consumer market and manufacturing hub, supported by extensive electronics supply chains and domestic demand. India is among the fastest-growing markets globally, benefiting from digital education initiatives, rising disposable incomes, and domestic electronics manufacturing incentives. Japan and South Korea continue generating strong demand for premium devices, while Southeast Asian markets such as Indonesia and Vietnam are emerging as important growth engines due to increasing digital adoption and expanding middle-class populations.

Latin America

Latin America accounts for approximately 5% of global laptop revenues, with Brazil and Mexico representing the largest markets. Educational technology investments, growing SME adoption, and expanding internet connectivity are supporting demand across the region. Government-led digital inclusion programs continue creating opportunities for affordable notebook deployments, while growing entrepreneurial activity is contributing to commercial laptop adoption.

Middle East & Africa

The Middle East and Africa region accounts for approximately 4% of global laptop revenues and represents an emerging growth opportunity. Saudi Arabia and the United Arab Emirates are investing heavily in digital transformation initiatives and smart city programs, driving demand for enterprise-grade computing solutions. South Africa, Egypt, Nigeria, and Kenya continue expanding digital education and workforce development programs, supporting steady notebook adoption. Increasing internet penetration and government digitization initiatives are expected to accelerate growth across the region during the forecast period.